Estate Planning for U.S. Transfer Taxes

Estate planning can be especially complex for families who are subject to both the U.S. tax system (including U.S. income tax and U.S. transfer tax) and the Canadian income tax system. This article explores common strategies that may help reduce your and your heirs' exposure to the U.S. transfer tax system while also taking Canadian tax rules into account. Intended for U.S. persons and non-U.S. persons with U.S. spouses living in Canada.

Estate planning can be especially complex for families who are subject to both the U.S. tax system (including U.S. income tax and U.S. transfer tax) and the Canadian income tax system. This article explores common strategies that may help reduce your and your heirs' exposure to the U.S. transfer tax system while also taking Canadian tax rules into account. Intended for U.S. persons and non-U.S. persons with U.S. spouses living in Canada.

Family Office Services

December 14, 2025

Estate Planning for U.S. Transfer Taxes

Common Canadian-U.S. Planning Strategies

This article applies to individuals living in Canada who are U.S. persons or who are non-U.S. persons with a spouse who is a U.S. person. For information on how to determine whether you are a U.S. person, please ask your RBC advisor for an article on that topic.

Estate planning can be especially complex for families who are subject to both the U.S. tax system (including U.S. income tax and U.S. transfer tax) and the Canadian income tax system. To maximize the amount of wealth transferred to your heirs when you pass away, you may want to consider using strategies to potentially help reduce your and your heirs' exposure to the U.S. transfer tax system while also taking the Canadian tax rules into account.

In this article, we explore examples of common strategies that may be used. Please note that the information provided is based on the U.S. transfer tax laws for U.S. federal purposes, Canadian federal tax laws and the Canada-U.S. Tax Treaty (the Treaty). It's also important to note that some U.S. states may levy a U.S. transfer tax on Canadians owning property located in such states (which is not covered in this article).

Note: The H.R.1 budget reconciliation bill known as the "One Big Beautiful Bill Act" (OBIBA) was signed into law on July 4, 2023. The OBIBA permanently increases the unified estate and gift tax exemption amount to US$15 million beginning in 2026 (indexed to inflation). This change also applies to the generation skipping transfer tax exemption. The existing 40% maximum tax rate remains unchanged. The increase in the U.S. estate, gift and GSTT exemptions is permanent and is not subject to expire, however changes to the exemptions can be made by future U.S. governments.

Note: Canadian provincial and territorial tax laws are not addressed in this article. However, it is important to note that Canadian provinces and territories are generally not subject to the provisions of the Treaty and will only allow foreign tax credits for U.S. transfer tax incurred on U.S. property if the provincial legislation provides for it. For example, British Columbia and Ontario do not provide any foreign tax credit relief for U.S. estate tax.

Overview of the U.S. transfer tax and Canadian tax systems

The U.S. transfer tax system includes a U.S. gift tax, U.S. estate tax and U.S. generation-skipping transfer tax (GSTT), which applies to the value of certain gifts made during your lifetime or on the value of certain property you own at the time of your death. A more detailed discussion of the U.S. transfer tax system is available in a separate article, which you may obtain from your RBC advisor.

The Canadian tax system does not include an estate or gift tax. Instead, property transferred by way of gifts made during your lifetime or bequests made upon your death are generally subject to Canadian tax through the 'deemed disposition' rules. When these rules apply, you're generally deemed to have sold your property for fair market value (FMV). As a result, you're taxed on the net capital gains accrued on your property. There are exceptions to these rules, such as when you transfer property to your spouse or a qualifying spousal trust.

In addition to the deemed disposition rules, income earned on property gifted during your lifetime to a spouse or minor child or grandchild may trigger the Canadian income attribution rules. These rules may require that you, as the transferor, pay Canadian tax on the income that's earned on the property you gifted.

It is important to keep both the Canadian and U.S. tax rules in mind when developing your estate plan.

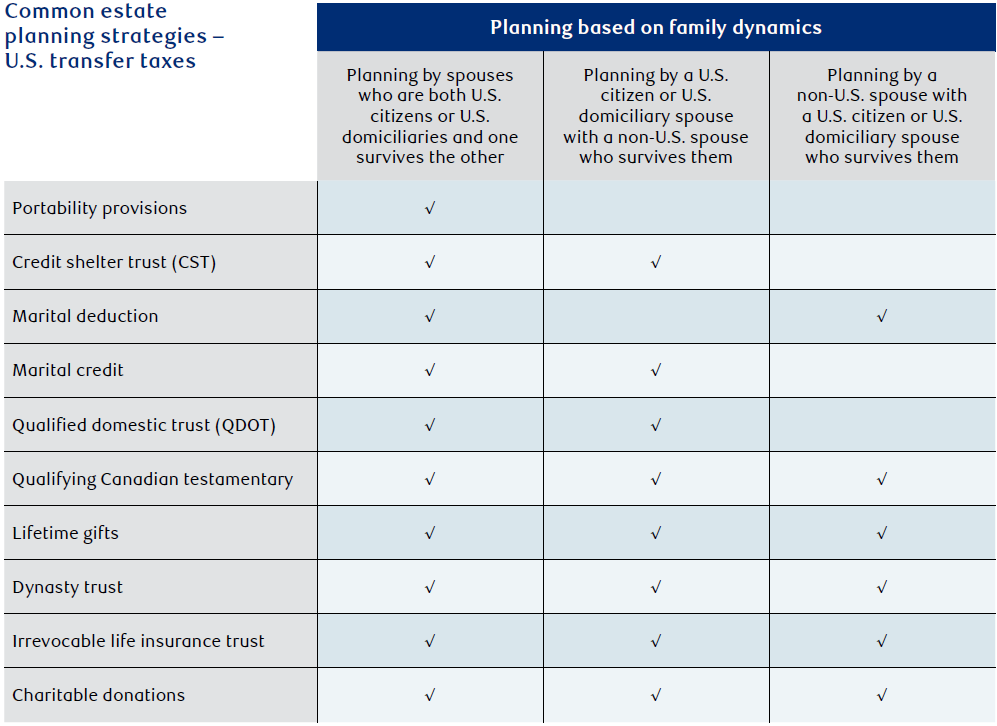

Common cross-border estate planning strategies

The following table lists some of the common cross-border estate planning strategies (this is not intended to be an exhaustive list) that may be used in different family dynamics.

Portability provisions

The U.S. transfer tax system contains portability provisions that may be incorporated in an estate plan for a couple where both spouses are a U.S. citizen or U.S. domiciliary.

The portability provisions allow a surviving spouse to use their deceased spouse's unused U.S. gift or estate tax exemptions, as well as their own, to minimize or eliminate U.S. gift and estate taxes. However, the provisions do not allow the surviving spouse to use the deceased spouse's unused GSTT exemption. The surviving spouse may use only their own GSTT exemption.

To access the portability provisions, an election has to be made on the deceased spouse's U.S. estate tax return to transfer the unused exemptions of the deceased spouse to the surviving spouse. The U.S. estate tax return must be filed in order to make the election, even if there's no U.S. estate tax liability.

