Income taxes at death

An individual's obligation to pay income tax and file an income tax return(s) continues in the year of death. This responsibility will generally be carried out by the deceased's legal representative. This article provides some information that may assist in fulfilling your requirements specific to the taxation of a deceased individual.

An individual's obligation to pay income tax and file an income tax return(s) continues in the year of death. This responsibility will generally be carried out by the deceased's legal representative. This article provides some information that may assist in fulfilling your requirements specific to the taxation of a deceased individual.

Family Office Services

October 14, 2025

Income taxes at death

Information for legal representatives of a deceased person

An individual's obligation to pay income tax and file an income tax return(s) continues in the year of death. This responsibility will generally be carried out by the deceased's legal representative. This article provides some information that may assist in fulfilling your requirements specific to the taxation of a deceased individual. In this article, any reference to a spouse includes a common-law partner and a spousal trust includes a common-law partner trust.

Responsibilities of the legal representative

You're likely the legal representative for the deceased person if you're named as the executor or estate trustee in their Will, you're appointed as the administrator of their estate by a court, or you're the liquidator for their estate in Quebec.

As the legal representative, you have a number of responsibilities and duties. One such duty includes notifying government authorities, such as the Canada Revenue Agency (CRA) and Service Canada, as soon as possible of the individual's date of death.

Under the Income Tax Act, you're responsible for filing all required tax returns for the deceased and making sure all taxes owing are paid. You may also be required to file a T3 Trust Income Tax and Information Return (Trust return) for income earned after the date of death by the estate or by a testamentary trust created by the terms of the Will, if you are appointed as the trustee of this trust. Sometimes, it may not be necessary to file a trust return if the estate is distributed immediately after death or if no income is earned in the estate prior to the final distribution. However, you should let the beneficiaries know which amounts they receive from the estate are taxable to them.

You may consider obtaining a clearance certificate from the CRA before distributing any property under your control. A clearance certificate certifies that all of the tax returns for the deceased and estate are up to date, and all taxes have been paid or that security has been provided to the CRA for the payment of taxes. If you don't receive a clearance certificate, you, as the deceased's legal representative, can be liable for any amount owing by the deceased or estate to the CRA. If the deceased or the estate owes taxes to other tax jurisdictions, such as the U.S. Internal Revenue Service (IRS), you may want to obtain a similar certificate, if possible, before making a distribution from the estate.

Instalments

No instalments have to be paid for a deceased person for the period after the date of death. However, you should ensure that any instalments due prior to the date of death were paid; if not, they should be paid as soon as possible.

Income tax returns

The deceased's income from January 1 of the year of death up to and including the date of death must be reported on a final income tax return. Any income earned after the date of death should be reported on a trust return instead of the deceased's final return. You must also file tax returns for any prior years for which the deceased had not filed a tax return.

For the year of death, you may be able to elect to file more than one tax return for the deceased for certain types of income. By filing more than one return, you may be able to reduce or even eliminate income taxes on the deceased's income in the year of death. These additional returns are referred to as optional returns and are discussed in a separate article which you may request from your RBC advisor.

Due dates for filing tax returns

The deadlines for filing returns may vary depending on whether it's a final return, an optional return, or a return for a year prior to death. If a return is filed late, a late-filing penalty and interest may be charged.

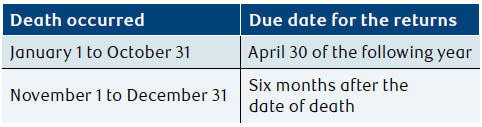

Final return

In general, the filing due date for the final return of the deceased and the return for their surviving spouse who was living with them is the same as for all individual income tax returns (April 30 of the following year if neither of them were carrying on a business), or six months after the date of death, whichever date is later.

If the deceased or their surviving spouse was carrying on a business, the following filing due dates apply to both individuals.

The due date for filing the return of a surviving spouse who was living with the deceased is the same as the due date for filing the deceased's final return.

The deceased's Will or a court order may establish a testamentary spousal trust. When testamentary debts of the deceased or the estate are being handled through the trust, the due date for the final return is extended to 18 months after the date of death.

