How the alternative minimum tax (AMT) rules may impact charitable giving

Since 2023, the government has introduced a number of changes to AMT which may have broadened its impact on high-income earners. If you are a high-income earner who is philanthropic, some of these changes may significantly affect you and the charities you support. These new rules may cause you to re-evaluate your personal charitable donation plans, including reviewing what assets to donate, how much to give, and when to give.

Since 2023, the government has introduced a number of changes to AMT which may have broadened its impact on high-income earners. If you are a high-income earner who is philanthropic, some of these changes may significantly affect you and the charities you support. These new rules may cause you to re-evaluate your personal charitable donation plans, including reviewing what assets to donate, how much to give, and when to give.

Family Office Services

November 14, 2025

How the Alternative Minimum Tax (AMT) Rules May Impact Charitable Giving

Since 2023, the government has introduced a number of changes to AMT which may have broadened its impact on high-income earners. If you are a high-income earner who is philanthropic, some of these changes may significantly affect you and the charities you support. These new rules may cause you to re-evaluate your personal charitable donation plans, including reviewing what assets to donate, how much to give, and when to give.

Changes to AMT were proposed in the government's 2023 federal budget. The proposals were amended and confirmed in the 2024 federal budget and then passed into law on June 20, 2024. These changes to AMT are effective as of January 1, 2024. Additional amendments were proposed on August 12, 2024, with respect to flow-through shares and the deduction of investment counsel fees but would have to be re-introduced by the new government and passed into law to be effective. For more information on these proposed amendments, please ask your RBC advisor for the article discussing how the AMT rules may impact individuals.

What is AMT?

AMT has been in effect since 1986 and is intended to prevent high-income individuals (and certain trusts) from significantly lowering their taxes by using certain tax preferences or incentives. Tax preferences or incentives are specific items that reduce your taxable income or tax liability, such as claiming certain exemptions like the lifetime capital gains exemption (LCGE), earning tax preferential income like capital gains or benefiting from charitable donations. Consequently, you're required to compute your tax liability by calculating your regular tax and AMT. You pay either the regular tax or the AMT, whichever is higher. The AMT calculation allows fewer deductions, exemptions and tax credits than the regular income tax rules.

If you're required to pay AMT, it may be recoverable over the next seven years. As such, it's often seen as a prepayment of taxes. For more details on the AMT rules, ask your RBC advisor for an article on how AMT impacts individuals.

You may also be subject to provincial/territorial AMT. For many provinces/territories, provincial/territorial AMT is calculated as a percentage of federal AMT. This article focuses on federal AMT.

What are the changes that may affect the tax benefits of charitable giving?

When you donate a publicly listed security in-kind to a registered charity, you receive a donation tax receipt for the full fair market value of the security. With this receipt, you may choose to claim a donation tax credit, which would reduce your regular taxes payable for the year. Donating in-kind also allows you to avoid including any capital gain accrued on the donated security in your taxable income. As such, you may have included donating securities in-kind in your charitable giving plan.

However, when calculating AMT, you need to include 30% of the capital gain realized on the in-kind donation of the security in adjusted taxable income (ATI). In addition, you can only claim 80% of the donation tax credit in determining your AMT liability.

On August 12, 2024, the previous Liberal government proposed further amendments to AMT related to in-kind donations of a flow-through class of property. These proposals are not yet law and requires re-introduction by the newly elected government. Therefore, the Canada Revenue Agency (CRA) is not administering this proposal. This provision, if enacted, ensures that you include only 30% of the "true" capital gain in ATI for AMT purposes on the in-kind donation of a flow-through class of property. The "true" capital gain is the proceeds received that is more than your original cost amount of the flow-through class of property.

To illustrate the potential tax impact of the changes to AMT related to charitable donations, the following are some examples. Be sure to consult with your qualified tax advisor for a more in-depth discussion on how these rules may affect your specific situation.

When you donate a publicly listed security in-kind to a registered charity, you receive a donation tax receipt for the full fair market value of the security. With this receipt, you may choose to claim a donation tax credit, which would reduce your regular taxes payable for the year.

Examples

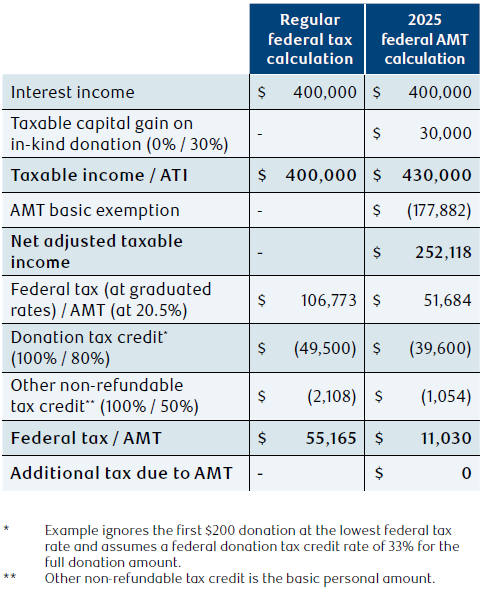

Example 1

Scenario: Earn $400,000 of interest income and want to donate publicly listed securities in-kind, valued at $150,000. The securities have an adjusted cost base (ACB) of $50,000 so that the accrued capital gain is $100,000.

