Flow-through shares and limited partnership units

Depending on your province of residence, you may be subject to tax at a rate of 50% or higher when your income exceeds $200,000. One potential tax minimization strategy is to purchase flow-through investments. These types of investments may help you reduce your taxable income and thus reduce your tax liability. This article provides an overview of flow-through investments and discusses the tax implications of purchasing flow-through investments.

Depending on your province of residence, you may be subject to tax at a rate of 50% or higher when your income exceeds $200,000. One potential tax minimization strategy is to purchase flow-through investments. These types of investments may help you reduce your taxable income and thus reduce your tax liability. This article provides an overview of flow-through investments and discusses the tax implications of purchasing flow-through investments.

Family Office Services

September 14, 2022

Flow-through shares and limited partnership units

Depending on your province of residence, you may be subject to tax at a rate of 50% or higher when your income exceeds $200,000. One potential tax minimization strategy is to purchase flow-through investments. These types of investments may help you reduce your taxable income and thus reduce your tax liability. This article provides an overview of flow-through investments and discusses the tax implications of purchasing flow-through investments.

Note: The 2022 budget proposed to eliminate the flow-through share regime for fossil fuel sector activities. This will be done by no longer allowing expenditures related to oil, gas and coal exploration and development to be renounced to flow-through share investors for flow-through share agreements entered into after March 31, 2023.

What is a flow-through investment?

A flow-through investment is a type of tax-advantaged investment vehicle. The tax advantages are meant to encourage investment in resource companies engaging in exploration and development in the mining, oil and gas, and renewable energy and energy conservation sectors. If structured properly, the resource company may "renounce" or "flow through" certain expenses it incurs to you, which you can then deduct personally on your tax return. The maximum amount you can deduct is the amount you paid for the investment. You may apply the deductions against all sources of income, thereby reducing your net income and the associated tax liability. There is no maximum amount of renounced expenditures that you may claim and therefore it is possible to create a non-capital loss. You may carry the non-capital loss (i.e. excess deductions) back three years or forward 20 years, and you may use the non-capital loss to reduce all sources of income.

There are two types of flow-through investments:

1. Flow-through common shares, which are issued directly by a resource company; and

2. Flow-through limited partnership (LP) units, which are issued by entities that purchase a diversified portfolio of flow-through shares.

What is a flow-through share?

A resource company may issue flow-through common shares directly from treasury in a similar fashion to regular common shares. However, flow-through shares are typically offered at a significant premium to the price of the company's common shares at the time of issuance. Individuals, trusts, corporations and partnerships can invest in flow-through shares, but only the original investors can deduct renounced expenses. These renounced expenses may be claimed in the year or carried forward. Original investors are entitled to deductions renounced by the resource company typically for a number of years after investment.

It's important to note that the adjusted cost base (ACB) of a flow-through share is deemed to be zero. This means when you eventually sell your shares, the full sale proceeds are generally taxed as a capital gain. You are usually able to sell your flow-through shares on the open market as soon as you've purchased your shares and the trade has settled; however, you should consult the prospectus and/or related offering documents of the investment for any holding restrictions.

While flow-through shares are qualified investments for registered accounts, such as a registered retirement savings plan (RRSP), you will not realize the associated tax benefits. Therefore, it generally does not make sense to purchase flow-through shares in these accounts.

Quebec residents and flow-through shares

If you're a resident of Quebec, please consult your qualified tax advisor, as tax treatment of flow-through shares may differ from the treatment in other Canadian provinces and territories.

In Quebec, flow-through shares provide an additional 20% deduction for exploration expenses incurred in the province, in addition to a basic deduction of 100% of their cost. The capital gain realized on the sale of shares may be exempt up to the amount of the share purchase price.

The company may also allocate out issue costs, such as brokers' commissions, legal and accounting fees, and printing costs to you. You can deduct such amounts over a period of five years.

What is a flow-through LP?

Flow-through LP units may be issued by an entity that purchases a diversified portfolio of flow-through shares. Flow-through LPs offer tax benefits to investors similar to flow-through shares, but they have some different features. Unlike flow-through shares, where only the original investor can deduct renounced expenses, the owner of the LP unit on the last day of the LP's fiscal year-end (usually December 31) is entitled to deduct the renounced expenses. Typically, the LP flows through about 90–95% of your invested amount in deductions in the first year, and the remaining 5–10% in the following year(s).

In general, approximately 18–24 months from the close of the LP offering, the LP is dissolved and your LP units are exchanged for shares of a mutual fund corporation on a tax-deferred basis. You may choose to either hold or sell the shares of the mutual fund.

Similar to flow-through shares, you may deduct the expenses renounced by the flow-through LP in the year or carried forward. However, instead of having a deemed ACB of zero, the ACB of your flow-through LP unit is reduced by the amount of flow-through deductions you claim on your tax return. This usually results in an ACB of zero, which generally means when the investment is disposed of, you may realize capital gains.

