Estate Planning for your RRSP/RRIF

Estate planning is important so that you can retain more of your assets, protect your estate and leave a lasting legacy for your family. You may have an RRSP/RRIF that's a significant part of your wealth; with that in mind, it should be properly accounted for in your estate plan. This article discusses some of the advantages and disadvantages of naming one or more beneficiaries of your registered retirement savings plan (RRSP) or registered retirement income fund (RRIF) and the tax implications for these plans at death.

Estate planning is important so that you can retain more of your assets, protect your estate and leave a lasting legacy for your family. You may have an RRSP/RRIF that's a significant part of your wealth; with that in mind, it should be properly accounted for in your estate plan. This article discusses some of the advantages and disadvantages of naming one or more beneficiaries of your registered retirement savings plan (RRSP) or registered retirement income fund (RRIF) and the tax implications for these plans at death.

Family Office Services

July 14, 2024

Estate Planning for your RRSP/RRIF

Estate planning is important so that you can retain more of your assets, protect your estate and leave a lasting legacy for your family. You may have an RRSP/RRIF that's a significant part of your wealth; with that in mind, it should be properly accounted for in your estate plan. This article discusses some of the advantages and disadvantages of naming one or more beneficiaries of your registered retirement savings plan (RRSP) or registered retirement income fund (RRIF) and the tax implications for these plans at death. Beneficiary designations discussed in this article include:

- Designating your spouse

- Designating your child or grandchild

- Designating a third party

- Designating a non-resident

Taxation of your RRSP/RRIF at death

As a general rule, when you pass away, the fair market value (FMV) of your RRSP/RRIF is included as income on your final tax return and taxed at your marginal rate. Any income earned in your RRSP/RRIF after the date of death and until December 31 of the year after the year of death (the exempt period) will be taxed in the hands of the beneficiary named on your plan or your estate (if there's no named beneficiary) in the year on the plan as income in the year it's paid. The taxation of any income earned in your RRSP/RRIF after the exempt period is as follows:

- If you have a depositary RRSP/RRIF, the income earned after the exempt period will be taxed to the beneficiary or the estate (if there's no named beneficiary) in the year it's credited or added to the deposit.

- If you have a trustee RRSP/RRIF, some of the income earned after the exempt period will be taxable to the RRSP/RRIF trust annually. The remaining income will be taxable to the beneficiary or the estate (if there's no named beneficiary) in the year it's paid out, to the extent that the funds have not been included in the RRSP/RRIF trust's income in a previous year.

- Finally, if you have an insured RRSP/RRIF, the income earned after the exempt period is taxable to the beneficiary or the estate (if there's no named beneficiary) in the year that it's paid out.

There are exceptions to these rules when you designate certain persons as the beneficiary of your plan. In these circumstances, the tax on your RRSP/RRIF proceeds may be deferred and/or taxed in your beneficiary's hands. These exceptions are discussed in the following sections.

How to designate a beneficiary

In all common law provinces and territories, you may designate a beneficiary of your RRSP/RRIF by naming them on the plan documentation or in your Will. If you live in Quebec, you cannot name a beneficiary on your plan documentation, you must do so in your Will. If you are able to name a beneficiary on the plan documentation, this may simplify the tax reporting and minimize probate taxes. You may also be able to minimize probate taxes by naming a beneficiary in the non-dispositive section of your Will. The non-dispositive section is outside the body of the Will. Please consult your qualified legal advisor if you're considering making a beneficiary designation in your Will.

If you name a beneficiary on your plan documentation, it's important to ensure the designation is consistent with any designation you may have made in your Will. In general, if there's a conflict between the designation on your plan and the designation in your Will, the later designation revokes the earlier one.

It's important to note that if the financial institution holding your plan is unaware of a later designation you may have made in your Will, when you pass away, the institution will pay the assets directly to the beneficiary named on the plan. This could lead to conflicts between your heirs who may seek legal remedies and incur unnecessary expenses.

