Establishing an RESP

With the high cost of post-secondary education, many parents and other family members recognize the need to save for education well before the expenses become a reality. That's why the registered education savings plan (RESP) is such a popular savings vehicle. Not only is the tax on the income accumulating in the plan deferred until funds are paid out, the federal government and some provinces may also contribute to the plan.

With the high cost of post-secondary education, many parents and other family members recognize the need to save for education well before the expenses become a reality. That's why the registered education savings plan (RESP) is such a popular savings vehicle. Not only is the tax on the income accumulating in the plan deferred until funds are paid out, the federal government and some provinces may also contribute to the plan.

Family Office Services

September 14, 2023

Establishing an RESP

With the high cost of post-secondary education, many parents and other family members recognize the need to save for education well before the expenses become a reality. That's why the registered education savings plan (RESP) is such a popular savings vehicle. Not only is the tax on the income accumulating in the plan deferred until funds are paid out, the federal government and some provinces may also contribute to the plan. This article discusses setting up an RESP, government incentives and saving strategies involving RESPs.

What is an RESP?

An RESP is a tax-deferred savings plan designed to allow the subscriber to open an RESP to save for a beneficiary's post-secondary education. You, as the subscriber, can contribute to the RESP, and the government may provide incentives by also contributing to the plan.

Depending on the type of plan, there could be more than one beneficiary and a beneficiary can be a beneficiary of more than one RESP.

If you have already set up an RESP and would like information regarding withdrawing funds from an RESP or you have questions regarding non-resident issues, please ask your RBC advisor for a separate article on these matters.

Contributions to an RESP

Contributions to an RESP are not tax-deductible. The beneficiary of an RESP must be a resident of Canada at the time contributions are made to the plan.

There is a $50,000 lifetime contribution limit per RESP beneficiary but no annual contribution limit. If the total contributions made for a single beneficiary exceed that beneficiary's lifetime limit of $50,000, you, as the subscriber, may be liable to pay a penalty of 1% per month on excess contributions made to an RESP. The 1% penalty will continue to accrue until you remove the over-contribution. The penalty is not charged for the month in which you make that withdrawal.

Contributions (except transfers from another RESP) cannot be made to a plan at any time after the end of the year that includes the 31st anniversary of the plan or 35th year if the plan is a specified plan. A specified plan is a single beneficiary RESP (non-family plan) where the beneficiary is entitled to receive the disability tax credit (DTC). The DTC is a non-refundable federal tax credit for individuals who have a severe and prolonged impairment.

If you have a family plan, you cannot make contributions for a beneficiary who is 31 years of age or over. However, you can transfer funds from another family plan, even if one or more of the beneficiaries are 31 years of age or over at the time of transfer.

Contributions to an RESP can be made in cash or in-kind. If you are contributing in-kind to an RESP, keep in mind that the asset you're contributing is considered disposed of. This means any accrued gains on the asset will be realized and are taxable to you. However, if the asset you're contributing is in a loss position, you may not be able to claim the capital loss. In this case, you may want to consider selling the asset to realize the loss and contributing cash instead.

Who can be a subscriber?

While parents and grandparents are typically the subscribers to RESPs, there are no restrictions on who can be the original subscriber of an individual RESP. There are restrictions for family plans. See the section on family plans for more details.

A public primary caregiver of a beneficiary under an RESP may also be a subscriber. This may include the department, agency or institution that cares for the beneficiary or the public trustee or public curator of the province or territory in which the beneficiary lives.

It may be possible for you and your spouse or common-law partner to be joint subscribers to an RESP. Or, if you are currently a sole subscriber on an RESP, you may be able to add a spouse or common-law partner as a joint subscriber to the RESP. Further, as of March 28, 2023, it may be possible for you and your former spouse or common-law partner to be joint subscribers to an RESP as long as both of you are the legal parents of a beneficiary of the plan. You will have to check with your particular plan provider to see if they allow for joint subscribers.

