Donation of publicly listed employee stock option shares

A strategy to eliminate tax on the exercise of your options and meet your philanthropic goals. As an employee, you may have been granted stock options by your employer. Once you've exercised the options, consider donating the shares acquired as a strategy to meet your philanthropic goals and realize tax savings.

A strategy to eliminate tax on the exercise of your options and meet your philanthropic goals. As an employee, you may have been granted stock options by your employer. Once you've exercised the options, consider donating the shares acquired as a strategy to meet your philanthropic goals and realize tax savings.

Family Office Services

October 14, 2025

Donation of Publicly Listed Employee Stock Option Shares

A strategy to eliminate tax on the exercise of your options and meet your philanthropic goals

As an employee, you may have been granted stock options by your employer. Generally, there are no tax implications when the stock options are first granted to you. However, when you decide to exercise the options, you will realize a security options benefit. Once you've exercised the options, consider donating the shares acquired as a strategy to meet your philanthropic goals and realize tax savings. This article discusses the tax benefits and considerations of donating publicly traded shares that you received from exercising your employee stock options.

Stock Option Taxation

Generally, when you decide to exercise your employee stock options to acquire publicly listed shares, you will realize a security options benefit. This benefit is equal to the difference between the fair market value (FMV) of the shares at the time you exercise the options and the amount you pay for the shares (the exercise price or strike price). The security options benefit is considered employment income and is taxable to you at your marginal tax rate. In some cases, this taxable income can be reduced by a security options deduction.

Security Options Deduction

If your options were granted before July 1, 2021 (or if you were granted certain qualifying options after June 2021 that replace options granted before July 2021), you may be eligible for an offsetting security options deduction equal to 50% of your security options benefit if certain conditions are met. For example, one of the conditions to be eligible for the security options deduction is if the exercise price was not less than the FMV of the shares at the time the options were granted. The deduction results in the security options benefit being effectively taxed at capital gains rates.

For options granted after June 30, 2021, a $200,000 limit applies on employee stock options that vest in a calendar year and qualify for the 50% security options deduction (the $200,000 limit). The $200,000 limit applies to employee stock options that are granted by mutual fund trusts and corporations that are not Canadian controlled private corporations (CCPCs), subject to certain exceptions. For the purpose of the $200,000 limit, the amount of employee stock options that vest in a calendar year and benefit from the security options deduction is determined based on the FMV of the underlying shares at the time the options are granted. For example, if the FMV of the underlying shares at the time of the grant is $100 and you were granted 3,000 options that vest in a particular year, you'll be able to claim the security options deduction on only 2,000 of the options ($200,000/$100 = 2,000).

If you exercise employee stock options granted after June 2021 that are in excess of the $200,000 limit, you will not be entitled to the security options deduction on the exercise of these options.

Note that for Quebec provincial tax, the security options deduction is generally only 25%. You may be eligible for a security options deduction of 50% on your Quebec return for stock options granted under an agreement concluded after February 21, 2017, provided certain conditions are met. A $200,000 annual limit for the security options deduction also applies in Quebec for options granted after June 30, 2021, by mutual fund trusts and corporations that are not CCPCs, subject to exceptions. For further details, please ask your RBC advisor for the article on the taxation of employee stock options.

Tax Benefits of Donating Stock Option Shares

There are two possible tax benefits you'll receive when donating your publicly listed stock option shares to a qualified donee. A qualified donee is an organization that can issue official donation receipts for gifts it receives. Examples of a qualified donee include registered charities such as a charitable organization, a public foundation and a private foundation. There are a number of other qualifying donees not mentioned here.

An Additional Deduction

You may receive an additional deduction if you donate your stock option shares that qualify for the security options deduction. In order to qualify for the additional deduction, you will need to donate the shares acquired on the exercise of your options in the same year you exercise the options and within 30 days of exercising the options. If you exercise your stock options in December, you will not have the full 30 days to make the donation, as you must donate the shares before December 31.