The portability provisions provide the surviving U.S. spouse with the potential to transfer wealth of up to two times the U.S. gift or estate tax exemption threshold to beneficiaries (free of U.S. gift or U.S. estate tax) either during their lifetime or upon their death.

Who may benefit from these provisions?

The portability provisions are generally useful for couples with estate values that are not expected to grow beyond the gift and estate tax exemption thresholds. Couples with such estates may want to consider leaving all of their property to each other and may choose to rely solely on the portability provisions when planning for U.S. estate tax.

Couples may want to consider including other planning strategies in their estate plans in case the portability provisions prove to be insufficient at the time of death, at which time, it may be too late to implement other strategies. For example, since the portability provisions cannot insulate the property and future growth in excess of the exemption thresholds, couples with larger estates risk greater exposure to U.S. gift tax and U.S. estate tax for themselves and their beneficiaries if they rely solely on the portability provisions. For these couples, other estate planning strategies may make sense.

Credit shelter trust (CST)

U.S. citizens and U.S. domiciliaries can protect their heirs from U.S. estate tax by leaving property to them in a CST, also known as a "bypass trust" or an "A/B trust".

A CST is an irrevocable testamentary trust created through your Will for the benefit of your beneficiaries, such as your spouse, children and/or grandchildren. When you pass away, the value of property up to your U.S. estate tax exemption may be transferred, free of U.S. estate tax, to the CST. Since the trust is funded with property from your estate, it's important not to hold property you intend to transfer to the CST jointly with a spouse.

When a beneficiary of a CST dies, the value of the property in the trust (property transferred in and any future growth) is excluded in determining the beneficiary's U.S. estate tax liability.

Trustee considerations

As the CST is a trust, you'll want to give some thought as to who will be the trustee(s) (i.e. who will hold responsibility and control over the trust). If you are thinking of appointing your spouse as a trustee, keep in mind that in order for the CST to provide for estate tax protection to a deceased beneficiary, the beneficiary spouse cannot be provided with a general power of appointment over the property in the CST.

The U.S. transfer tax laws provide that a general power of appointment is such a power exercisable in favour of the beneficiary, the beneficiary's estate and creditors of the beneficiary or the beneficiary's estate. These powers do not actually need to be exercised to cause exposure to U.S. estate tax. Therefore, care should be taken when determining the powers that will be provided to the trustee(s) of the CST.

Income earned in a CST may be distributed to a beneficiary during their lifetime, while the beneficiary's authority to access the capital of the trust must be restricted. The beneficiary may be granted the power to request a trustee to distribute, annually, up to 5% of trust property or $5,000, whichever is greater. It's also possible to structure the CST to allow a beneficiary to access the capital of the trust without creating a general power of appointment by including an "ascertainable standards" clause. This clause restricts the use of the capital only for health, education, support or maintenance.

An independent trustee, if named in the Will, is permitted to make additional payments of capital or income from the trust to a beneficiary. Such a trustee is someone who has not contributed to, and cannot benefit from, the trust. They must not be a person related to the settlor (the person who created the trust) or beneficiary nor an employee of either. Examples of independent trustees may be a corporate trustee that's a financial institution or a family friend.

It's important to consider these restrictions on the beneficiaries when deciding how much of your estate will be transferred to the CST. In addition to the CST, you may want to consider less restrictive strategies or making gifts to your beneficiaries directly if you want them to have greater access to a portion of the property in your estate.

Canadian tax considerations

For Canadian tax purposes, the transfer of property on your passing to someone other than your spouse or to a qualifying Canadian testamentary spousal trust on behalf of your spouse may result in a deemed disposition of the property. If the trust is not a qualifying Canadian testamentary spousal trust, the property in the trust will generally be subject to a deemed disposition at every 21 years during the existence of the trust. One way to deal with this deemed disposition is to have the trust distribute appreciated property to Canadian resident beneficiaries before the 21st anniversary of the trust. The gain from the distributed appreciated property can then be deferred until the beneficiary passes away or earlier if the property is disposed. Where the property is transferred to your spouse or to a qualifying Canadian testamentary spousal trust, there is a deemed disposition on the property only when your surviving spouse passes away.

In order for the CST to be a qualifying Canadian testamentary spousal trust, the CST and the deceased spouse must both be Canadian residents immediately before the passing of the deceased spouse. Further, a CST that's deemed resident in Canada cannot be a qualifying Canadian testamentary spousal trust (because it has to be factually resident in Canada). Another criteria that must be met is the CST must provide that only the surviving spouse is entitled to receive all of the income from the CST during their lifetime and no other person can benefit from the income or the capital of the CST during the spouse's lifetime.

Other intended heirs such as children and grandchildren may be able to receive the trust assets after the death of the surviving spouse. However, if you'd like them to benefit from your estate prior to your death or the death of your surviving spouse, you may want to consider making outright lifetime gifts or provide them with distributions from your estate.

To illustrate how the CST may be an effective estate planning strategy, please refer to Appendix 1 for an example of an estate plan using a CST where both spouses are U.S. citizens or U.S. domiciliaries and Appendix 2 where only one spouse is a U.S. citizen or U.S. domiciliary and they are survived by a non-U.S. spouse.

Marital deduction

The marital deduction provides the estate of the first spouse to pass away with an unlimited deduction to reduce the value of their taxable estate that is subject to U.S. estate tax. To qualify for the marital deduction, the surviving spouse must be a U.S. citizen and the property of the first spouse to pass away must be left to the surviving U.S. citizen spouse, either directly or to a spousal trust that makes an election to treat the property as Qualified Terminal Interest Property (QTIP).

The QTIP election provides the surviving U.S. citizen spouse with a lifetime income interest in the property of the spousal trust. There are two important requirements:

• The annual income of the spousal trust must be paid to the surviving spouse annually; and

• The surviving spouse must be the only beneficiary who can access the capital of the trust during their lifetime.

When the surviving spouse passes away, the property will be included in their taxable estate for U.S. estate tax purposes. Therefore, the marital deduction in effect provides a deferral of U.S. estate tax that's determined upon the surviving spouse's death. The U.S. estate tax is levied based on the taxable assets of the surviving spouse's estate and the tax laws applicable in the year of death. The surviving spouse may use their own U.S. estate tax exemption and may use any unused exemption ported from their deceased spouse through the portability provisions.

Note that property that transfers to a CST upon the death of the first spouse does not qualify as QTIP and therefore the estate can't claim a marital deduction for this property. Only the value of property up to the deceased spouse's U.S. estate tax exemption may be transferred to a CST free of U.S. estate tax. As a result, the property directed to the CST is protected from U.S. estate tax upon the surviving spouse's death but the property in a spousal trust that makes a QTIP election is not.

Where the surviving spouse is not a U.S. citizen, there's an option to claim the marital deduction by the estate of the first spouse to pass away, provided the property subject to U.S. estate tax is transferred to a QDOT for the benefit of the surviving non-U.S. spouse.

Marital credit

Under the Treaty, it may be possible for the estate to claim a marital credit for property left to a surviving spouse, even if the spouse is not a U.S. citizen. The marital credit essentially doubles the unified credit that may be claimed by the deceased's estate.

