Joint ownership accounts

As part of the estate planning process, individuals will often consider establishing a joint account with one or more of their adult children or other family members. This article explores the different joint account types available, how these accounts operate, and the resulting potential benefits and considerations for each type.

As part of the estate planning process, individuals will often consider establishing a joint account with one or more of their adult children or other family members. This article explores the different joint account types available, how these accounts operate, and the resulting potential benefits and considerations for each type.

Family Office Services

October 14, 2025

Joint ownership accounts

Key considerations and understanding your options at RBC Dominion Securities

As part of the estate planning process, individuals will often consider establishing a joint account with one or more of their adult children or other family members. Sometimes this is done as a tool for expediency so that a joint account holder can help to manage the account, or to make the assets immediately available to the surviving accountholder(s) upon the death of the first joint accountholder. In other cases, a joint account is a planning technique used as part of a strategy recommended by an individual's qualified legal and tax advisors to seek to minimize probate tax. Whatever the motivation behind the account, before you open a joint account, it's important to be aware of the different joint account types available at RBC Dominion Securities Inc., how these different joint account types operate, and the resulting potential benefits and considerations for each joint account type. It's also important to consider how a joint account fits into your overall holistic estate plan. There may be other estate planning tools that are more appropriate in light of your current or future estate plans.

Any reference to a spouse in this article also includes a common-law partner.

Joint tenancy vs tenancy in common

There are generally two forms of shared ownership which allow for two or more people to own an asset together. Tenancy in common and joint tenancy.

Tenancy in common

The term "tenancy in common" is used to describe the ownership of an asset by two or more individuals together, but without the right of survivorship. Each accountholder is entitled to a defined, possibly unequal, portion of the account in question. Co-owners in a tenancy in common arrangement can own equal or unequal interests in an asset. Upon the death of one of the accountholders, their interest will not pass to the surviving accountholder, but will form part of the estate of the deceased accountholder and will be distributed in accordance with their Will. If the deceased didn't have a Will then the provincial or territorial intestacy laws will dictate how the assets of the deceased will be distributed.

Joint tenancy

Joint tenancy allows two or more people to own an asset together. Each joint accountholder generally has an equal undivided interest in the account.

Where the joint tenancy is between spouses, upon the death of one spouse, the deceased's ownership interest in the account automatically passes to the surviving spouse. By passing directly to the surviving spouse, the account doesn't form part of the deceased spouse's estate and therefore wouldn't generally be subject to probate fees.

Where the joint tenancy is between a parent and adult children, upon the death of the parent, the account may be considered to form part of the deceased parent's estate. The adult children are required to demonstrate that the parent intended to gift the account and its assets to them, as opposed to having added the children to the account for the purpose of ease of account administration. Where the adult children so demonstrate, the account will generally pass to them as surviving joint tenants. Otherwise, the account forms part of the deceased parent's estate and may be subject to probate. The following is a non-exhaustive list of the matters which may assist in determining the parent's intention:

• What was said and done by the parties before or at the time of the transfer or immediately after it

• The language used in any bank or financial institution documents pertaining to the account

• Control and use of the funds in the accounts during the parent's lifetime

• The tax treatment of the joint account. Was the income and capital gains generated by the investments in the account reported solely by the parent or by all joint accountholders?