Flow-through LPs are generally not qualified investments for registered accounts.

Special considerations for flow-through LPs

If you choose to purchase flow-through investments through an LP, you should be aware that while you're holding the LP units, the LP may realize and allocate some capital gains and potentially other taxable income to you. This is because, for tax purposes, an LP itself is not a taxpayer. Instead, the income or losses earned by the LP are allocated to its partners for inclusion on their tax returns, even if cash has not been distributed from the LP to the partners. A gain realized in an LP may be from dispositions of flow-through shares due to corporate acquisitions or restructurings of the issuers, or it may be due to portfolio management decisions made by the portfolio manager.

To prevent double taxation, the ACB of your LP units is adjusted by income or losses allocated to you by the partnership. Losses are subtracted from and income is added to your ACB at the beginning of the year following the allocation. If you receive a cash distribution from the LP, this amount will reduce your ACB.

Mineral exploration tax credit (METC)

In October 2000, the federal government introduced a temporary 15% investment tax credit as part of a program to promote exploration and to help moderate the impact of the downturn on mining communities. The program has been extended many times and is currently available to investors subscribing to qualifying flow-through share agreements on or before 2025. The METC may be claimed on the amount of certain renounced mineral exploration expenses. The credit, which is only available to individuals and not to trusts, partnerships or corporations, is deductible from federal income taxes payable and is in addition to the existing flow-through deductions. Flow-through investments qualifying for this additional credit are commonly referred to as "super" flow-through shares to distinguish them from regular flow-through shares.

You may claim the METC to reduce your tax liability in the current year. For any excess credit, you may carry it back for up to three years or forward for 20 years, if it was earned in a year after 2005. You may also be able to claim a refund of your unused METC, but it can only be done in the year it's earned. This refund will reduce the amount of credit available to you for other years. The METC you claim in the year may result in an income inclusion in the following year in the absence of a new investment in flow-through shares or LP units.

If you reside in a province/territory that provides an investment tax credit, this tax credit may be claimed in combination with the federal credit. However, the provincial/territorial credit received or entitled to be received in a taxation year will reduce your federal tax credit.

Critical mineral exploration tax credit (CMETC)

Budget 2022 proposed a new 30% CMETC for renounced exploration expenses of specified minerals used in the production of batteries, permanent magnets, semiconductors and other clean technologies. The rules for the CMETC will generally follow the existing METC rules. Eligible expenditures would not benefit from both the CMETC and METC. The CMETC will apply to expenditures renounced under eligible flow-through share agreements entered into after April 7, 2022, and on or before March 31, 2027.

Alternative minimum tax (AMT)

If you're purchasing a flow-through investment in order to reduce your taxable income, it's very important to consider AMT. This tax aims to ensure that every Canadian individual pays a minimum amount of tax. The calculation of AMT is based on an adjusted taxable income, which seeks to remove the advantages of certain tax-preferential items such as deductions from flow-through investments. If the AMT calculated is greater than your regular tax liability, the AMT becomes your tax liability for the year. The difference between the AMT you have to pay in a year and your regular tax liability can be carried forward for seven years to reduce your future regular income tax liability when your taxes payable exceed your AMT. For more information about AMT, ask your RBC advisor for an article on this topic.

Please speak with a qualified tax advisor to help you determine how AMT will affect you if you're considering flow-through investments.

Corporate ownership of flow-through investments

A corporation can purchase flow-through investments in order to reduce its taxes. The tax benefit to the corporation of the deductions flowed through depends on the type of income the renounced expenses are being deducted against (i.e. investment income, active business income under the small business limit or active income taxed at the general corporate rate). A corporation is not subject to AMT, however, corporate minimum tax may be applicable in the corporation's province/territory of residency if it makes a large flow-through investment purchase.

A corporation may benefit from owning flow-through investments in particular if it has capital loss carryforwards that may be used to offset the resulting capital gain arising on the disposition of the investment. For example, after purchasing a flow-through investment personally and deducting the expenses on your personal tax return, you may be able to transfer the flow-through investment to your corporation on a tax-deferred basis. When the corporation sells the investment, the corporation will realize a capital gain, which may be sheltered by the corporation's capital loss carry-forwards. Please take note of any holding period requirements if you're contemplating this strategy.

Possible drawbacks of flow-through investments

Investment risk

What will the proceeds from sale be when the flow-through shares/mutual fund shares are sold 18–24 months from now? There is a risk that the underlying investment will not perform well and you may realize a loss on the sale. You may want to review the prospectus/offering documents for more information regarding a particular investment.

Consider if the tax savings will make up for any potential investment losses. Appendix A demonstrates how investment risk could impact the expected tax savings for an individual investing in flow-through LP units.

