Income splitting and the attribution rules

If you're a high-income earner and you support family members who earn little or no income, you may be able to reduce the overall amount of income tax paid by your family by income splitting. Income splitting between family members is recognized as acceptable tax planning, but the income attribution rules restrict the use of certain income splitting strategies. This article discusses the various attribution rules as well as income splitting strategies that may help leave your family with more available funds.

If you're a high-income earner and you support family members who earn little or no income, you may be able to reduce the overall amount of income tax paid by your family by income splitting. Income splitting between family members is recognized as acceptable tax planning, but the income attribution rules restrict the use of certain income splitting strategies. This article discusses the various attribution rules as well as income splitting strategies that may help leave your family with more available funds.

Family Office Services

June 14, 2025

Income splitting and the attribution rules

If you're a high-income earner and you support family members who earn little or no income, you may be able to reduce the overall amount of income tax paid by your family by income splitting. Income splitting between family members is recognized as acceptable tax planning, but the income attribution rules restrict the use of certain income splitting strategies. To determine whether you may benefit from family income splitting, it's important to understand how attribution works. This article discusses the various attribution rules as well as income splitting strategies that may help leave your family with more available funds to meet other financial planning goals.

Any reference to a spouse in this article also includes a common-law partner.

Income splitting

In Canada, each individual separately reports the income they earn and pays tax based on a progressive tax system (i.e., as your taxable income increases, the marginal tax rate that applies to the next dollar of taxable income increases). As such, a family where one spouse is a high-income earner will pay more tax than a family with the same household income but where both spouses earn equal amounts.

Income splitting is a strategy that takes advantage of the progressive tax system so that a family can retain more after-tax income. It involves shifting income from a family member in a higher tax bracket to one in a lower tax bracket. To achieve effective income splitting, it's important to understand the attribution rules that are designed to prevent family income splitting in certain circumstances.

Attribution rules

In specific cases, if you transfer or loan property to a family member, any investment income or loss, as well as any taxable capital gain or allowable capital loss from that property (or substituted property), may attribute back to you to be reported on your income tax return, rather than your family member's return. Generally, the attribution rules apply to income from property (passive investment income and gains) but not business income, except in the case of low- or no-interest loans to non-arm's length adults. In addition, the attribution rules don't apply to transfers of property for fair market value (FMV) consideration or to loans at the lower of a commercial interest rate or the Canada Revenue Agency's (CRA) prescribed interest rate at the time the loan is made, if the annual interest is paid within 30 days after each year-end. Essentially, whether attribution applies depends on who the property is being transferred to, their relationship to the transferor and the type of income being earned.

Transfers and loans to a spouse

If you transfer or loan (at low or no interest) property to your spouse, any income or loss, as well as any taxable capital gain or allowable capital loss from that property (or substituted property), will attribute back to you.

Transfers and loans to a minor

If you transfer or loan (at low or no interest) property to a minor who you don't deal with at arm's length, such as your child or grandchild, or to a minor who is your niece or nephew, the income or loss from that property (or substituted property) will attribute back to you. Any capital gain or loss from that property is taxed or claimed in the hands of the minor. For purposes of the attribution rules, a minor is a person who has not turned age 18 by the end of the taxation year.

You're deemed not to be dealing at arm's length with anyone you're related to, as defined in the Income Tax Act (ITA). Individuals connected by blood relationship, marriage or common-law partnership or adoption are related. But under the ITA, you're not related to your niece or nephew. A more detailed discussion on "related" is beyond the scope of this article. For unrelated persons, it's a question of fact whether you're dealing with that person at arm's length.

Transfers and loans to a non-arm's length adult

You can transfer assets to an adult, including a non-arm's length adult (such as a child, grandchild, sibling or parent), without attribution. However, if you make a low- or no-interest loan to a non-arm's length adult and one of the main reasons for the loan is to reduce or avoid tax by causing the income from the loaned property (or substituted property) to be included in the income of the borrower instead of in your hands, any income or loss (which may include business income or loss) from that property may attribute back to you. Any taxable capital gain or allowable capital loss from that property will not attribute back to you.

