Intergenerational business transfers

Some tax relief for business succession within your family. You've worked hard over the years to build a successful business and it's your wish to pass it to the next generation. However, the Income Tax Act (ITA) contains long-standing anti-avoidance rules that make it more attractive, from a tax perspective, to sell your shares of a qualified small business corporation (QSBC) or shares of the capital stock of a family farm or fishing corporation (FFFC) to an arm's-length third party rather than a family member.

Some tax relief for business succession within your family. You've worked hard over the years to build a successful business and it's your wish to pass it to the next generation. However, the Income Tax Act (ITA) contains long-standing anti-avoidance rules that make it more attractive, from a tax perspective, to sell your shares of a qualified small business corporation (QSBC) or shares of the capital stock of a family farm or fishing corporation (FFFC) to an arm's-length third party rather than a family member.

Family Office Services

November 14, 2025

Intergenerational Business Transfers

Some tax relief for business succession within your family

You've worked hard over the years to build a successful business and it's your wish to pass it to the next generation. However, the Income Tax Act (ITA) contains long-standing anti-avoidance rules that make it more attractive, from a tax perspective, to sell your shares of a qualified small business corporation (QSBC) or shares of the capital stock of a family farm or fishing corporation (FFFC) to an arm's-length third party rather than a family member.

To address this inequality between family and non-family business sales, Bill C-208, a private member's bill, was introduced and received Royal Assent on June 29, 2021. The rules outlined in the bill became effective immediately on this date. The legislation in Bill C-208 amended the ITA to provide that, under certain conditions, the transfer of QSBC or FFFC shares by a taxpayer to a corporation controlled by the taxpayer's child or grandchild, who is at least 18 years of age, is excluded from the anti-avoidance rules; in the case of a reorganization of a business involving QSBC or FFFC shares, siblings are now considered related for this purpose.

Subsequently, the 2023 Federal Budget, the revised August 4, 2023 draft legislation, and Bill C-59, which received royal assent on June 20, 2024, have made changes to the rules initially introduced in Bill C-208 to ensure that only "genuine" intergenerational business transfers benefit from the exceptions to the anti-avoidance rules. This article provides an overview of these very complex tax rules.

Sale of family business to your adult child

As mentioned, an existing anti-avoidance rule in the ITA provides that, where you transfer your QSBC shares or shares of an FFCC to another corporation that you don't deal at arm's length with, the transfer may result in a deemed dividend instead of a capital gain. As a result, you may pay much more tax, as the rate of tax on a dividend is generally much higher than a capital gain. In addition, you wouldn't be able to claim the capital gains exemption on the sale of your shares. This conversion of a capital gain to a deemed dividend would not occur if you sold the shares of your corporation to an arm's-length third party.

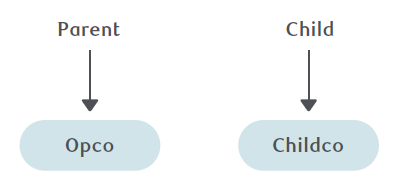

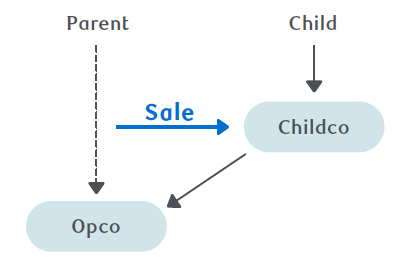

The following diagram shows a very simplified example of the structure before and after the sale. In the example, you are not dealing at arm's length with Childco, as you're related to your child who controls Childco.

Before the sale of your QSBC/FFCC to your adult child's corporation

After the sale of your QSBC/FFCC to your adult child's corporation

The legislation introduced by Bill C-208 attempted to fix this issue by providing exceptions to the anti-avoidance rule for certain transfers of QSBC shares or shares of an FFCC from an individual to corporations owned by their child (definition of "child" to be discussed later). However, the rules introduced by Bill C-208 contained insufficient safeguards and applied even where no transfer of a business to the next generation had taken place.

The rules which were contained in Bill C-59 amended the rules introduced by Bill C-208 to ensure they apply only where there's a genuine intergenerational business transfer. These rules are applicable for transactions that occur on or after January 1, 2024.

A genuine intergenerational transfer would be a transfer of shares of a corporation (the subject corporation) by a natural person (the transferor, referred to as the "parent" in this article) to another corporation (the purchaser corporation) where several conditions are satisfied. These rules apply where all of the following are met:

- Each share of the subject corporation is a QSBC share or a share of an FFCC at the time of the transfer

- The purchaser corporation must be controlled by one or more persons, each of whom is an adult child of the transferor

- The transferor must not have used this exception for a previous disposition of shares in respect of the same business (other than if the exception was used before January 1, 2024)

The meaning of "child" for these purposes would include the transferor's or their spouse's child, grandchild, great-grandchild and their respective spouses; it would also include the transferor's or the transferor's spouse's niece or nephew and the niece or nephew's spouse or child. In this article, wherever "spouse" is used, it also includes a common-law partner.

