Foreign withholding tax on dividends from foreign equities and American depository receipts (ADR)

When investing in foreign equities in any form, there are always additional considerations with respect to foreign withholding tax. These taxes can, in certain instances, impact your return on investment.

When investing in foreign equities in any form, there are always additional considerations with respect to foreign withholding tax. These taxes can, in certain instances, impact your return on investment.

Family Office Services

June 14, 2022

Foreign withholding tax on dividends from foreign equities and American depository receipts (ADR)

When investing in foreign equities in any form, there are always additional considerations with respect to foreign withholding tax. These taxes can, in certain instances, impact your return on investment. Canada has tax treaties with many countries that provide for a lower withholding tax rate on the dividends paid to Canadian residents. In some cases, the treaty rate may not be used to determine the withholding tax charged on your foreign income; instead, the foreign countries' domestic non-resident withholding tax rates are applied. Therefore, you may find that sometimes you pay more tax than expected on the foreign equity dividends you earn. It's important to understand the impact of foreign withholding tax when thinking about costs associated with investing in foreign equities. This article discusses withholding tax on foreign equities that are shares of companies outside of Canada and the U.S. that you hold either directly or indirectly through an American depository receipt (ADR).

Withholding tax applied to foreign dividends

When investing in foreign equities, it may be done by purchasing the equity itself, or it may be done indirectly through an ADR, but both pay foreign dividends. An ADR is a security that represents a non U.S. company's publicly traded stock. The ADR is typically created when a U.S. bank purchases a foreign company's shares in its domestic market, and re-issues them in the U.S., which may allow investors to more easily invest in foreign markets.

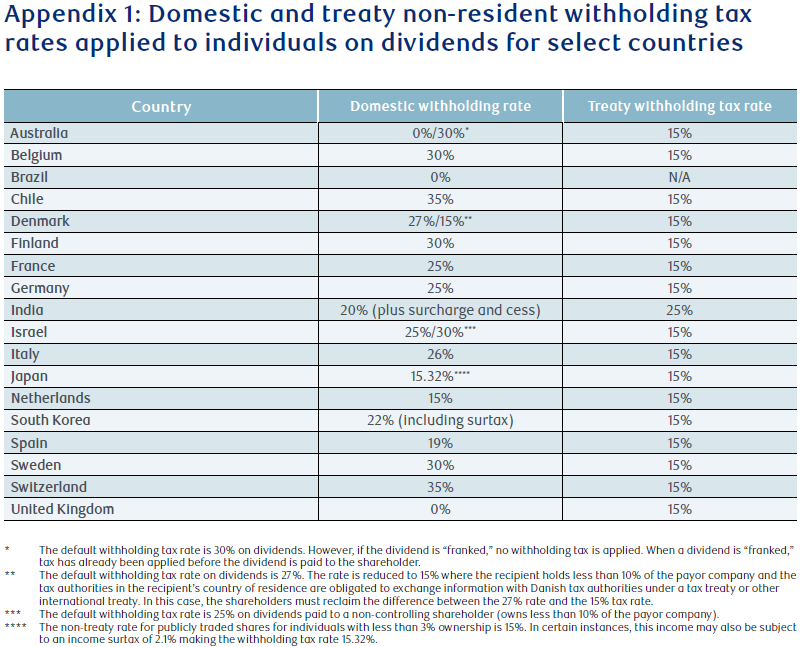

Generally, the foreign payor is obligated to withhold taxes on dividends paid to non-residents at a rate according to the domestic tax rules of the country where the payor company is incorporated, unless the rate is reduced by a tax treaty. Often times, the domestic withholding tax rate is significantly higher than the treaty tax rate, which is typically around 15% (Appendix 1 lists domestic withholding tax rates and treaty withholding tax rate for a sample of various foreign countries). However, due to the administrative process, the foreign country's domestic non-resident withholding tax rate may be used instead of a reduced treaty tax rate.

Foreign equities and ADRs are generally held in bulk by foreign custodians on behalf of underlying individual owners. These foreign custodians don't have access to information on who the underlying owner is or their residency; thus generally don't withhold taxes on dividends at the applicable treaty rate. Instead, they pay the dividend less the foreign country's domestic non-resident withholding tax, without consideration of tax treaties.

Recovering excess withholding tax

Canadian foreign tax credit

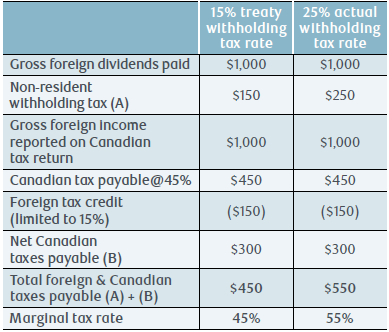

As a Canadian resident, you're required to report the gross foreign dividend (before withholding tax) on your Canadian income tax return and pay tax at your marginal tax rate. Canadian tax rules allow you to claim a foreign tax credit for foreign withholding tax paid to alleviate double taxation. However, the rules limit the foreign tax credit that can be claimed to the tax treaty rate on the foreign dividend income.