Transfers and loans to a trust

If you transfer or loan (at low or no interest) property to a trust for the benefit of your spouse or a minor who you don't deal with at arm's length or your minor niece or nephew, any income earned on the property (or substituted property) that the trust pays or makes payable to these individuals may attribute back to you.

Where you've made a low- or no-interest loan to the trust (but not a gift) and income earned on that property is paid or made payable to a non-arm's length adult beneficiary (not your spouse) and one of the main reasons for the loan is to reduce or avoid tax by causing the income from the loaned property to be included in the income of the beneficiary instead of in your hands, that income may attribute back to you.

Any taxable capital gains from the property (or substituted property) transferred or loaned to the trust and paid or made payable to your spouse would attribute back to you. If instead the taxable capital gains are paid or made payable to minor beneficiaries or a non-arm's length adult beneficiary, attribution wouldn't apply.

Reversionary trust rules (super attribution)

These rules may apply if a Canadian resident trust holds property on condition that:

• the property may revert to the person who contributed it; or

• the person who contributed the property can determine, after the trust is created, who can receive the property; or

• the property cannot be disposed of except with the contributor's consent or in accordance with their direction.

As an example, the first condition may be met where the settlor is also a capital beneficiary of the trust or if the trust is a revocable trust. The second and third conditions may be met where the settlor or a contributor is the sole trustee of the trust.

When the super attribution rules apply, income or losses, as well as taxable capital gains or allowable capital losses from the property transferred to the trust (or substituted property), are attributed back to the contributor of the property. In addition, the trust capital cannot be rolled out to the beneficiaries at cost during the contributor's lifetime. An exception to this rule is where the contributor of the property or their spouse is a capital beneficiary of the trust, and the terms of the trust allow it, the trust property can be rolled out at cost to either of these two individuals.

The super attribution rules don't apply to property or income earned on that property, if it's a genuine loan to the trust. The loan must not be part of the terms of the trust. The super attribution rules also don't apply to a genuine sale of property at FMV to the trust by a beneficiary.

If you're considering using a trust for income splitting, the best defence against the attribution rules is to carefully consider the settlement of the trust, the parties to the trust and the types of transactions that take place with the trust. As such, it's strongly recommended that you seek the assistance of a qualified tax or legal advisor in setting up the trust.

