Family Office Services

October 14, 2025

Income Splitting Using a Prescribed Rate Loan

You may be able to reduce the overall amount of income tax paid by your family by setting up a prescribed rate loan to split income. This article explains how prescribed rate loans work. Any reference to a spouse in this article also includes a common-law partner.

Using a Prescribed Rate Loan

The Income Tax Act (ITA) contains "attribution" rules and other anti-avoidance rules that generally do not allow or limit income splitting with certain family members (these are discussed later in the article). The application of these rules means that income and, in some cases, capital gains earned on funds provided by a higher-income individual to lower-income family members for investment is taxable to the higher-income individual; as a result no tax savings are achieved.

However, the ITA also contains rules that allow you to ensure the attribution rules do not apply and achieve your income-splitting objectives in very specific circumstances. One circumstance in which the attribution rules do not apply is where a "loan for value" is made to lower-income family members or to a trust for the benefit of lower-income family members. A loan for value includes (but is not limited to) a formal loan arrangement that satisfies the following conditions:

• The rate of interest charged on the loan is at the Canada Revenue Agency (CRA) prescribed interest rate at the time the loan is made, and

• The annual interest is paid every year no later than 30 days after the taxation year (by January 30)

Where a loan for value, also known as a prescribed rate loan, is properly implemented and administered, income and capital gains earned on the borrowed funds can be taxed in the borrowing family member's hands.

A prescribed rate loan strategy allows you to shift investment income and capital gains that would otherwise be taxed in your hands at a high marginal tax rate to the hands of your lower-income family members, including your spouse, adult children or minor children through a trust. By splitting income with your lower-income family members, you may be able to reduce your family's overall tax bill.

The CRA Prescribed Rate

Every quarter, the CRA updates and publishes the prescribed interest rates. The rate is based on the average 90-day T-bill rates of the first month of the previous quarter. To implement a prescribed rate loan, the interest rate on your loan should be the CRA prescribed rate in effect during the quarter that you make the loan. Even if the prescribed rate changes in the future, the interest rate on the outstanding prescribed rate loan remains the same.

The CRA considers a loan to be a low-interest loan if the interest rate charged on the loan is below the lesser of the CRA prescribed interest rate or a commercial interest rate that would be agreed to by arm's length parties. Low-interest or no-interest loans to your spouse or minor child may trigger the income attribution rules. Low-interest or no-interest loans to any other non-arm's length adult may also trigger the attribution rules if one of the main reasons for making the loan is to split income.

Examples of How Prescribed Rate Loans Can Be Used

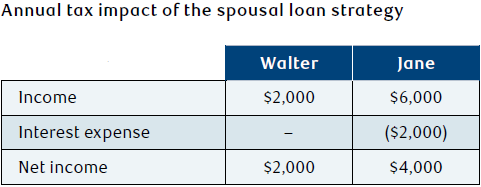

Example of a Prescribed Rate Loan to a Spouse (the "Spousal Loan Strategy")

Walter has excess cash and wants to utilize a loan at the CRA prescribed rate to split income with his spouse, Jane. Jane signs a promissory note to Walter for $200,000, which is payable upon demand at the prescribed rate of 1% (prescribed rate at the time the loan was made), with interest paid annually.

Jane invests the $200,000 and generates an annual return of 3% in interest income, or $6,000. If the loan is outstanding for the entire year, Walter will receive $2,000 of interest income from Jane, while Jane will have $6,000 of investment income with a deduction of $2,000 for the interest she paid to Walter. Generally, the timing of the income inclusion or deduction on the prescribed rate loan depends on the year the interest is related to, when the interest is received or paid, and the method (cash vs. accrual) the individual regularly follows in computing their income.

Walter, who is in the top tax bracket, is able to shift $4,000 of taxable income to Jane, who is in a lower tax bracket. If there is a 20% difference between their tax brackets (e.g. 45% versus 25%), then the family will save $800 ($4,000 x 20%) on their total tax bill annually. If you would like more information about a prescribed rate loan to your spouse, ask your RBC advisor for the article on the spousal loan strategy.