Designating your spouse

You may choose to name your spouse as a beneficiary of your RRSP/RRIF. For your RRIF, you're also given the option of naming your spouse as the successor annuitant. A spouse can be a legally married spouse or a common-law partner.

Your spouse as beneficiary

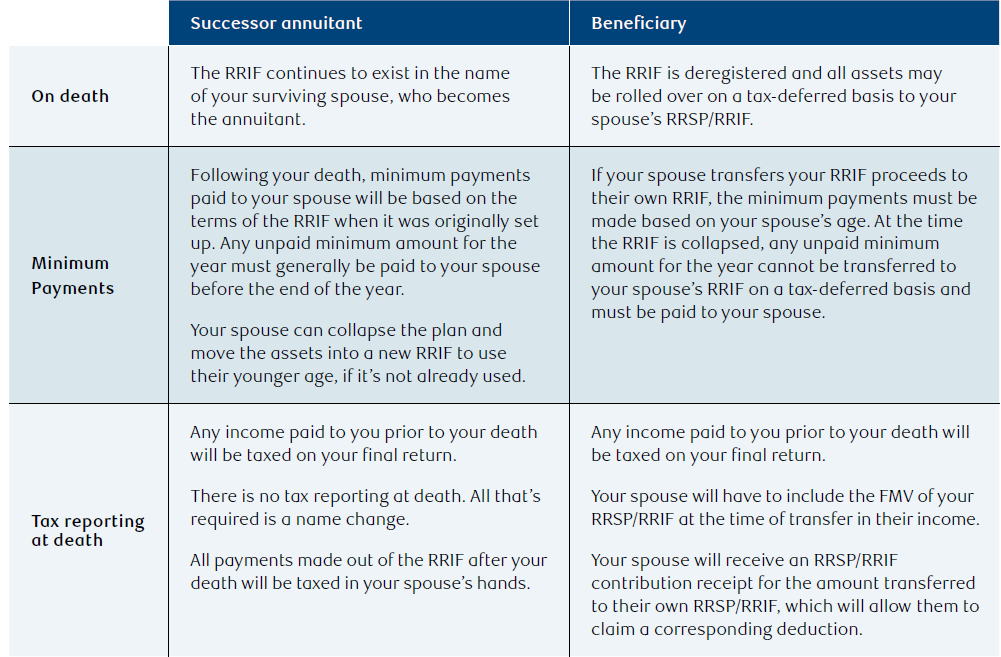

When you designate your spouse as the sole beneficiary on the plan documentation, your RRSP/RRIF will be wound up on your death and your spouse may transfer the plan assets directly to their RRSP/RRIF as a tax-deferred rollover. If your spouse transfers the plan assets to their RRSP, they must be 71 years of age or under at the end of the year the transfer is made. Alternatively, your spouse may transfer the funds from your RRSP/RRIF directly to an issuer to purchase an eligible annuity. In each of these cases, the tax on the amount transferred is deferred until your spouse withdraws the money from their RRSP/RRIF, receives a payment from the annuity or passes away. Your spouse must make these direct transfers by December 31 of the year following the year of your death. If these conditions are met, you will not receive any tax slips for the FMV of your RRSP/RRIF at the date of death. Your spouse will receive a tax slip for the amounts transferred, which they will need to include in their income for the tax year in which the transfer was made. They are generally able to claim an offsetting deduction, so no tax is payable on these funds.

It's important to note that if your spouse does not transfer the funds from your RRSP/RRIF to their own RRSP/RRIF or use the funds to purchase an eligible annuity by December 31 of the year following the year of death, or is not named as sole beneficiary of your RRSP/RRIF on the plan documentation, they may still be able to defer the tax on some or all of the RRSP/RRIF proceeds to which they are entitled. However, they will not be able to directly roll over these funds to their own RRSP/RRIF or to an issuer to purchase an eligible annuity, and the tax reporting for both you and your spouse will be much more complex.