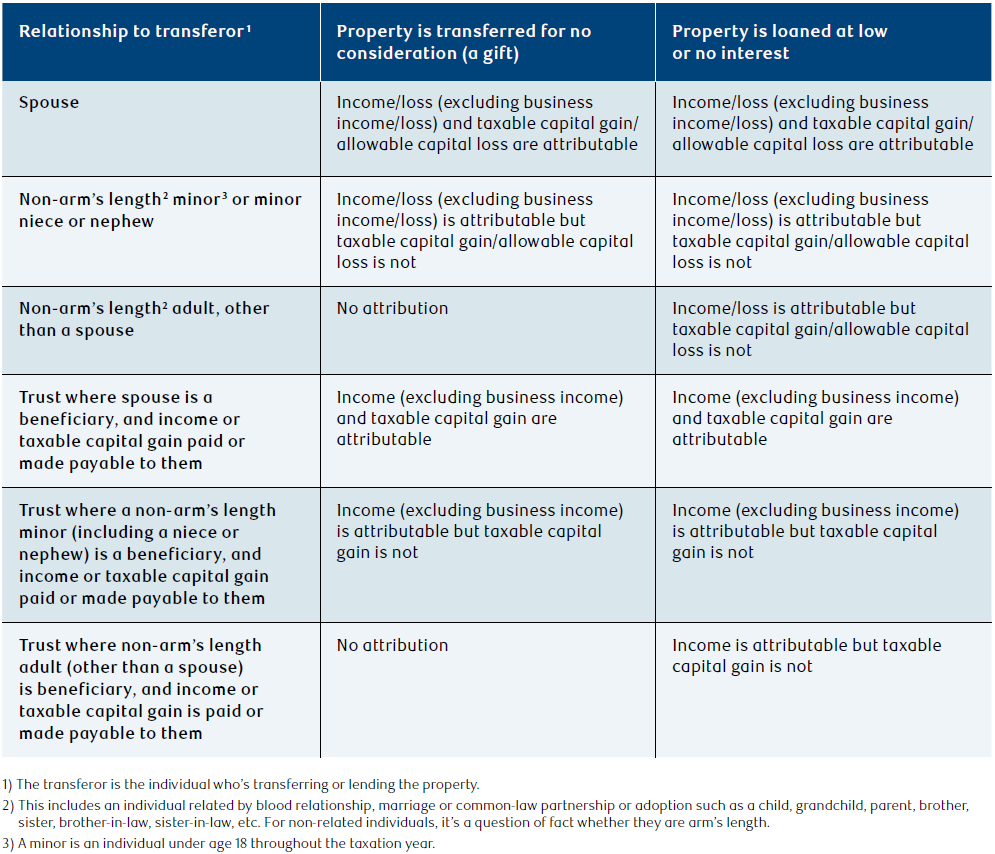

Summary of attribution rules

The following table summarizes the attribution rules.

Tax on split income (TOSI)

The TOSI rules aren't attribution rules, but they do affect income splitting. They're designed to discourage splitting income from a related business with family members who don't meaningfully contribute to the business. This article doesn't include a discussion of the TOSI rules, but it's important to also determine if the TOSI rules will apply to any income splitting strategy you're considering. This should be reviewed by a qualified tax advisor.

Dispositions on transferring property

Property includes cash but could also be assets with an accrued gain or loss. If you transfer property, other than cash in Canadian dollars, to your spouse, it's automatically deemed to be disposed of at cost unless you elect to have it transfer at FMV when you file your tax return for the year of transfer. You will also have to report the taxable capital gain or allowable capital loss when your spouse eventually sells that property because of the attribution rules.

Instead, if you elect to transfer property to your spouse at FMV and your spouse pays you FMV consideration for the property transferred, the taxable capital gain or allowable capital loss on a subsequent sale of the property by your spouse will not attribute back to you. If you transfer property in a loss position at FMV to your spouse, you cannot realize the loss because of the superficial loss rules. For more information on the superficial loss rules, please ask your RBC advisor for the article on this topic.

If you transfer property with an accrued gain or loss to a non-arm's length individual other than your spouse, you will be deemed to have disposed of it at FMV, resulting in a gain or loss on the date of transfer. You'll need to report this gain or loss on your tax return.

Strategies for income splitting with your spouse

Although the attribution rules may restrict the income splitting opportunities available to you, there are still several ways you can split income with family members. The following income splitting strategies may help you achieve tax-efficiency by equalizing your and your spouse's income.

Invest your lower-income spouse's earnings

If your spouse works or has other sources of income and pays tax at a lower marginal tax rate than you do, consider paying for all of the family's living expenses and tax obligations. This will allow your spouse to save their earnings and build an investment portfolio in their own name. The income and capital gains earned in the account will not attribute back to you and will be taxable to your spouse at their lower marginal tax rate since the investments are funded with their own money.

Gift to your spouse to contribute to a tax-free savings account (TFSA)

You can gift money to your spouse for them to contribute to their own TFSA. Attribution will not apply while the money or substituted property is held in the TFSA and to the extent your spouse doesn't, at the time of contribution, have an excess TFSA amount. This strategy can help your spouse earn tax-free investment income and save for retirement or other goals. If your spouse withdraws the gifted money or substituted property from the TFSA and it's invested, the attribution rules will apply to any future income or losses or taxable capital gains or allowable capital losses from the property.

Earnings on invested income (second-generation earnings)

If you transfer or loan (at low or no interest) property to your lower-income spouse, any income or loss, or taxable capital gain or allowable capital loss from that property (or substituted property), will attribute back to you. However, if the income (but not capital gains) is invested by your spouse, the attribution rules will not apply to any investment earnings (second-generation earnings) from the reinvested income and can be taxed in your spouse's hands at their lower marginal tax rate. The income that can be reinvested with no further attribution does not include any capital gains realized on the transferred or loaned property (or substituted property). Income for this purpose includes interest, dividends, rents or royalties.

You can track the annual income carefully or maintain separate accounts for the original funds and the investment income earned. Over several years, this strategy can result in your lower-income spouse accumulating capital for investment where the earnings will be taxed in their hands.

