Family Office Services

February 14, 2024

Multiple Wills

As part of your estate planning, you may look for ways to reduce or avoid taxes payable on your death, including probate taxes. There may be several strategies available to you. The use of multiple Wills is one potential strategy you may wish to consider.

The multiple Wills strategy is discussed in more detail in this article; however, it may not apply to your specific circumstances. In particular, this strategy may not be available or relevant in all provinces, particularly where probate taxes are low or non-existent.

Probate taxes

When you pass away, your executor (or liquidator in Quebec) may be required to obtain a grant of probate in order to be able to fully administer your estate. Probate is an administrative procedure to validate a Will and confirm the authority of the executor named in the Will to act on behalf of the estate.

Your executor's authority is not derived from the probate process but from the Will itself. Third parties, however, may require probate in order to release your assets to your executor or change the legal ownership of property, such as securities or real estate. Probate offers the third parties protection against legal liability. For example, probate protects third parties from claims that assets were distributed to the wrong person. This is the case even if probate was granted in error and is subsequently revoked.

Most provinces charge a tax when your Will is probated, commonly known as "probate taxes". Probate taxes range from a nominal or low flat fee in some provinces to a percentage of the fair market value of the estate assets. In Quebec, a Notarial Will does not require probate.

The multiple Wills strategy

In an effort to reduce or avoid probate taxes, some estate planners advocate the use of multiple Wills. Historically, multiple Wills were used primarily to deal with assets held in different jurisdictions or where you wanted different executors to deal with different assets. Now, multiple Wills are also used in some provinces as a means of minimizing probate taxes.

The multiple Wills strategy involves segregating your assets so that different assets are subject to different Wills. For example, a "primary" Will may deal with assets that require probate in that jurisdiction, such as solely owned bank accounts, investment portfolios and real estate. A "secondary" Will may hold the remaining assets that do not require probate, such as privately held shares or personal effects, such as antiques, art and jewelry.

Where this strategy is available, your executor has the choice to probate any of your Wills, and probate taxes would only apply to the assets included in the Will being probated. By separating assets that may require probate from those that do not, you may therefore avoid paying probate on those assets that don't otherwise require probate.

Multiple Wills may also be structured based upon jurisdiction, to take advantage of lower or nominal probate taxes in different jurisdictions, such as Quebec and Alberta. For example, an Ontario resident who wishes to take advantage of the multiple Wills strategy may have an "Ontario" Will to deal with real property located in Ontario and an "Alberta" Will to deal with other property situated in Alberta. Note that if you're not domiciled in Quebec at the date of death, you can only use a separate "Quebec" Will to deal with real estate located in Quebec and not moveable assets, such as a bank account. Multiple Wills may also be used to simplify estate administration when assets are held in multiple jurisdictions.

In the right circumstances, multiple Wills can significantly reduce the probate taxes that the estate would otherwise pay. Whether or not multiple Wills should be used depends upon your intentions, the nature of the assets held, where they're held, the value of the assets, and the corresponding anticipated savings in probate taxes that follow from the implementation of this strategy.

Implementation of the multiple Wills strategy

While this strategy may be appealing, its successful implementation can be thwarted by improper drafting and execution of the Wills. Care must be taken by you and your professional advisors to ensure that common pitfalls are avoided. For example:

- The execution (signing) of one Will should not have the effect of revoking the other. The Wills should be carefully worded so the intention for multiple Wills to co-exist is clear.

- Each Will should clearly identify the property it's dealing with to avoid situations where multiple Wills deal with the same property in different ways or where more than one executor is appointed with authority over the same property.

- The Wills should identify which assets are to be used to pay debts and expenses of the estate, as well as legacies. Otherwise, this may cause conflict in the administration of the estate, particularly if there are different beneficiaries under each Will.

Private company shares

The multiple Wills strategy has, in recent years, been commonly used where an individual holds private company shares of considerable value because the transfer of ownership may not require probate. The reason is that provincial corporate statutes may offer the directors of a corporation the discretion to transfer a deceased shareholder's shares without probate.

If you're a director and/or officer of the corporation, a new director and/or officer may need to be appointed on your death. If you're the sole director and officer of the corporation, a new director and officer may need to be appointed before any instructions relating to your private corporation contained in your Will can be carried out. Your executor or your beneficiaries who've inherited your shares may be able to step into your shoes as shareholder and vote on your shares to remove and replace you as a director and/or officer of a corporation. Once the new officers and directors have been appointed, in accordance with the existing corporate constating documents (e.g. the articles of incorporation and by-laws), these changes must be filed with the appropriate government authority. New corporate documentation will also need to be provided to third parties (e.g. a financial institution with a corporate bank or investment account) to confirm the new officer's and/or director's authority to deal with corporate assets. (For corporate accounts held at financial institutions, probate may nonetheless be required by such financial institutions, guided by their internal policies, in order to make changes on the account.)

