Investment holding companies

When it comes to earning investment income through a corporation, you need to consider both corporate taxes and personal taxes when you withdraw funds from the corporation. This article identifies situations where the use of an investment holding company may be beneficial and outlines possible drawbacks.

When it comes to earning investment income through a corporation, you need to consider both corporate taxes and personal taxes when you withdraw funds from the corporation. This article identifies situations where the use of an investment holding company may be beneficial and outlines possible drawbacks.

Family Office Services

June 14, 2025

Investment holding companies

When it comes to earning investment income through a corporation, you need to consider both corporate taxes and personal taxes when you withdraw funds from the corporation. This article identifies and discusses situations where the use of an investment holding company may be beneficial and outlines the possible drawbacks. It also summarizes some estate planning considerations related to the use of an investment holding company. Any reference to a spouse in this article also includes a common-law partner.

What is an investment holding company?

An investment holding company isn't a defined term in the Income Tax Act. Instead, it's a term used to describe a corporation that doesn't operate an active business and is typically used to own shares of a private corporation with an active business and/or hold passive assets, such as publicly traded securities, bonds, real estate and so on.

Investing through a holding company

The intent of the Canadian tax system is to be tax neutral between investment income earned personally and investment income earned through a corporation, a concept known as integration. This means after a corporation pays tax on its investment income and a shareholder pays personal tax on dividends received from the corporation, the total corporate and personal taxes payable should be the same as if an individual earned the investment income personally. Accordingly, there should be no material tax advantage or disadvantage to earning investment income through a corporation. That said, the Canadian tax system isn't perfect and generally there's a tax cost to earning investment income (other than taxable Canadian dividends) through a corporation in all provinces and territories. It should be noted that there is a significant tax cost to earning foreign income, subject to foreign withholding tax, through a corporation versus earning the same type of income personally. So, you may be wondering why someone would want an investment holding company. Some of the benefits are outlined in the following sections.

Benefits of using a holding company

Deferring personal tax

A common corporate structure involves a holding company owning shares of an operating company. Integrating a holding company into an existing corporate structure may be beneficial if you want to remove excess funds from your operating company but don't want to pay personal tax on the withdrawal.

Let's say you wanted to extract funds from your operating company to invest. If you withdraw the excess earnings personally from your operating company, you'd first have to pay personal tax, leaving less for reinvestment. Instead, if you had a holding company, it's possible, in certain circumstances, to move excess earnings from your operating company to your holding company as a tax-free inter-corporate dividend. As such, the use of a holding company can defer personal taxes, leaving more funds for reinvestment purposes.

Keep in mind, though, in every province and territory, there's currently a cost to earning investment income (except taxable Canadian dividends) through a corporation versus earning the income personally. This is because the combined corporate and personal tax you pay on this income (when it's paid to you as a dividend) is higher than the personal tax you'd have to pay if you earned the income personally. If you're in the highest marginal tax bracket, in some provinces and territories, there may be a slight prepayment of tax on investment income earned in a corporation due to the differences between corporate and personal tax rates.

Taxable Canadian dividends (eligible and non-eligible) earned through a corporation are tax neutral. This is because any taxes paid by the corporation are refunded once it pays a taxable dividend to its shareholders. However, for eligible dividends (e.g., dividends from portfolio investments), there may be a slightly higher corporate tax paid in most provinces and territories if not paid out as a dividend by the corporation in the year received, even if you're at the highest personal marginal tax rate. This occurs if your personal tax rate on Canadian eligible dividend income is lower than the corporate tax rate of 38.33%.

Creditor protection

If you have excess funds in your operating company, you may want to move them to a holding company to protect those funds from creditors of your operating company. If the operating company needs working capital, the holding company can lend the money back to your operating company on a secured basis to maintain the potential protection from creditors. Similarly, for rental operations, holding rental properties within a corporation may limit your liability to corporate assets and provide some personal creditor protection.

When it comes to creditor protection, you should speak with a qualified legal advisor about the options available to you. You may also want to speak to a qualified tax advisor about the tax implications of moving funds from your operating company to a holding company.