If your RRIF is closed in the year of death, and the RRIF minimum payment for the year was not made to you before death, it will need to be paid as income to your spouse that year. The minimum payment is not eligible for the tax-deferred rollover. If your RRIF is closed in the year following death, the minimum amount for that year will be paid as income to your spouse and will also not be eligible for the tax-deferred rollover. It may not be necessary to catch up on any unpaid minimum for the year of death.

There is no requirement for your spouse to transfer all of the RRSP/RRIF proceeds into their own RRSP/RRIF or to an issuer to buy an eligible annuity. In fact, there are certain situations in which it may make sense for your spouse not to do a direct transfer and to instead receive the RRSP/RRIF proceeds outright.

For example, if your spouse has an immediate need for cash or does not need further retirement savings, they may want to receive the plan proceeds directly. In addition, for tax purposes, if you have minimal income in the year of death or have unused losses carried forward from prior years, it may make sense for your spouse not to do the direct transfer. In these circumstances, your legal representative can choose the amount of the RRSP/RRIF proceeds to be taxed on your final tax return or in your spouse's hands. Please refer to Appendix A for a more detailed discussion of the tax reporting options available to your legal representative.

Where there is no beneficiary named on the plan documentation, or your estate is named as the beneficiary and your spouse is beneficially entitled to some or all of the RRSP/RRIF proceeds under your Will or provincial or territorial intestacy laws, there may still be an opportunity for them to transfer these proceeds into their RRSP/RRIF or to an issuer to purchase an eligible annuity on a tax-deferred basis. The ability to do so is dependent on the powers granted to the legal representative. Please refer to Appendix A for a more detailed discussion of the tax reporting options available to your legal representative and beneficiary.

There may also be an opportunity for tax deferral if some or all of your RRSP/RRIF proceeds pass to a lifetime benefit trust (LBT) set up under your Will for the benefit of your mentally infirm spouse. More details on LBTs can be found later on in this article.

Your spouse as successor annuitant

You are given the additional option of naming your spouse (and only your spouse) as the successor annuitant of your RRIF. When you name your spouse as a successor annuitant, your RRIF continues to exist after your death and your spouse becomes the annuitant. As such, administratively, it's much easier to transfer your RRIF to your spouse by designating them as a successor annuitant rather than a beneficiary. All payments made out of the RRIF after your death are taxed in your spouse's hands.

If you do not end up designating your spouse as a successor annuitant prior to your death, it may still be possible for your spouse to become the successor annuitant after you pass away. This may be the case, for example, where there is no named beneficiary on the plan, and your spouse is beneficially entitled to the RRIF proceeds under your Will or provincial or territorial intestacy laws. Your legal representative will need to consent to the designation and your financial institution will also need to agree. Please refer to Appendix B for a summary of the differences between appointing your spouse as a beneficiary or a successor annuitant of your RRIF.

If your RRIF minimum payments were based on your age, and you have a younger surviving spouse, your spouse will be able to collapse the RRIF and open a new one with payments based on their age. This will reduce the minimum payment they're required to receive each year.

Designating your child or grandchild

If you name your child or grandchild as the beneficiary of your RRSP/RRIF, the FMV of the plan at the date of death will generally be included on your final tax return. This rule is subject to certain exceptions.

Financially dependent child or grandchild

If your child or grandchild is financially dependent on you, regardless of their age, the FMV of your RRSP/RRIF on death can either be taxed in your beneficiary's hands or on your final tax return. This allows for a redistribution of some or all of your income to your child or grandchild who receives the funds. In a case like this, since your beneficiary likely has minimal income, this is generally advantageous.

In order for your child or grandchild to be considered financially dependent on you, they must have lived with you and depended on you prior to your death. As well, their net income for the year before your death must have been less than the basic personal exemption for that year. If your child or grandchild suffers from a mental or physical disability, their net income for the year before death must have been less than the basic personal exemption plus the disability amount for that year. If your child or grandchild's net income is above these thresholds, they may still be considered financially dependent if they can prove their dependency with facts and circumstances.