The amount of the additional deduction is equal to 50% of the lesser of two amounts:

(1) The security options benefit

(2) The FMV on the disposition, minus the exercise price

If the stock option shares have remained the same or increased in value at the time of making your donation, the additional deduction effectively eliminates your security options benefit. Alternatively, if the shares have declined in value at the time of making your donation, your additional deduction is reduced proportionately. In other words, your additional deduction will be less than 50% of your security options benefit.

If you live in Quebec, on your Quebec provincial income tax return, you may receive the additional deduction on top of your regular security options deduction.

It's important to note that you will not qualify for this additional deduction if you donate publicly listed stock option shares that were not eligible for the security options deduction under the rules that apply to options granted on or after July 1, 2021.

A Donation Tax Credit

In addition to eliminating or reducing your security options benefit, you will also receive a donation tax receipt equal to the FMV of the shares you donate. This allows you to claim a donation tax credit which can be used to reduce the taxes payable on your other sources of taxable income.

Cashless Exercises

If you have been granted employee stock options but do not have the cash needed to pay for the shares upon exercise of the options, you can consider a cashless exercise of your options. A cashless exercise involves short selling the underlying shares as a means of acquiring the cash needed to exercise the options. Generally, short selling is a speculative practice that involves using a broker to sell shares that you do not own.

Using some of the funds raised from the short sale, you exercise your stock options. The broker receives the shares from your employer and uses them to cover the short sale. The broker then pays you the difference between the cash received from the short sale and the cash used to exercise your stock options.

In a cashless exercise, if you direct the broker to immediately donate all or a portion of the proceeds to a qualified donee, you may still be eligible for a portion of the additional deduction. The deduction is prorated to reflect the proportion of the proceeds that you instruct the broker to donate and is determined by the following formula:

A x B/C

Where:

A is the amount of the additional deduction that would have been available if the shares were acquired and then donated within the time limit.

B is the amount donated to charity by the broker.

C is the total proceeds of disposition of the shares acquired via the option.

Check with your RBC advisor to determine if you meet the requirements to execute a cashless exercise.

An Example

Kate exercises options to acquire 200 shares of her corporate employer. These options were granted to her prior to July 1, 2021. The exercise price is $25 a share and the FMV at the time of exercise is $250 a share. She directs the broker, who is administering the stock option plan for her employer, to execute a cashless exercise and donate the net proceeds of $45,000 to a registered charity. (The amount donated of $45,000 is calculated as $50,000 proceeds from the sale of shares, less $5,000 paid to her employer to cover the exercise price.)

Kate has a security options benefit equal to $45,000 (i.e. the FMV of the shares at the time of acquisition, less the exercise price). Assume Kate is entitled to a security options deduction of $22,500 (50% of $45,000) since she meets all the relevant criteria. If she had donated the shares to a registered charity, she would have been entitled to an additional deduction of $22,500 (50% of $45,000). But since she donated 90% of the proceeds from the disposition of the shares, she is only entitled to an additional deduction of $20,250 ($22,500 x $45,000/$50,000).

