Charitable donations of securities

Gifting shares instead of cash may enhance your tax benefit. To encourage charitable giving, the government provides you with a tax credit when you make a personal donation to a registered charity. This article discusses a further potential tax benefit if you donate certain securities in-kind.

Gifting shares instead of cash may enhance your tax benefit. To encourage charitable giving, the government provides you with a tax credit when you make a personal donation to a registered charity. This article discusses a further potential tax benefit if you donate certain securities in-kind.

Family Office Services

October 14, 2025

Charitable donations of securities

Gifting shares instead of cash may enhance your tax benefit

To encourage charitable giving, the government provides you with a tax credit when you make a personal donation to a registered charity. You can use this donation tax credit to reduce your taxes payable. This article discusses a further potential tax benefit if you donate certain securities in-kind.

Please note the strategies discussed in this article pertain only to individuals who are donating securities held on account of capital. Holding a security on account of capital means that if you were to sell the security, you'd realize a capital gain or loss. If you'd realize income or losses from the sale of a security, you're holding that security on account of income. If you're uncertain which pertains to your situation, it's important to seek advice from your qualified tax advisor. Further, if you report gains on the sale of securities on account of income, it's important to seek advice from your qualified tax advisor as to a donation strategy that makes sense for you.

Gifting certain types of securities

Generally, when you gift property, the property is deemed to have been disposed of at fair market value (FMV). As such, you may realize taxable capital gains if the property has increased in value since you first acquired it. The capital gains triggered when donating securities may be eliminated in some cases if you donate the securities in-kind.

In order to qualify for the elimination of capital gains, the donated securities can be:

- Shares, debt obligations or rights listed on a designated stock exchange;

- Mutual funds;

- Interests in related segregated fund trusts; or

- Government of Canada or provincial government bonds.

In addition, you must make a donation to a qualified donee. Qualified donees are generally organizations that can issue official donation tax receipts for the gifts they receive. They can be charitable organizations, public foundations or private foundations. Typically, a registered charity is a qualified donee. In this article, the terms qualified donees and registered charities are used interchangeably.

The Canada Revenue Agency (CRA) maintains a list of qualified donees. When you're ready to make a donation, you may want to check the list to determine if a particular charity is currently registered and can issue official donation tax receipts.

Before making a donation in-kind, it's important to contact the qualified donee and verify that they can accept in-kind donations.

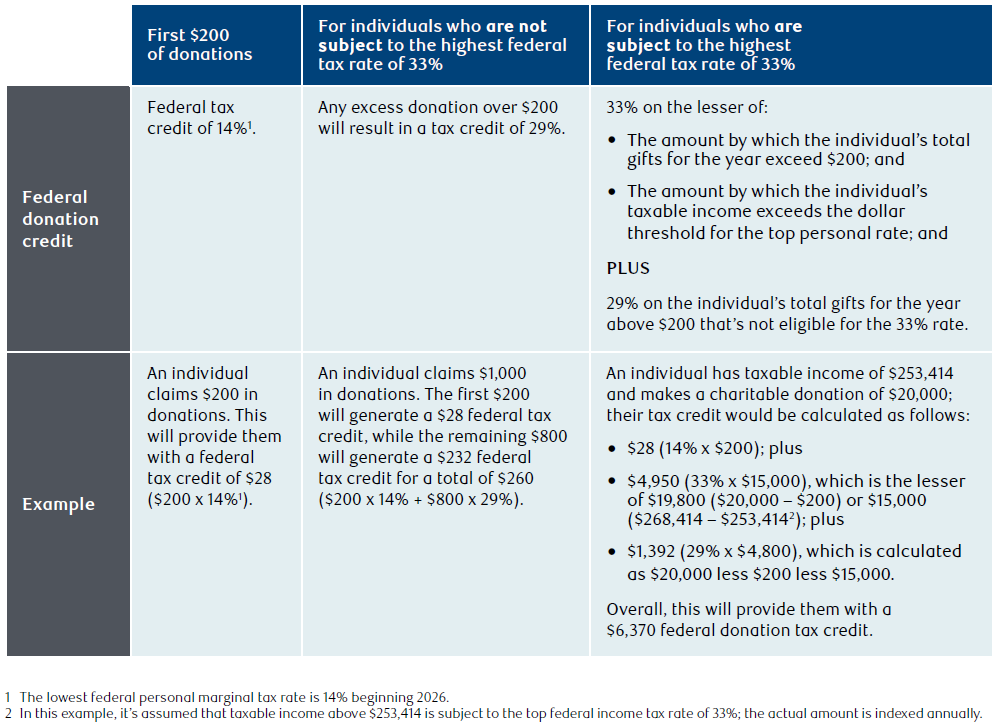

Mechanics of a donation tax credit

When you make a donation to a registered charity, you may claim a tax credit on your personal tax return. The donation tax credit reduces your federal and provincial/territorial income taxes in the year you make the donation.