Tax risk

To be eligible for the renunciation, expenses incurred by the resource company must meet certain criteria. You should be aware there is a tax risk that the CRA will deny the renunciation of expenses that do not meet these qualifications. You will then lose the ability to deduct these expenses. If you have already deducted them, you may be reassessed in a later tax year, which may result in having taxes owing as well as interest charges. A three-year extension to the normal three-year reassessment period may apply.

Time horizon and liquidity

As there is generally no secondary market for units of flow-through LPs, in most cases you will need to wait until the partnership is dissolved and your units are converted to shares of a mutual fund corporation before you can liquidate your position. The units may not be converted into mutual fund shares for 18–24 months or longer after the close of the LP offering, and there may be a short holding period once the LP units are converted to shares of a mutual fund corporation.

Additional tax reporting

Claiming the deductions and tax credits associated with flow-through investments may complicate your tax filing situation. Further, if you invest in flow-through LP units, you will need to keep track of the ACB of the investment. This may result in additional accounting fees.

Other considerations prior to purchasing the investment

When determining whether a flow-through investment is right for you, in addition to the risks discussed, you may want to consider the following with a qualified investment advisor and qualified tax advisor:

- What are the specific features and inherent risks associated with a particular flow-through investment?

- What is the issuer's track record?

- Is there a prospectus or offering memorandum?

- Is future financing required (i.e. additional future instalment payment or liability for debts incurred by the partnership)?

- When will the tax deductions be available?

- How does the investment affect your overall asset allocation strategy and your risk tolerance?

- How long do you plan to hold the investment?

- Has the issuer received an Advanced Income Tax Ruling from the CRA regarding certain aspects of the investment? If so, ask to see a copy.

Conclusion

Investing in flow-through investments may provide you with immediate tax savings. However, there are many other factors you should consider, such as the investment risk, the diversity of your investment portfolio and the opportunity cost. Please consult with qualified professional advisors before making these types of investment decisions.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

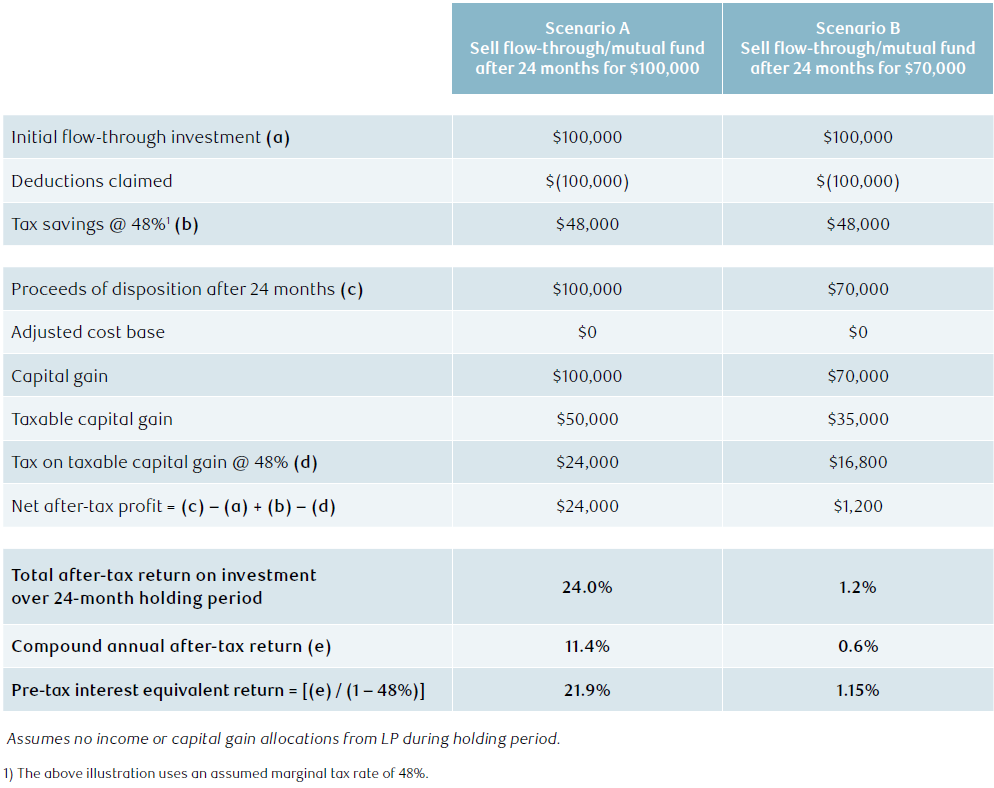

Appendix A: Flow-through LP unit example

Let's look at an example to illustrate the tax implications for an individual investing in flow-through LP units, and how investment risk could impact expected tax savings.

Scenario A illustrates an investor purchasing units for $100,000 and selling the resulting mutual fund shares for $100,000 after 24 months. Scenario B illustrates the same initial investment of $100,000; however, the mutual fund shares are sold for $70,000 after 24 months.