For example, assume you're resident in Canada with a marginal tax rate of 45%. You earn foreign dividends of $1,000 in your non-registered account during a tax year. You have no other foreign source income during the year. The treaty withholding tax rate on the foreign dividend is 15%. The following table compares the overall tax impact if the actual foreign withholding tax was 25% instead of 15%.

If Canadian tax rules allowed you to claim the full $250 withholding tax as a foreign tax credit, then you would only pay $200 of tax to the Canada Revenue Agency (CRA) ($450 Canadian tax payable – $250 foreign tax credit). However, due to the foreign tax credit limit, you would end up paying $300 in Canadian taxes plus the $250 withheld. Therefore, in this example, the global tax rate would be 55%.

The example illustrates that if the withholding tax was equal to or less than the treaty rate, then you would pay a global tax rate equal to your marginal tax rate of 45%. However, if the actual withholding tax paid is more than the treaty rate, your global tax rate would be higher than your marginal tax rate.

Due to the foreign tax credit limit, some foreign equity dividends may be ultimately taxed at a global tax rate that's higher than your normal marginal tax rate. As such, when evaluating the merits of investing in foreign equities, you should consider the effect of the actual foreign withholding tax that will be applied in determining your after-tax investment return.

Canadian income tax deduction for foreign withholding tax

If you invest in foreign equities or ADRs of countries where there's no tax treaty between Canada and that country, you may be able to take a special income tax deduction on your Canadian income tax return for foreign withholding taxes paid in excess of 15%. Generally, any amount paid in excess of 15% must first be deducted in calculating your taxable income. This would reduce the amount that can be claimed as a foreign tax credit to 15% and also reduce the amount of foreign income when calculating the foreign tax credit. It can be a complex calculation, so you may want to seek advice from your qualified tax advisor.

Recovering withholding tax from foreign jurisdiction

The process to recover the excess foreign withholding tax may be complex, labour-intensive and costly compared to the benefit. Each country has its own process for recovering the excess withholding tax. Commonly, you may need to provide documentation to support that you're entitled to the treaty rate, proof of your country of residence and evidence that you paid withholding tax in excess of the treaty rate. You may need to obtain a reclaim form from the relevant local embassy or tax agency of the country of the equity issuer's origin. You may also need to provide certifications from the CRA and your broker on the reclaim forms, which may be challenging.

Processes, timeframes, success rates and requirements vary greatly from jurisdiction to jurisdiction. Although some countries have a streamlined process to handle the recovery requests, there is generally no guarantee your application will be successful. In addition, you may need to pay fees as part of the reclaim process and may need to involve a qualified tax advisor.

Impact on investment decision

If you're investing in foreign equities directly or through ADRs, you may pay foreign withholding tax in excess of or less than the treaty rate on a security-by-security basis. It's important to take this into account in determining your after-tax return on your investment.

In addition, there may be other factors you should consider when deciding if you want to invest in a foreign equity or ADR. These factors may include the size of your portfolio, your desired level of diversification, and your personal preference related to the level of control over the individual securities in your portfolio. It's important to consider all of these factors when you make your investment decision.

Foreign dividends earned in registered plans

When you hold foreign equities and ADRs within a registered or locked-in retirement plan (e.g. RRSP, RRIF, LIRA LIF, LRIF, PRIF, TFSA), there may still be withholding tax on the dividend income you earn. You have no ability to claim a foreign tax credit on your Canadian income tax return for the withholding tax applied to your dividend income in a registered plan. As a result, the income you earn on the foreign investment is the net dividend received. Therefore, if you purchase foreign equities and ADRs in your registered plan, you should consider the net after-tax return.

Foreign equities held through mutual funds

The issue of excess withholding tax on foreign dividends can also affect those holding foreign equities in a pooled form such as a mutual fund or an exchange-traded fund (ETF). In the case where the equities are held in a fund, the foreign dividend payor may not be able to identify the underlying unit holders and therefore will apply the domestic withholding rate.

Sale of foreign equities and ADRs

Generally, there is no withholding tax on the sale of foreign equities or the sale of an ADR. You may trigger a capital gain or loss on the sale and will need to report this capital gain or loss on your Canadian tax return. Based on the current capital gains inclusion rate of 50%, only half of the gain or loss is taxable or allowable.

If excess withholding tax is an issue, you may want to consider investing in foreign equities and ADRs that focus on growth and don't pay out a regular dividend. This will allow you to eliminate or minimize the amount of withholding tax you'll be subject to and benefit from the preferential tax treatment of capital gains. However, there may be higher risks associated with these types of investments. Speak with your RBC advisor about your risk tolerance and whether this strategy makes sense for your portfolio.

Conclusion

If you're thinking about investing in foreign equities, either directly or indirectly through ADRs, you should be aware of the foreign withholding tax that may apply. The withholding tax rate that applies to the dividends you receive may be greater than expected, affecting your after-tax return. The impact of the higher foreign withholding taxes on an overall portfolio may be modest; as such, there may be more important factors for you to consider. Speak to your RBC advisor for assistance on building your portfolio. If you require more information regarding the taxation of your investments, speak with your qualified tax advisor.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

Appendix 1: Domestic and treaty non-resident withholding tax rates applied to individuals on dividends for select countries