The donation tax credit is non-refundable, which means the tax credit can't reduce the amount of your tax below zero. Federally, the tax credits that may be available to you depending on your taxable income may be available to you depending on your taxable income. The following table illustrates how you calculate your donation tax credit.

In addition to the federal tax credit illustrated in this table, you may also receive a provincial/territorial donation tax credit. The amount of the credit will vary depending on your place of residence. If you currently live in a province that has a surtax (Ontario has a surtax), the donation tax credit will reduce your taxes payable, which will reduce your surtax payable.

Donation timing and carry-forward

You're not required to claim the donation tax credit in the year you make the donation. Instead, you may carry it forward for up to five years (or 10 years for a gift of certified ecologically sensitive land). This gives you flexibility with regards to claiming your donations. For instance, it may make sense to save all of your donation receipts for a higher-income year in order to maximize the credit you receive at the higher federal rate. Alternatively, if you make small annual donations, you may claim the combined donations to utilize the higher credit for gifts above $200 in a future year. You can't carry back donations to a previous tax year.

Limit on donation amount

There's no limit to the amount you can donate in a year. However, for tax purposes, you can generally only claim a charitable donation of up to 75% of your net income in a taxation year. If you're a resident of Quebec, the limit is 100% of your net taxable income for Quebec tax purposes. This limit is also 100% of your net income in the year of death and the preceding year.

For example, assume Jane's net income for the year is $100,000 and she's a resident of Alberta. She received a large inheritance in the same year and decides to make a donation of $200,000 to her favourite charity. Jane will only be able to claim a maximum of $75,000 (75% x $100,000) of donations for tax purposes this year. Jane can carry forward the remainder for a maximum of five years.

Combining the elimination of capital gains with donation tax credit

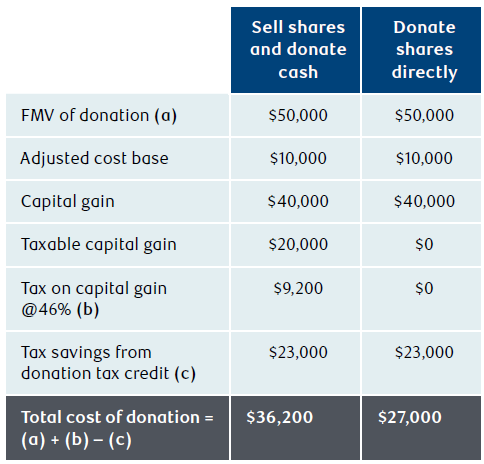

When you donate securities in-kind, you may benefit from the elimination of the capital gain accrued on the securities plus the donation tax credit. As such, it may cost you less to make a donation of securities than a donation of cash. The following example illustrates this point by comparing two alternatives for donating shares of a publicly traded company with a FMV of $50,000 and an adjusted cost base (ACB) of $10,000 to a registered charity. The donor's combined federal and provincial marginal tax rate is 46% and the donor is also entitled to a combined federal and provincial donation tax credit at a rate of 46%.

In this example, the donor realizes savings of $9,200 ($36,200 – $27,000) by donating appreciated property instead of selling it and donating the proceeds. The difference is a result of the eliminated capital gains tax on the donated securities.

Donate some securities to eliminate tax on sale of securities

If you sell securities with an accrued capital gain, you may trigger a tax liability. As an alternative to selling the securities, you may want to consider donating the securities to eliminate the taxable capital gain. If you plan to use some of the sale proceeds to fund lifestyle expenses or make reinvestments, you may only want to donate a portion of the securities you're planning to dispose of and sell the remainder.

You may be able to use the donation tax credit on the portion of the securities you donate to eliminate the tax liability on the capital gain triggered on the disposition of the remaining portion (i.e. portion not donated). Ask your RBC advisor about a tool that can help you estimate the portion of securities you need to donate to eliminate the tax on the securities you sell.

Valuation of donated securities

When you make a donation in-kind, the charity needs to determine the FMV of the gift in order to issue a donation receipt. For a donation of publicly traded shares, the CRA accepts the closing bid price of the share on the date the charity receives the shares as the FMV of the shares. It will also accept the midpoint between the high and the low trading prices for the day if that's a better indicator of FMV on normal and active market trading. You may want to contact the charity to understand their method of valuation for your gift.

Alternative minimum tax (AMT)

If you're making a donation to reduce your tax liability, it's very important to consider AMT. This tax aims to ensure that every Canadian individual pays a minimum amount of tax. The calculation of AMT is based on an adjusted taxable income, which seeks to remove some of the advantages of certain tax-preferential items such as the donation tax credit or the elimination of capital gains on the donation of publicly traded securities. If the AMT calculated is greater than your regular tax liability, the AMT becomes your tax liability for the year. The difference between the AMT you have to pay in a year and your regular tax liability can be carried forward for seven years to reduce your future regular income tax liability when your taxes payable exceed your AMT.