The Treaty provides that to qualify for the marital credit, the first spouse to pass away must be a resident of Canada or the U.S. and the taxable property of the estate must be transferred to a surviving U.S. or Canadian spouse directly or to a spousal trust. The surviving spouse must be a resident of the U.S. or Canada, and if both spouses are residents of the U.S. at the time of death, at least one spouse must be a Canadian citizen. Theoretically, the marital credit may be claimed when the surviving spouse is a U.S. or a non-U.S. citizen. Therefore, a deceased spouse with a U.S. citizen surviving spouse could decide to claim the marital credit instead of the marital deduction.

Keep in mind that the property held by a surviving spouse directly when the deceased has claimed the marital deduction or the marital credit may be exposed to U.S. estate tax. Property transferred to a spousal trust when the marital deduction is claimed must make a QTIP election, and as a result the property is exposed to U.S. estate tax because the trust can't be structured to provide U.S. estate tax protection. When the marital credit is claimed, the QTIP election is not required, which may potentially allow for the spousal trust to be structured in a way that provides U.S. estate tax protection.

A decedent's estate which claims the marital credit cannot also claim a marital deduction.

Qualified domestic trust (QDOT)

When the surviving spouse is not a U.S. citizen, the estate of first spouse has the option of setting up a QDOT in lieu of claiming the marital credit. The QDOT allows the estate of the deceased first spouse to claim an unlimited marital deduction to defer U.S. estate tax for this deceased spouse.

The QDOT is a trust where the surviving spouse is the sole beneficiary. The surviving spouse may receive distributions of income earned in the QDOT annually without triggering U.S. estate tax for their deceased spouse. However, U.S. estate tax will be triggered for their deceased spouse on the value of capital property that's distributed to the surviving spouse during their lifetime and on the value of any property remaining in the QDOT on the surviving spouse's death.

When the deferral ends and U.S. estate tax is triggered for the estate of the deceased first spouse, the surviving spouse cannot use their own U.S. estate tax exemption to minimize or eliminate it. This is because the estate tax is a deferral of the first spouse's estate tax liability. The U.S. estate tax liability is calculated based on the estate tax rates that existed in the year of first spouse's death, not the rates that exist in the year capital is distributed or in the year of the surviving spouse's death.

Specific QDOT considerations

There is a trade-off for implementing the QDOT to receive a complete deferral on the first spouse's death versus claiming the marital credit, which may not provide a complete deferral. While the U.S. estate tax of the first spouse to die is deferred with a QDOT, the estate tax when the deferral ends applies not only on the value of property transferred to the QDOT but also on the value of any growth on the property. Therefore, if the property in the QDOT is expected to grow substantially, the estate tax liability could potentially be much greater than the estate tax liability on the value of the property at the time of the first spouse's death. Also, where the marital credit is claimed, it may be possible to transfer the property to an estate tax protected spousal trust to provide estate tax protection for the property transferred in and any growth in the value of the property. This may result in a larger transfer of wealth to future generations.

A QDOT may be useful in certain circumstances such as when the current U.S. estate tax liability will be a significant amount, the surviving spouse is expected to live a long time, the estate does not otherwise have the liquidity to pay the tax liability and/or the spouse is expected to become a U.S. citizen. If the surviving spouse becomes a U.S. citizen during the life of the QDOT, the QDOT is able to distribute capital to the U.S. citizen surviving spouse free of U.S. estate tax and the value of the property is included in the estate of the surviving spouse upon their death.

QDOT criteria

There are a number of criteria that must be met in order for a trust to qualify as a QDOT. First, at least one trustee must be a U.S. citizen or U.S. corporation. If the property in the QDOT has a value of at least US$2 million at the time of the first spouse's death (or an alternate valuation date, if applicable), at least one trustee may need to be a U.S. bank or a bond or letter of credit may need to be provided in favour of the Internal Revenue Service (IRS).

A Will may be drafted to include provisions to allow for the flexibility to implement a QDOT. However, even if it's not provided for in the Will, a QDOT may still be implemented by the executor if it's set up within nine months of the death of the first spouse. Where a QDOT is provided for in a Will, it may be structured as a qualifying Canadian testamentary spousal trust.

Other heirs such as children and grandchildren may receive property in the QDOT after the death of the surviving spouse. If the desire is for these beneficiaries to benefit from the estate prior to the death of the surviving spouse, you may want to consider providing for them with outright distributions from the estate or providing them with lifetime gifts.

You should seek the advice of a qualified cross-border professional if you're considering incorporating a QDOT in your estate plan.

Qualifying Canadian testamentary spousal trust

A qualifying Canadian testamentary spousal trust is a special type of trust that can be established by a Canadian resident through their Will to transfer property to a trust for the benefit of the surviving spouse. This type of trust provides certain Canadian tax benefits and it may be possible to structure it to protect the surviving spouse from U.S. estate tax.

As mentioned previously, CST, a spousal trust that makes the QTIP election or a QDOT may be structured as a qualifying Canadian testamentary spousal trust that provides deferral of Canadian tax that may otherwise arise upon the death of the first spouse under the Canadian deemed disposition rules. The tax on accrued capital gains on property that's transferred into the trust is deferred until the property is sold or when the surviving spouse dies.

Considerations for the qualifying Canadian testamentary spousal trust

To be considered a qualifying Canadian testamentary spousal trust, certain conditions must be met. As such, it may be difficult for such a trust to be structured to qualify equally as a U.S. resident trust. If the qualifying Canadian testamentary spousal trust is not resident in the U.S., the U.S. foreign trust rules must be considered for U.S. beneficiaries. For more information on U.S. foreign trust rules for Canadian trusts, please ask an RBC advisor for an article on this topic.

To protect the property transferred to the trust and future growth of the property from U.S. estate tax, your spouse as a beneficiary should not be given a general power of appointment. If you want to provide your spouse with more flexibility, an independent trustee may be named who can approve additional capital distributions. When your surviving spouse dies, their estate will be exempt from having to include the value of the property in the trust in determining their U.S. estate tax liability. However, it's important to recognize that the estate of the first spouse to die may be subject to U.S. estate tax as a result of transferring property to the U.S. estate tax protected spousal trust. For example, where a non-U.S. spouse is survived by a U.S. citizen spouse, U.S. estate tax may apply to U.S. situs property transferred to the spousal trust, if their own pro-rated unified credit is not sufficient to offset their U.S. estate tax liability.

In Appendix 3, there's an example of estate planning using a qualifying Canadian testamentary spousal trust strategy where a non-U.S. spouse is survived by a U.S. citizen or U.S. domiciliary spouse.

Lifetime gifts

An estate planning strategy that may allow you to reduce the value of your estate for U.S. estate tax purposes is making gifts during your lifetime. You can consider rebalancing the ownership of property with a spouse. Alternatively, gifts may be made directly to your heirs or to a living trust for their benefit.

