Family Office Services

August 14, 2024

Discount instruments

Reporting on your income tax return

Discount instruments don't pay regular coupon interest, don't have a stated interest rate, and the taxable interest isn't reported on a tax slip — therefore, you may wonder how to appropriately report the income associated with these investments on your income tax return.

Discount instruments are fixed-income investments, such as T-bills, strip bonds, strip coupons, banker's acceptance notes and commercial paper, that don't pay regular coupon interest.

This article addresses the tax implications for individuals only. It does not discuss tax implications for corporations, partnerships, unit trusts and trusts where any of these entities are beneficiaries.

Discount instruments held to maturity

A discount instrument held to maturity will appear in the "Discount Instruments" section of your year-end "Summary of Security Dispositions" statement. This statement also includes the sale of stocks and bonds during the year. It's for you, or your qualified tax advisor, to use to calculate your capital gains and losses on these investments.

However, a Canadian dollar discount instrument that's held to maturity does not create a capital gain or loss. The difference between the par value of maturity and the price paid to purchase the discount instrument is considered interest income for tax purposes. This means the difference between the price you paid for the discount instrument and the amount you receive at maturity is taxable to you as interest income.

Note that this interest income will not appear on a T5 slip. You will need to manually calculate this interest income on the maturity of the discount instrument and include it on your personal income tax return as interest income.

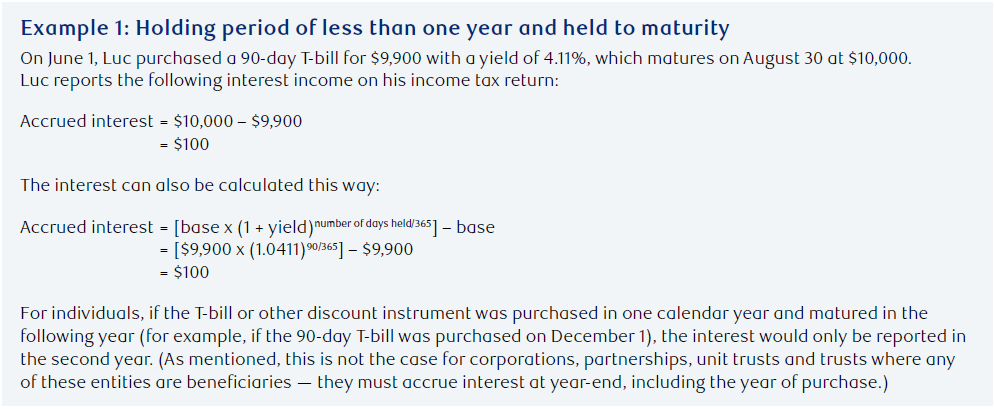

If you hold a discount instrument to maturity and it matures in one year or less, the interest income should be reported in the year of maturity.

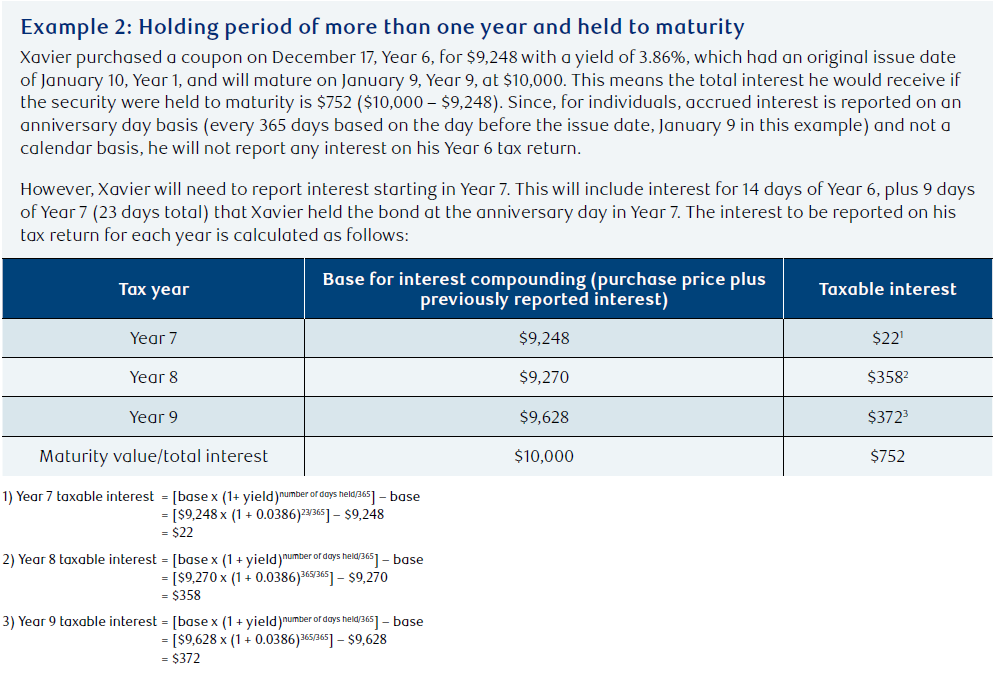

If the discount instrument matures later than one year, you'll need to report the accrued interest earned each year, except in the year acquired.