Choosing the Method of Donation

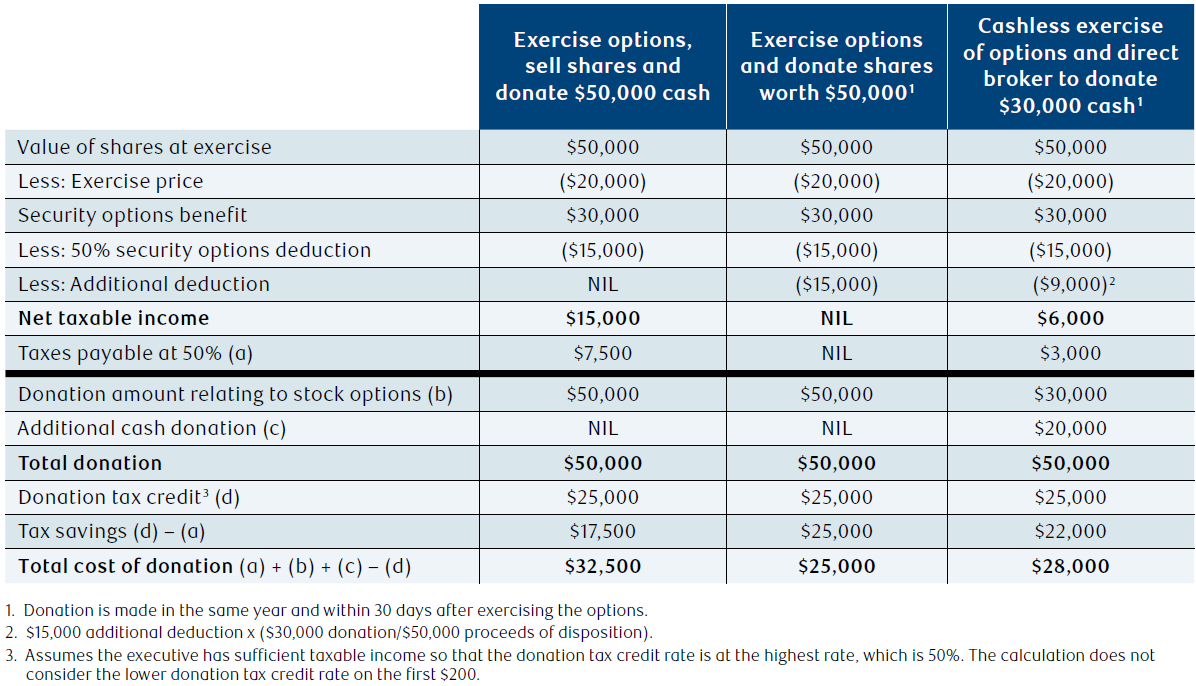

Example 1 – Options Granted Before July 1, 2021

Assume an executive has 1,000 options expiring next month. The exercise price is $20 a share and the current FMV is $50 a share. The executive and their spouse regularly make a cash donation at year-end of $50,000. If the executive chooses to use a cashless exercise, they will only be able to donate the net cash of $30,000. In this case, the executive and their spouse will make an additional cash donation of $20,000 by year-end to meet their annual donation goal. They are wondering if there is a more tax-efficient way to execute their charitable intentions.

The following illustration compares the tax implications of three different methods in which you can donate your employee stock option shares. The illustration assumes the executive is in the highest marginal tax bracket and taxed at a rate of 50%.

Based on this illustration, exercising options and donating the shares to a registered charity is the most tax-efficient option. The executive would save $7,500 ($32,500 – $25,000) by donating $50,000 of shares instead of $50,000 of cash due to the additional deduction. The executive would also save $3,000 ($28,000 – $25,000) by donating $50,000 of shares instead of choosing a cashless exercise and directing the broker to donate the net proceeds. This is because the additional deduction is prorated in the case of a cashless exercise. That said, if the executive does not have all the necessary funds to exercise their options, a cashless exercise may be better than having the options expire and not having any funds to donate.

