How the alternative minimum tax (AMT) rules may impact individuals

Since 2023, the government has introduced a number of changes to AMT which could broaden its impact on high-income earners. Under the new rules, AMT may now impact you, when it may not have in the past. If AMT is triggered, you could face an unexpected tax liability, thus it's important to understand when and how AMT applies. This article explains what AMT is and discusses some of the potential effects it may have on you.

Since 2023, the government has introduced a number of changes to AMT which could broaden its impact on high-income earners. Under the new rules, AMT may now impact you, when it may not have in the past. If AMT is triggered, you could face an unexpected tax liability, thus it's important to understand when and how AMT applies. This article explains what AMT is and discusses some of the potential effects it may have on you.

Family Office Services

November 14, 2025

How the Alternative Minimum Tax (AMT) Rules May Impact Individuals

Since 2023, the government has introduced a number of changes to AMT which could broaden its impact on high-income earners. Under the new rules, AMT may now impact you, when it may not have in the past. If AMT is triggered, you could face an unexpected tax liability, thus it's important to understand when and how AMT applies. This article explains what AMT is and discusses some of the potential effects it may have on you.

Changes to AMT were proposed in the government's 2023 federal budget. The proposals were amended and confirmed in the 2024 federal budget and then passed into law on June 20, 2024. These changes to AMT are effective as of January 1, 2024. Additional amendments were proposed on August 12, 2024, with respect to flow-through shares and the deduction of investment counsel fees. As these additional proposals (mentioned later in the article) were introduced before the newly elected government and were not yet law, they would have to be reintroduced. At the time of publishing this article, the new government has not reintroduced these proposals.

What is AMT?

AMT has been in effect since 1986 and is intended to prevent high-income individuals (and certain trusts) from significantly lowering their taxes by using certain tax preferences or incentives. Tax preferences or incentives are specific items that reduce your taxable income or tax liability, such as claiming certain exemptions like the lifetime capital gains exemption (LCGE), earning tax preferential income like capital gains or benefiting from charitable donations. AMT is a mechanism to ensure that high-income individuals (and certain trusts) pay at least a minimum amount of tax every year.

Consequently, you're required to compute your tax liability by calculating your regular tax and AMT. You pay either the regular tax or the AMT, whichever is higher. The AMT calculation allows fewer deductions, exemptions and tax credits than the regular income tax rules.

Historically, AMT applied in relatively limited scenarios, such as when an individual claimed the LCGE or claimed large flow-through share deductions. However, due to the recent changes, more high-income individuals may now be affected.

How is AMT Calculated?

AMT is calculated based on this formula: A x (B - C) - D, where:

A = the AMT rate (20.5%)

B = the AMT base which is referred to as adjusted taxable income (ATI)

C = the AMT basic exemption (indexed to inflation and is equal to the start of the fourth federal tax bracket)

D = the allowable non-refundable tax credits for AMT purposes

For the AMT calculation, you start with your federal taxable income and adjust for certain tax preference items to arrive at your ATI. Examples of tax preference items include tax shelter deductions, employee stock option deductions, the LCGE, and capital gains. This is not an exhaustive list.

Your ATI is then reduced by a basic exemption amount to arrive at your net adjusted taxable income. The exemption amount is a deduction available to all individuals and qualified disability trusts. You then apply a fixed AMT rate to your net adjusted taxable income to arrive at a resulting tax amount or your "gross minimum amount."

Lastly, you deduct certain allowable non-refundable tax credits from the gross minimum amount to determine your federal minimum amount for the year. Non-refundable tax credits can be used to reduce your taxes but can't generate a tax refund even if the amount of the credits exceeds your tax liability.

If your federal minimum amount is greater than your federal income tax liability, you pay the federal AMT. You may also be subject to provincial/territorial AMT. For many provinces/territories, provincial/territorial AMT is calculated as a percentage of federal AMT.

A qualified tax advisor can help you determine if you have an AMT liability for a given year by preparing a draft tax return for you that factors in all of your relevant circumstances, such as income, deductions, exemptions and tax credits.

AMT Carry-Forwards

If you are subject to AMT, you can carry forward the difference between the AMT you paid and your regular income tax liability as a tax credit for seven years, or until it's used up whichever is sooner. This AMT tax credit can be used to offset your future regular taxes, to the extent your regular tax liability exceeds your AMT liability in future years. In this sense, AMT is like a prepayment of tax.