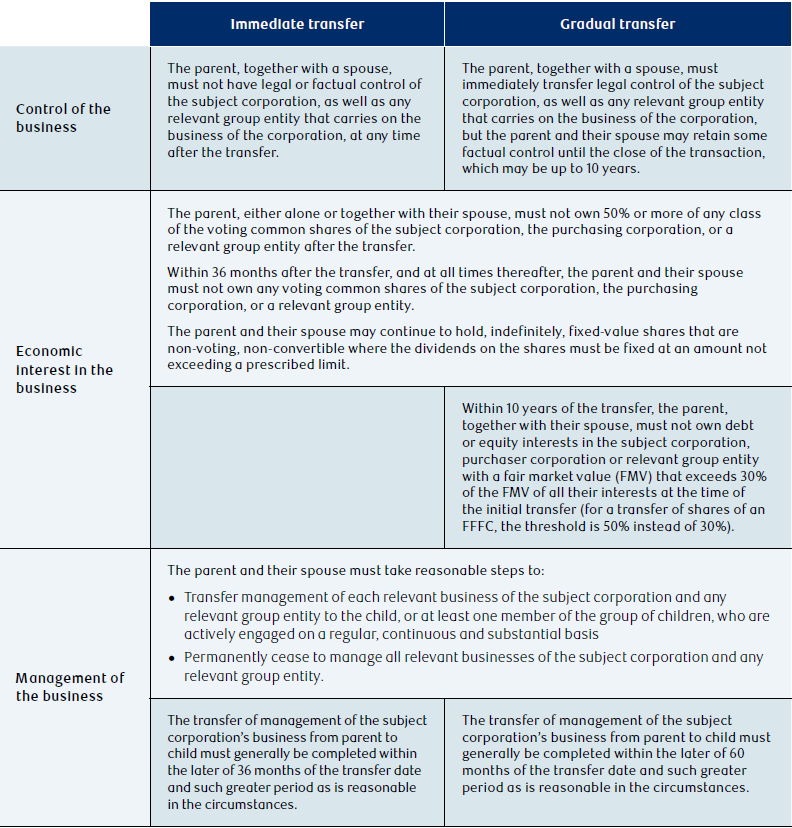

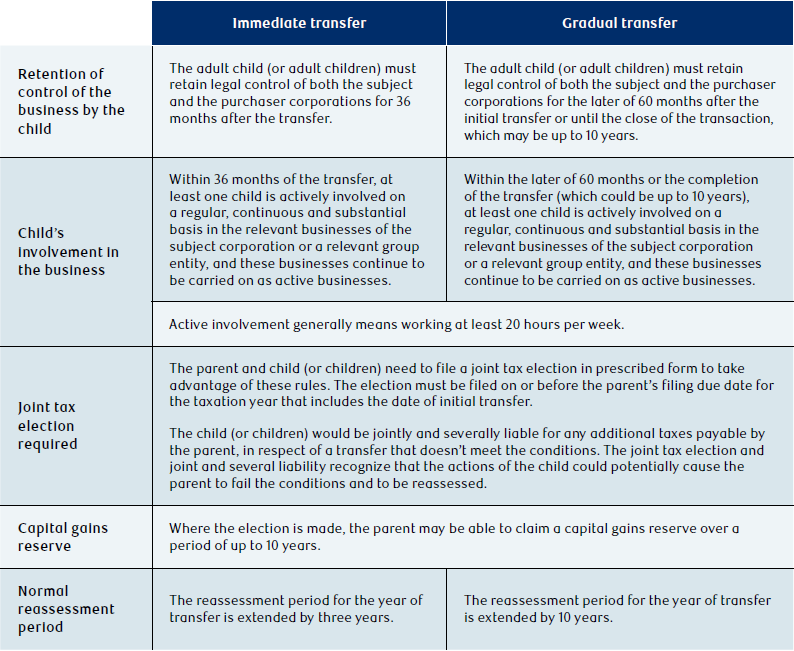

The conditions to be considered a genuine intergenerational business transfer would include the following (discussed in more detail later):

- Transfer of factual and legal control of the business

- Transfer of economic interest in the business

- Transfer of management of the business

- Child retains control of the business

- Child works in the business

To provide flexibility, the legislation also introduced two transfer options to undertake a genuine intergenerational share transfer:

- An immediate intergenerational business transfer completed within 36 months

- A gradual intergenerational business transfer completed over a period of up to 10 years

The conditions and rules for immediate versus gradual transfers are different but overlap in some circumstances. These rules are complex and a detailed discussion is beyond the scope of this article. The following chart provides a brief summary of some of the key requirements.

The intergenerational business transfer legislation recognizes that some of the mentioned tests may not be met due to certain triggering events (for example, when the shares in the hands of the child (or children) are sold to an arm's-length party, upon the death or physical or mental impairment of an active child or an insolvency event). In these scenarios, the relevant tests are deemed to have been met.

Siblings involved in the reorganization of a family business

Existing rules in the ITA may convert an otherwise tax-free intercorporate dividend into a taxable capital gain in certain circumstances. However, there is an exception to these rules where related parties are involved. Although siblings are generally considered related for most provisions of the ITA, they were considered unrelated under these particular rules. As a result, they couldn't rely on this exception, and reorganizations of a family business where siblings were involved could be extremely complex.

The legislation introduced by Bill C-208 provides a new exception so that siblings will be considered related in the case where the dividend was received or paid, as part of a transaction or an event, or a series of transactions or events, by a QSBC or an FFFC.

As a result of these new rules, reorganizations involving siblings may be much less cumbersome. These rules became effective when Bill C-208 received Royal Assent on June 29, 2021.

Conclusion

If you have a QSBC or an FFFC that you intend to transfer to the next generation, or where you're contemplating a reorganization involving your siblings, you should consult with your qualified tax advisor to see if you can take advantage of these new rules. In addition, you'll have many non-tax considerations before transferring your family business to the next generation. You and your family may need to have open discussions on issues such as who's going to take over the business, how to structure your retirement funding, and how to equalize your estate, etc. It's important that you start the process early to have sufficient time for proper planning.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.