For more information about AMT and charitable giving, ask your RBC advisor for an article on that topic. Be sure to speak with a qualified tax advisor to help you determine how AMT may affect your charitable giving.

Donating securities in-kind at death

When an individual passes away, the individual is generally deemed to have disposed of their capital property immediately before death. If the deceased owned securities discussed earlier in this article and these securities were donated in-kind by the deceased's estate, the capital gain accrued on these securities may be eliminated. The capital gain may be eliminated if the donation is made within 60 months of the individual's death and the estate is a graduated rate estate (GRE) or was a GRE that continues to meet the other requirements of a GRE, other than the 36-month time period.

Generally, a GRE of an individual is an estate that arose on and as a consequence of the individual's death for the first 36 months after death. To be considered a GRE, the estate also needs to remain a testamentary trust and be designated for its first taxation year as the deceased individual's GRE. For more information regarding donation of securities on death, ask your RBC advisor for an article on income taxes at death.

Donating depreciated securities in-kind

Donating appreciated securities is attractive for tax purposes, as you can eliminate the capital gain. However, in some cases, donating depreciated securities may also make sense. Year-end tax planning often involves tax loss selling and charitable giving as two strategies that may be used to reduce your tax bill. Combining the two strategies is possible, as an in-kind donation of depreciated securities will trigger a capital loss for tax purposes and result in a donation tax credit equal to the FMV of the security donated. The capital loss triggered is not eliminated; it's applied first against any capital gains realized in the same year. Any remaining net capital losses can then be carried back and applied against capital gains from the previous three years, or they can be carried forward and applied against capital gains realized in a future year. You should be mindful of the "superficial loss" rules if you're planning to repurchase the same security. For more information on the superficial loss rules, please ask your RBC advisor for the article on that topic.

Gifting other types of securities

The following sections discuss the donation of other types of securities.

Donating flow-through investments

In 2011, the federal government introduced rules to limit what they saw as excessive tax benefits that resulted from the elimination of the taxable capital gains on the donation of flow-through investments. Generally, these rules tax the portion of any capital gain realized on the sale of the flow-through securities up to the original cost of the investment. As a result, a deemed capital gain may be triggered when flow-through investments are donated. These rules apply to donations of a "flow-through share class of property" made on or after March 22, 2011.

However, these rules do not apply to flow-through common shares acquired before March 22, 2011, or mutual fund corporation shares that are received in exchange for flow-through limited partnership units acquired before August 16, 2011 (no contributions to the partnership can be made on or after August 16, 2011). For more information on donating flow-through investments, please ask your RBC advisor for an article on that topic.

Donating shares acquired through employee stock options

You may benefit from favourable tax treatment when donating shares acquired through exercising employee stock options to a qualified donee. When you exercise your stock options, you receive a taxable employment benefit which is equal to the difference between the FMV of the shares on the day of exercise and the option exercise price. If you exercise employee stock options and donate the acquired shares to a qualified donee, part or all of the employment benefit may be eliminated. For more information, ask your RBC advisor for an article on donating shares acquired from employee stock options.

Donating exchangeable shares

As a result of a reorganization of shares or a sale of shares to a foreign acquirer, you may have acquired exchangeable securities in order to allow you to defer the capital gains on the disposition of your securities. These exchangeable shares are generally not publicly traded but they may be exchanged for publicly traded securities. When you exchange your exchangeable shares for publicly traded shares, a deemed disposition will occur and a capital gain or loss will be triggered. The capital gain triggered on the conversion will be eliminated if the converted publicly traded securities are gifted to a registered charity within 30 days of the exchange. Another requirement is that, at the time the unlisted security is issued, it must be exchangeable for the publicly traded security and the publicly traded security must be the only consideration received on exchange.

Donating registered assets versus non-registered securities in-kind

You may donate the assets in your registered account, such as your RRSP/RRIF to a qualified donee during your lifetime or upon death. However, the assets in your registered account will not benefit from the zero capital gains inclusion treatment, as the value of the securities in your registered plan is considered income on your tax return, not a capital gain. If you withdraw securities from your RRSP/RRIF, the amount you withdraw is taxable to you as income. You could choose to donate the securities after withdrawing them from your RRSP/RRIF, which allows you to benefit from the donation tax credit.

Given there's no special exemption on the donation of registered assets, if you have a registered account and a non-registered account, you may want to consider making an in-kind donation of securities with accrued capital gains rather than donating your registered assets.

Conclusion

Making charitable donations provides individuals with a chance to give back to their community and receive tax incentives at the same time. When you donate certain securities, such as publicly traded shares, in addition to getting a donation tax receipt for the FMV of the securities donated, any capital gains you've accrued on the donated securities may also be eliminated. If you plan on making a donation, review your portfolio to determine if there are any securities with large capital gains. Speak with a qualified tax advisor to determine whether it makes sense for you to donate securities with accrued capital gains.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.