Charitable Donations Through Your Corporation

Being an incorporated business owner, you may want to make a charitable donation through your corporation. To encourage charitable giving, the government provides a corporation with a tax deduction when the corporation makes a donation to a registered charity. The deduction reduces the corporation's taxable income, which in turn reduces the corporation's taxes. In addition, if a private corporation makes a donation of publicly traded securities, there may be an additional tax incentive.

Being an incorporated business owner, you may want to make a charitable donation through your corporation. To encourage charitable giving, the government provides a corporation with a tax deduction when the corporation makes a donation to a registered charity. The deduction reduces the corporation's taxable income, which in turn reduces the corporation's taxes. In addition, if a private corporation makes a donation of publicly traded securities, there may be an additional tax incentive.

Family Office Services

June 14, 2025

Charitable Donations Through Your Corporation

Being an incorporated business owner, you may want to make a charitable donation through your corporation. To encourage charitable giving, the government provides a corporation with a tax deduction when the corporation makes a donation to a registered charity. The deduction reduces the corporation's taxable income, which in turn reduces the corporation's taxes. In addition, if a private corporation makes a donation of publicly traded securities, there may be an additional tax incentive. This article provides an overview of how your private corporation can qualify for the donation tax deduction and the tax benefits of donating publicly traded securities in-kind.

Qualifying Donations

To qualify for the donation tax deduction, your corporation must make a donation to a qualified donee. Qualified donees are generally organizations that can issue official donation receipts for the gifts they receive. They can be charitable organizations, public foundations or private foundations. Typically, a registered charity is a qualified donee. In this article, the terms qualified donees and registered charities are used interchangeably.

The Canada Revenue Agency (CRA) maintains a list of qualified donees on their website. When your corporation is ready to make a donation, you may wish to check the list to determine if a particular charity is currently registered and can issue official donation receipts.

The CRA considers a gift to be a voluntary transfer of money or property for which you expect and receive no consideration. You can make these gifts in cash or in-kind if the qualified donee accepts non-cash gifts.

Donation receipts are issued for the eligible amount of a gift made to a qualified donee; this is generally the fair market value (FMV) of the donation. In certain instances, an advantage may be deemed to be received, which reduces the amount of the eligible donation. An advantage is generally the total value of any property, service, compensation, use or any other benefit you're entitled to as a partial consideration for, or in gratitude for, the gift. An example of this would be if your corporation purchased a table for a charity benefit and it cost $500. The value of the food and party is considered an advantage with a value of $250; therefore, the eligible donation amount would be $250 ($500 less the $250 advantage amount).

Corporate Donation Tax Deduction

A corporation is entitled to a tax deduction for the donation amount against their taxable income. By reducing taxable income, the corporation reduces their tax liability. A corporation does not need to claim the full donation in a particular year. Donations can be carried forward for up to five years. Generally, a corporation can claim a deduction for charitable donations up to 75% of the corporation's net income for the year.

Generally, if your corporation is a Canadian-controlled private corporation (CCPC), and it earns both active business income that's eligible for the small business tax rate and passive investment income, the donation deduction reduces the CCPC's taxable income subject to the small business tax rate rather than the investment income.

Gifting Publicly Traded Securities

If your corporation wishes to make a cash donation but doesn't have the cash on hand, it may have to sell some securities to raise the cash. If the FMV of the securities being sold exceeds its adjusted cost base (ACB), it will trigger a capital gain in the corporation. A percentage of the capital gain is included in computing the corporation's income and taxable to the corporation. The non-taxable portion is added to the corporation's capital dividend account (CDA). Once the corporation receives the cash proceeds from the sale, it may donate the cash to a qualified donee and deduct the amount donated from its taxable income.

A corporation can also donate certain types of securities directly to qualified donee. This can be an effective donation strategy if the corporation has securities with large accrued capital gains. The corporation can deduct the full FMV of the securities donated to a qualified donee against its taxable income, reducing overall taxes payable. In addition, the capital gain on the securities donated to a qualified donee may be eliminated and the full value of the capital gain is added to the corporation's CDA. This increases the amount that can be paid tax-free to the corporation's shareholders.

Types of Securities Eligible for Elimination of Capital Gains

To qualify for the elimination of capital gains, the donated securities can be:

- Shares, debt obligations or rights listed on a designated stock exchange;

- Mutual funds;

- Interests in related segregated funds; or

- Government of Canada or provincial government bonds.

Before making a donation of securities, it's important to contact the qualified donee and verify that they can accept in-kind donations.