• Evidence of the parent's intention to gift the account to the children

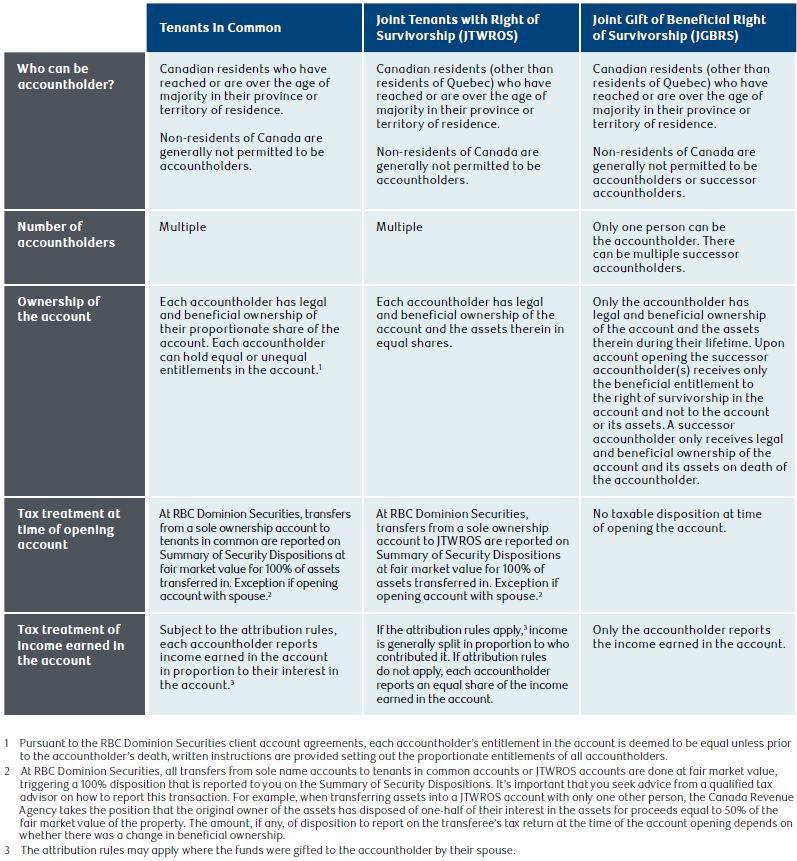

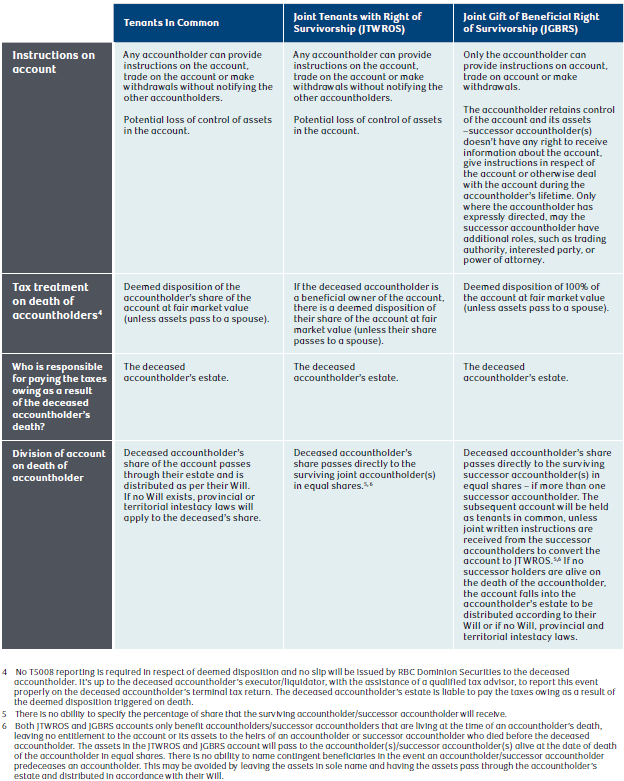

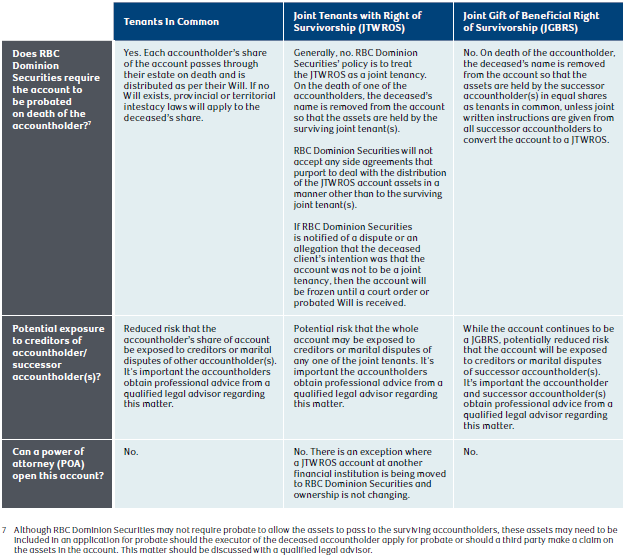

Types of joint tenancy accounts available at RBC Dominion Securities

Please note the following accounts are not available to residents of Quebec. A Quebec resident is not permitted to be an accountholder or successor accountholder of the following types of accounts.

Joint Tenants with Right of Survivorship (JTWROS)

By opening an RBC Dominion Securities JTWROS account and agreeing to the terms of the client account agreement, it's assumed by RBC Dominion Securities that all joint accountholders have both legal and beneficial ownership of the account. This means that not only are the accountholders the registered legal owners of the account, but all joint accountholders have beneficial ownership of the account, including the assets of the account as soon as the account is opened. On the death of one of the joint accountholders, the JTWROS account will be treated in accordance with the applicable client account agreement and account opening forms and the name of the deceased will be removed from the account so that the JTWROS is subsequently held in the name(s) of the surviving joint accountholder(s) without requesting probate. Although RBC Dominion Securities will generally not require probate as described above, these assets may need to be included in an application for probate should the executor of the deceased accountholder apply for probate or should a third party make a claim upon the assets of the account. It's important you discuss this matter with a qualified legal advisor before opening a JTWROS account.