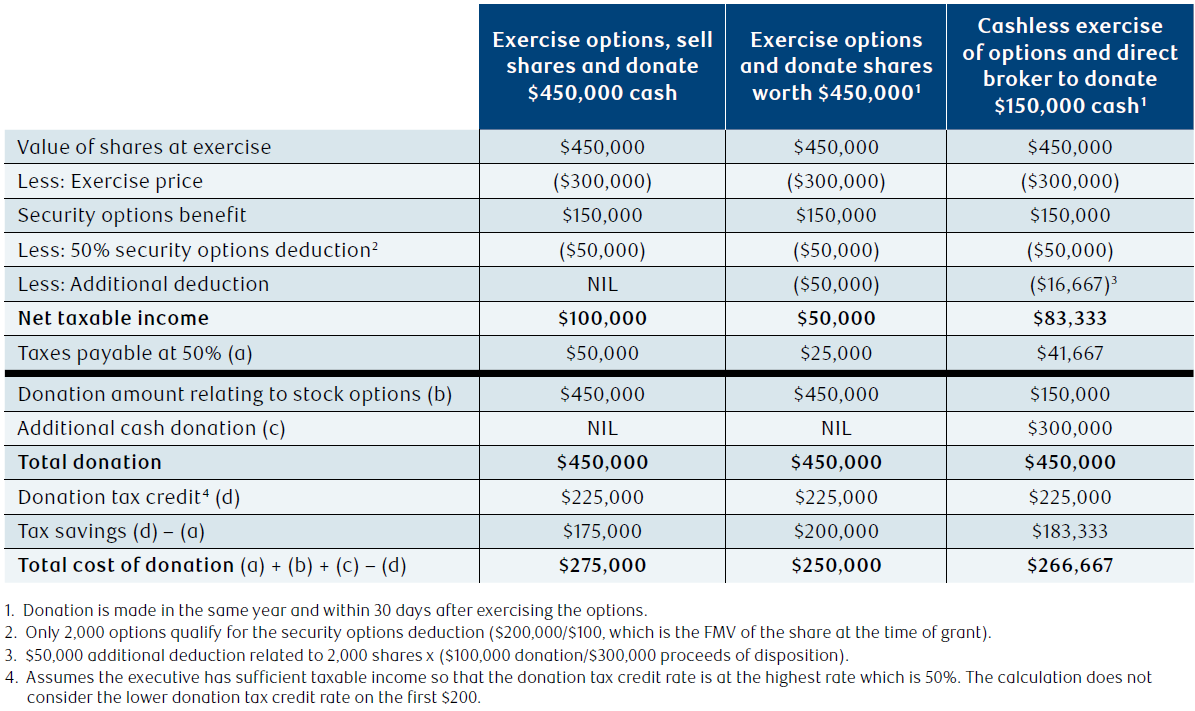

Example 2 – Options Granted After June 30, 2021

Assume an executive has 3,000 options that vest and expire in the same year. The exercise price is $100 per share. The FMV of the underlying share at the time of grant was $100 a share. The current FMV of a share is $150. The executive and their spouse regularly make a cash donation at year-end of $450,000. If the executive chooses to use a cashless exercise, they will only be able to donate the net cash of $150,000. In this case, the executive and their spouse will make an additional cash donation of $300,000 by year-end to meet their annual donation goal. They are wondering if there is a more tax-efficient way to execute their charitable intentions.

The following illustration compares the tax implications of three different methods in which you can donate your employee stock option shares. The illustration assumes the executive is in the highest marginal tax bracket and taxed at a rate of 50%.

Based on this illustration, exercising options and donating the shares to a registered charity is still the most tax-efficient option. Although under the rules that apply to stock options granted after June 30, 2021, you are not able to eliminate the entire tax liability on the exercise of the options by donating the shares, there are still savings to be had. The executive would save $25,000 ($275,000 – $250,000) by donating $450,000 of shares instead of $450,000 of cash due to the additional deduction. The executive would also save $16,667 ($266,667 – $250,000) by donating $450,000 of shares instead of choosing a cashless exercise and directing the broker to donate the net proceeds. This is because the additional deduction is prorated in the case of a cashless exercise. That said, if the executive does not have all the necessary funds to exercise their options, a cashless exercise may be better than having the options expire and not having any funds to donate.

Alternative Minimum Tax (AMT)

AMT is an alternative method used to calculate your taxes owing and is the federal government's attempt to limit the tax advantage you can receive from claiming certain tax deductions, credits and allowances. As a result, if you exercise options, claim a security options deduction and donate the publicly listed securities acquired on the exercise, you may be subject to AMT. For more details on AMT, please ask your RBC advisor for an article on this topic. A qualified tax advisor can assist you with determining whether AMT would apply in your specific situation.

Conclusion

If you intend to donate to charity, consider donating the shares you acquired by exercising your employee stock options. Not only is it a great way to reduce your out-of-pocket donation cost, but in certain circumstances, you may be able to eliminate your entire tax liability on the exercise of your options. Speak to a qualified tax advisor to determine if this strategy is right for you to help meet your philanthropic goals in the most tax-efficient way.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.