For example, Mrs. Smith gifts $100,000 to Mr. Smith, her lower-income spouse, who invests the funds and earns 5% of interest income. The $5,000 of interest income is taxed in Mrs. Smith's hands because of the attribution rules, but the earnings become Mr. Smith's capital which he can then reinvest. The future income/loss or taxable capital gains/allowable capital losses earned on the $5,000 would be taxable to Mr. Smith going forward.

If, instead, Mr. Smith bought shares with the $100,000 gifted from Mrs. Smith and sold the shares for $105,000, this would result in a taxable capital gain, which would be attributed to Mrs. Smith and taxed in her hands. If Mr. Smith used the $105,000 to purchase other shares, any dividends earned on the entire $105,000 would continue to be attributed to Mrs. Smith. If Mr. Smith then put those dividends into a separate account, any income/loss or taxable capital gain/allowable capital loss earned on the reinvested dividends would not attribute to Mrs. Smith.

Use a prescribed rate loan

This strategy involves you loaning funds to your spouse at the CRA's prescribed interest rate at the time the loan is made. Your spouse will then invest the loaned funds for the purpose of generating investment income which may include interest, dividends and capital gains. This investment income will be taxable to your spouse at their lower marginal tax rate, which effectively reduces your family's overall tax bill. Your spouse must pay you annual interest on the loan by January 30 of the following year (and by January 30 of every subsequent year the loan is in place). If the interest payment is late by even one day, the attribution rules will apply for that particular year and all subsequent years. You must include the interest your spouse pays you on the loan as income when you file your income tax return. This strategy can result in tax savings when the interest your spouse pays you is less than the income they earn by investing the borrowed funds.

Transfer capital losses from your spouse to you

If your spouse has unrealized capital losses that they're unable to use personally and you have taxable capital gains that would be subject to tax, your spouse may be able to transfer their unrealized capital losses to you. Even if your spouse can use the losses themselves, they may want to transfer the capital losses to you if you're in a higher marginal tax bracket and have taxable capital gains that would otherwise be subject to tax at a higher marginal rate.

If your spouse simply transfers their securities to you, they'll automatically roll over to you at cost and the attribution rules will prevent the loss from being realized in your hands when the securities are sold. Instead, the strategy involves your spouse selling the loss securities to you for FMV consideration and electing out of the rollover rules. It's important that you pay FMV consideration for the securities. You then trigger the superficial loss rules by holding the securities for at least 30 days before selling them on the market. Triggering the superficial loss rules denies your spouse from claiming the capital loss but allows the capital loss to be added to the adjusted cost base (ACB) of the securities which now belong to you. You can then sell the securities at a loss and claim the capital loss to offset capital gains.

Transfer future growth of a security to your spouse

If you own a security that you anticipate may increase in value, consider transferring it to your spouse so that any future capital gain will be taxed at your spouse's lower marginal tax rate. You can transfer the future growth either by:

• Transferring the security in-kind to your spouse, electing out of the rollover rules and having your spouse pay you FMV consideration using their own funds; or

• Selling the security on the open market and having your spouse purchase the same security with their own funds.

If your spouse purchases the security for FMV with their own funds, it will not trigger the attribution rules, and any future capital gain will be taxable in your spouse's hands.

Buy a non-income producing asset from your spouse

If your lower-income spouse has a non-income producing asset such as a family car, a piece of artwork, or jewellery, consider buying it from them for FMV and electing out of the rollover rules. Your spouse can invest the sale proceeds, and the income earned or capital gains realized on the invested funds will be taxable in their hands at their lower marginal tax rate. Keep in mind that your spouse may realize a capital gain on the sale of the asset to you.

Split eligible pension income

If you receive eligible pension income and pay tax at a higher marginal rate than your spouse, you may consider splitting up to 50% of that income with your spouse and have it taxed at their lower tax rate. Eligible pension income includes:

• RRIF or life income fund (LIF) income received by the plan annuitant if they're at least age 65 in the year. The age of the non-annuitant spouse is not relevant.

• Pension income from an employer plan received at any age by a plan member. A pension plan member who's a Quebec resident must be at least age 65 to split pension income on their Quebec income tax return.