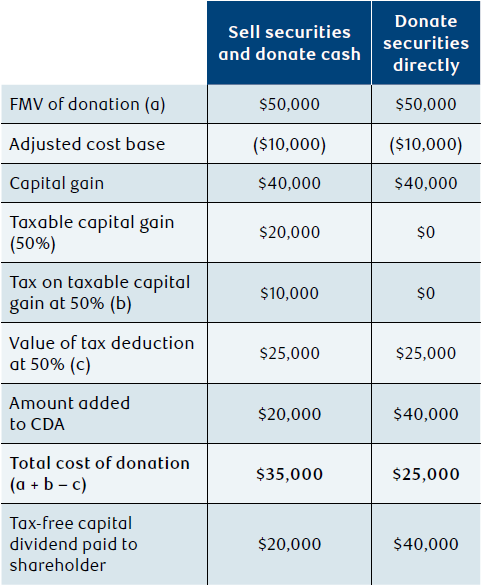

Corporate Donation Example

Let's compare the tax result of a corporation selling securities and donating the proceeds versus donating the securities directly. The following example assumes a corporation is holding securities that it wishes to donate with a FMV of $50,000 and an ACB of $10,000. The corporation earns only investment income, which is subject to a combined federal and provincial tax rate of 50%. The corporation has sufficient net income to utilize the full tax deduction.

As the example illustrates, donating securities directly to the charity results in additional tax savings of $10,000 to the corporation due to the elimination of the tax on the capital gain. In addition, you, the shareholder, can receive a larger amount of tax-free capital dividends from the corporation.

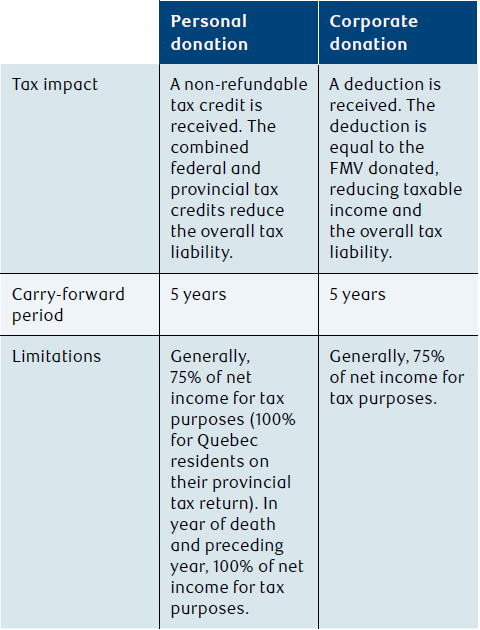

Donating Personally or Through a Corporation

As mentioned, when a corporation makes a donation, it's entitled to a tax deduction against its taxable income. In contrast, when you make a donation personally, you're entitled to claim a tax credit. This tax credit is an amount that reduces your taxes owing.

Comparison of Personal and Corporate Donations

For more information on the tax impact of personal donations, please ask your RBC advisor for the article titled "Charitable donations."

If you intend to make a cash donation and have cash in both your personal and corporate accounts, there's generally not a significant tax difference between donating personally or through your corporation. This is because if you're at or near the highest marginal tax bracket, the personal donation tax credit on donations above $200 has approximately the same value as the corporate donation tax deduction plus the personal tax savings from not having to first withdraw the funds from the corporation before making a personal donation.

If you intend to donate publicly traded securities with accrued gains, it's generally preferrable, from a tax perspective, to donate the securities with the largest accrued capital gains because you want to maximize the benefit of eliminating the capital gains accrued on your holdings. However, if you have surplus assets in your corporation that you with to withdraw, you may want to consider first donating the securities with accrued gains in your corporation and then withdrawing the funds. This is because by donating securities directly from your corporation, your corporation can receive the elimination of the capital gain, the donation tax deduction as well as the addition to the CDA which provides you with the ability to withdraw assets from your corporation on a tax-free basis.

Establishing a Charitable Foundation

If you're thinking about leaving a legacy and wondering about the ways to do so for yourself and your family, you may wish to consider establishing your own private foundation. Alternatively, you can choose to make an irrevocable donation using the RBC Charitable Gift Program. Through the RBC Charitable Gift Program, you can establish a charitable gift fund with a customized name. You or your corporation can donate cash or other assets to the gift fund, which is administered by the Charitable Gift Funds Canada Foundation, a registered public foundation. The foundation will make grants to the charity, or charities, of your choice in the name of your fund. You can still take advantage of the eliminated capital gains, in addition to leaving a legacy, by donating publicly traded shares held in your corporation to your own charitable gift fund. For more information on the RBC Charitable Gift Program, speak with your RBC advisor.

Conclusion

Corporate charitable donations provide shareholders a chance to support their community and receive tax incentives at the same time. By donating appreciated publicly traded securities through your private corporation, you may be able to receive three tax benefits: eliminating capital gains tax on the securities donated, getting a tax deduction for the fair market value of the securities donated, and increasing the CDA balance which allows you to withdraw funds from your corporation as tax-free dividends. Speak to a qualified tax advisor to see if donating through your corporation makes sense in your circumstances.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.