Example of a Prescribed Rate Loan to an Adult Child

Judy believes she has accumulated more than enough wealth to live comfortably, and she dislikes paying income taxes at the highest marginal tax rate. Her 19-year-old son, Jimmy, however, has no taxable income. If Judy could find a way to split her income with Jimmy, the family could reduce their total tax liability.

Judy approaches her advisor at RBC, who understands her present situation and overall objectives. As Jimmy is still a young adult, Judy is not comfortable making an outright gift to him to achieve family income splitting. To be able to maximize the benefits of family income splitting with Jimmy, her RBC advisor recommends that she consider approaching her qualified tax advisor to discuss the merits of income splitting with Jimmy through the use of a loan at the CRA prescribed rate.

To illustrate the benefits of family income splitting, let's assume Judy is considering investing $100,000 in a bond yielding 3% (interest is paid annually). Through discussions with her RBC advisor and her qualified tax advisor, she decides to lend $100,000 to Jimmy to enable him to purchase the bond.

At the beginning of the year, Judy loans $100,000 to Jimmy at the CRA prescribed interest rate, which at the time is 1%. Jimmy earns interest income of $3,000 annually on his investment in the bond and reports it on his income tax return. He has no other sources of income. He is required to pay Judy $1,000 a year in interest but he can deduct this expense on his tax return. The resulting $2,000 of net taxable income does not attract any income tax since this amount is less than Jimmy's basic personal tax exemption.

Judy must report the interest income Jimmy is paying her on the loan, so she is reporting 1% instead of the 3% she would have reported if she bought the bond herself. As Jimmy is earning 2% tax-free (3% net of the 1% interest expense), the combined family tax bill is lower than if Judy had earned the bond interest in her name.

Jimmy must pay the interest on the loan for the current year to Judy no later than January 30 of the following year. Judy must include the interest on the loan on her income tax return. Generally, the timing of the income inclusion or deduction on the prescribed rate loan depends on the year the interest is related to, when the interest is received or paid and the method (cash vs. accrual) the individual regularly follows in computing their income.

Important Factors to Keep in Mind

You may want to keep these factors in mind when considering a prescribed rate loan strategy:

• To make this strategy worthwhile, not only should the invested funds generate a return at least equal to the interest expense on the loan and any additional administrative costs, but the borrower must also be able to actually pay the interest to you each year by the deadline (January 30 of the following year) to avoid the application of the attribution rules.

• The prescribed rate loan strategy may not be tax-effective for your family if you plan to invest in a very tax-efficient portfolio (e.g. deferred capital gains, return of capital, etc.). In this case, the taxes you pay on the loan interest may exceed any tax savings that result from shifting the investments to your lower-income family member. If there is no annual income being generated, there is no tax, therefore no tax savings. The point of a prescribed rate loan is to shift highly taxed income to lower-taxed family members so that there are more after-tax funds available.

• If you dispose of appreciated securities to fund the loan, you will trigger capital gains, on which income tax will be payable. Even if you transfer securities to the borrower and take back a promissory note, you may trigger income tax consequences that can be more complex than liquidating and loaning cash instead.

• Once you formally establish a prescribed rate loan, the rate applies for the life of the loan, even if prescribed rates subsequently increase or decline. There is no legislative restriction on the amount of the loan or the term of the loan. It's possible to implement a prescribed rate loan strategy using a demand loan.

• In the first year of the loan, the amount of interest payable should be pro-rated based on the number of days in the year that the loan is outstanding. This is also the case if the loan is repaid during a year.

• If the annual interest payment is not paid to you by January 30 of the following year, the attribution rules will apply and you will have to report and pay income tax on the investment income earned on the loaned funds. Even if this deadline is missed by one day, the attribution rules will be triggered. Once this occurs, attribution will apply to the year that the deadline was missed, and all subsequent years. In other words, your income-splitting strategy will be rendered ineffective.