Aside from being able to minimize the tax burden on your death, if you name your financially dependent child or grandchild as the beneficiary of your RRSP/RRIF, it may be possible to defer the taxation of your RRSP/RRIF if your beneficiary is a minor or has a disability.

Minor child or grandchild

If you designate your financially dependent minor child or grandchild as beneficiary of your RRSP/RRIF, the funds in your plan can be used to purchase a term-certain annuity. The payments from the annuity must start no later than one year after the purchase and all payments must be made to your minor beneficiary by the end of the year they turn 18.

Your child or grandchild will pay tax on the annual annuity payments at their marginal tax rate in the year they receive the payment. Since your child or grandchild likely has nominal income, this can minimize the overall taxes payable on your RRSP/RRIF proceeds. Also, since the taxation of your RRSP/RRIF proceeds can be spread over a number of years, this provides for a tax-deferral opportunity.

If you do not name your financially dependent minor child or grandchild as a beneficiary of your RRSP/RRIF on the plan documentation, but they are a beneficiary of your estate and are beneficially entitled to some or all of the RRSP/RRIF proceeds, there may still be an opportunity to defer the tax. Please refer to Appendix A for a more detailed discussion of the tax reporting options available to your legal representative and beneficiary.

Leaving property to a minor

If you name your financially dependent minor child or grandchild as beneficiary of your RRSP/RRIF, provincial or territorial laws that govern minor children's property may prevent them from directly receiving the RRSP/RRIF proceeds. This is because a minor child does not have the legal capacity to receive the RRSP/RRIF proceeds paid to them as beneficiary or provide a valid discharge to the financial institution administering the RRSP/RRIF.

Depending on the value of your RRSP/RRIF on death and the applicable provincial or territorial laws, the RRSP/RRIF proceeds will generally need to be paid to a parent on behalf of the minor child or grandchild, a court appointed guardian of property for the minor child or grandchild, the Public Guardian or Trustee, or into court. For example, in Ontario, if you name a minor child or grandchild as the beneficiary of your RRSP/RRIF, and the value of your plan on death exceeds $35,000, the proceeds will either need to be paid into court and held there until your beneficiary turns 18 or to a court appointed guardian of property for your minor child or grandchild.

If the RRSP/RRIF proceeds must be paid into court, there will be limited access to these funds until your child or grandchild reaches the age of majority. As well, the opportunity to defer the taxation of the RRSP/RRIF over a number of years may be lost, as the court may not be willing to purchase an annuity for your minor child or grandchild.

Applying to the court to be appointed as guardian of the minor child or grandchild's property can also be a time-consuming and expensive process. Consider whether the potential probate and tax savings associated with naming your minor child or grandchild as the beneficiary of your RRSP/RRIF outweigh the costs and complexities involved with a guardianship application.

To avoid having a guardian of property appointed for your minor child or grandchild or having the RRSP/RRIF proceeds paid into court, you may choose to name your estate as the beneficiary of your RRSP/RRIF. In this case, with proper planning, your RRSP/RRIF proceeds may pass to a testamentary trust created under your Will for the benefit of your minor child or grandchild. If you set up a trust in your Will, you can specify the timing of the gift or define the precise circumstances in which your child or grandchild will receive the funds. This will help ensure the RRSP/RRIF proceeds are paid to your child or grandchild at an age when they are more mature and able to handle this inheritance responsibly.

You should note that by utilizing this strategy, you may forgo the probate and tax savings that result from naming your minor child or grandchild as the beneficiary of your RRSP/RRIF. Your RRSP/RRIF will generally be subject to probate. As well, the FMV of your RRSP/RRIF as of the date of death will likely need to be included on your final tax return. However, if the testamentary trust is properly structured and the RRSP/RRIF proceeds are used to purchase a term-certain annuity to age 18, there may be an opportunity to defer the taxes on your RRSP/RRIF.

You should seek the advice of a qualified legal advisor in your province or territory of residence before naming a minor beneficiary for your RRSP/RRIF.