You will need to provide your social insurance number (SIN) when you open the RESP. When the subscriber is a public primary caregiver, they will need to provide their business number.

If you did not originally open the RESP, you may become the subscriber if one of the following situations applies:

• On the breakdown of a relationship, you receive subscriber's rights as a result of a court order or written agreement. There is no requirement to separate the RESP assets upon relationship breakdown so former spouses or common-law partners can remain as joint subscribers of a plan after separation or divorce;

• You have, under a written agreement, acquired a public primary caregiver's rights as a subscriber under the RESP; or

• After the death of the subscriber, you acquire a subscriber's rights or you continue to make contributions to the RESP for the beneficiary.

It is also possible for the deceased subscriber's estate to acquire the subscriber's rights under the RESP and become the subscriber.

Death of the subscriber

The maximum life span of an RESP is 35 years (40 years for a specified plan). You may therefore be concerned about the RESP if you were to pass away before the RESP funds have been fully utilized by the beneficiaries. On the death of an RESP subscriber, the terms of the RESP and the relevant provincial law may impact what happens to the RESP.

Here are some planning strategies you can consider to help ensure that someone can continue to manage the RESP:

• Have both you and your spouse or common-law partner act as joint subscribers of the RESP. If one of you were to pass away, the survivor will become the sole subscriber; or

• Designate a successor subscriber in your Will. This can be an individual, estate, trust or company.

A successor subscriber will assume responsibility for the management of the RESP and may also continue to make contributions to the plan. The successor subscriber will generally have the same rights that you have as the original subscriber, subject to the terms of the RESP. This may include having access to the contributions that have been made to the plan so it may be possible for them to remove funds from the plan for their own benefit. Keep this in mind when you're choosing a successor subscriber for your RESP.

If you do not designate a successor subscriber in your Will and you were the sole subscriber of the RESP, the executor or liquidator of your estate may be able to arrange for someone to take over the RESP as a successor subscriber in certain circumstances. The executor or liquidator should seek legal advice if they want to choose a new subscriber. If the executor or liquidator does not arrange for a new subscriber, a person who makes contributions to the RESP after the death of the subscriber can become a successor subscriber.

If you pass away, there are circumstances in which your executor or liquidator may be compelled to wind up the RESP. This can happen if there is no surviving joint subscriber on the RESP, you did not name a successor subscriber in your Will, and the executor or liquidator of your estate does not arrange for a successor subscriber. In this case, the value of the RESP may become part of your estate and be distributed according to your Will.

Depending on the situation, an RESP may be subject to probate on the death of a subscriber. The executor, liquidator or successor subscriber may be asked to provide the death certificate of the original subscriber and inform the financial institution holding the plan of the identity of the new subscriber.

Who can be a beneficiary?

You can name someone as a beneficiary of an RESP if, at the time of designation:

• The intended beneficiary's SIN is provided to the RESP provider; and

• The intended beneficiary is a resident of Canada.

Replacing a beneficiary

In both individual and family RESPs, you may be able to replace an existing beneficiary with a new beneficiary if your specific RESP contract allows you to name a replacement.

Generally, when you replace one RESP beneficiary with a new beneficiary, the CRA treats the contributions for the former beneficiary as if they had been made for the new beneficiary on the date they were originally made. If the new beneficiary already has an RESP, this may create an over-contribution situation and the subscriber may be subject to a penalty. The CRA will not include any contributions made for the former beneficiary when they determine whether the new beneficiary's lifetime contribution limit has been exceeded if:

• The new beneficiary is a sibling of the former beneficiary and is under 21 years of age; or

• Both beneficiaries are connected by a blood relationship or adoption to an original subscriber of the RESP and both are under 21 years of age.