Purifying your corporation

If you own shares of a qualified small business corporation (QSBC), you may be able to save a significant amount of tax by claiming the lifetime capital gains exemption (LCGE) on a future sale of those shares. Although a detailed discussion of the QSBC share conditions is beyond the scope of this article, two of the conditions are addressed here. First, at the time you sell your shares, the corporation must be a small business corporation (SBC). An SBC is a Canadian-controlled private corporation (CCPC) where all or substantially all (90% or more) of the fair market value (FMV) of the company's assets are used mainly in an active business carried on primarily in Canada. In simplified terms, a CCPC is a Canadian corporation with no class of shares listed on a prescribed stock exchange and that isn't controlled by a non-resident of Canada or a public corporation or a combination of both. Second, throughout the 24 months immediately before the shares are sold, the corporation must be a CCPC and more than 50% of the FMV of the assets of the corporation must be used mainly in an active business carried on primarily in Canada.

To keep your operating company onside with these QSBC requirements, you may want to remove surplus funds not required for active operations, or "purify" your corporation, on a regular basis to ensure you can claim the LCGE. You can generally remove the excess funds from your operating company by transferring them to an investment holding company on a tax-deferred basis. Speak with a qualified tax advisor to determine how best to accomplish this.

Controlling the amount and timing of income

By incorporating, you have the flexibility to control when and how much to pay yourself personally. This flexibility can be useful if you wish to manage your personal marginal tax rate and minimize the amount of income that's taxed each year personally. In addition, some federal non-refundable tax credits and federal benefits, such as the age amount and Old Age Security benefits, are reduced or eliminated when your net income exceeds certain thresholds. By keeping the income in your holding company, you can manage your personal income level to keep it below these thresholds.

An investment holding company may also provide flexibility if you own an operating company, along with other shareholders, that pays out dividends each year. If you don't want to receive the dividends personally, having a holding company as part of your corporate structure could provide you with this flexibility.

The ability to control the timing of when you receive income personally may allow you to avoid the requirement to pay personal tax instalments. For example, you can choose to pay yourself dividends every second year rather than every year. This is because instalment payments are based on either the previous year's taxes owing, or the current year's expected liability. If you have little or no tax liability every second year, you can base your instalment payments on the year you expect to have little income.

Implementing an estate freeze

If you have a personal investment portfolio or other passive assets, such as a rental property, that's expected to appreciate in value, you can implement an estate freeze to "freeze" the value of your assets and transfer the future growth to other family members as part of your estate plan. You can accomplish an estate freeze by using an investment holding company where you exchange your investments for property with no growth potential, such as fixed-value preferred shares of the investment holding company. This exchange may be done without triggering immediate tax consequences. In addition, freezing the value of your assets allows you to plan for the tax that will be payable upon the eventual disposition of your assets, including a deemed disposition on death.

You can then issue the new growth shares of your investment holding company, at a nominal amount, to your family members directly, or through a family trust which may provide more flexibility. This will allow the future growth in the value of your assets to accrue to other family members and defer the tax until they eventually dispose of the shares. When considering an estate freeze, it's important to note that the strategy only makes sense if your assets are expected to continue to appreciate in value and there is a clear successor or next generation of owners you want to pass along the growth to.

Income splitting

If you have an investment holding company, you may be able to pay dividends to family members who are shareholders of the corporation. If your family members have little or no other income, it may be possible for these dividends to be taxed at their lower marginal tax rates. It's important to note that there are "tax on split income" (TOSI) rules as well as corporate attribution rules which limit the ability to income split certain types of income from a corporation with family members.

Although the next section provides an overview of the TOSI rules, it's crucial to note that the application of these rules isn't clear when a corporation earns only passive investment income. To determine if the TOSI rules apply to your specific situation, please consult with a qualified tax advisor.

TOSI rules

The TOSI rules were designed to discourage income splitting with family members who don't meaningfully contribute to the business activities of a private corporation. The TOSI rules were previously known as the "kiddie tax" rules because they limited income splitting of certain types of income from a private corporation with minor children. However, as of January 1, 2018, the rules were expanded to also apply to any Canadian resident aged 18 or over. The TOSI rules have significantly curtailed the ability to split income with family members.

