Comparing saving options

There are a number of tax-efficient options for Canadians when it comes to saving for the future. For those who don't have enough excess cash to maximize all of the forms of saving available to them, the question regularly becomes: Where do I save first or should I pay down my debt instead? This article examines some of the considerations you may want to think about when deciding between allocating money towards a registered retirement savings plan (RRSP) or a tax-free savings account (TFSA) or paying down debt.

There are a number of tax-efficient options for Canadians when it comes to saving for the future. For those who don't have enough excess cash to maximize all of the forms of saving available to them, the question regularly becomes: Where do I save first or should I pay down my debt instead? This article examines some of the considerations you may want to think about when deciding between allocating money towards a registered retirement savings plan (RRSP) or a tax-free savings account (TFSA) or paying down debt.

Family Office Services

April 14, 2024

Comparing saving options

RRSP, TFSA or paying down debt

There are a number of tax-efficient options for Canadians when it comes to saving for the future. For those who don't have enough excess cash to maximize all of the forms of saving available to them, the question regularly becomes: Where do I save first or should I pay down my debt instead? This article examines some of the considerations you may want to think about when deciding between allocating money towards a registered retirement savings plan (RRSP) or a tax-free savings account (TFSA) or paying down debt.

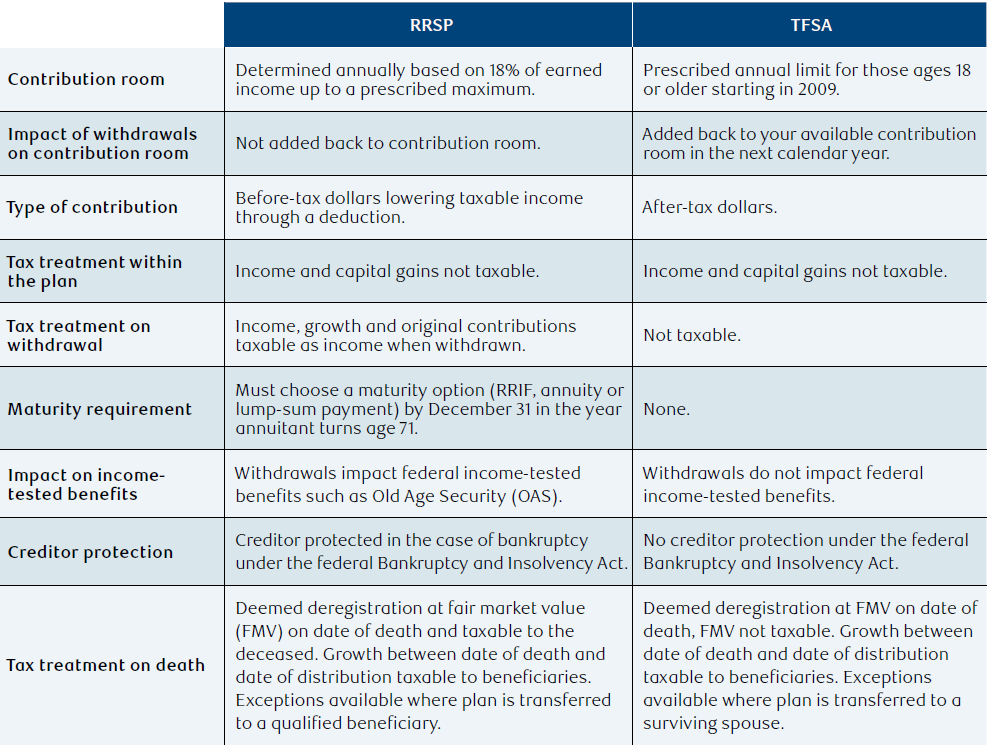

RRSP and TFSA basics

RRSPs and TFSA are registered accounts created by the government to encourage saving. The table below summarizes some of the key attributes of these accounts to give you a starting point for the comparison. If you'd like more information, please ask your RBC advisor for additional articles on each of these accounts.

Evaluating your options

When examining your saving choices, it's important to note there is no single or absolute answer. Instead, there are many considerations that may make a particular savings vehicle more suitable for you.

The following sections outline some typical considerations you may want to take into account, which include:

- Interest rates and rates of return on investments;

- Risk tolerance;

- Marginal tax rates;

- Flexibility;

- Personal habits; and

- Income-tested retirement benefits.