Additionally, if one of the two previously mentioned criteria are not met, a beneficiary replacement may trigger the repayment of certain government incentives. There are also certain government incentives that require the RESP to only have siblings as beneficiaries. If the replacement beneficiary causes the RESP to not meet this sibling-only requirement (e.g. the replacement beneficiary is a cousin of the other beneficiaries in the RESP), those government incentives will need to be repaid to the government. These rules are complex and it is important to speak with the RESP provider prior to naming a replacement so that you fully understand the implications of doing so.

Death of a beneficiary

In the unfortunate event that the beneficiary of the RESP passes away before depleting all the funds in the account, you may designate a replacement beneficiary.

In a family plan where there are multiple beneficiaries, the RESP assets, including CESG, can be shared between the beneficiaries. So, if one of the beneficiaries passes away, their share of the RESP assets may be utilized by other beneficiaries. However, each beneficiary can only receive a lifetime maximum CESG of $7,200. Any CESG remaining in the RESP after the plan has been wound up must be returned to the government.

If there are no beneficiaries of the plan and you decide to not name a replacement beneficiary, you may choose to withdraw the original contributions and it may be possible for you to withdraw the income and growth earned in the RESP. The government incentives may need to be repaid to the government on wind-up of the plan. For more information on withdrawing funds from an RESP, ask your RBC advisor for a separate article on this matter.

Types of plans

The following are different types of RESPs:

• Individual RESPs;

• Family RESPs; and

• Group RESPs.

The type of plan is determined according to the arrangement you enter into with the RESP provider; it is not determined by the number of beneficiaries in the plan. For example, you can set up a family plan that has only one beneficiary. An RESP provider may not offer all the different types of RESPs, so it is important to check with the provider to understand your options.

Individual plans

An individual plan is established for one beneficiary and has fewer limitations than a family plan. The beneficiary can be the subscriber and may or may not be related to the subscriber. There is no age limit for beneficiaries of individual plans. If you want to establish a plan for yourself, or someone who is not related to you by blood or adoption, or if the beneficiary is 21 years of age or over when you establish the plan, you can set up an individual plan.

Family plans

Family plans allow more than one beneficiary in the plan. The beneficiaries must be related by a blood relationship or adoption to each living subscriber or to a deceased original subscriber. This means you can include your children, grandchildren, siblings and adopted children in a single family RESP. Nieces and nephews are excluded as beneficiaries of family plans but you can name them as beneficiaries of individual plans. Adoption includes both legal adoption and adoption in fact. Adoption in fact may exist where the parent of the child is in a common-law relationship and the common-law partner provides parental care on a continuing basis to the child. An individual is not considered to be a "blood relative" of himself or herself.

For family plans established after 1998, each beneficiary must be less than 21 years of age at the time they are named as a beneficiary. However, when one family plan is transferred to another, a beneficiary who is 21 years of age or over can still be named as a beneficiary of the new RESP.

Group plans

A group RESP may also be known as a pooled RESP or scholarship trust plan. These plans pool together all of the members' contributions and government grants. The plan provider makes investment choices on behalf of the members and determines contribution schedules. Payouts from these plans will depend on investment returns and the number of beneficiaries in the plan that qualify for post-secondary education in a given year. The plan may stipulate additional requirements regarding how and when payouts can be made.

There may be substantial fees associated with opening up a group RESP. It is therefore important to understand the provider's fee structure before opening such a plan, as these fees may not be refundable. Also, because there's a contribution schedule set by the provider, if you miss payments, your participation in the plan may be terminated and as a result, you may forfeit the growth earned on your contributions.

Group plans can vary greatly depending on the provider and the arrangement; it is very important to understand all of the restrictions and fees associated with a group plan when considering this option.

Which plan is right for you and your family?

If you have several children, a family plan may be easier to administer. Another advantage of a family RESP is that the funds in the plan do not have to be paid equally to the beneficiaries. This can be useful if one of the named beneficiaries doesn't go on to post-secondary education or if the beneficiaries have different educational costs. For example, if one child stays at home while attending school and another child goes to school out of town, the child living away from home may have significantly higher costs.