Since U.S. citizens and U.S. domiciliaries are exposed to U.S. estate tax on their worldwide estate value, they may gift any type of property they own in order to reduce their exposure. For non-U.S. persons, U.S. gift tax only applies to U.S. situs tangible property (see examples below). But upon death, the estate tax applies to both U.S. situs tangible as well as intangible property. Therefore, non-U.S. persons may consider gifting U.S. situs intangible property before other types of property to avoid estate tax on such property.

U.S. gift tax should be taken into account when gifting strategies are utilized. Keep in mind that GSTT may also apply when gifts are made to "skip" individuals such a grandchildren and great-grandchildren. U.S. citizens and domiciliaries are subject to U.S. gift tax and U.S. GSTT on any type of property gifted. Non-U.S. persons are subject to U.S. gift tax and U.S GSTT only on gifts of U.S. situs property that is tangible property.

Tangible U.S. property includes U.S. real estate and cars, boats, artwork, jewelry permanently located in the U.S. and cash located in a safety deposit box in the U.S. or in a non-deposit account at a U.S. financial institution.

Exclusions and exemptions

Gifts made during the year up to an annual exclusion threshold can be made free of U.S. gift tax or GSTT. For 2026, gifts made in the year with a combined value of up to US$19,000 per year can be made to any person free of U.S. gift tax or U.S. GSTT. If the gifts are made to a non-U.S. citizen spouse, the annual exclusion amount is US$194,000 per year. Gifts to a U.S. citizen spouse are not subject to U.S. gift tax.

The U.S. gift tax and U.S. GSTT laws provide U.S. citizens and domiciliaries a lifetime U.S. gift tax and U.S. GSTT exemption. For 2026, each of these exemptions amounts to US$15 million. These lifetime exemptions allow for taxable gifts in excess of the annual exclusion amounts to be made without incurring U.S. gift tax or U.S. GSTT. Non-U.S. persons are not eligible for the lifetime U.S. gift tax exemption; however, they are eligible for the lifetime GSTT exemption.

Double tax exposure with gifting

Canadian tax laws must be considered when property is gifted. Due to differences in Canadian and U.S. tax laws, the potential for double tax may result where both Canadian tax and U.S. gift tax and U.S. GSTT are payable. If a gift of property will result in significant exposure to double taxation, you may want to consider selling the property instead of gifting it. A sale of the property at FMV is not subject to U.S. gift tax and U.S. GSTT.

When property is gifted

When property is gifted to someone other than your spouse, Canadian tax may be triggered because you're deemed to have disposed of the property at FMV and you may be liable for capital gains tax.

If U.S. gift tax and U.S. GSTT are also triggered, double taxation may result, since you can't offset U.S. gift tax or U.S. GSTT against the Canadian tax on the accrued gains and vice versa. For example, if you gift U.S. real estate to a child, you can't claim a foreign tax credit for U.S. gift tax you incurred against your Canadian taxes. Further, you can't reduce the U.S. gift tax incurred with the Canadian tax you paid on the capital gain.

The same issue applies where the gift is made to a grandchild or greatgrandchild where, in addition to Canadian tax, there may be U.S. gift tax and U.S. GSTT incurred.

When income is earned on the property gifted

The Canadian income attribution rules may apply to subsequent income and capital gains earned on property gifted to minors or a spouse, which may result in double taxation. This is because there will be different individuals being taxed under the Canadian and U.S. tax laws.

For example, the Canadian income attribution rules require the spouse making the gift to be taxed on interest, dividends and capital gains earned on the property gifted to their spouse. If the property is a gift to a minor child or a grandchild, the income attribution rules apply to the interest and dividends earned on the property, not the capital gains. In contrast, for U.S. income tax purposes, generally your spouse, child or grandchild who owns the property is subject to U.S. income tax on the income or gains earned.

When there are different individuals taxed on the income or the gain for Canadian and U.S. tax purposes, foreign tax credits are not permitted to be claimed in order to minimize or avoid double taxation.

What happens when the gifted property is sold?

When the gifted property is eventually sold, double tax can result due to the taxation timing of the accrued gains on the property.

For example, if you were to gift property to someone other than your spouse, you would pay Canadian tax on the accrued gains in the year the gift is made. For Canadian tax purposes, the cost base of the property to the individual who receives the gift is the FMV of the property at the time of the gift.

For U.S. income tax purposes, no income tax would be triggered on the accrued gains when property is gifted and there is no change to the cost base. The cost base of the gifted property (for U.S. tax purposes) becomes the recipient's cost base. However, if U.S. gift tax applies, there may be an increase to the cost base for the individual who receives the property by a portion or all of the U.S. gift tax incurred.

When the property is sold, the individual who was gifted the property is subject to U.S. income tax on the accrued gains. Since accrued gains were already subject to Canadian tax in the year the gift was made, there is a potential for double tax since foreign tax credits cannot be claimed.

To minimize the double tax, it is possible to make an election under the Treaty in the year the gift is made to treat the gift as a disposition for U.S. income tax purposes. This will result in a change to the cost base for U.S. tax purposes to FMV for the individual receiving the property. In this case, the U.S. and Canadian tax occurs in the same year. As such, it may be possible to claim foreign tax credits to reduce or eliminate double taxation. This election may make sense where the U.S. income tax triggered on the accrued gains can be fully eliminated through claiming foreign tax credits.

Gift splitting

When both spouses are U.S. citizens or U.S. domiciliaries, they may use "gift splitting" to reduce the value of their taxable estate. Gift splitting allows one spouse to fund the entire amount of the gift but to have the gift treated as though one-half was made by each spouse. For example, one spouse makes a gift of US$38,000 with their own property to a child or grandchild but each spouse is treated as having made a gift of US$19,000. Since the value of the gift made by each spouse is within the annual gift tax exclusion threshold for both U.S. gift tax and U.S. GSTT purposes, the gift is not taxable.

You can make an election to split the gift by filing a U.S. gift tax return. Gift splitting is not available when one spouse is not a U.S. citizen or a U.S. domiciliary. The ability to split gifts provides a spouse who will have a larger estate on death the ability to make larger gifts of property without triggering U.S. gift tax and U.S. GSTT. For example, a U.S. citizen couple with three children may gift up to US$114,000 (US$38,000 x 3) annually without triggering U.S. gift tax, and the gift may be made by the spouse who would benefit the most by reducing their worldwide estate value. If the couple also make gifts to three grandchildren, they'll be able to make tax-free gifts of US$228,000 (US$38,000 x 6) annually. These gifts can also be made to the spouses of your children, which can further increase the amount of tax-free gifts that can be made.

The Canadian tax issues discussed earlier (deemed disposition and attribution rules) need to be considered where split gifts are made and the child or grandchild who earns income on the property gifted is a minor. Note that the Canadian tax rules do not recognize the U.S. gift splitting rules. Therefore, the entire gift is deemed to have been made by the spouse who funds the gift.

Payments not considered gifts

A U.S. citizen or U.S. domiciliary can make direct payments on behalf of a child or grandchild to educational organizations for tuition expenses (e.g. tuition fees) or to a healthcare provider for medical services (e.g. amounts paid for a medical test to diagnose a disease). These payments may exceed the annual exclusion amounts, since they're not considered to be gifts for the purposes of U.S. gift tax.