Child or grandchild with a disability

If you name your financially dependent child or grandchild who is dependent on you because of a physical or mental disability as the beneficiary of your RRSP/RRIF, they can transfer your RRSP/RRIF proceeds to their own RRSP/RRIF. They can also use the proceeds to purchase an annuity, regardless of their age. These options effectively defer taxation of your RRSP/RRIF until your child or grandchild withdraws the funds from their RRSP/RRIF, receives a payment from the annuity or passes away. Please note that this planning may still be possible if your financially dependent disabled child or grandchild is entitled to some or all of the RRSP/RRIF proceeds through your estate. Please refer to Appendix A for a more detailed discussion of the tax reporting options available to your legal representative and beneficiary.

Also, if your child or grandchild is dependent on you because of a mental disability, it may only be possible to implement this type of planning (as well as other planning opportunities discussed later) if the child has a power of attorney for property (protection mandate in Quebec) or court appointed guardian of property.

Before designating your disabled child or grandchild as a beneficiary of your RRSP/RRIF, consider the negative effects it may have on their eligibility for provincial or territorial disability-related income support payments. Disability-related income support programs generally stipulate income and asset limits for individuals who receive these benefits. These income and asset limits are generally quite low. Leaving even modest RRSP/RRIF assets to your disabled beneficiary upon your death could jeopardize their entitlement to receive support payments going forward.

Transfers to a registered disability savings plan (RDSP)

If your financially dependent child or grandchild is a beneficiary of, or is eligible to open, an RDSP upon your death, they can roll over the RRSP/RRIF proceeds they receive to their RDSP on a tax-deferred basis. This option may preserve your child's or grandchild's entitlement to government disability-related income support. All provincial and territorial disability support programs fully or partially exempt an RDSP as an asset and income. In addition, your beneficiary will only be taxed on the funds at their marginal tax rate once they withdraw them from their RDSP, which in most cases, is spread over a number of years. This may both minimize and defer the overall taxes paid on your RRSP/RRIF proceeds. Please note that this planning may still be possible if your financially dependent disabled child or grandchild is entitled to some or all of the RRSP/RRIF proceeds through your estate. Please refer to Appendix A for a more detailed discussion of the tax reporting options available to your legal representative and beneficiary.

To be eligible for the rollover, your beneficiary must be age 59 or under at the end of the calendar year in which the contribution of the RRSP/RRIF proceeds is made to the RDSP. The contribution of the RRSP/RRIF proceeds to the RDSP is not eligible for any government grants.

Your beneficiary can only roll over an amount to their RDSP to the extent of their available maximum lifetime contribution limit of $200,000. Consideration should be given to any contributions or transfers that were previously made to the beneficiary's RDSP since these will count towards their lifetime contribution limit. If the RRSP/RRIF proceeds exceed your beneficiary's contribution limit, they can transfer the remaining RRSP/RRIF proceeds to their own RRSP/RRIF or to an issuer to purchase an eligible annuity on a tax-deferred basis. If they don't choose one of these options, your legal representative can choose to tax any RRSP/RRIF proceeds above the amount transferred to the RDSP on your final tax return or in your beneficiary's hands in order to minimize the tax burden. That said, any amount your disabled child or grandchild receives from your RRSP/RRIF that's not contributed to their RDSP could still affect any provincial or territorial benefits they may be receiving.

If you have significant funds that you wish to provide to your disabled beneficiary, there are other planning opportunities available to ensure you do not jeopardize their government disability-related income support payments. These planning opportunities are discussed in the following sections.

Other planning opportunities

Henson Trust

Consider having your RRSP/RRIF assets flow to your estate and setting up an absolute discretionary trust for your disabled child or grandchild in your Will. This type of discretionary testamentary trust is often referred to as a Henson Trust. Under the terms of a Henson Trust, the trustee has the absolute discretion to distribute income and capital from the trust to your beneficiary as they see fit. The beneficiary has no vested interest in the income or capital of the trust and cannot claim or demand payments from the trust. As a result, many government disability-related income support programs do not consider this type of trust to be an asset of the beneficiary and may not jeopardize your beneficiary's entitlement to this support.