In making a decision about where to save, give some thought to your personal goals and objectives to determine the best savings vehicle for you. Questions to consider could include, what are these savings for and when will you need them? Do you want to minimize tax today or smooth tax over your lifetime? Where do your priorities lie? Once you've determined your goals and objectives, you can look at which considerations are the most important to you. For example, if you need funds in the short-term (e.g. for vacation), investing in a TFSA may make sense, as it provides you with the flexibility to withdraw funds with minimal tax consequences.

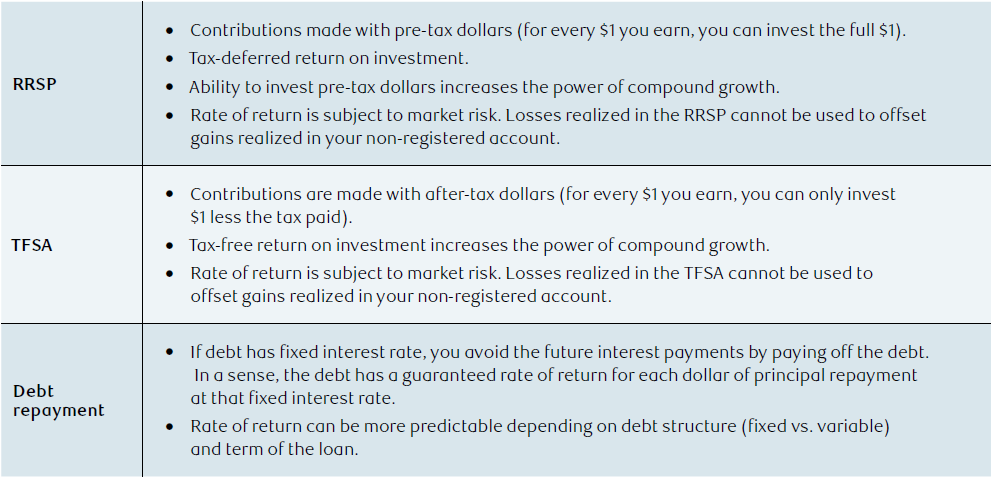

Interest rates and rates of return on investments

Once you've determined the potential rate of return on your RRSP/TFSA, you can compare the rate of return to the interest you'll be saving on the early debt repayment. For example, if you have locked in a very low interest rate on your debt and expect market returns to be higher, it may be more beneficial for you to invest rather than paying down that debt.