Accrued interest is the interest you earned in the year even if it's not paid in the year. The accrued interest is calculated every year on the "anniversary day" and is based on the yield-to-maturity rate, at the time of purchase. The anniversary day is one year less a day after the date of issue, and every successive year after that. For example, a bond issued on January 6, Year 1 would have an anniversary day of January 5; Year 2 and each year after that it would also be January 5. For individuals, no interest would need to be reported in the year the discount instrument is acquired, unless it's sold in the year (this is not the case for corporations, partnerships, unit trusts and trusts where any of these entities are beneficiaries — they must accrue interest at year-end, including the year of purchase.)

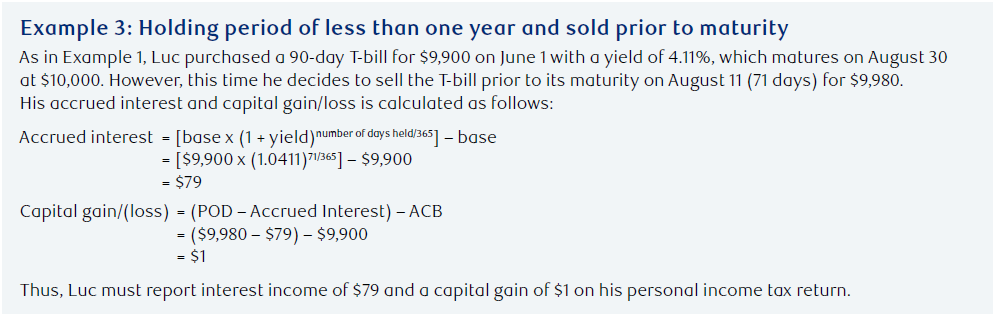

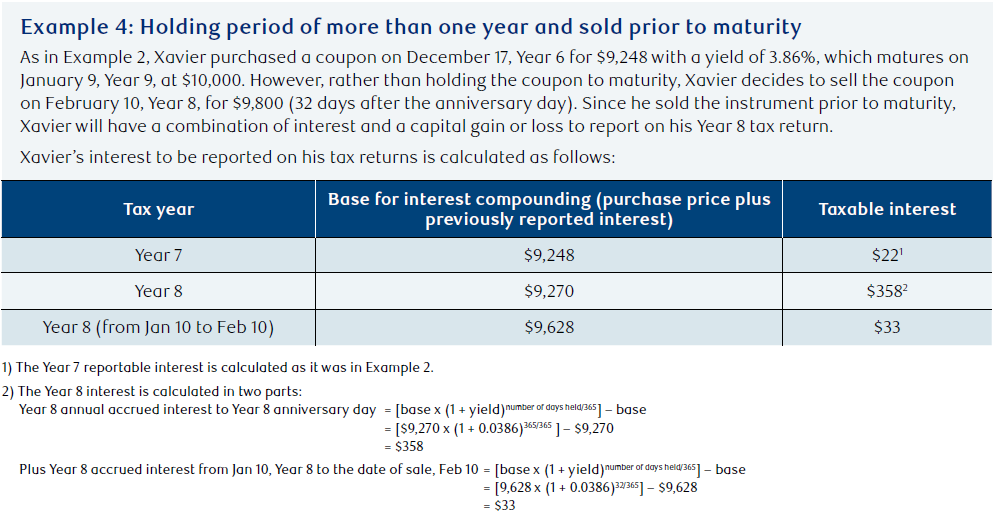

Selling a discount instrument prior to maturity

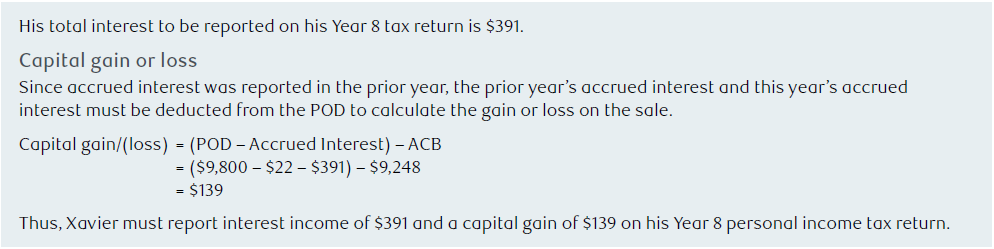

If you sell a discount instrument prior to maturity, there will generally be a combination of interest and a capital gain or loss realized for tax purposes. You (or your qualified tax advisor) must manually calculate this interest and capital gain or loss and report them on your tax return.