If you don't have sufficient regular taxes payable in the next seven years, your AMT credit will expire and become a permanent tax. You may not be able to fully recover your AMT credit if you claim the same types of exemptions, deductions and credits or have the same type of tax preferential income every year.

AMT Exceptions

AMT doesn't apply in the year of death, which is a much welcome exception due to the significant capital gains that can result from the deemed disposition on death. This includes the year of death of a life beneficiary of a spousal or common-law partner trust, an alter ego trust or in the year of the second to die of a joint partner trust. AMT also doesn't apply in the case of personal bankruptcy.

In terms of other entities, AMT does not apply to corporations as well as to certain taxable trusts, such as graduated rate estates (GREs), employee life and health trusts, and employee ownership trusts (EOTs).

Some Key Changes to AMT

In addition to the AMT rate and the AMT basic exemption, the following list highlights a few of the recent changes:

• 100% of capital gains and losses realized is now included in ATI (as opposed to 50% for calculating regular income tax).

• 30% of the capital gain realized on the in-kind donation of publicly listed securities to a qualified donee is included in ATI (as opposed to a 0% inclusion for regular income tax).

• 100% of employee security options benefit is included in ATI (as opposed to 50% inclusion rate for qualified securities).

• 50% of the capital loss carry forward or back is allowed as a deduction (the same as for calculating regular income tax).

• 50% of non-capital losses and limited partnership losses of other years is allowed as a deduction (as opposed to 100% for calculating regular income tax).

• 50% of certain deductions such as interest and carrying charges incurred to earn income from property, employment expenses (other than those incurred to earn commission income), moving expenses and childcare expenses are allowed (as opposed to 100% for calculating regular income tax).

• 80% of the donation tax credit and 50% of most other non-refundable tax credits, such as the basic personal amount, are allowed as a non-refundable tax credit for AMT purposes (as opposed to 100% for calculating regular income tax).

As previously mentioned, the following proposed amendments in the August 12, 2024 draft legislation would need to be reintroduced by the current government to be effective. At the time of publishing the article this has not happened.

• 100% of certain fees paid to investment council are allowed for AMT purposes (in line with the deduction for regular income tax). The August 12, 2024 proposed amendments would need to limit the deduction to 50%.

• Resource-property and flow-through share deductions and expenses are added back when calculating ATI, which generally makes it more likely that AMT would apply when you invest in flow-through shares. Under the proposed amendments, 100% of resource-property and flow-through share deductions and expenses would have been allowed (in line with the deductions for regular income tax). If this change is reintroduced by the current government and enacted, it should make investing in flow-through shares more attractive to investors who are sensitive to AMT.

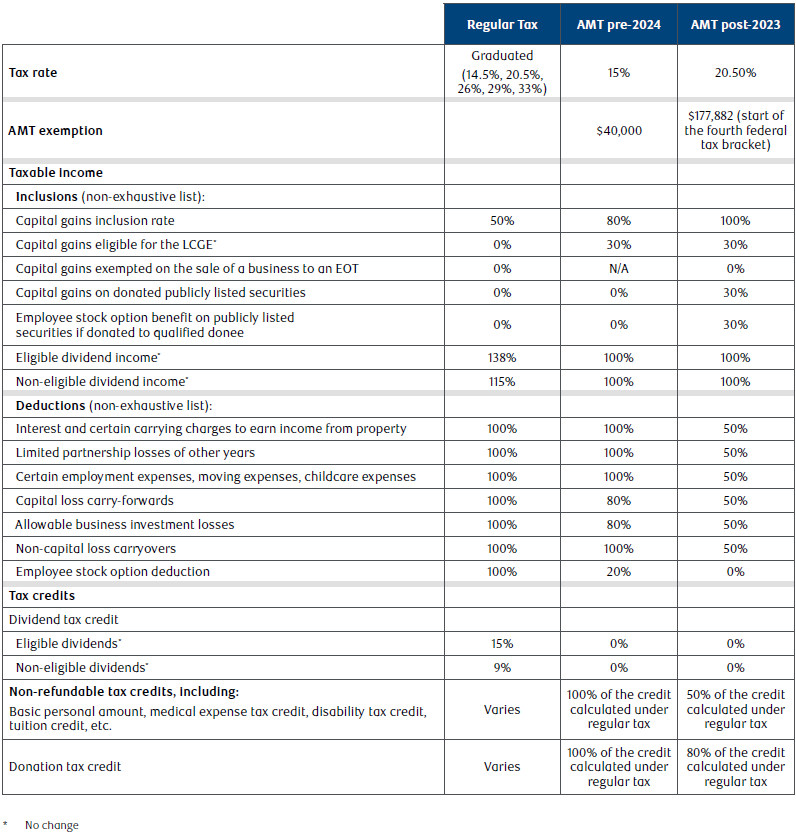

Refer to the appendix of this article for a table that compares the regular tax calculation with the pre-2024 and post-2024 AMT calculations.