Previous year return(s)

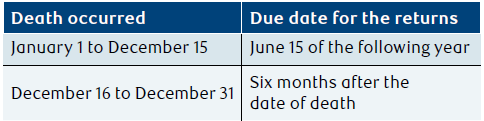

When an individual passes away after December 31, but on or before the filing due date for their income tax return for the immediately preceding year and that return hasn't been filed, the return, as well as the balance owing, is due six months after the date of death. The due date for filing the prior year return of a surviving spouse who was living with the deceased is the same as the due date for filing the deceased's prior year return. However, any balance owing on the surviving spouse's return still has to be paid on or before April 30 of the current year to avoid interest charges.

The filing due dates for prior year returns that are already due, but which the deceased had not yet filed, remain the same.

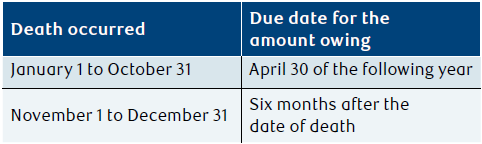

Due date for balance owing

The due date for a balance owing on a final return depends on the date of death and may be different from the filing due date of the return (e.g. where the deceased or their surviving spouse was carrying on a business).

No matter when the person dies, any balance owing on the surviving spouse's return still has to be paid on or before April 30 of the following year to avoid interest charges.

If the amount owing is not paid in full on or before the due date, interest - compounded daily - will be charged on the unpaid amount, from the day after the due date of the return to the date the amount owning is paid.

Some factors in determining the deceased's income for the final return

The deceased's income from January 1 of the year of death up to and including the date of death must be reported on the final income tax return. This includes all periodic amounts earned prior to death — such as salary, interest, rent and most annuities — even if the deceased didn't receive them before they died. These amounts must be payable prior to death to be included on the deceased's final return.

In addition, the deceased is deemed to have disposed of all of their capital property immediately before death.

Deemed disposition of capital property

In general, a deceased person is deemed to dispose of all of their capital property at fair market value (FMV) immediately before death. Although there isn't an actual sale, the deemed disposition may result in a capital gain or, except for personal-use property, a capital loss. The resulting capital gain or loss is included in the deceased's final tax return.

There's an exception to the deemed disposition rule for capital property left to a spouse or a qualifying spousal trust. In this case, the property is deemed to roll over to the spouse or to the spousal trust at the deceased's adjusted cost base (ACB), any capital gain or loss is deferred until the property is disposed of (or is deemed to be disposed of) by the spouse or by the spousal trust. As the legal representative, you can elect to transfer the deceased's capital property, on a property-by-property basis, to a surviving spouse or to a spousal trust at FMV rather than at the deceased's ACB. You may wish to do so if the deceased owned shares in a qualified small business corporation or qualified farm or fishing property, or where the deceased has unutilized capital losses at the date of death. This election must be made when you file the final tax return for the deceased.

Investment income

Report all investment income the deceased received from January 1 to the date of death. This type of income includes dividends and interest. Also include the following:

• amounts earned from January 1 to the date of death that haven't been paid;

• amounts earned from term deposits, guaranteed investment certificates (GICs), and other similar investments from the last payment date to the date of death;

• bond interest earned from the last payment to the date of death, if the deceased didn't report it in a previous year; and

• compound bond interest that accumulated to the date of death, if the deceased didn't report it in a previous year.

You can report some types of investment income as "rights or things" on a separate optional return. For more details on the "rights or things" optional return, ask your RBC advisor for the article on optional returns for a deceased individual.

RRSP or RRIF income

Generally, a deceased annuitant is deemed to have received, immediately before death, an amount equal to the FMV of all the property of the registered retirement savings plan (RRSP)/registered retirement income fund (RRIF) plan at the time of death. You have to include this amount in the deceased's income on their final return. There are a few exceptions to this rule, which are discussed in a separate article on estate planning for your RSP/RRIF. For more details on the exceptions, ask your RBC advisor for a copy of the article.

Sometimes, the FMV of the RRSP or RRIF can decrease between the date of death and the date of final distribution to the beneficiary or the estate. If the total of all distributions from the RRSP or RRIF is less than the FMV of the property that was included in the deceased annuitant's income for the year of death, you, as the deceased's legal representative, can request that the difference between the FMV and the total of all distributions be deducted on the deceased's final return. Generally, for the deduction to be allowed, the final distribution must occur by the end of the year that follows the year of death.

Death benefits (other than Canada or Quebec Pension Plan death benefits)

A death benefit is an amount received after a person's death for their employment service. A death benefit payable in respect of the deceased person is not reported on the final return for the deceased; rather, it's considered to be income of the estate or the beneficiary that receives it. Up to $10,000 of the total of all death benefits paid may not be taxable. Any amount of death benefits above $10,000 would be taxable to the beneficiary or estate that receives it.

