Donating Flow-Through Investments

To encourage charitable giving, the government provides you with a tax credit when you make a donation to a registered charity. This donation tax credit can be used to reduce your taxes payable. In some cases, you may receive a further benefit if you donate flow-through investments. This article discusses the tax implications of donating flow-through investments in kind from your personal non-registered account.

To encourage charitable giving, the government provides you with a tax credit when you make a donation to a registered charity. This donation tax credit can be used to reduce your taxes payable. In some cases, you may receive a further benefit if you donate flow-through investments. This article discusses the tax implications of donating flow-through investments in kind from your personal non-registered account.

Family Office Services

August 14, 2024

Donating Flow-Through Investments

To encourage charitable giving, the government provides you with a tax credit when you make a donation to a registered charity. This donation tax credit can be used to reduce your taxes payable. In some cases, you may receive a further benefit if you donate flow-through investments. This article discusses the tax implications of donating flow-through investments in kind from your personal non-registered account.

Tax Benefits of Donating Flow-Through Investments

When you purchase a flow-through investment and subsequently donate the investment in-kind, you may benefit from the following:

- Deduction of exploration and development expenses flowed through to you against your taxable income.

- Applicable federal mineral exploration tax credit (METC), critical mineral exploration tax credit (CMETC), and applicable provincial/territorial flow-through share tax credits that reduce your taxes payable.

- Donation tax receipt for the fair market value (FMV) of the donated flow-through investment; and

- A portion of the capital gain realized on the donation of the investment may be eliminated.

Capital Gains on Donating Flow-Through Investments

Generally, when you gift property, the property is deemed to have been disposed of at FMV. As such, you may realize taxable capital gains if you donate property that has an adjusted cost base (ACB) that is lower than its FMV. If you donate the publicly traded securities in-kind, the capital gains realized may be eliminated.

The elimination of capital gains works differently for flow-through investments. Because the ACB of a flow-through investment is typically zero or close to zero, there would be a significant benefit if the capital gain could be eliminated on the donation of a flow-through investment.

In 2011, the federal government introduced rules to limit what they saw as excessive tax benefits. Under these rules, you may realize a deemed capital gain when you donate flow-through investments. The deemed capital gain is equal to the actual capital gain realized on the donation or your "exemption threshold," whichever is less. In very simplified terms, your exemption threshold is equal to the original cost of all flow-through shares of the same class, less any cumulative capital gains realized on the disposition of flow-through shares in the same class. This essentially means the exemption from capital gains tax will be available only to the extent that the actual capital gain on the donation of flow-through investments is in excess of your original cost amount.

Please note if you are a resident of Quebec, you may still be able to eliminate the entire capital gain when all the conditions are met for provincial tax purposes.

Grandfathering for Certain Flow-Through Investments

The deemed capital gains rules do not apply to flow-through common shares acquired before March 22, 2011, or shares of a mutual fund corporation that are received in exchange for flow-through limited partnership (LP) units acquired before August 16, 2011 (no contributions to the partnership can be made on or after August 16, 2011).

Generally, only the original cost of flow-through shares acquired on or after March 22, 2011, and flow-through LP units acquired on or after August 16, 2011, will be added to your exemption threshold. For example, if you only owned flow-through common shares purchased prior to March 22, 2011, your exemption threshold will remain at zero and you can donate the shares and benefit from the old rules (i.e. you will still be able to exclude your entire capital gain realized at the time of donation). Likewise, if you acquired flow-through LP units before August 16, 2011, once they are exchanged for shares of a mutual fund corporation, you can donate them and still benefit from the old rules.

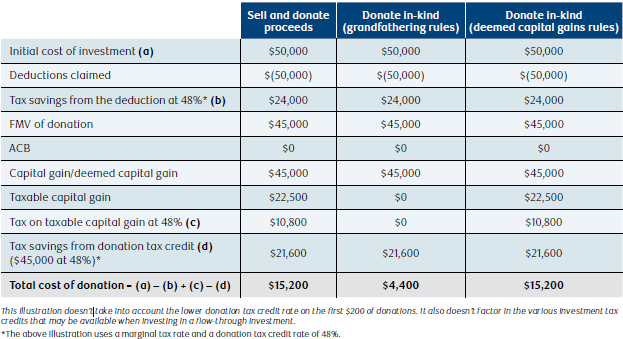

Example - Tax Impact of Donating a Flow-Through Investment

Here's an example to illustrate the impact of the deemed capital gains rules. Say you purchased 500 flow-through shares of XYZ Co. for an original cost of $50,000. Under the grandfathering rules, the taxable capital gain would later be zero.

Under the deemed capital gains rules, the exemption threshold is calculated as the original cost of $50,000.

The deemed capital gain is calculated as the lesser of:

a. The actual capital gain on the donation ($45,000); and

b. The exemption threshold ($50,000).

As a result, you realize a deemed capital gain of $45,000 on the donation.

The following table illustrates the tax implications of selling the capital shares versus donating the shares in-kind. In this example, we are assuming the capital gain realized on the shares is $45,000.

Alternative Minimum Tax (AMT)

If you're purchasing and donating a flow-through investment to reduce your tax liability, it's very important to consider AMT. This tax aims to ensure that every Canadian individual pays a minimum capital gain tax. The calculation of AMT is based on an adjusted taxable income, which seeks to remove the advantages of certain tax-preferential items such as deductions from flow-through investments. In addition, starting in 2024, only 50% of the donation tax credit can be used to reduce AMT. If any capital gains you realize on the donation of the flow-through investment is exempt under the regular tax calculation, you will need to calculate 30% of the exempt capital gains as income for AMT purposes. If the AMT calculated is greater than your regular tax liability, the AMT becomes your tax liability for the year. The difference between the AMT you have to pay in 2024 and your regular tax liability can be offset by a credit for seven years to reduce your future regular income tax liability when your taxes payable exceed your AMT. For more information about charitable giving and AMT, ask your RBC advisor for an article on this topic.

Be sure to speak with a qualified tax advisor to help you determine how AMT will affect you if you're thinking of donating flow-through investments.

Conclusion

Making charitable donations provides you with a chance to give back to your community and receive tax incentives at the same time. When you donate flow-through investments, in addition to getting a donation tax receipt for the FMV of the investment, some of the accrued capital gain on the investment may also be eliminated. Speak with a qualified tax advisor to determine whether it may make sense for you to donate flow-through investments in-kind.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your donation is treated properly and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.