In contrast, this flexibility is not available to individual plans. The income earned in an individual plan can only be paid to the named beneficiary of the plan. This could be an issue if the named beneficiary is unable to go or decides not to go to post-secondary school, or does not use all of the funds within the plan.

Families who have children with a significant age difference may want to consider opening individual plans or additional family plans. This is because an RESP has to be wound down by December 31 in the year that includes the 35th (40th for a specified plan) anniversary of the plan. For example, if you established a plan 15 years ago, it will have to be wound down in 20 years from now. If a newborn child is added to this plan, the child will only be 20 when the plan winds down, at which time they may not have completed post-secondary school.

Transfers between RESPs

You can make transfers from one RESP to another without tax implications when:

• The transferring RESP and the receiving RESP have the same beneficiary;

• A beneficiary of the receiving plan is a sibling of a beneficiary of the transferring plan and the receiving plan is a family plan; or

• A beneficiary of the receiving plan is a sibling of a beneficiary of the transferring plan, the receiving plan is an individual plan, and the beneficiary of the receiving plan was under 21 years of age when the receiving plan was opened.

In any other case, transfers may result in an excess contribution. This is because each beneficiary under the receiving RESP assumes the RESP contribution history for each beneficiary under the transferring RESP. The CRA treats each contribution as if it had been made into the receiving RESP on the date of the original contribution to the transferring plan. In addition, CRA treats each subscriber under the transferring RESP as a subscriber under the receiving RESP. This means they may be liable for tax on any excess contributions.

Transfers of property between RESPs are generally not restricted. The effective date of the plan where funds have been transferred, whether it is a partial or total transfer, will be the earlier of:

• The effective date of the plan the funds came from; and

• The effective date of the plan the funds were transferred to.

The effective date is relevant in determining when contributions and transfers to an RESP must end, when accumulated income payments can start and when the plan must be terminated.

When a transfer is made to a plan, there are very strict conditions that must be met in order to transfer the CESG, CLB and other provincial government incentives to the receiving plan. Speak with your RESP provider for additional information.

Canada Education Savings Grant (CESG)

For many subscribers, the CESG is the most attractive feature of an RESP. No matter what your family income, the government pays a basic CESG of 20% on the first $2,500 of annual contributions or a maximum annual CESG of $500 for each beneficiary. The lifetime limit of CESG is $7,200 per beneficiary. If the beneficiary has unused grant room from a previous year, the maximum CESG that can be received in a particular year is $1,000.

Lower-income families may be eligible for an additional grant of 10% or 20% on the first $500 of RESP contributions annually. Eligibility for the additional grant in a particular year is based on the beneficiary's primary caregiver's adjusted income from the second preceding tax year. The primary caregiver's adjusted income includes the net income reported on line 23600 their tax return and the net income of their spouse or common-law partner, if applicable. This adjusted income is compared to thresholds that are annually adjusted to inflation to determine whether an RESP contribution can attract additional grant. For the plan to receive the additional CESG, all of the beneficiaries of a family plan have to be siblings.

For example, let's assume the beneficiary's primary caregiver's adjusted income is $49,500 in 2021. As this income is below the first threshold of $53,359 for 2023, the first $500 of annual RESP contributions will receive an additional 20% CESG of $100, providing a CESG of $600 on a $2,500 contribution. Where the primary caregiver's 2021 adjusted income is between $53,359 and $106,717 (between the 2023 first and second thresholds), the first $500 of RESP contributions for 2023 will receive an additional 10% CESG of $50, providing a CESG of $550 on a $2,500 contribution.

Check to determine if your RESP plan provider supports the additional CESG.