The TOSI rules apply to many types of income received from a private corporation, including interest, dividends, shareholder benefits and certain capital gains. When TOSI applies, the income is subject to tax at the highest personal marginal tax rate, regardless of the individual's actual marginal tax rate. In addition, the individual who receives split income cannot reduce the tax on this income by claiming personal tax credits other than the dividend tax credit, the foreign tax credit and the disability tax credit. As a result of TOSI, many income splitting opportunities have become ineffective.

There are TOSI exclusions, which differ depending on the age of the individual receiving the income or the age of the business owner. For example, there's an exclusion available for a business owner who's at least age 65, which allows their spouse to receive split income without the TOSI rules applying. These exclusions are more restrictive for minors. For more information on the TOSI rules, ask your RBC advisor for the article discussing income splitting through private corporations.

The corporate attribution rules

If you own an investment holding company and want to direct income earned in the corporation to a family member, you should be aware of the corporate attribution rules. Corporate attribution generally applies when an individual transfers or lends property to a corporation, and one of the main reasons for the transfer or loan may reasonably be considered to reduce the income of the transferor or lender and to benefit a spouse or a related minor child (which also includes a grandchild, niece or nephew). It's fairly easy to be caught by these attribution rules. For example, some of the most common methods used to implement an estate freeze are considered a transfer of property to a corporation which triggers the corporate attribution rules if a spouse or related minor child benefits from the estate freeze.

If corporate attribution applies, the individual who transferred or loaned property to the corporation is deemed to have received interest income in the year. The deemed interest income is equal to the CRA's prescribed interest rate for the period multiplied by the outstanding amount of the transferred property or loan. The annual deemed interest benefit is reduced by the following:

• Any actual interest received in the year by the individual in respect of the transfer or loan

• Taxable dividends (grossed-up actual dividends) received by the individual in the year on shares that were received from the corporation as consideration for the transfer

• Taxable dividends paid to your spouse or a related minor that are subject to TOSI

Corporate attribution doesn't apply to an SBC, but would generally be a concern for investment holding companies.

There are strategies to get around the application of the corporate attribution rules, however, these are beyond the scope of this article. Since the application of corporate attribution is quite complex, it is strongly recommended you discuss these issues with a qualified tax advisor prior to implementing any income splitting strategies involving an investment holding company.

Minimizing U.S. estate taxes

U.S. investments (such as shares of U.S. public corporations) held by your Canadian corporation are generally not subject to U.S. estate tax, provided you're not a U.S. person. Therefore, it may be possible to reduce or eliminate your U.S. estate tax exposure by holding certain U.S. assets in a Canadian holding company. That said, earning U.S. dividends in a corporation may result in significantly higher combined corporate and personal tax than holding these assets personally due to the way foreign dividend income is taxed in a corporation.

Before using a Canadian corporation to hold U.S. assets, ensure the strategy is reviewed by a qualified cross-border tax advisor who can evaluate the risks from both a Canadian and U.S. perspective to determine if using a Canadian corporation will achieve your objectives.

Minimizing probate taxes

If you own shares of an investment holding company, you may be able to reduce probate taxes on death by using a "multiple Wills strategy," depending on your province or territory of residence. This is because under provincial corporate statutes, it may be possible to transfer share ownership on death without probate.

The multiple Wills strategy involves having a "primary" Will that deals with assets that require probate to transfer ownership, such as bank accounts or an investment portfolio, and a "secondary" Will to transfer assets that typically don't require probate, such as artwork or private company shares. By separating assets in this way, you may avoid paying probate on the assets that don't otherwise require it.

Note that probate tax savings alone may not be significant enough to justify establishing an investment holding company. The reduction of probate taxes should be viewed as a secondary benefit of using an investment holding company. In addition, there may be circumstances where a secondary Will may need to be probated. For example, if your Will contemplates that the shares or the assets of the company be transferred to a trust set up in your Will, probate may be required by a financial institution to open an investment account for the trust. Furthermore, some financial institutions may require that a secondary Will be probated as a matter of policy.

Ask your RBC advisor for the article on multiple Wills. For more information on whether a multiple Wills strategy makes sense for you, consult with a qualified legal advisor.

Considerations for using a holding company

While having a holding company may provide certain advantages, you need to weigh these benefits against the potential disadvantages, such as the ongoing accounting and legal costs associated with having a corporation.