Before utilizing this estate planning tool, it's important that you consult with a qualified legal advisor to determine whether an interest in a discretionary trust is excluded for the purposes of determining your beneficiary's eligibility for provincial or territorial disability-related income support. For more information, please ask your RBC advisor for an article on Henson Trusts.

Lifetime benefit trust (LBT)

If your child or grandchild is financially dependent on you because of a mental impairment (not physical impairment), it may be possible to defer the tax on your RRSP/RRIF proceeds by having them pass to an LBT set up under your Will for the benefit of your child or grandchild.

An LBT is a personal trust under which a mentally infirm spouse of the deceased or a child or grandchild of the deceased who was financially dependent on the deceased because of mental impairment is the only person entitled to receive or use any of the income or capital of the trust during their lifetime. The trustee(s) of an LBT must have the discretion to distribute amounts to the beneficiary and are required to consider the needs of the beneficiary in determining whether to pay amounts to the beneficiary.

The LBT must purchase a "qualifying trust annuity" (QTA) with the RRSP/RRIF proceeds and must be named as the annuitant of the QTA. The QTA must be for the life of the beneficiary or for a fixed term equal to 90 years minus the age of the beneficiary. Any annuity payments will be taxable to the beneficiary. This is the case regardless of whether the annuity payments are paid to the beneficiary or if they remain in the trust. The FMV of the annuity at the time of the beneficiary's death will be taxable to the beneficiary upon their death. Any income remaining in the LBT after the beneficiary's death may be made available to other beneficiaries named in the LBT.

You may wish to discuss with a qualified tax and legal advisor whether a standard Henson Trust would qualify as an LBT.

Designating a third party

You can designate any individual or registered charity as a beneficiary of your RRSP/RRIF. If you designate anyone other than your spouse or financially dependent child or grandchild, your RRSP/RRIF will be deregistered on your death.

In such a case, the gross RRSP/RRIF proceeds will be transferred to your named beneficiary (assuming they're a Canadian resident). Your estate will be responsible for paying the taxes on the FMV of your RRSP/RRIF at death, which could reduce the amount any other beneficiaries named in your Will receive.

As an example, assume that on death you own $600,000 of assets after tax, plus $300,000 in an RRSP. You have three beneficiaries and wish to give each an equal share. If you designate one beneficiary to receive your RRSP of $300,000 and name the other two as beneficiaries under your Will, the beneficiaries under your Will won't receive their full share of $300,000 from the remaining $600,000. The income tax payable on your RRSP is about $138,000 (assuming a combined federal and provincial tax rate of 46%). After your estate pays the tax, there will only be $462,000 remaining to divide between the two beneficiaries named in your Will who are not receiving the RRSP proceeds. Each of them will receive $231,000 while your beneficiary named on the RRSP plan will receive the full $300,000.

If your estate has insufficient funds to pay the tax on your RRSP/RRIF, the Canada Revenue Agency (CRA) can seek payment of the tax owing from the beneficiaries who received the RRSP/RRIF proceeds.

Note that any growth in your RRSP/RRIF after the date of death will be taxable to your named beneficiary in the year the RRSP/RRIF proceeds are paid out to your beneficiary if the proceeds are paid out during the exempt period. This growth is taxable to the beneficiary as income.

If a charity is named as the beneficiary of your RRSP/RRIF, the legal representative of your estate may be able to claim a donation tax credit on your terminal tax return to reduce your taxes, including any taxes payable on the FMV of your RRSP/RRIF at death. Certain conditions will need to be met. For more information on these conditions, please ask your RBC advisor for our article on charitable donations.

Designating a non-resident

Your RRSP/RRIF assets can generally be rolled over to an RRSP/RRIF for your non-resident spouse or financially dependent child or grandchild, as long as they have a valid Canadian social insurance number (SIN) and it's done by way of a direct transfer. Please note that a non-resident spouse may become a successor annuitant of a RRIF even if they have no Canadian SIN and defer tax on the RRIF assets. Any amount not eligible for the rollover is generally subject to a 25% non-resident withholding tax unless a reduced treaty rate applies. For example, the minimum payment from your RRIF would not be eligible for the rollover and be subject to non-resident withholding tax.