RRSP deduction

RRSP contributions can't be made to the deceased's RRSP after death. It may, however, be possible to use the available contribution room of the deceased at death to make a contribution to the surviving spouse's RRSP in the year of death or during the first 60 days after the end of that year. This assumes the surviving spouse can have an RRSP at the time of contribution (i.e. they are age 71 or younger in the year of contribution). These contributions may be claimed as a deduction on the deceased individual's final return, up to the deceased's RRSP deduction limit for the year of death.

Pension income splitting

It may be possible to split pension income included on the deceased's final return. To make this election, as the legal representative, you and the surviving spouse must jointly elect to split the deceased's pension income. The election must be filed by the due date for the deceased's final return. For more information on your ability to split pension income on death, ask your RBC advisor for an article on pension income splitting.

Funeral and estate administration expenses

Funeral and estate administration expenses are personal expenses and aren't deductible in calculating the income of the deceased or the estate.

Personal non-refundable tax credits

If the deceased was a Canadian resident from January 1 of the year of death to the date of death, they're entitled to the full personal amounts on their final tax return. If the deceased was a resident of Canada for only part of the time from January 1 of the year of death to the date of death, the personal amounts may have to be prorated.

Medical expenses

Medical expenses paid by the deceased or their spouse, for either of them or their dependent children under age 18, for any 24-month period that includes the deceased's date of death may be claimed on the deceased's final tax return. To claim medical expenses for 24 months in the year of death, the tax return of a prior year could be adjusted so that no medical expense is claimed in that year, leaving the expense available for the year of death.

Donations

Prior to 2016, charitable donations made in a Will were generally deemed to be made by the individual immediately before death and were claimed on the deceased's final tax return; any excess amount that couldn't be claimed in the year of death could have been claimed on the immediately preceding year's tax return. Charitable donations couldn't be carried forward from the deceased individual to be claimed by their estate.

As of January 1, 2016 (for deaths occurring after 2015), donations made by Will or by designation under an RRSP, a RRIF, TFSA or life insurance policy are no longer be deemed to be made by an individual immediately before death. Instead, the donations are deemed to be made by the estate at the time the donation is made to a qualified donee. The donation tax receipt is based on the FMV of the gift at the time the property is transferred to and received by the qualified donee. The estate can claim a donation in the year a gift is made or in the five subsequent years.

If the estate is a "graduated rate estate" (GRE) at the time the donation is made and the donated property (or property that was substituted for such property) was acquired by the estate on and as a consequence of the death, the trustee of the estate will have the flexibility to allocate the available donation among any of the following:

• the taxation year of the GRE in which the donation is made;

• an earlier taxation year of the GRE;

• the GRE's tax return for the five years (or 10 years for a gift of certified ecologically sensitive land made after February 10, 2014) following the year the GRE made the donation;

• the last two taxation years of the deceased individual.

Note that this flexibility doesn't extend to a testamentary spousal trust and is only applicable to a GRE. Generally, a GRE of an individual is the estate that arose on and as a consequence of the individual's death for a period of no longer than 36 months after death. To be considered a GRE, the estate also needs to remain a testamentary trust and be designated for its first taxation year (or, if the estate arose before 2016, for its first taxation year that ends after 2015) as the deceased individual's GRE. This isn't a complete definition of a GRE. A GRE is discussed in more detail in the article on testamentary trusts. For more details on GREs, ask your RBC advisor for a copy of the article.

If an estate that was formerly a GRE makes the donation after the 36-month period but within 60 months after the date of death, and the estate continues to meet all of the requirements of a GRE, other than the 36-month time limit, it will still qualify for some flexibility in claiming the donation. In this case, the donation can be allocated among any of the following:

• the taxation year of the estate in which the donation is made;

• any of the estate's five years (or 10 years for a gift of certified ecologically sensitive land made after February 10, 2014) following the year the donation is made;

• any previous taxation year of the estate in which the estate was a GRE (i.e. only in the first 36 months after the death);

• the last two taxation years of the deceased individual.

As discussed, when an individual dies, the individual is deemed to have disposed of all capital property immediately before their death. Where this property is publicly traded securities, ecological property or cultural property, a zero percent capital gain inclusion rate may apply for in-kind donations of such property made by a deceased's estate. However, the zero percent rate only applies if the donation is made within 60 months of the individual's death and the estate is a GRE or was a GRE that continues to meet the other requirements of a GRE, other than the 36-month time period.