Restricted access to the small business limit

If you have a CCPC with an active business, it may benefit from the federal small business deduction, which provides a low tax rate on the first $500,000 of active business income (known as the "business limit"). However, if a CCPC, and any associated corporations, earn between $50,000 and $150,000 of passive investment income in a year, the CCPC's federal business limit for the following year will be reduced. The CCPC's business limit is eliminated when passive income of the CCPC, and its associated corporations, exceeds $150,000. This reduction in the business limit may result in higher corporate taxes being paid on your operating company's active business income.

These rules discourage accumulating excess income (over and above what is needed for the continued active operations of the business) in an operating company or an associated holding company. For example, two corporations are associated for tax purposes if you have an investment holding company that controls an operating company. In this situation, you may want to reduce the amount of passive investment income earned in both of your corporations, so it lessens the impact it has on the small business limit of your operating company. If you only have a holding company that's not associated with any operating company, these passive investment income rules don't affect your holding company.

Restricted personal use of corporate funds

If you were to invest personally, all income earned would be taxed in your hands. As such, you can use the after-tax returns however you wish. On the other hand, if you invest within a holding company, the after-tax returns belong to your corporation and you cannot use the corporate funds personally, unless you first withdraw the money from the corporation. The tax implications of the withdrawal will depend on how you withdraw the funds (e.g., as a regular taxable dividend versus a capital dividend).

Restricted use of losses

If you invest personally, any capital losses you realize can be used to offset capital gains to reduce your taxable income. However, if you invest through your corporation, any losses realized in the corporation must be applied against the corporation's capital gains and can't be used to offset your personal income. That said, whether you incur these capital losses personally or through your corporation, if you or your corporation can't use the losses in the year they are incurred, they can be carried back to any or all of the three immediately preceding taxation years or carried forward indefinitely to use against future capital gains.

Restricted access to the LCGE

As mentioned, if you sell shares of a QSBC, you may be able to save a significant amount of tax by claiming the LCGE. Since an investment holding company invests in mostly passive assets, it generally doesn't qualify as a QSBC. As a result, the LCGE is generally not available to you if you sell shares of an investment holding company.

But, what if the only asset held by your holding company is shares of a QSBC? Unfortunately, if your holding company were to sell shares of a QSBC, it wouldn't be able to claim the LCGE since only individuals (and not corporations) can claim the LCGE. However, with this structure, your investment holding company may itself be a QSBC since its only asset is QSBC shares. If you sell your shares of your investment holding company, you may still qualify for the LCGE. However, a purchaser would generally not be interested in purchasing the shares of a holding company and you may need to reorganize your corporate structure before selling it to access the LCGE.

Increased complexity and cost

In addition to the increased complexity of a corporate structure, investing through a holding corporation may require you to adhere to a few corporate formalities. For example, the directors of the holding company will need to pass a resolution to declare and pay dividends. A corporation is also subject to greater regulation and compliance; for instance, your holding company will have to hold annual shareholder meetings and maintain corporate records.

The administrative, legal and accounting costs associated with establishing and maintaining a holding company are also factors to consider. When setting up a holding company, certain documents must be filed with the government, including articles of incorporation. If you ever make changes to the structure of your corporation, articles of amendment will need to be filed as well. In terms of ongoing professional fees, your holding company will incur annual costs to prepare financial statements, file a corporate tax return, and file tax slips for any dividends paid.