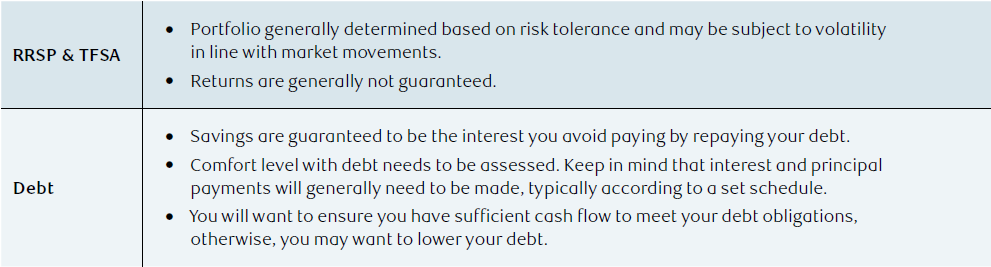

Risk tolerance

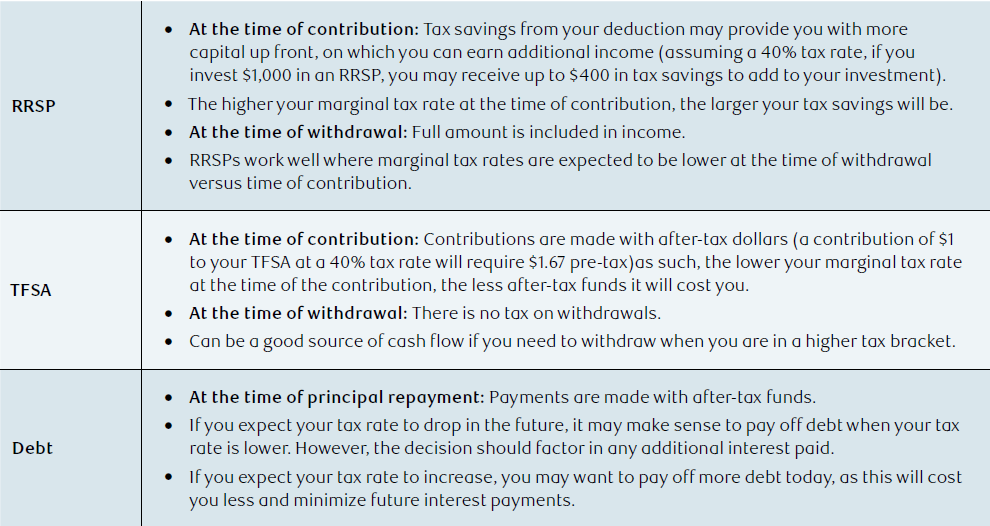

Marginal tax rates

Flexibility

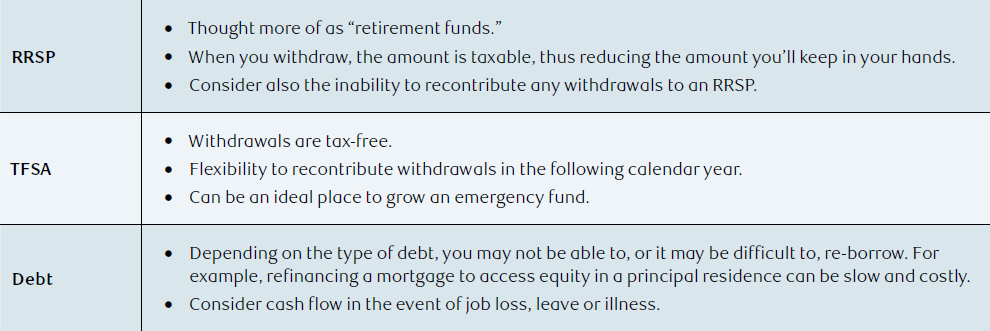

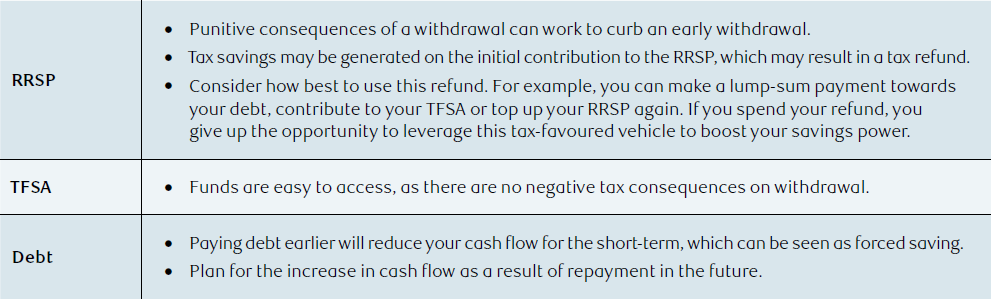

Personal habits – know yourself

Income-tested retirement benefits

Other considerations

Time horizon: How long you plan to invest for should be considered when determining your saving strategy. As an example, RRSPs are generally better-suited for long-term savings, whereas TFSA, debt repayment and non-registered investments may be better solutions for short-term. This is because withdrawals from an RRSP are fully taxable while the initial contribution is tax-deductible. As such, you'll generally want to keep the pre-tax dollars invested in the RRSP for as long as possible.

Employer matching: Does your employer match TFSA or RRSP contributions? If so, to the extent your excess cash provides, it may make sense to contribute to one or both savings vehicles up to the maximum employer match. This allows you to increase your annual compensation, by getting more from your employer that would not otherwise be available. You'll also be able to grow these plans more quickly, as your contribution will be topped up by your employer.

Home Buyers' Plan/Lifelong Learning Plan: While the RRSP isn't as flexible as the TFSA, there are two unique programs for the RRSP. They are the ability to access $35,000 for a home under the Home Buyers' Plan or withdrawing up to $20,000 for qualifying post-secondary education under the Lifelong Learning Plan. If you're interested in learning more, please ask your RBC advisor for additional articles on these specific programs.

Debt terms: Not all debt is created equally. Some lenders will set limits on the quantum and means of prepaying a debt, specifically with mortgages. Typically, accelerated monthly payments or annual lump-sum payments up to a pre-determined amount will be allowed, or some combination of the two. Before deciding on making any early repayments, make sure you understand the terms of the loan and determine if there are any additional fees associated with an early repayment if possible.

Conclusion

There's no one correct answer in deciding how to save. It's a personal decision that should be made based on your goals, circumstances, tax rates and personal habits. To help with the decision-making process, please speak with your RBC advisor, who can help you examine your options.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.