Splitting eligible pension income can potentially reduce your family's tax bill and enable both you and your spouse to receive the $2,000 federal pension income tax credit. You may also be entitled to a provincial pension income tax credit. Since pension income splitting provides an opportunity to reallocate income from one spouse to another and reduce the net income of the higher-income spouse, it can reduce or eliminate the Old Age Security clawback or other government tested benefits. For a more detailed discussion, please ask your RBC advisor for the articles on pension income splitting and the pension income tax credit.

Contribute to a spousal registered retirement savings plan (RRSP)

The main advantage of a spousal RRSP is that it enables you and your spouse to income split by having any withdrawals taxed in the lower-income spouse's hands. Withdrawals from a spousal RRSP or registered retirement income fund (RRIF) will not attribute back to the higher-income spouse who made the RRSP contributions unless a spousal contribution was made in the year of withdrawal or the previous two calendar years. Also, minimum RRIF withdrawals from a spousal RRIF are not subject to the attribution rules.

Since RRIF income can be split between spouses under the pension income splitting rules, there's been some discussion as to whether contributing to a spousal RRSP still makes sense. The following are some of the key reasons that, even with pension income splitting available, using a spousal RRSP may still be a useful strategy for you and your spouse:

• You and your spouse retire prior to age 65 and need to make withdrawals from your RRSP or RRIF to supplement your retirement income. In this case, it may be beneficial to be able to draw on a spousal RRSP or RRIF owned by the lower-income spouse to fund the shortfall. Since RRIF income can't be split prior to age 65, withdrawals from the spousal RRSP or RRIF can be taxed at the lower-income spouse's marginal tax rate.

• The lower-income spouse retires before the higher-income spouse, who previously made contributions to the spousal RRSP. In this case, the lower-income spouse may be able to withdraw funds from their spousal RRSP or RRIF in retirement and be taxed at their lower marginal tax rate, assuming they're outside of the attribution period.

• You and your spouse have retirement income taxed at different marginal tax rates and you want to split more than 50% of your income. A typical scenario is where one spouse has significant investment income while the other spouse doesn't. If the spouse with the investment income has unused RRSP contribution room, they could make spousal RRSP contributions so that the spouse who's not earning investment income can receive RRSP or RRIF income in retirement to equalize their incomes.

• You're still working after age 71, have RRSP contribution room and want to benefit from an RRSP deduction. In this case, you can make a spousal RRSP contribution as long as your spouse is under age 72 in the year. This will allow you to claim an RRSP deduction to reduce your taxable income and have the future RRSP or RRIF withdrawals taxed in your spouse's hands.

Share Canada Pension Plan/Quebec Pension Plan (CPP/QPP) retirement benefits

If you receive a higher CPP/QPP retirement pension than your spouse, consider sharing your pension. To qualify for CPP/QPP sharing, certain conditions must be met, including the requirement that both you and your spouse must be at least 60 years of age and receiving or have applied for your benefits. You can apply to Service Canada or Retraite Québec to share CPP or QPP respectively.

By electing to share your pension, a portion of your retirement income may be shared with your lower-income spouse and taxed in their hands. The pension sharing process combines both your and your spouse's pension entitlements that have accumulated during the time you've lived together and reallocates 50% of the combined entitlements to each spouse.

Gift or loan funds to your spouse to finance a business

If you gift or loan funds to your spouse and they use the funds to earn business income, this income will not attribute back to you. It will be taxed in your spouse's hands. If you have funds earning investment income and you're in a high marginal tax bracket, this strategy may be an effective way to reduce your highly taxed investment income and provide capital to your spouse who's starting a business.

Pay your spouse a salary

If you're carrying on a business and have a spouse who's employed in the business, you can pay your spouse a salary, whether or not your business is incorporated. The amount of salary you pay your spouse must be reasonable based on the duties they perform. This strategy allows you to take advantage of your lower-income spouse's marginal tax rate. It'll also enable your spouse to make contributions to CPP/QPP and accumulate RRSP contribution room to help increase their retirement savings.

Strategies for income splitting with your child or grandchild

You may want to consider these strategies if you'd like to provide support for your child or grandchild and reduce your family's overall tax burden.

Gift to an adult child or grandchild

Since the attribution rules don't apply to outright gifts of property to an adult child or grandchild, consider gifting them funds, which they can invest. Any income earned or capital gains realized on the investments will be taxed in your child's or grandchild's hands at their lower marginal tax rate. If you gift an asset in-kind, you'll realize a disposition at FMV resulting in a capital gain or capital loss on the date of the transfer. You will need to report this gain or loss on your tax return.