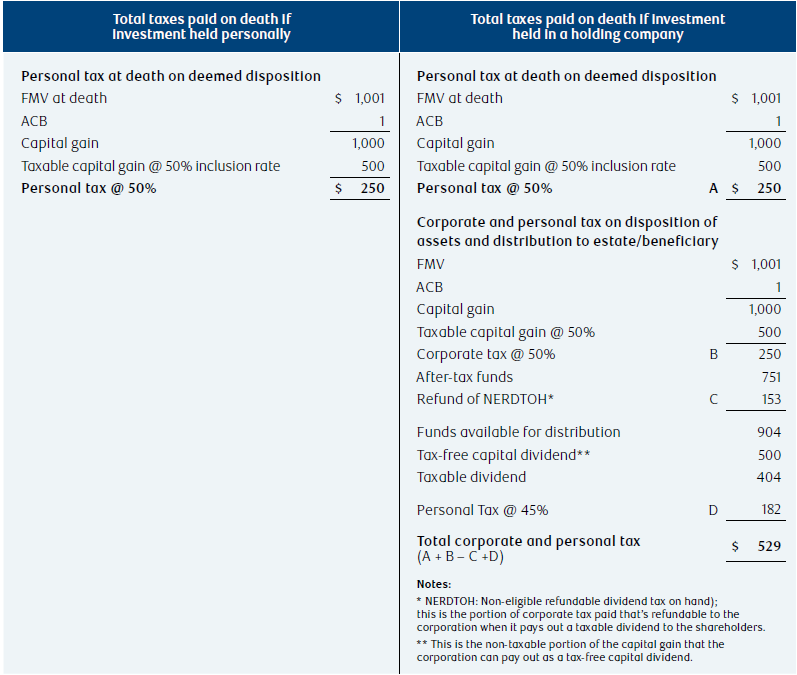

Double taxation at death

If you own shares of a holding company, you, your estate and your corporation may be subject to double taxation at death. First, you're taxed on the capital gain arising from the deemed disposition of the holding company shares at death. The amount of the capital gain is based on the FMV of the shares of the holding company on death, which in turn derive their value from the investments and assets within the holding company. Second, distributions from the corporation to your estate or other beneficiaries, generally in the form of dividends, may result in both corporate tax on the disposition of assets inside the corporation and then personal tax on the dividend paid.

The gain on the investments within the holding company may therefore be taxed twice – once as a capital gain on the deemed disposition at death and again as combined corporate and personal tax on the disposition of the assets inside the corporation and the distribution as a dividend to your estate or beneficiaries.

It's possible to defer this potential double tax by transferring the shares of the holding company to a surviving spouse or qualifying spousal trust on a tax-deferred basis. There are also post-mortem tax-planning techniques that may reduce or eliminate this double taxation. For example, if your corporation is wound up by your estate, it may result in a deemed dividend on the redemption of the shares and a capital loss to the estate. If this is done within the first taxation year of your estate and your estate is a graduated rate estate (GRE), your GRE may be able to carry back the capital loss realized on the wind-up to your final tax return to offset the capital gain realized on the deemed disposition of your shares. In this case, the double taxation may be reduced by the loss carry-back, since the net result is only the corporate tax on the disposition of the assets in your corporation, if any, and the tax on the dividend to your estate. The government has proposed to extend the period where the loss carry-back would be available from the first year of your GRE to the first three years of your GRE for deaths after August 11, 2024.

There are more complex post-mortem tax planning techniques available to reduce or eliminate the double tax issue or where the loss carry-back strategy just discussed is not available, but these are beyond the scope of this article. For more information, talk to a qualified tax advisor.

Estate planning considerations

When engaging in estate planning, you should consider how your investment holding company and the company's assets will be dealt with on your death. You should also consider what steps your executor/liquidator may need to take to transfer your shares or corporate assets to your beneficiaries.

Corporations don't cease to exist on the death of a shareholder. A corporation is its own legal entity, separate from its owners. On your death, your investment holding company will remain in existence and can continue to operate as a holding company. If you're the sole officer and director of your company, you may want to consider appointing additional officers and directors prior to your death. These individuals can continue to provide direction with respect to your corporate assets after you pass away. Otherwise, your executor/liquidator may need to take certain steps and incur fees to deal with your investment holding company after death.

On your death, the shares of your investment holding company will form part of your estate and be distributed in accordance with your Will, or if you have no Will, the governing provincial or territorial intestacy laws. When drafting your Will, consider whether you want the shares to pass outright to your named beneficiaries or if you want the company to be wound up. You may also want to consider the tax implications of these different options to your estate and beneficiaries.

To ensure you have properly addressed all estate planning issues with respect to your investment holding company, speak with a qualified legal and tax advisor.

Conclusion

Although there may be no tax benefit to investing through a holding company, the use of a corporation may still serve other purposes, such as creditor protection. If you're thinking of setting up an investment holding company, consider both the benefits and the potential costs.

If you have an existing holding company, you should periodically weigh the reasons for maintaining it against the reasons for dissolving it. For example, you may not want to wind up your holding company if the dissolution would result in the realization of previous tax deferrals and accrued capital gains.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.