Joint Gift of Beneficial Right of Survivorship (JGBRS)

RBC Dominion Securities JGBRS is a joint account which allows the accountholder to retain legal and beneficial ownership of the account, including the assets of the account, during their lifetime, while gifting the beneficial entitlement to the right of survivorship in the account to any friends and family members named as successor accountholder(s). The terms of the RBC Dominion Securities client account agreements governing the JGBRS account expressly state that the intention of the accountholder is to make an inter vivos gift of the beneficial entitlement to the right of survivorship in the account, at the time of account opening. Neither the account nor the assets therein are gifted at the time of account opening. This means that the successor accountholder(s) does not have any entitlement to or control over the account or its assets until the death of the accountholder. The successor accountholder(s) is not permitted to provide any instructions in relation to the account while the accountholder is alive or to withdraw funds from the account. Accordingly, the accountholder retains sole control of the account during their lifetime.

On the death of the accountholder, legal and beneficial ownership of the account and the assets held in the account will transfer to the successor accountholders. The name of the deceased will be removed from the account so that the JGBRS is subsequently held in the name of the successor accountholder(s) without requesting probate. If there are multiple successor holders, the holders will hold their portion as tenants in common, unless joint written instructions are given from all successor accountholders to convert the account to a JTWROS. Although RBC Dominion Securities does not require probate to allow the assets to pass to the successor accountholder(s), these assets may need to be included in an application for probate should the executor of the deceased accountholder apply for probate or should a third party make a claim to the assets in the account. It's important that you discuss this matter with a qualified legal advisor before opening a JGBRS account.

Comparing the joint account options at RBC Dominion Securities

For a comparison of the joint ownership accounts available at RBC Dominion Securities, please refer to the Appendix to this article. The Appendix highlights some of attributes of the different types of joint ownership accounts including probate considerations as well as taxes on account opening and death. We recommend you discuss these features with an independent, qualified legal advisor who may assist you in determining which account, if any, may be suitable in meeting your estate planning and financial objectives.

Key considerations before transferring assets into a joint account

Ability for the deceased accountholder's estate to pay taxes at death

Consider the potential tax implications of the following example:

Mr. X owns a non-registered investment account with a fair market value of $3 million and an adjusted cost base of $1 million, a house worth $400,000 and a registered retirement savings plan (RRSP) valued at $1 million. He's designated his wife as the beneficiary of his RRSP. Mr. X had previously opened a JGBRS account and transferred his non-registered investment account to a JGBRS account, naming his three daughters as successor accountholders.

Upon his death, his three daughters receive the assets in the JGBRS outright. Assuming a marginal tax rate of 50%, a $500,000 tax liability is triggered on the deemed disposition of the assets in the JGBRS account that's payable by Mr. X's estate. As the bulk of Mr. X's assets passed outside of his estate (only the $400,000 house formed part of the estate), there would be insufficient assets in his estate to pay the taxes owing. The executor of the estate would be faced with a liquidity issue and a potentially insolvent estate.

Lack of flexibility in making gifts and potential unintended consequences

There is no limit to the number of joint potential accountholders (JTWROS account) or successor accountholders (JGBRS account). However, the surviving joint accountholders may only receive the assets in the account in equal shares. There is no ability to specify the percentage share received by each surviving joint accountholder, which would limit your ability (as the accountholder) to gift assets to friends and family in differing proportions. Furthermore, any funds held in a JTWROS account or a JGBRS account would likely be unavailable to fund charitable or other bequests set out in your Will, as the assets generally pass outright to the surviving joint accountholder(s) and don't form part of your estate.

Both the JTWROS and JGBRS accounts only benefit joint accountholders that are living at the time of your death, leaving no entitlement to the heirs of a joint accountholder who has died before you. The assets in the JTWROS and JGBRS account will pass to the joint accountholder(s) alive at the time of your death in equal shares. There is no ability to name contingent beneficiaries in the event a joint accountholder predeceases you. This may be avoided by leaving the assets in your sole name and having the assets pass through your estate and distributed in accordance with your Will.

In the case of the JGBRS account, where the successor accountholder predeceases you, you could change the distribution by withdrawing the assets of the account, closing the account and opening a new JGBRS account with newly named successor accountholders. Note that changes to an account will not be possible where you no longer have mental capacity. Moreover, an attorney appointed pursuant to an enduring power of attorney is not permitted to make changes to a joint account.

In the event there are no surviving successor accountholders following your death, your assets would form part of your estate and will be distributed in accordance with your Will or if you have no Will, provincial or territorial intestacy laws.