• The rules require that interest payments made by the borrower should be done using their own funds. The payment of interest from a joint account held between the lender and borrower may be problematic, as it may be more difficult to demonstrate that the interest payment is made from the borrower's own funds. The borrower should document the interest payments on the loan for the relevant tax year and there should be an actual traceable payment made.

• It's possible that over the lifetime of the loan, as a result of market fluctuations, you may not achieve maximum income splitting for a certain period. You may be tempted to recall the loan during that time. Keep in mind that if the investment portfolio in which the loan proceeds are invested has declined in value, there may not be sufficient funds to repay the loan. This could result in negative tax consequences. Be sure to discuss any tax consequences that may result from the repayment of the loan with a qualified tax advisor.

• If you establish a prescribed rate loan and the CRA prescribed rate falls, it could be to your advantage to call your current loan and establish a completely new loan at the lower rate. However, the process of modifying an existing loan requires careful steps, since the income attribution rules could be triggered if it's not executed correctly. For more information, ask your RBC advisor for a copy of the article on modifying a prescribed rate loan.

• You should ensure that the demand loan remains legally enforceable. Some legal advisors believe that making the annual interest payments on the prescribed rate loan is sufficient action to avoid the loan from becoming unenforceable. Making the interest payment annually is an acknowledgement by the borrower that the loan is still outstanding and enforceable. The alternatives are to renew the promissory note on an annual basis or to have the borrower acknowledge in writing that the promissory note is still valid. You should consult with a qualified legal advisor to determine what is required to keep the loan enforceable in your jurisdiction.

• If you pass away while your loan remains outstanding, and your Will doesn't address how the loan is to be dealt with on your death, the loan will generally need to be repaid by the borrower to your estate. This may have tax consequences for the borrower. If you want the loan to remain in place or you would like the loan to be forgiven on your death, you should include these instructions in your Will. If you forgive the loan in your Will, the debt forgiveness rules in the ITA are not triggered. A discussion of these rules is beyond the scope of this article.

• If the borrower passes away while the loan is outstanding, the loan will also generally need to be repaid by the borrower's estate. If there are insufficient assets to repay the loan, this could have negative tax consequences.

Alternative Minimum Tax (AMT)

Alternative Minimum Tax (AMT) is a parallel tax calculation designed to prevent individuals and certain trusts from paying little or no tax by limiting the tax advantages they could receive in a year through certain tax preferences, such as claiming certain deductions or earning tax-preferred income. You pay either the regular tax or the AMT, whichever is highest. In recent years, the government has introduced a number of changes to the AMT that may have broadened the impact it may have to high-income earners and most trusts.

For AMT purposes, you can only deduct 50% of deductible interest expense instead of 100% for regular tax purposes. This rule may have a significant impact on a borrowing spouse or a family trust that is deducting the interest paid on the prescribed rate loan.

To read more about the AMT and how the AMT may impact trusts, please ask your RBC advisor for the articles on these topics.

Due to the potential impact of the AMT, the effectiveness of a prescribed rate loan may not be as great as it once was. Be sure to speak with your qualified tax advisor about ways to mitigate the effects of the AMT if you are considering a prescribed rate loan.

Gifting Versus Prescribed Rate Loan

It's possible to income split by making an outright gift of assets to adult family members, other than a spouse. Income and capital gains earned on the gifted funds can be taxed in the adult family member's hands (other than a spouse). Gifting assets to a spouse or minor child, however, triggers the attribution rules, and prevents income, and capital gains in the case of a spouse, from being taxed in their hands. On the other hand, if properly implemented, a prescribed rate loan may enable all income and capital gains earned on the loaned capital to be taxed in the hands of any of your lower-income family members.