If you name any other non-resident individual as a beneficiary of your RRSP/RRIF, your plan will be deregistered on your death and the full FMV as at the date of death will generally be transferred to your named beneficiary. Your estate will be responsible for paying the taxes on the FMV of your RRSP/RRIF as at the date of death. Any income earned after the date of your death and paid to your non-resident beneficiary will be subject to non-resident withholding tax.

Conclusion

When creating your estate plan, it's important to consider the appropriate beneficiary to inherit your RRSP/RRIF. Even if you have named a beneficiary on your RRSP/RRIF, consider reviewing all your beneficiary designations regularly to ensure they're up to date and that they reflect any changes to your personal family situation.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

Appendix A – Tax reporting options on death

This appendix assumes that you, the annuitant of the RRSP/RRIF, are a Canadian resident at the time of death.

General rule

As a general rule, on your death, the FMV of your RRSP/RRIF is included as income on your final tax return. Any income earned in your RRSP/RRIF during the exempt period will be taxed in the hands of the beneficiaries named in your plan or your estate (if no beneficiary is named on the plan) in the year it's paid. The taxation of any income earned after the exempt period will depend on whether the RRSP/RRIF is a depositary, trusteed or insured RRSP/RRIF.

One exception to this general rule occurs where your spouse is named as successor annuitant of your RRIF. In such a case, the FMV of the RRIF on the date of death is not included in your final tax return. The RRIF continues and all payments made from the RRIF after your death are taxable to your spouse.

A second exception to this tax reporting occurs where your spouse is named as the sole beneficiary of your RRSP/RRIF on the plan documentation and the RRSP/RRIF proceeds are transferred directly to your spouse's RRSP/RRIF or used to purchase an eligible annuity by December 31 of the year following the year of death. In this case, your spouse will include the total amount paid out of the RRSP/RRIF on their tax return and will claim an offsetting deduction for the amount transferred to their RRSP/RRIF. Please note that your spouse will not be able to transfer any unpaid RRIF minimum payment to their own RRSP/RRIF. This amount will be taxable to your spouse.

Optional reporting

If neither exception described previously applies, you may want to consider the following options:

Where your spouse or financially dependent child or grandchild is named as beneficiary of your RRSP/RRIF plan

If your spouse or financially dependent child or grandchild is named as the beneficiary of your RRSP/RRIF on the plan documentation, and they receive an amount from your RRSP/RRIF that qualifies as a "refund of premiums" (in the case of an RRSP) or "designated benefit" (in the case of a RRIF), your legal representative can choose to claim a reduction to the RRSP/RRIF amount reported in your final tax return. A refund of premiums or designated benefit includes the FMV of your RRSP/RRIF at the date of death and any income earned in the RRSP/RRIF from the date of death to December 31 of the year after the year of death.

Your legal representative must attach a letter to your final tax return to explain any reduction to the RRSP/RRIF amount reported on your final tax return. If the reduction to the RRSP/RRIF amount you reported on your final tax return is claimed after the final tax return has been filed, your legal representative must write a letter to the CRA and ask for an adjustment to your final tax return. Any reduction to the amount claimed as RRSP/RRIF income on your final tax return will increase the amount of RRSP/RRIF income reported on your spouse's or financially dependent child's or grandchild's tax return.

It's important to note that if your RRSP/RRIF is not collapsed in the year of death, the FMV of your RRSP/RRIF may need to be included in your terminal tax return. This may create a cash flow issue, as tax will be owing on this amount. Once your RRSP/RRIF is collapsed and the refund of premiums or designated benefit is paid out to your spouse or financially dependent child or grandchild, your legal representative may be able to reduce the amount of the RRSP/RRIF proceeds that were taxable on your terminal return and obtain a refund of any taxes paid.