Eligibility for CESG

A beneficiary must be a resident of Canada at the time of the RESP contribution in order to be eligible for CESG. They must also be 15 years of age or less in the year in order to be eligible for CESG. A beneficiary who is turning 16 or 17 during the current calendar year can also qualify for the CESG if one of the following two conditions is met:

• Contributions to all RESPs for the beneficiary are at least $2,000 (and not withdrawn) and were made before the calendar year in which the beneficiary turned 16; or

• Contributions for the beneficiary of at least $100 per calendar year were made in any four years (and not withdrawn) before the calendar year in which the beneficiary turned 16.

If no previous RESP existed for the beneficiary who is turning 16 or 17 in the current calendar year, they will not be eligible to receive the CESG. Any beneficiary who was already 17 years of age at the start of the calendar year will also not be eligible for the CESG.

Accumulating unused grant room

A beneficiary must be a resident of Canada in order to accumulate grant room for any given year. Grant room does not accumulate for years when the beneficiary was not a resident of Canada and it cannot be recovered, even if the beneficiary subsequently becomes a Canadian resident again. The grant room is not pro-rated where the beneficiary was only a Canadian resident for part of the year.

Grant room accumulates at a rate of $500 per year ($400 from 1998–2006) until the end of the year the beneficiary reaches the age of 17, whether or not an RESP account has even been opened for them.

Since the annual CESG is 20% of the RESP contribution made during the year, an RESP contribution of $2,500 attracts the full $500 basic CESG for the year. If you make an RESP contribution of less than $2,500 in a year for a particular beneficiary, it will not attract the full CESG. You can carry forward the remaining CESG amount, also referred to as unused grant room, for future years. Each beneficiary has their own grant room, even if the contributions you make on their behalf are combined with those of other beneficiaries in a family RESP.

Using up the unused grant room

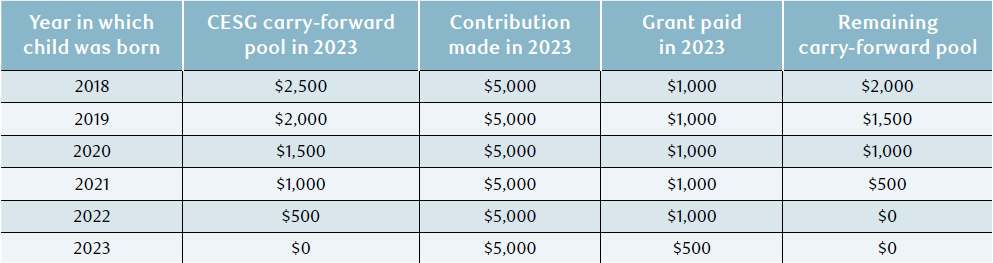

When you make a contribution to an RESP of more than $2,500 per year, you may be able to use the carry-forward pool. The maximum grant available in a year is limited to $1,000 or 20% of the first $5,000 of RESP contributions that you make. This will allow you to use up $500 of unused grant room.

For example, a child who is born in 2018 and for whom no RESP contributions have ever been made, will have a total pool of $2,500 in 2023 in unused grant room ($500 for each of 2018-2022). A contribution of $5,000 in 2023 will attract grant of $1,000, made of $500 for the 2023 contribution and $500 from the unused grant room.

To determine what past contributions have been made to an RESP and the amount of the grant carry-forward pool, you can contact Employment and Social Development Canada (ESDC).

Sharing CESG among beneficiaries of a family plan

One of the benefits of a family plan is that accumulated CESG contributions do not have to be paid out equally among beneficiaries. However, keep in mind that the maximum lifetime CESG each beneficiary can receive is $7,200. If a beneficiary doesn't pursue post-secondary education and is not able to share the accumulated CESG with another beneficiary, that beneficiary's CESG may have to be returned to the government.