The funds must not be given directly to the child or grandchild to pay for these expenses, otherwise the payment will be considered a gift. Paying for books, supplies, room and board, or other types of educational expenses directly would also be considered gifts, as they would not qualify as tuition payments.

Note that since these direct payments will not be used to earn income, they are not subject to the Canadian income attribution rules.

Rebalancing non-U.S. situs property with your non-U.S. citizen spouse

A U.S. citizen or U.S. domiciliary can potentially minimize their exposure to U.S. estate tax by rebalancing the ownership of property with a spouse who's not a U.S. person. A rebalancing strategy could involve making tax-free gifts annually that don't exceed the annual exclusions under the U.S. gift tax rules.

Since U.S. estate tax for non-U.S. persons applies only to U.S. situs property and the cost base of the property gifted for U.S. income tax purposes becomes the recipient's cost base, gifts of non-U.S. situs property followed by gifts of U.S. situs intangible property may be chosen over U.S. situs tangible property.

Generally, it's not advisable for U.S. citizens and U.S. domiciliaries to make gifts in excess of the annual exclusions. Doing so would require the use of their lifetime gift or GSTT exemptions in order to avoid U.S. gift tax and U.S. GSTT and every dollar used reduces the U.S. estate tax and U.S. GSTT exemption they can use upon their death.

However, there are situations where it could make sense to use your lifetime exemptions. For example, if you're a U.S. citizen living in Canada and you own a home (i.e. a non-U.S. situs property) in sole or joint name, you may benefit (for U.S. estate and income tax purposes) from gifting your portion of ownership in the home to your non-U.S. citizen spouse, especially if the value of the home has increased substantially and your intention is to eventually sell the home. For U.S. estate and U.S. gift tax purposes, the transfer made will be considered a taxable gift on the value that exceeds the annual exclusion. A gift of appreciated property by a U.S. person generally does not trigger income tax on the gain. You may use your lifetime gift tax exemption to minimize or eliminate the U.S. gift tax on the excess amount. If you pass away after the property is gifted to your spouse, it will generally not be included in determining your U.S. estate tax since you no longer own the property. From a U.S. income tax perspective, there may also be a benefit to gifting because a U.S. person who sells a principal residence has a limit on the amount of the gain triggered that may be excluded from U.S. income tax. Therefore, transferring ownership of a principal residence in Canada to a non-U.S. spouse who is also not a U.S. green-card holder or U.S. resident may remove the requirement to pay U.S. income tax altogether, which can result in overall tax savings for the couple, especially since the spouse may claim the principal residence exemption to avoid Canadian income tax on the sale.

Concerns with making larger gifts

Outright gifts received by your beneficiaries may be exposed to U.S. estate tax in their hands. Also, you may not be comfortable with the idea of making larger outright gifts and giving up control of a significant portion of your wealth. To address these concerns, you may consider making gifts to a "dynasty trust".

Dynasty trust

A dynasty trust (sometimes referred to as a generation-skipping transfer trust) is a special type of irrevocable trust. This trust may help maintain the amount of wealth that can be transferred from generation to generation by protecting its beneficiaries from U.S. estate tax on property transferred into the trust and future growth of the trust property.

The trust may also serve to protect the property from uncontrolled spending by your beneficiaries and may protect the property from your beneficiary's creditors and their spouses (in the case of matrimonial disputes). Probate tax and the associated estate administration delays generally don't apply to property in a dynasty trust.

A dynasty trust can be created during your lifetime as an inter-vivos trust or upon your death as a testamentary trust created by your Will. The individual or estate funding the trust may be subject to U.S. gift tax or U.S. estate tax.

Considerations for a dynasty trust

Similar to the CST, in order to provide U.S. estate tax protection, a beneficiary of a dynasty trust must not be given broad powers to access the trust property. Therefore, a beneficiary cannot be given a general power of appointment. The trust can provide limited powers that allow a beneficiary to request a trustee to distribute, annually, up to 5% of trust property or $5,000, whichever is greater. In addition, the beneficiary can be given the power to require trustees to make distributions of capital if they're made within "ascertainable standards" for health, education, support or maintenance. A beneficiary can be a trustee, provided that they're given only these limited powers. For greater flexibility, it's also possible to include an independent trustee that's not bound by the ascertainable standards provision for distributing additional capital to the beneficiaries.

In order for the settlor to avoid U.S. estate tax on property transferred to an inter-vivos trust, the settlor must not retain a life interest in the property transferred to the trust and the gift cannot be revocable. This means the settlor can't maintain a right to income, possession or enjoyment; the right to designate who will enjoy the property; or the right to take the property back. In addition, the settlor can't have the power to determine beneficial enjoyment of the trust property after the trust has been settled.

As a result, the settlor is generally not a beneficiary or trustee of the dynasty trust. However, it may be possible for the settlor to be a beneficiary if the trust is structured properly as a self-settled trust. Here, the settlor is one of a group of beneficiaries who typically comprises the settlor and their children and perhaps grandchildren.

Where protection from U.S. transfer tax is desired, certain precautions need to be taken when creating a self-settled trust. First, the settlor of the trust can't retain a life interest in the property of the trust. Second, the trust must be governed by the laws of a jurisdiction that permits self-settled trusts and allows these trusts to benefit from the U.S. "spendthrift trust" rules. The spendthrift rules protect the trust property from the creditors of the trust beneficiaries and ordinarily would not apply in the case of self-settled trusts. However, there are a number of foreign jurisdictions, as well as U.S. states, including Delaware, Alaska and Nevada, that have enacted exceptions for self-settled trusts to benefit from the U.S. spendthrift trust rules. Therefore, provided the settlor does not have a "right" to the trust property, it may be possible that they can enjoy the "use" of them. This can be a complicated distinction that requires very careful structuring and advice from a qualified cross-border tax and/or legal professional to be successful.

To maintain their lifestyles for the long term, settlors should also consider retaining sufficient property outside of the dynasty trust in their own name.

Dynasty trust setup

Dynasty trusts may be set up as U.S. trusts for U.S. beneficiaries living in the U.S. If the trust is considered U.S. resident and not Canadian resident, the assets in the trust will generally not be subject to the Canadian 21-year deemed disposition rules. However, the Canadian deemed disposition rule would continue to apply to Canadian real property and business property even if these properties are in a U.S. resident trust.

A dynasty trust set up as a U.S. trust may be deemed to be resident in Canada (i.e. a dual Canadian and U.S. resident trust). A dual Canadian and U.S. resident trust is subject to taxation in both Canada and the U.S. Fortunately, offsetting foreign tax credits to reduce or eliminate double taxation of income taxed in the trust may be available.

The Canadian income attribution rules must also be considered, which could attribute the income of the trust to the settlor when it's distributed to a beneficiary who's a minor or the settlor's spouse.