If your spouse decides to transfer the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to their own RRSP/RRIF or uses the proceeds to purchase an eligible annuity, your spouse can claim a deduction on their tax return for the amount transferred.

If your financially dependent minor child or grandchild uses the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to purchase a term-certain annuity, your child or grandchild can claim an offsetting deduction on their tax return for the amount transferred.

If your financially dependent disabled child or grandchild transfers the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to their own RRSP/RRIF or uses the proceeds to purchase an eligible annuity, they can claim an offsetting deduction on their return for the amount transferred. If they transfer the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to their RDSP, they will also be able to claim an offsetting deduction. CRA Form RC4625, Rollover to a Registered Disability Savings Plan (RDSP) Under Paragraph 60(m), must be attached to both your and your beneficiary's tax returns. The receipt indicating the amount rolled over must also be attached to your beneficiary's return.

In all cases mentioned, the transfer or purchase must be completed in the year the RRSP/RRIF proceeds are received by the beneficiary or within 60 days following the year-end. Also, please note that your spouse cannot transfer the RRIF minimum payment for the year the proceeds are received to their RRSP, RRIF or annuity. The RRIF minimum payment for that year will be taxable to your spouse.

Where your spouse or financially dependent child or grandchild is the beneficiary of your estate

If you do not name your spouse or financially dependent child or grandchild as a beneficiary of your RRSP/RRIF on the plan documentation, but they are a beneficiary of your estate under your Will or provincial or territorial intestacy laws and are beneficially entitled to some or all of the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit, your beneficiary and your legal representative can jointly elect to tax these proceeds in your beneficiary's hands.

Your legal representative and your spouse or financially dependent child or grandchild will have to jointly file an election to designate some or all of the RRSP/RRIF proceeds paid to the estate as a refund of premiums or designated benefit received by your beneficiary. The joint tax election can be made on CRA Form T2019, Death of an RRSP Annuitant – Refund of Premiums for 20__ (Revenu Québec Form TP-930-V), if you have an RRSP and on CRA Form T1090, Death of a RRIF Annuitant – Designated Benefit for Year 20__ (Revenu Québec Form TP-961.8-V) if you have a RRIF. Your legal representative can then claim a reduction in the amount of RRSP/RRIF income included on your final tax return. Your spouse or financially dependent child or grandchild will have a corresponding income inclusion on their tax return.

Note that if your financially dependent child or grandchild is a minor or mentally incapable, they may require a legal representative to make this joint tax election with the legal representative of your estate.

If your spouse decides to transfer the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to their own RRSP/RRIF or uses the proceeds to purchase an eligible annuity, your spouse can claim a deduction on their tax return for the amount transferred.

If your financially dependent minor child or grandchild uses the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to purchase a term-certain annuity, your child or grandchild can claim an offsetting deduction on their tax return for the amount transferred.

If your financially dependent disabled child or grandchild transfers the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to their own RRSP or RRIF or uses the proceeds to purchase an annuity, they can claim an offsetting deduction on their return for the amount transferred. If they transfer the RRSP/RRIF proceeds that qualify as a refund of premiums or designated benefit to their RDSP, they will also be able to claim an offsetting deduction. CRA Form RC4625, Rollover to a Registered Disability Savings Plan (RDSP) Under Paragraph 60(m), must be attached to both your and your beneficiary's tax returns. The receipt indicating the amount rolled over must also be attached to your beneficiary's return.

In all cases mentioned, the transfer or purchase must be completed in the year the RRSP/RRIF proceeds are received by the beneficiary or within 60 days of year-end.

Appendix B – Successor annuitant vs. beneficiary of your RRIF

If you want your spouse to inherit your RRIF assets, you'll need to decide whether to name them as a beneficiary or successor annuitant of your RRIF. The table below summarizes the implications of both options. Please keep in mind that your designation decision may be changed at any time, provided you have mental capacity.

For purposes of this comparison, it's assumed your beneficiary completes a direct transfer of your RRIF proceeds to their RRSP or RRIF by December 31 of the year following the year of your death.