Gifting assets reduces your net worth and future income taxes; it also reduces income and probate taxes on death because you no longer own the assets. When you make a gift, however, you are giving up control of and access to these assets and may potentially be jeopardizing your financial security. If you are concerned about this, a prescribed rate loan may be appropriate, as it allows you to maintain access to your capital should you need it, and maximize the potential for income splitting with your family members.

Attribution Rules

A simple transfer of funds to your spouse or minor children, or a low or no-interest loan to your spouse, adult children or minor children through a trust, doesn't achieve maximum family income splitting due to the attribution rules. The following sections explain how the attribution rules could affect income splitting.

Spousal Attribution

If you gift or loan (at low or no interest) funds to your spouse, any investment income or loss and capital gain or loss earned on the funds, or substituted property, will be taxable in your hands because of the attribution rules. You cannot simply transfer assets to your lower-income spouse in the hope of having the income taxed in your spouse's hands. However, you can avoid the attribution rules by implementing a prescribed rate loan (spousal loan strategy) in accordance with the terms and conditions described earlier.

Attribution and Adult Children

The income and capital gains earned on funds transferred as a gift to an adult child is not attributed back to the parent; therefore, any outright gift will achieve family income splitting.

When a gift is made, it's generally not revocable and consequently, the parent making the gift loses control of and access to the funds. As a parent, you may not be comfortable with that for a number of reasons. In order to retain access to the funds, you may want to loan funds to your adult child, instead of making a gift, as you can generally recall a loan. However, when a low or no-interest loan is made to an adult child and one of the main reasons for making the loan was to reduce or avoid tax by causing income from the loaned property to be included in the income of your adult child, then generally interest and dividend income, but not capital gains or losses, earned on the loaned funds (or substituted property) will be taxed to the parent who made the loan instead of in the hands of the adult child. These rules also apply to low- or no-interest loans that you make to a non-arm's length adult individual where one of the main reasons for the loan is income splitting. These attribution rules don't apply if you charge interest on the loan at the CRA prescribed rate in accordance with the terms and conditions described earlier.

Attribution and Minor Children

If you gift or loan (at low or no interest) funds to your minor child to invest, typically through a trust arrangement, any interest and dividends earned on the funds, or substituted property, that is paid or made payable to the minor, will attribute back to you and be taxed in your hands. Capital gains earned on the funds, or substituted property, are not subject to attribution. Where the taxable capital gains are earned in a properly structured trust for the minor's benefit and are paid or made payable to the minor, the taxable capital gain will be taxed in the minor's hands.

Attribution and Trusts ("Super Attribution")

Special attribution rules, which we refer to as the "super attribution" rules, may apply if a Canadian resident trust holds property on condition that:

• The property, or substituted property, may revert back to the person from whom the property was received

• The person from whom the property was received has the power to determine who receives the property, or substituted property, after the creation of the trust, or

• During the lifetime of the person from whom the property was received, the property cannot be disposed of without their consent or direction

Examples of when the first condition may exist is where the settlor is also a capital beneficiary of the trust or if the trust is a revocable trust. One example of when the second and third conditions may exist is where the settlor is the sole trustee of the trust.

When the super attribution rules apply, income or losses and taxable capital gains or allowable capital losses on the property transferred to the trust (or substituted property) are attributed back to the person from whom the property was received. In addition, the trust property cannot be rolled out to beneficiaries at cost during the contributor's lifetime. If the person from whom the property was received or their spouse is a capital beneficiary of the trust and the terms of the trust allow it, then the trust property can be rolled out at cost to either of these two individuals.

Conclusion

Reducing the family tax bill is the main benefit of family income splitting. A prescribed rate loan between a higher-income earner and lower-income family members may be a way to achieve this. Keep in mind, though, that a prescribed rate loan does need to be properly implemented and managed. It's not a "set up and forget" strategy, as you'll need to ensure that the correct interest payments are made on time annually. Speak with a qualified tax advisor about whether this strategy makes sense in your circumstances and to assist you with the implementation and management of the strategy.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.