If the dynasty trust is set up as a U.S. trust, a U.S. beneficiary will avoid punitive U.S. income tax rules known as the "throw-back rules" that apply to "foreign non-grantor trusts" as well as the annual reporting rules relating to foreign trusts. In simplified terms, the throw-back rules apply to U.S. beneficiaries of a foreign non-grantor trust on distributions of accumulated income (i.e. income of the trust that's accumulated and distributed in a different calendar year).

In general, a foreign non-grantor trust is a non-U.S. trust with beneficiaries where the settlor or transferor of property is not a U.S. person. If the non-U.S. grantor (settlor or transferor) can revest title to the property to himself/herself or the only beneficiaries of the trust during the grantor's life is himself/herself or the spouse, the trust would be considered a grantor trust. The throw-back rules generally do not apply to a grantor trust.

When the U.S. throw-back rules do apply to distributions of accumulated income of a non-grantor trust to a U.S. beneficiary, the accumulated income and capital gains distributed are taxed at the beneficiary's marginal U.S. tax rate (i.e. the income does not retain its character and does not benefit from potentially lower tax rates). An interest charge is also applied on the tax owed because U.S. tax was not paid during the period the income was accumulating in the trust. The U.S. beneficiary can claim a foreign tax credit for any Canadian or other foreign income taxes paid on the income accumulated.

In comparison, a foreign grantor trust is a non-U.S. trust where the settlor or transferor of property to the trust is treated as the owner of the property. As a result, the settlor is taxed on the income earned by the trust annually (whether or not the income is distributed from the trust to a beneficiary).

While property that remains in a dynasty trust is protected from U.S. estate tax, income earned in a U.S. resident non-grantor trust is still subject to U.S. income tax. The trustee must decide whether the income remains in the trust and is taxed in the trust or is distributed to a beneficiary and taxed in their hands.

Also, while the U.S. income tax rates that apply to income taxed in the trust or in a U.S. beneficiary's hands are similar, the tax brackets for income taxed in the trust are much more compressed as compared to those for an individual. This may result in a larger U.S. income tax liability if income is taxed in the trust.

For Canadian tax purposes, a dynasty trust set up to include current beneficiaries other than a spouse cannot be a qualifying Canadian testamentary spousal trust. Therefore, the transfer of property to a dynasty trust by a resident of Canada is subject to the Canadian deemed disposition tax rules, which would trigger Canadian tax on accrued capital gains.

Potential alternatives to a dynasty trust

Upon your passing, an alternative to transferring property to a dynasty trust would be to transfer it to a CST or to a qualifying Canadian testamentary spousal trust.

Your children and grandchildren can be successive beneficiaries of the capital of a CST or spousal trust, which can be transferred to a dynasty trust once the surviving spouse dies. However, if your wish is that your children and grandchildren benefit from your estate prior to the death of your surviving spouse, you may provide for them through outright distributions from your estate or allocate a portion of your estate to a dynasty trust.

U.S. citizens or U.S. domiciliary funding a dynasty trust

U.S. gift tax, estate tax or GSTT may be triggered on gifts or bequests made to a dynasty trust. These taxes may be reduced or eliminated by using your lifetime gift tax, estate tax and GSTT exemptions.

As a U.S. citizen or U.S. domiciliary, for 2026, you can transfer US$15 million to a dynasty trust without triggering U.S. gift tax or U.S. GSTT by using your lifetime gift tax exemption, assuming you made no prior taxable gifts. Using your lifetime gift tax exemption to transfer property to the trust during your lifetime can maximize the amount of property that's protected from U.S. estate tax. This is because any future growth of the property while in the trust is also protected. If your net worth is close to or exceeds the exemption, you can potentially protect a greater amount of property from U.S. estate tax if you transfer the property to the trust during your lifetime.

If you wait until your death and the property has continued to grow in value, the maximum that can be transferred and protected is limited to your U.S. estate tax exemption. Any excess wealth, including any growth, will be exposed to U.S. estate tax and potentially the U.S. GSTT.

It may also be possible to fund the trust with your annual gift and GSTT exclusion. However, this can be complex, since the annual gift tax exclusion can only be used for a gift to a beneficiary that's a "present interest". Since a gift to a trust is a future interest, the annual exclusion does not apply. However, the gift to a trust can qualify as a present interest if the beneficiaries are provided a power to withdraw the funds contributed to the trust. A gift of a present interest to a trust is discussed in more detail later in the irrevocable life insurance trust (ILIT) section.

If you or the beneficiaries are residents of Canada, the Canadian tax implications discussed earlier must also be considered.

Non-U.S. person funding a dynasty trust

As a non-U.S. person, you can fund a dynasty trust during your lifetime without incurring U.S. gift tax or U.S. GSTT (provided the property gifted is not U.S. tangible property). You may also choose to set up a dynasty trust through your Will.

Where your beneficiaries reside in the U.S., there may be benefits to funding a dynasty trust that's resident in the U.S. upon your death instead of during your lifetime. This is because the trust will not be a deemed Canadian trust. As a U.S. trust, the trust assets (other than Canadian real property or Canadian business property) will generally not be subject to the Canadian 21-year deemed disposition rules.

Irrevocable life insurance trust (ILIT)

When a U.S. or non-U.S. person, who's the life insured on a policy, dies owning the policy outright or having "incidents of ownership" in the policy, the death benefit paid will be included in their worldwide estate value for purposes of determining U.S. estate tax. Incidents of ownership may result from having the ability to name or change beneficiaries, borrow against the policy, access the cash value and assign or cancel the policy.

For a U.S. citizen or U.S. domiciliary, the death benefit is subject to U.S. estate tax. For non-U.S. persons who are Canadian residents, the death benefit reduces the amount of the unified credit that may be claimed to minimize their U.S. estate tax liability.

Specific considerations for an ILIT

To minimize exposure to U.S. estate tax, an ILIT may be set up during your lifetime, which is structured to have ownership of the life insurance policy. While the life insured can't be the trustee of the ILIT without creating incidents of ownership, they can contribute cash to the ILIT in order to fund the purchase of the life insurance policy.

There may be other ways to structure the ownership of life insurance in order to reduce your exposure to U.S. estate tax; however, the ILIT may prove to be a more appropriate structure to use. For example, having your spouse own the life insurance policy where you're the insured may reduce your exposure to U.S. estate tax. However, if your spouse owns the policy and predeceases you, the policy will need to be transferred to someone other than yourself and this may trigger income tax. Also, if you provide your spouse, who will own the policy, with the funds to facilitate the purchase of the policy, you may be considered to have incidents of ownership in the policy.

If a corporation owns the policy, exposure to U.S. estate tax still exists if the life insured has ownership in the corporation. For example, if the life insured is a U.S. citizen who owns more than 50% of the corporation's shares, it is possible they will be considered to have incidents of ownership in the policy and will be required to include the value of the death benefit in their worldwide estate. Even where ownership in the corporation is less than 50%, the value of the life insured's shares is increased by the proportionate amount of the death benefit paid to the corporation.