First, you need to calculate the accrued interest as noted in Example 1. To calculate the capital gain or loss, subtract the accrued interest from the proceeds of disposition (POD) and then subtract your adjusted cost base (ACB) as usual.

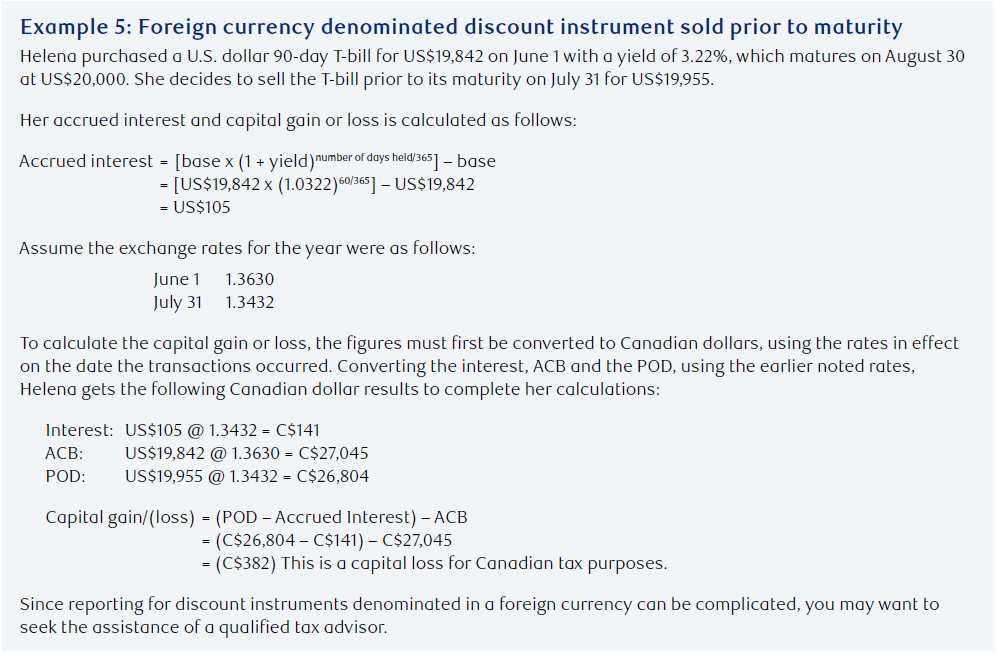

Foreign exchange

For individuals, all amounts you report on your Canadian tax return must be reported in Canadian dollars, regardless of the actual currency of the instrument. If the instrument is denominated in a foreign currency, the proper amount of interest must be determined in Canadian dollars using the appropriate foreign exchange rate.

First, interest is calculated in the foreign currency as previously described. The resulting interest must then be converted to Canadian dollars using an appropriate foreign exchange rate. There is flexibility in how the annual accrued interest is converted to Canadian dollars (e.g. foreign exchange rate on anniversary day or average exchange rate for the year), so you should consult with your professional tax advisor to determine the appropriate foreign exchange rate to use. However, the Canada Revenue Agency has commented that interest accrued up to the date of maturity or disposition should be converted using the "spot rate in effect on that date."

When dealing with a discount instrument denominated in a foreign currency, a capital gain or loss calculation must be done if the discount instrument is sold prior to maturity or if it matures at par. This is because there may be a foreign currency gain or loss at maturity, even if it matures at par. Generally, the appropriate exchange rates to use are the rates prevailing at the time of purchase and at the time of disposition.

Let's look at an example where a discount instrument, denominated in U.S. dollars, is purchased and sold before maturity.

Conclusion

If you hold a Canadian denominated discount instrument until maturity, the difference between the par value at maturity and the price you paid to purchase the instrument will be taxable to you as interest income.

If the discount instrument has a holding period of more than one year, you will need to report the accrued interest earned each year on the anniversary day using the effective interest rate.

If you sell a discount instrument prior to maturity, there may be a combination of interest and a capital gain or loss realized for tax purposes.

When discount instruments are denominated in a foreign currency, the interest and capital gain or loss must be reported on your Canadian income tax return in Canadian dollars.

Since reporting for discount instruments require you to manually calculate your interest and capital gain or loss, if any, you may want to seek the assistance of a qualified tax advisor.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that your action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.