When AMT Generally Won't Apply

AMT generally won't apply if:

• You have significant employment income and don't claim any large deductions or tax credits.

• The majority of your income is derived from fully taxed interest income or even tax-preferred dividend income. This is because the average tax rate on dividend income above the AMT basic exemption ($177,882 for 2025) is greater than the AMT rate of 20.3%. As such, AMT won't likely apply if you receive only dividend income (eligible or non-eligible), even if it's a significant amount.

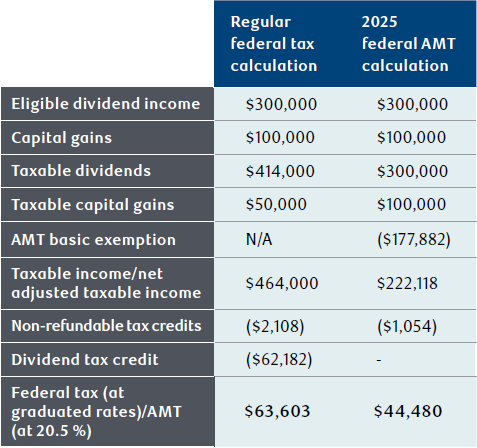

Here's an example of when AMT won't apply.

The table above illustrates a comparison of your estimated federal tax liability with your estimated AMT liability. In this scenario, you sell your qualified farm property or qualifying small business corporation shares and claim the LCGE. This is because 30% of the capital gains eligible for the LCGE are included in income for AMT purposes.

The scenario assumes you've earned $300,000 of eligible dividends and $100,000 of capital gains for the year. The regular federal tax is $63,603, and the 2025 federal AMT is $44,480. Since the regular tax of $63,603 is greater than AMT of $44,480, you'd have no AMT liability.

Who Could Be Affected by AMT?

Here are some common examples of when AMT may be triggered:

• You sell your qualified farm property or qualifying small business corporation shares and claim the LCGE. This is because 30% of the capital gains eligible for the LCGE are included in income for AMT purposes.

• You make a sizable donation to registered charities during your lifetime, especially where you donate publicly listed securities in-kind. Only 80% of the donation tax credit is allowed for AMT purposes, and 30% of the capital gain realized on the donation of the security in-kind is included in income for AMT purposes. Keep in mind that AMT doesn't apply in the year of death or to GREs.

• You invest in tax shelters, such as flow-through shares and limited partnership units, which may allow you to take large deductions and claim tax credits. As briefly mentioned before, the proposal to eliminate this adjustment in calculating ATI has not yet been re-introduced by the new government at the time of publishing this article.

• You derive your income solely from capital gains that are subject to the 50% inclusion rate. This is because the federal AMT rate of 20.5% is higher than the regular top federal rate on capital gains of 16.5% (33% multiplied by 50% inclusion rate). As such, realizing a significant amount of capital gains with a 50% inclusion rate can trigger AMT, subject to the exemption threshold and income from other sources.

• You claim a deduction for a net capital loss carry-forward on your current year tax return. For example, if you realized a capital loss in a prior year and couldn't use the loss in that year, it becomes a net capital loss. This net capital loss can be used to reduce taxable capital gains in any of the three preceding years or in any future year. If you carry forward that capital loss to a future year, only 50% of it can be applied to reduce capital gains for AMT purposes (as opposed to 100% for calculating regular income tax). As an example, if you incur a capital loss of $10,000 in a year and a capital gain of $10,000 in the following year, you can carry forward the capital loss to offset the capital gain the following year. In calculating your ATI, the entire capital gain of $10,000 is taxable but only 50% of the capital loss carried forward of $5,000 can be claimed. Therefore, for AMT purposes, your taxable amount would be $5,000 whereas your taxable amount for regular income tax purposes is NIL.