In this example, you wouldn't have an AMT liability but you would owe $55,165 in regular federal tax.

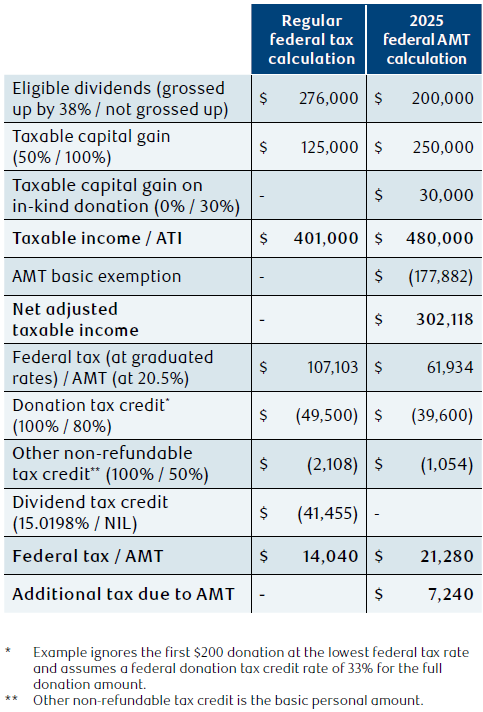

Example 2

Scenario: Earn $200,000 in eligible dividend income from Canadian companies, realize $250,000 in capital gains, and want to donate publicly listed securities in-kind, valued at $150,000. The donated securities have an ACB of $50,000 so that the accrued capital gain is $100,000.

In this example, since the minimum tax of $21,280 is greater than the regular tax of $14,040, you'd have an AMT liability and owe $21,280 in federal taxes.

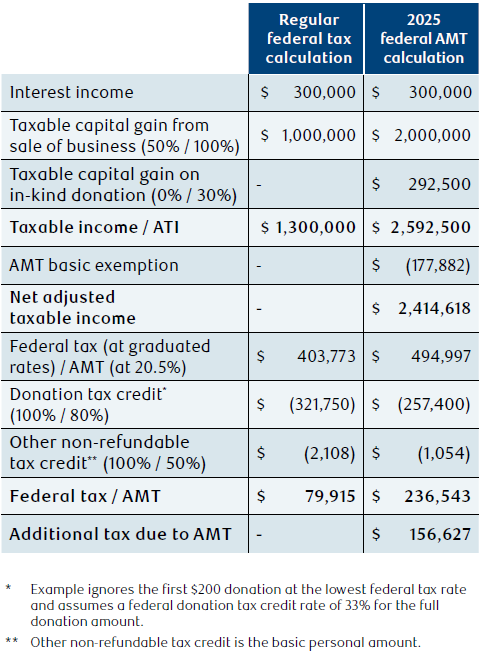

Example 3

Scenario: Earned $300,000 of interest income and also sold your business, realizing a capital gain of $2,000,000 on the sale. For simplicity's sake, assume that the sale does not qualify for the LCGE. You also wish to donate securities in-kind, valued at $975,000 with a nominal ACB.

Since the minimum tax of $236,543 is greater than the regular tax of $79,915, you'd have an AMT liability and owe $236,543 in federal taxes.

AMT carry-forwards

If you're subject to AMT, you can carry forward the difference between the AMT you paid and your regular income tax liability as a tax credit for seven years, or until it's used up whichever is sooner. This AMT tax credit can be used to offset your future regular taxes, to the extent your regular tax liability exceeds your AMT liability in future years. In this sense, AMT is like a prepayment of tax.

If you don't have sufficient regular taxes payable in the next seven years, your AMT credit will expire and become a permanent tax. You may not be able to fully recover your AMT credit if you claim the same types of exemptions, deductions and credits or have the same type of tax preferential income every year.

Strategies to Minimize the Impact of AMT

- Instead of making one large donation, consider spreading out your donations over a number of years. This strategy may be especially useful if you sell capital property (such as securities or real estate) and are able to save the sale proceeds over the same number of years.

- Consider whether you're able to adjust the types of income you earn in the year you make a significant donation. For example, you may be able to make a donation to your RRSP/RRIF, or drawing a salary or bonus from your corporation may be preferable to realizing capital gains in the year you make a large donation. This is because non-tax preferred income is taxed (such as salary income) minimize the impact AMT may have.

- Instead of making your donations personally, consider having your corporation make the donation. This is because AMT is applicable to individuals and corporations. In addition, 100% of the capital gains from the donation of publicly listed securities are added to the corporation's capital dividend account (CDA) and can be paid tax-free to you as a capital dividend to the extent the CDA is positive.

- AMT doesn't apply on death. As such, donations made through your graduated rate estate will not be affected by AMT.

The changes to AMT may create an additional tax liability for those with charitable intentions. With proper planning, you may still support your cause and make a difference in a tax-efficient manner.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To obtain your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal or financial advisor before acting on any of the information in this article.