Alternative estate planning vehicles and other strategies to consider

There may be estate planning vehicles or strategies other than a joint account that are more appropriate in light of your current or future estate planning objectives. Such vehicles and strategies may include, creating an alter ego trust or joint partner trust, setting up a testamentary trust in your Will, making an outright gift to adult children, or being the donor of a power of attorney.

Alter ego trust or joint partner trust

An alter ego trust (or a joint partner trust, if you wish to include your spouse as a beneficiary of this trust) is an inter vivos trust created by you when you're age 65 or older. The terms of the trust must provide that you (or your spouse in the case of a joint partner trust) are entitled to receive the income of the trust while alive and that no other person other than you (or your spouse) can receive or use the income or capital of the trust during your (or your spouse's) lifetime. One of the benefits of creating this trust is that you can generally transfer your capital property into this trust on a tax deferred basis. Any taxes on the accrued gains on the property transferred to the trust will be deferred until the property is subsequently sold or you (or your spouse in the case of a joint partner trust) die. This differs from the normal tax treatment when assets are transferred to an inter vivos trust, where you're immediately deemed to have disposed of your property at fair market value.

Another benefit to creating an alter ego or joint partner trust is that the assets placed in the trust will generally not form part of your (or your spouse's) estate on death and will not be subject to probate taxes. The terms of the trust document will determine how your assets are distributed after your (or your spouse's) death.

There are considerations relating to these types of trusts, such as the set up and administration costs, as well as the complexity of administering these trusts. You can choose to name RBC Estate & Trust Services as sole trustee, co-trustee, agent for trustee or successor trustee. This provides the benefit of professional advice and administrative support when dealing with potentially complex family dynamics.

Testamentary trust

A testamentary trust is a trust created by your Will which comes into effect on your death. It's generally funded with assets that form part of your estate. A testamentary trust is an alternative to a direct or outright distribution of estate assets. It provides a means of transferring your assets to your intended beneficiaries, while allowing you to control the timing and distribution of the assets to them. The assets held in the trust are invested and managed by the trustee of the trust, who distributes the income and capital to the beneficiaries in accordance with your wishes stated in your Will.

You may wish to consider a testamentary trust if you have concerns about your children's ability to manage finances or if you wish to provide a lasting legacy to your children, grandchildren and great grandchildren. A testamentary trust may also assist with respect to protecting your assets from the potential claims of your beneficiaries' creditors.

Outright gift

You may wish to consider a gift of assets outright to your adult children during your lifetime if you will not need the assets to support your living expenses. In this case, the gifted assets will generally not be included in the calculation of probate fees on your death. This strategy may suit your needs if you're comfortable giving up control of the assets and placing them in the control of your adult children. This also may appeal to you if you would like the next generation to benefit from your gift during your lifetime and you are comfortable that your adult children will manage the funds appropriately. There could, however, be tax and other consequences for you when you transfer the assets to your children, so it's important to obtain professional legal and tax advice before proceeding with this strategy.

Granting a power of attorney or a trading authority

If your intention in creating a joint account is to make it convenient for an adult child to manage your property, consider giving your adult child a power of attorney instead, which will allow your adult child to deal with the assets of your sole name account for your benefit during your lifetime. On your death, the assets of the account will form part of your estate. This will give you some certainty that on your death the assets in the account will go to your heirs in accordance with your wishes expressed in your Will. Another way to allow an adult child to assist you in managing your account is to grant trading authority (a form of limited power of attorney) over the assets in that account. This authority will not affect the way in which assets pass on your death, or your ability to continue to manage your assets during your lifetime. It will, however, enable your adult child, or any other person you choose to appoint, to make trading decisions on your behalf, within the parameters of the trading authority, which you have defined and granted. Your RBC Dominion Securities advisor and a qualified legal advisor will be able to discuss the types of authority available and the powers the different authorities can provide.

Choosing the right option for you

Should you choose to proceed with a joint account, it's important that you ensure the account attributes align with your current and future estate planning objectives. To ensure that your circumstances have been properly considered, you're advised to obtain professional advice from a qualified legal advisor. As part of any estate planning process, it's also important to prepare your loved ones who are receiving the assets with the right financial guidance. This may help them to feel empowered with the knowledge, skills and confidence they need to make smart financial decisions with their assets and work towards reaching their own goals. RBC Dominion Securities advisors are available to assist in providing financial guidance as well as educational strategies for your loved ones.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

Appendix - Comparing the joint account options at RBC Dominion Securities

Below you will find a summary of the three types of joint ownership accounts available at RBC Dominion Securities. This chart highlights some of the attributes of the different types of joint ownership accounts and may assist a qualified legal advisor in guiding you to determine which account, if any, may be suitable in meeting your estate planning objectives.