• You borrow money to invest and earn income from property such as interest, dividends or rental income and you deduct your interest expense. You may have borrowed using a line of credit or using a prescribed rate loan. The new AMT rules limit the deduction of interest and certain carrying charges to 50% for AMT purposes.

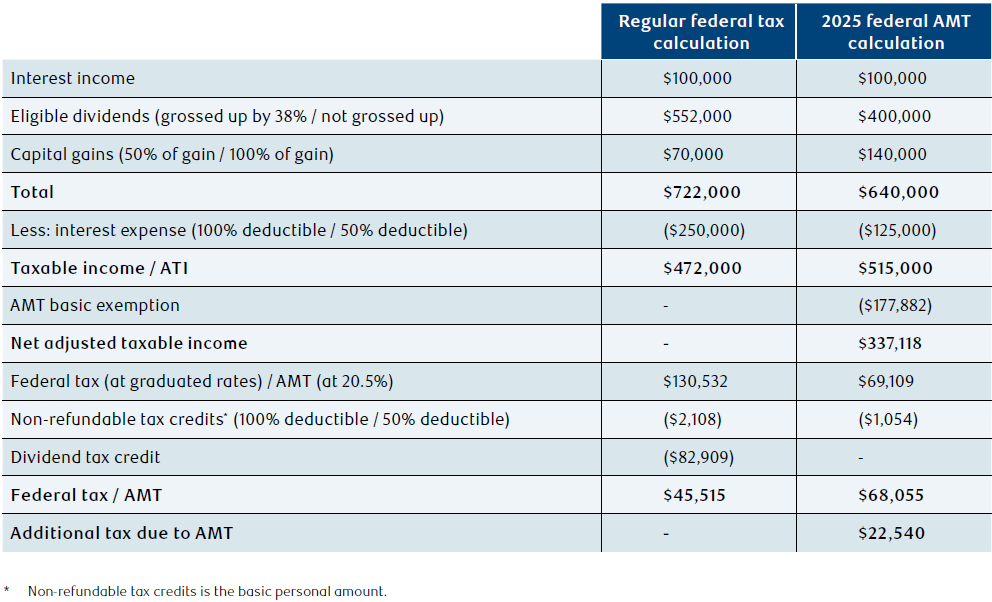

Here's an example of when AMT will apply.

The table above illustrates a comparison of your estimated regular federal tax and AMT, assuming you have an investment portfolio of which a portion was invested with borrowed funds. Your portfolio earns $100,000 of interest income, $400,000 of eligible dividends, and $140,000 of capital gains. Due to your borrowings, you have an interest expense of $250,000 for the year.

Since the minimum tax of $68,055 is greater than the regular tax of $45,515, you'd have an AMT liability and owe $68,055 in federal taxes.

Planning Opportunities

If you think you might be subject to AMT, speak with a qualified tax advisor to determine your AMT exposure as well as the potential steps you may take to reduce AMT. For example, if you plan on making a large charitable donation, selling assets that may trigger a significant capital gain or exercising employee stock options that benefit from the stock option deduction, you may want to look at the timing of your transactions. To minimize AMT, you can consider making donations, exercising your employee stock options or selling assets gradually, if possible.

It's also now important to try to match capital gains and capital losses in the same year to avoid the 50% AMT adjustment for capital loss carry-overs. So in a year when you incur capital losses, it may make sense to trigger some capital gains to absorb the losses in the same year.

If you've previously paid AMT and have an expiring AMT carry-over, speak with your qualified tax advisor about making use of it. Since the AMT carry-over can't be carried back to prior years and the carry-forward expires after seven years, it's important you have proper planning in place if you've paid AMT or expect to be affected by AMT in the future.

For example, if you have an AMT liability or are unable to use expiring AMT carryovers, you may defer claiming an RRSP deduction to increase your regular taxes payable. RRSP deductions can be carried forward indefinitely, so you can always claim them in a future year when you're not affected by AMT. You may also consider paying down loans to reduce a large tax-deductible interest expense. Similarly, you can consider generating additional taxable income, perhaps through RRSP or RRIF withdrawals. If you're an incorporated business owner, you can review your remuneration strategy and consider drawing a higher salary and dividends from the corporation or making charitable donations in your corporation rather than personally.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

Appendix

The appendix table compares the regular tax calculation with the pre-2024 and post-2023 AMT calculations.