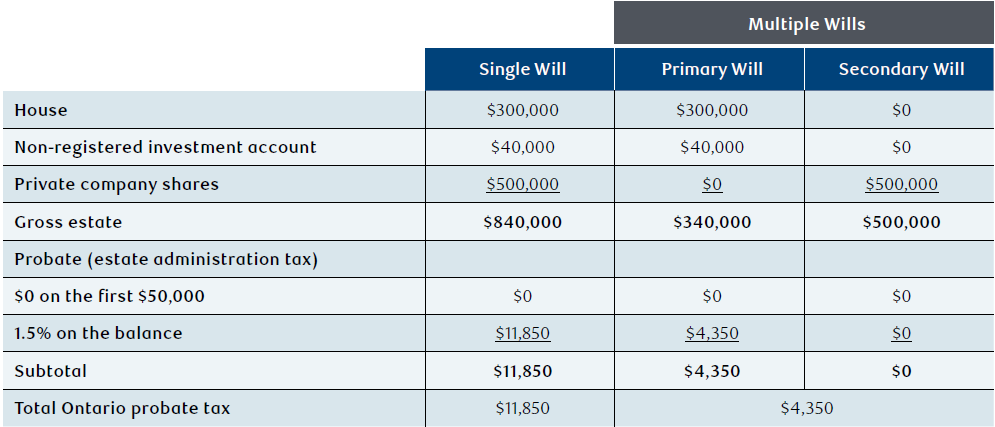

Example of how multiple Wills can be used to minimize probate taxes

Barry is the owner of a small privately owned business that's worth $500,000. He has a principal residence that's valued at $300,000 (no mortgage) and $40,000 in a non-registered investment account at RBC. Barry has no dependants and no spouse. He resides in Ontario.

What probate taxes would apply in the province of Ontario if Barry had one Will instead of multiple Wills?

As outlined, in Ontario, no probate fees are payable on the first $50,000 of the value of the estate. For an estate valued over $50,000, probate is calculated as $15 for every $1,000 (or part thereof) of the value of the estate above this level. If only one Will is used, the probate tax payable would be $11,850. If multiple Wills are used, the probate taxes payable would be reduced to $4,350. Barry may save $7,500 by using a secondary Will to deal with the private company shares, provided they don't require probate.

Circumstances where a secondary Will might require probate

There are a few scenarios where a secondary Will might require probate. These include:

- If one of your Wills is contested by beneficiaries or other interested parties.

- If third parties are unable to effect a change of ownership of assets dealt with in a secondary Will.

- If the Will does not provide for an outright distribution of the deceased's assets but rather requires ongoing administration. Such may be the case where the Will creates trusts. A financial institution may be unable to open an estate or testamentary trust account without a probated Will because of the potential unlimited liability to which it may be exposed. A financial institution may be held liable if it negotiates a cheque payable to the estate or trust where the Will presented may not be the last Will of the deceased, or if it's not a valid Will and the executor doesn't have the legal authority to act on behalf of the estate. This issue should be considered and discussed with your financial institution as well as your estate planning lawyer at the time of drafting your secondary Will.

- If there's a concern that one of these issues may arise, it may not be worthwhile implementing the multiple Will strategy.

Benefits of obtaining probate

Although certain assets may not require probate to change ownership and thus can be dealt with in a secondary Will, it may still be beneficial to obtain probate. The benefits of obtaining probate include:

- Probate starts the clock on claims that can be made against the estate – certain claims that may be brought against an estate may be time limited. Depending on applicable law, the limitation period may run from the date of the grant of probate. Without the grant of probate, the limitation period may never expire.

- Protection for the executor – if an executor administers an estate pursuant to a Will that has not been probated, and the Will is later found to be invalid, the executor may be personally liable to the proper beneficiaries.

- Protection for third parties – probate provides third parties, such as banks and brokerage firms, with confirmation that they're dealing with the person who's legally authorized to act on behalf of the deceased's estate. It protects them from future claims that the deceased's assets were transferred to the wrong person.

Provincial differences

Each province has its own legislation that affects the application of the multiple Wills strategy. Not all provinces recognize multiple Wills. As well, probate taxes are based on provincial statutes. If you live in a province that has very low or nominal probate taxes, there may not be a necessity for this strategy. It's imperative that your estate planning lawyer verifies the validity of this strategy in your jurisdiction prior to implementation.

Conclusion

The multiple Wills strategy may help you reduce the probate taxes payable on your death.

For more information on the multiple Wills strategy and whether it should be implemented as part of your overall estate plans, you're advised to consult with a qualified legal advisor.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from an estate planning lawyer, tax, legal and/or insurance advisor before acting on any of the information in this article.