Gift to an adult child or grandchild to contribute to a TFSA, first home savings account (FHSA) or RRSP

As the attribution rules don't apply to gifts to an adult child or grandchild, consider gifting them funds to contribute to their own TFSA, FHSA or RRSP. Any income earned or capital gains generated within these plans will not attribute back to you. In addition to reducing your income, this strategy can help your child or grandchild earn tax-free or tax-deferred investment income, claim tax deductions in the case of an FHSA or RRSP contribution, and save for other financial planning goals.

You can also gift (or loan) funds to an adult child or grandchild to purchase a principal residence. When your adult child or grandchild eventually sells the home, they may be able to use their principal residence exemption to eliminate the taxes on any capital gain. Beware that the value of the home may be exposed to your child's or grandchild's marital or creditor claims.

Use a prescribed rate loan to an adult child or grandchild

Similar to loaning to your spouse at the CRA's prescribed interest rate, you can loan funds to your adult child or grandchild at this rate and not have the attribution rules apply. It would also be important for the child or grandchild to pay you annual interest on the loan by January 30 of the following year (and by January 30 of every subsequent year that the loan is in place).

Use a family trust to gift or loan funds for the benefit of a child or grandchild

Since minors generally don't have the legal capacity to contract, they may not be able to open an account and invest funds on their own. You may want to use a family trust for income splitting, where the trustee can invest the funds for the benefit of a minor. You may also want to use a family trust so the trustee maintains control over the property you intend to benefit your child or grandchild. Income splitting with a minor is only possible if the trust is properly structured to avoid the super attribution rules previously discussed.

If the beneficiary of the trust is a minor child or grandchild, and you transfer or loan (at low or no interest) funds to the trust, there will be attribution to you of any income (e.g., interest and dividends) paid or made payable to the minor beneficiary. In contrast, the taxable capital gains realized and paid or made payable to the minor beneficiary can be taxed in their hands at their lower marginal tax rate. As such, you may want to invest the gifted or loaned funds in growth-oriented securities. As always, the investment merits of the securities should be considered along with the tax benefits.

If you loan funds to the trust at the CRA's prescribed interest rate at the time of the loan, the attribution rules shouldn't apply. To ensure the attribution rules don't apply, the trustee must pay you annual interest on the loan by January 30 of the following year and by January 30 of every subsequent year the loan is in place. To the extent that the investment income can be paid or made payable to the beneficiary, that income will be taxable to your child or grandchild at their lower marginal tax rate, which effectively reduces your family's overall tax bill.

If the beneficiary of the trust is an adult child or grandchild, you can gift funds to the trust or loan funds at the CRA's prescribed interest rate. In either case, the income earned or the taxable capital gains realized in the trust can then be taxed in your adult child's or grandchild's hands, to the extent it's paid or made payable to them.

Contribute to a registered education savings plan (RESP)

You can contribute to an RESP to save for your child's or grandchild's post-secondary education. The maximum lifetime contribution you can make to an RESP is $50,000 for each beneficiary. The federal government will also contribute to the plan by providing grants and bonds, in certain circumstances. Not only is the income earned in the plan tax-deferred, but also all the income as well as the government incentives paid to your child or grandchild as an education assistance payment are taxable to them at their lower marginal tax rate.

Contribute to a registered disability savings plan (RDSP)

You can contribute to an RDSP for a family member with a disability. The maximum lifetime contribution to an RDSP for a beneficiary is $200,000. The federal government will also contribute to the plan by providing grants and bonds, in certain circumstances. Not only is all the income earned in the plan available to the beneficiary, but also all the income as well as the government incentives will be taxable to the beneficiary at their lower marginal tax rate when they withdraw the funds.

Conclusion

Income splitting may be an effective way to reduce your family's overall tax burden, but to do so successfully it's important to understand and stay clear of the attribution rules. These rules are very complex and there are many of them. A discussion with a qualified tax advisor will help ensure that your personal situation and objectives are carefully reviewed to address and maximize the effectiveness of any available income splitting strategies.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.