For example, Mr. and Mrs. Smith set up a family plan for their 10-year-old twins. They contribute $5,000 per year for six years, designating $2,500 for each beneficiary. Since they contributed equal amounts to each child, the grant allocated to each child will be $500 per year for a total of $3,000. Assuming a 4% average annual rate of return and that contributions and grant are paid into the plan at the end of the year, the plan will have a total balance of $39,798 at the end of six years, including the CESG. Since the total CESG in this plan does not exceed $7,200, if one child goes to a school that is much more expensive than the other child's school, all or the majority of the CESG in the plan can be paid out to the child who needs it. There is no requirement to pay out $3,000 of CESG to each child.

The impact on CESG when a large lump-sum contribution is made

There is a $50,000 lifetime contribution limit per RESP beneficiary but no annual maximum contribution limit. So should you contribute $50,000 up front to your RESP to take immediate advantage of the tax deferral opportunity?

The issue is that if you contribute $50,000 up front, you will forfeit the ability to receive future CESG, which may otherwise be available if you make annual contributions.

The CESG is paid based on 20% of the annual RESP contribution amount, to a maximum of $500, or if there is CESG unused grant room, to a maximum of $1,000. So, if you make a one-time lump-sum contribution of $50,000 to the plan, the maximum CESG the plan could receive is $1,000. Grants are not paid to the plan in future years for past years' contributions.

If you wish to maximize the RESP, one strategy you may want to consider is instead of making a full lump-sum contribution right away, contribute a lump-sum of $14,000 in the first year you set up the RESP in addition to the $2,500 regular contribution. This will leave you with enough contribution room to make annual contributions that will maximize the CESG and allow you to make use of the lifetime contribution limit. If we break down the numbers, in order to receive the full $7,200 of CESG, annual contributions of $2,500 must be made for 14 years plus a contribution of $1,000 in the 15th year (this is assuming there is no unused grant room). The total contributions you will need to make to maximize the CESG is $36,000, leaving $14,000 of unused RESP contribution room. Making the lump-sum contribution of $14,000 as early as possible can help you maximize the tax-deferral benefit of the RESP.

When deciding if you want to make a lump-sum contribution up front, you'll want to consider:

• Your ability to make a large immediate contribution;

• The age of the beneficiary. This is used to determine the balance of the unused grant room, the number of years remaining where grant can be received and the approximate timing of future withdrawals;

• Your marginal tax rate on non-registered investment income;

• Your expected rate of return on the investment income (both inside and outside the RESP); and

• Your beneficiary's expected marginal tax rate when the funds are withdrawn. This is often minimal given the basic personal exemption and other tax credits available to students.

Speak with your RBC advisor about the RESP funding strategy calculator. It can help illustrate the potential outcome of making a $50,000 lump-sum contribution to an RESP compared to annual contributions that maximizes the CESG received.

Canada Learning Bond (CLB)

A $500 CLB is available for children of modest-income families born on or after January 1, 2004. These children also qualify for CLB instalments of $100 per year until age 15. The total lifetime maximum CLB payable per child is $2,000.

You do not have to make contributions to an RESP in order to receive the CLB. Further, unlike CESGs, CLBs cannot be shared with other beneficiaries. You will have to check to see if the RESP plan provider supports receipt and payment of the CLB.

Eligibility for the CLB is based on the:

• Number of qualified children in the family; and

• Adjusted income of the primary caregiver, which includes the income of a spouse or common-law partner. Like the additional CESG, adjusted income from the second preceding year is used to determine eligibility for the CLB.

Additional government incentives

A number of provincial governments provide additional incentives for their residents who open up an RESP. They are as follows:

• The British Columbia Training and Education Savings Grant (BCTESG) will provide a one-time grant of $1,200 to the RESP of a child who is a resident of British Columbia and has a custodial parent or a legal guardian who is also a resident. The grant is available for children born in 2006 or later. The earliest you can request the grant is when the beneficiary turns six. After that, you may apply any day before their ninth birthday.