The use of an ILIT may avoid these issues and provide protection against U.S. estate tax exposure for both U.S. and non-U.S. persons who are the life insured on the policy. When the death benefit is paid into the ILIT upon your death, it can be accessed to pay your estate taxes or other tax liabilities by having the ILIT loan the funds to your estate, or it can purchase your estate property.

Note that contributions made by a U.S. citizen to the ILIT may be subject to U.S. gift tax or U.S. GSTT. This is because generally, a transfer to a trust provides a "future interest" for a beneficiary and therefore, the transferor would not qualify to claim the annual gift tax exclusions. However, if the gifts are made to the trust to provide the beneficiary with a "present interest" in the amount of the gift, the annual gift and GSTT exclusions may be claimed. Having a present interest means that beneficiaries must have the right to withdraw the funds contributed to the trust at the time of contribution. This right is referred to as a "Crummey Power". The Crummey Power can be limited to a period of time, such as 30 days. However, if limited, the amount of the annual exclusion would be reduced. A non-U.S. person is not subject to U.S. gift tax on property other than U.S. tangible property. Therefore, they can fund the ILIT with an unlimited amount of non-U.S. tangible property without incurring U.S. gift tax or U.S. GSTT and would not require the trust to include a Crummey Power.

If you already own a life insurance policy where you're the insured, it is possible to transfer it to an ILIT. However, keep in mind that transfers made within three years of your death will still result in the death benefit being included in your worldwide estate and there is a potential for U.S. gift tax and U.S. GSTT.

Other issues to consider

For Canadian tax purposes, the transfer of an existing life insurance policy to an ILIT will trigger a deemed disposition of the policy at FMV, which may result in Canadian tax (the gain, calculated as the FMV less the ACB of the policy, is taxable as income). During the life of the insured, the 21-year deemed disposition rule does not apply to a life insurance policy owned by a trust; however, it will apply to other property that may be owned by the trust.

If there's the potential that the policy will be required for investment or retirement purposes, an ILIT may not be appropriate. This is because access to the cash surrender value and borrowing against the policy is not permitted.

When a Canadian insurance policy is issued on the life of a U.S. citizen by a Canadian insurance provider, U.S. excise tax of 1% of the gross amount of the insurance premiums may be required to be remitted to the U.S. Also, a Canadian insurance policy must meet the U.S. definition of a life insurance policy and must avoid the U.S. "modified endowment contract" rules and the "transfer for value" rules in order to be considered an exempt policy under U.S. tax laws. A discussion of these rules is beyond the scope of this article.

You should contact a qualified cross-border professional for advice on whether to incorporate the use of life insurance in your estate planning. They can help you understand the Canadian and U.S. tax implications and provide advice as to whether a reduction of your exposure to U.S. estate tax using an ILIT outweighs the costs of setting one up and the annual fees associated with maintaining it. You should also speak with a licensed life insurance representative for information regarding your insurance needs.

Dynasty ILIT

It may be possible to reduce your and your heir's exposure to U.S. estate tax even further by structuring an ILIT as a dynasty trust. The dynasty ILIT allows you to reduce your own exposure to U.S. estate tax and protect the property in the trust and future growth from U.S. estate tax for your spouse, children, and successive generations.

Charitable donations

Charitable donations made during your lifetime or through your Will may reduce your exposure to U.S. estate tax. For example, a U.S. citizen can make charitable gifts, which are not subject to U.S. gift tax, to reduce the amount of property in their estate. They can also make charitable bequests, which results in a deduction against the value of the taxable estate in calculating their U.S. estate tax liability. The charitable gifts or bequests must be made to qualified U.S. or foreign charities. A non-U.S. person may do the same, but to reduce the value of their taxable estate, they must donate U.S. situs property and the gifts or bequests must be made to U.S. qualified charities.

Under the Treaty, contributions made by a U.S. citizen or resident to a Canadian registered charity generally qualify as charitable contributions for U.S. income tax purposes. However, charitable deduction on your U.S. income tax return is subject to certain restrictions, various percentage limitations based on your adjusted gross income depending on the type of donation, and you must generally have Canadian source income to claim a deduction for contributions made to a Canadian charity. These rules are complex so you should review your philanthropy plans with a qualified cross-border accountant.

For Canadian tax purposes, a donation tax credit for gifts made to U.S. qualified charities may only be claimed against U.S. source income. However, a donation credit for gifts made to a qualified university in the U.S. or to a U.S. charitable organization to which the Government of Canada has made a gift may be claimed against Canadian sources of income.

Planning for the future

When you're creating an estate plan for U.S. citizens in Canada, you must take into consideration both Canadian and U.S. tax laws. When some of the members of your family are not U.S. citizens, the planning is even more complex. This article has presented some of the common cross-border estate planning strategies that may be considered to reduce U.S. estate tax exposure for you and your beneficiaries.

It's important to review your estate plans on a regular basis to help ensure they still meet your needs and intentions and to account for any changes to legislation. While the currently enacted exemptions for gift tax, estate tax and GSTT exemptions are permanent and provide some degree of certainty, it's impossible to know whether these exemption amounts may be changed by future governments. Therefore, your estate plans should be flexible, allowing for adjustments to be made when necessary due to shifting circumstances.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

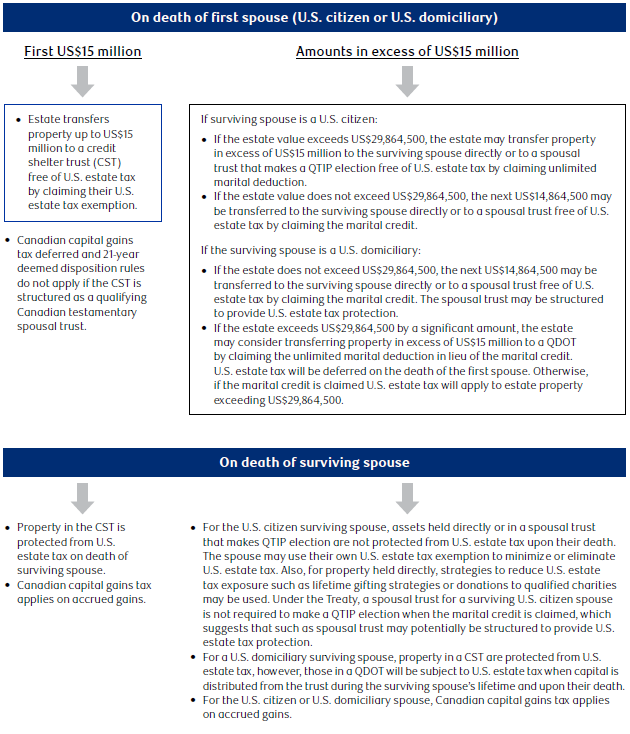

Appendix 1 – Estate planning for spouses who are U.S. citizens or U.S. domiciliaries and one survives the other

Estate planning for spouses who are U.S. citizens or domiciliaries may involve structuring their Wills to contain provisions for the creation of a credit shelter trust (CST) and other trusts such as a QTIP spousal trust in the case of a surviving U.S. citizen spouse or a QDOT in the case of a surviving U.S. domiciliary spouse. Each of these trusts may be structured as a qualifying Canadian testamentary spousal trusts to defer immediate Canadian taxation on the death of the first spouse.