If a donation is claimed on the estate's return, the maximum charitable donation that can be claimed is 75% of net income of the estate. If the donation is claimed on the deceased's final return or the tax return for the year before the year of death, the maximum charitable donation that can be claimed is 100% of net income.

Alternative minimum tax (AMT)

AMT limits the tax advantage a person can receive in a year from certain tax incentives (e.g. tax deductions from flow-through shares). AMT doesn't apply to a person for the year of death. To the extent the deceased had paid AMT in one or more of the seven years before the year of death, they may be able to deduct part or all of the AMT previously paid from tax owing on the final return.

Net capital losses

Typically, capital losses can only offset capital gains for tax purposes; however, if the deceased had unused capital losses at death, there may be an opportunity to deduct these unused capital losses, after certain adjustments, from other types of income in the year of death or the immediately preceding year.

Generally, when allowable capital losses are more than taxable capital gains, the difference is a "net capital loss."

Net capital losses in the year of death

If a net capital loss occurs in the year of death, there are two methods for claiming this loss.

The first method is to carry back the net capital loss from the year of death to reduce any taxable capital gains in any of the three tax years before the year of death. The net capital loss you carry back can't be more than the taxable capital gains in those years.

After you carry back the loss, there may be an amount remaining. You may be able to use some or all of the unutilized net capital loss to reduce any other income on the deceased's final return, the return for the year before the year of death, or both returns. The amount you can claim is the unutilized net capital loss less any capital gains deductions the deceased has claimed to date.

For the second method, you can choose not to carry back the net capital loss to reduce taxable capital gains from earlier years. You may prefer to reduce any other income on the final return, the return for the year before the year of death, or both returns. As with the first method, the amount you can claim is the unutilized net capital loss less any capital gains deductions the deceased has claimed to date.

Applying net capital losses to a previous year may reduce any capital gains deductions the deceased claimed in that year or a following year.

Net capital losses before the year of death

If the deceased has any unapplied net capital losses incurred before the year of death, you can apply the loss against taxable capital gains on the final return. If there's still an amount remaining, you may be able to use it to reduce any other income on the deceased's final return, the return for the year before the year of death, or both returns. You can't use the net capital losses of other years to create a negative taxable income for any year. As these special rules on the deductibility of capital losses for deceased persons are quite complex, consult a qualified tax advisor for further details.

Net capital loss in the first year of the estate

As the legal representative, you're responsible for administering the deceased's estate. If you dispose of capital property in the administration of the estate, the result may be a net capital loss. Usually, you'd claim these losses on the estate's income tax return. However, if the allowable capital losses exceed the taxable capital gains realized by the deceased's estate in its first taxation year and the estate is a GRE, you can choose to claim all or part of these losses on the deceased's final return. Any net capital loss realized after the date of death but in the first taxation year of the GRE can only be applied to the year of death (and not to the year before the year of death). Where the estate is not a GRE, the carry-back of net capital losses to the deceased's final return isn't possible. An estate, whether it's a GRE or not, can carry forward net capital losses realized in the estate if the estate continues.

In 2024, the government proposed a change to allow a legal representative to carry back net capital losses of a GRE that are realized in its first three taxation years, as opposed to only the first taxation year, to the deceased's final tax return if the individual died on or after August 12, 2024. This proposed change was not enacted into law by the government prior to its dissolution. At the time of publishing this article, it's uncertain as to whether this change will be reintroduced by the government.

U.S. estate tax

You're required to file a U.S. estate tax return for a deceased Canadian if they held at least US$60,000 of U.S. situs assets at the time of their death, even if there's no U.S. estate tax liability. There are penalties under the U.S. Internal Revenue Code should a legal representative knowingly fail to file a U.S. estate tax return. For more information, ask your RBC advisor for the article on U.S. estate tax for Canadians.

If U.S. estate tax was paid to the IRS, in certain circumstances, to minimize double taxation, it may be possible to claim a foreign tax credit on the deceased's final Canadian income tax return for the U.S. estate taxes paid.

Conclusion

Filing tax returns for a deceased person and determining whether any post-mortem tax planning will save taxes can be complicated. For those in this situation, it's advisable to seek assistance from a qualified tax and/or legal advisor.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.