• The Quebec Education Saving Incentive (QESI) is a refundable tax credit that is paid into an RESP by the Quebec government to support the education savings of its residents. Annual RESP contributions of up to $2,500 are eligible for a basic amount of 10%. Lower-income families are eligible for an additional amount (up to $50) on the first $500 of annual RESP contributions. A total cumulative QESI amount of $3,600 can be granted per child.

• The Saskatchewan Advantage Grant for Education Savings (SAGES) provided a grant of 10% on contributions made to an RESP for a child residing in Saskatchewan. The SAGES program has been cancelled and any grants previously received in existing plans have been converted to accumulated income.

Payments of the following education savings incentives can only be paid into an individual plan or a family plan if all of the beneficiaries in the plan are siblings:

• CLB;

• Additional CESG; and

• British Columbia Training and Education Savings Grant (BCTESG).

You will have to check to see if the RESP plan provider supports the additional provincial incentives.

Opportunities and constraints for grandparents

Grandparents may have the desire and the financial means to contribute to an RESP for their grandchildren. It can be a wonderful way to give a meaningful gift.

If you are a grandparent, you can establish an RESP yourself (i.e., be the subscriber) and contribute to the RESP for your grandchildren. However, you may want to consider an alternative approach. You could consider gifting the funds to your son or daughter who in turn establishes the RESP for your grandchildren. In both cases, you provide the financial gift and your grandchildren are the beneficiaries of the RESP, but in the latter case, your child (the parent of the beneficiaries) will be the subscriber of the plan.

The advantage of the second approach is that if one of the beneficiaries does not attend post-secondary education, the subscriber may be able to transfer the earnings from the RESP to their own registered retirement savings plan (RRSP), within certain limits. This is discussed further in a separate article on withdrawing funds from an RESP. Ask your RBC advisor for a copy of this article.

The subscriber must be 71 years of age or younger to do this. As RESP plans have a potential life span of 35 years (40 for a specified plan), by the time you realize that one of your grandchildren will not attend school, you may have exceeded the age at which you are eligible to make an RRSP contribution, whereas your son or daughter may still be able to benefit.

The disadvantage of this approach is that you have little or no legal control over the funds. Your son or daughter will have control over the funds and there is no guarantee that they will follow your wishes. Even if the funds are contributed to an RESP, as the subscribers, they will have the ability to withdraw the contributions.

If you're considering a family plan, grandparents may have an advantage when establishing multiple beneficiary plans. As a grandparent, you can include all of your grandchildren in one family RESP. A parent, by comparison, cannot include the same list of beneficiaries since they cannot include nephews and nieces as beneficiaries of a family plan.

Investment options

Investment risk and asset allocation

As with any other investment account, you must consider your risk tolerance, investment objectives, investment time horizon and any investment preferences you may have when you determine the appropriate investments for the RESP funds. Keep in mind that if any losses are realized in the RESP, you cannot personally claim the loss.

Another point you should consider is that while you can invest in foreign securities in the RESP, the income may be subject to non-resident withholding tax. You cannot claim a foreign tax credit on your personal tax return for any foreign tax withheld. If you are considering foreign investments, you may want to invest in securities that generate income that is not subject to non-resident withholding tax. For example, generally, U.S. interest income and UK dividends are not subject to withholding tax. However, as always, it is important to analyze the investment merits of the investments before looking at the tax implications when deciding how to structure your portfolio.

Types of eligible investments

There are rules that restrict the types of investments you can make in an RESP. Common types of qualified investments include GICs, publicly traded shares and bonds, and mutual funds. If an RESP acquires a non-qualified or prohibited investment, or holds a property that ceases to be a qualified investment or becomes a prohibited investment, you may be subject to penalty tax. It is important to consult with your qualified tax advisor and the RESP provider when deciding on types of investments to hold in your RESP.

Conclusion

There are many considerations you need to take into account when opening an RESP. The type of plan you choose, how you will fund the RESP and who the subscriber of the plan will be can have a number of implications in the future. Speak to your RBC advisor to help you assess the options that are available to you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.