On the death of the first spouse, the transfer of property to a CST will be subject to U.S. estate tax; therefore, only the value up to the deceased's available U.S. estate tax exemption, which would offset the liability, should be transferred. The maximum U.S. estate tax exemption for deaths in 2026 amounts to US$15 million worth of property for U.S. citizens or U.S. domiciliaries, which equates to a unified credit of US$5,945,800. Therefore, there is no U.S. estate tax on the first US$15 million of taxable estate property transferred to the CST. The surviving spouse is protected from U.S. estate tax on the property that remains in the CST upon the surviving spouse's death including any growth of this property. This protection is not available if the property is transferred to the spouse directly.

For property in excess of the estate tax exemption of US$15 million, the options for the estate of the first spouse to die will depend on whether the surviving spouse is a U.S. citizen or U.S. domiciliary.

When the surviving spouse is a U.S. citizen

If the surviving spouse is a U.S. citizen, the estate of the first spouse to pass away may claim an unlimited marital deduction on property in excess of US$15 million that are transferred directly to the surviving U.S. citizen spouse or to a spousal trust for their benefit, provided the spousal trust makes a QTIP election.

The QTIP election provides the surviving U.S. citizen spouse with a lifetime income interest in the property of the spousal trust. It requires that the annual income of the spousal trust be paid to them annually and that they be the only beneficiary that can access the capital during their lifetime. With a QTIP spousal trust, the value of the property in the trust is included in determining the U.S. estate tax liability of the surviving U.S. citizen spouse upon their death. However, the surviving spouse may use their own U.S. estate tax exemption to minimize or eliminate the U.S. estate tax liability. Where the value of the surviving spouse's estate will exceed their U.S. estate tax exemption, the surviving spouse may consider strategies to reduce their exposure to U.S. estate tax such as making lifetime gifts to family or charitable gifts or bequests.

If all the property of the estate of the first spouse to pass away does not exceed US$29,864,500, their estate may choose to claim the marital credit in lieu of the unlimited marital deduction. The marital credit essentially doubles the unified credit of the first spouse to die, and this allows for another US$14,864,500 (i.e. US$5,945,800 divided by 40% maximum U.S. estate tax rate) worth of property to be transferred free of U.S. estate tax to the surviving spouse in addition to the US$15 million transferred to the CST. Theoretically, under the Treaty, a spousal trust for a surviving U.S. citizen spouse is not required to make a QTIP election when the marital credit is claimed, which suggests that the spousal trust could be structured to provide U.S. estate tax protection (i.e. wording in the U.S. Treasury Department's technical explanations to the Treaty indicates that the spousal trust is not required to make a QTIP election even if the trust is structured to provide U.S. estate tax protection to the surviving spouse).

As a summary, upon the surviving spouse's death, the US$15 million in the CST and any future growth is protected from U.S. estate tax. If the US$14,864,500 of excess property is held directly or in a QTIP spousal trust, the surviving spouse may use their own U.S. estate tax exemption to minimize or eliminate the U.S. estate tax liability. If the US$14,864,500 of excess property is transferred to a spousal trust, since the Treaty allows a marital credit the property in the trust may be protected from U.S. estate tax.

When the surviving spouse is a U.S. domiciliary

If the surviving spouse is a U.S. domiciliary, the first spouse to pass away may claim the marital credit on next US$14,864,500 of estate property. This allows the first spouse who passes away to transfer up to US$29,864,500 free of U.S. estate tax for the benefit of the surviving spouse with the first US$15 million to the CST and the next US$14,864,500 to a spousal trust that may be structured to provide U.S. estate tax protection to the surviving spouse.

If the estate of the first spouse exceeds US$29,864,500, the excess will be subject to U.S. estate tax. If the estate tax is significant and the surviving spouse has a long-life expectancy, the estate may consider, in lieu of claiming the marital credit, transferring the property in excess of US$15 million to a QDOT, in order to defer U.S. estate tax. The deferral lasts until capital is distributed from the trust or the surviving spouse dies. When the deferral ends the U.S. estate tax liability is calculated based on the estate tax rates that existed on the death of the first spouse based on the property in the QDOT including growth of the property. Note that the estate tax exemption available to the estate of the surviving spouse upon their death can't be used to minimize or eliminate the U.S. estate tax liability incurred on property from the QDOT.

When there are U.S. citizen or domiciliary children and grandchildren

U.S. citizen or U.S. domiciliary children and grandchildren can be provided for with successive trusts created upon the death of the surviving spouse. If your wish is that they benefit from your wealth prior to the death of your surviving spouse, you could provide for them with separate distributions upon your death or during your lifetime. These distributions can be made to them outright or to separate trusts (e.g. dynasty trusts). You may be subject to U.S. estate tax if the transfer occurs upon your death and U.S. gift tax, if it occurs during your lifetime. The cost base of the property that transfers upon your death is adjusted to fair market value (FMV). Those gifted during your lifetime transfer at your cost base (subject to a possible increase in the cost base by some or all of any U.S. gift tax incurred) resulting in the accrued gains being taxable for U.S. income tax purposes to your beneficiaries if they sell the property.

Dynasty trusts set up as U.S. trusts (or dual resident trusts, if the U.S. beneficiaries reside in Canada) may be more appropriate than setting up Canadian testamentary trusts. This is because U.S. beneficiaries of Canadian testamentary trusts may be subject to the adverse U.S. throw-back rules if income earned in the trust is not distributed annually. While you can make annual distributions to avoid these rules, this may result in the accumulation of property that the beneficiaries are not able to use up during their lifetime, which may be exposed to U.S. estate tax.

For Canadian tax purposes, the transfer of property to a dynasty trust will trigger the deemed disposition rules, which results in you realizing any accrued gains on the property. The Canadian tax may be minimized or offset by claiming a foreign tax credit for U.S. estate tax incurred. The cost base of the property transferred to the dynasty trust is adjusted to FMV. For gifts made during your lifetime, the transfer also triggers a deemed disposition and Canadian income attribution rules may also apply to income earned on the property gifted.

For purposes of the dynasty trust, where you have beneficiaries living in the U.S. and you structure the dynasty trust as a U.S. resident trust, the 21-year deemed disposition rule that applies to Canadian trusts may be avoided, except for certain types of Canadian property such as Canadian real property. If the beneficiaries are residents of Canada, the dynasty trust may be deemed to be a Canadian resident trust under the Canadian non-resident trust rules notwithstanding the fact that it may also be considered a U.S. resident under U.S. tax laws. These trusts will be subject to the 21-year deemed disposition rule. Whether the trust is resident in Canada or deemed resident in Canada, foreign tax credits may be claimed in Canada for U.S. income tax paid, which may minimize the possibility of double taxation.

The following diagram illustrates the potential estate planning that may be implemented when the spouses are U.S. citizens or U.S. domiciliaries.

This example assumes the first spouse dies in 2026 and qualifies for the maximum U.S. estate tax exemption of US$15 million.