Pension income splitting

Your family may be able to reduce its total tax bill by allocating certain types of retirement income from a spouse who's subject to tax at a higher rate to a spouse who's subject to tax at a lower rate. This article summarizes the pension income splitting rules, which you may want to consider as part of your overall retirement income plan.

Your family may be able to reduce its total tax bill by allocating certain types of retirement income from a spouse who's subject to tax at a higher rate to a spouse who's subject to tax at a lower rate. This article summarizes the pension income splitting rules, which you may want to consider as part of your overall retirement income plan.

Family Office Services

October 14, 2025

Pension Income Splitting

Your family may be able to reduce its total tax bill by allocating certain types of retirement income from a spouse who's subject to tax at a higher rate to a spouse who's subject to tax at a lower rate. This article summarizes the pension income splitting rules, which you may want to consider as part of your overall retirement income plan. Any reference to a spouse in this article also includes a common-law partner.

The Basics

Who Can Benefit from Pension Income Splitting?

If you or your spouse receives eligible pension income during the year, one of you can allocate, or split, up to 50% of the eligible pension income to the other spouse. These rules benefit couples where the recipient of the eligible pension income is subject to tax at a higher rate than their spouse. By shifting some of the higher-taxed income into the lower-taxed spouse's hands, you can lower your overall family tax bill.

To be eligible for pension income splitting, generally both of you must be residents of Canada on December 31 of the tax year.

When eligible pension income that was subject to withholding tax is allocated to a spouse, a proportionate amount of the withholding tax is also allocated to the spouse. For example, pension payments received from a company pension are likely subject to withholding tax. If you choose to allocate 40% of the pension payment to your spouse, 40% of the withholding tax on these payments would also be credited to your spouse. When your spouse files their tax return, the credit can be used to reduce their taxes payable or may result in a tax refund.

Eligible Pension Income

For the purposes of splitting pension income, the transferring spouse is the individual who receives eligible pension income and elects to allocate part of that income to their spouse (the receiving spouse).

Only certain income is eligible to be split under the pension income splitting rules. The type of income that's eligible depends on the age of the transferring spouse. While the age of the receiving spouse isn't relevant for the purposes of these rules, their age may be relevant for determining whether they qualify for a non-refundable pension tax credit.

Here are some examples of eligible pension that may be split with your spouse (this list is not exhaustive):

For a transferring spouse who's age 65 or over during the year:

1. A life annuity payment from a superannuation or employer pension plan (including the Saskatchewan Pension Plan)

2. In certain cases, a life annuity payment from a retirement compensation arrangement (RCA)

3. An annuity payment from a registered retirement savings plan (RRSP)

4. A payment from a pooled registered pension plan (PRPP)

5. A payment from a RRIF, LIF, RLIF, LRIF or prescribed RRIF

6. An annuity payment from a deferred profit-sharing plan (DPSP)

7. A payment (including the income portion) from a regular annuity or an income averaging annuity contract

8. A payment from certain foreign pension plans (including U.S. Social Security)

For a transferring spouse who's under age 65 during the year:

1. A life annuity payment from a superannuation or employer pension plan (including the Saskatchewan Pension Plan)

2. A payment described in 3 to 7 from the previous list that you receive as a consequence of the death of your spouse

3. A payment from certain foreign pension plans (including U.S. Social Security)

Income That Doesn't Qualify

The types of income that don't qualify for pension income splitting include:

• Old age security (OAS) benefits

• Canada Pension Plan (CPP) benefits

• Quebec Pension Plan (QPP) benefits

• Death benefits

• Retiring allowances

• RRSP withdrawals, other than annuity payments from an RRSP

• Amounts from a RRIF that are transferred to an RRSP, another RRIF or an annuity

• Any foreign source pension income that's not taxable in Canada

• Income from a U.S. Individual Retirement Account (IRA)

• Amounts received from a salary deferral arrangement

The Election to Split Pension Income

If you and your spouse decide to pension income split, both of you will need to file a joint election. The filing due date is generally April 30 (or June 15 for self-employed taxpayers and their spouses) of the year following the tax year you plan to make the election. The election is made on the Canada Revenue Agency (CRA) Form T1032 – Joint Election to Split Pension Income. This form is available on the CRA website.

There's nothing in particular that needs to be done at the time you receive the income because the income is not split at source. As a couple, you can decide how much income to allocate, if any, between the two of you. In fact, there's no need to transfer the pension income that's allocated for tax purposes to a spouse. The joint election allows you and your spouse to split the income on your tax returns to reduce your family's total tax payable without the requirement of physically splitting the money.

Pension Splitting in the Year of Death

The maximum amount of eligible pension that can be split may be affected where a spouse passes away in the year. If the transferring spouse passes away, there's no change — up to 50% of the eligible pension income they received can be split. If the receiving spouse passes away, the maximum amount of eligible pension income received by the transferring spouse that can be split will be pro-rated.

Consider a couple, Spouse A and Spouse B, where Spouse A received eligible pension from January to June. If Spouse A passes away in June, the maximum amount of eligible pension income that can be split is calculated in the same way as it was for the years prior to death. For example, if Spouse A had $20,000 of eligible pension income, they'd be eligible to allocate up to 50% of the $20,000, or $10,000, to the surviving spouse. However, if instead Spouse B passes away in June, the amount that can be split is pro-rated for the months they were alive, up to and including the month of death. Using the same example, Spouse A can allocate up to 50% of $20,000 multiplied by 6 out of 12 months, or $5,000, to Spouse B.

The pension income splitting form must be filed with both the deceased's final return and the surviving spouse's return in order to split the eligible pension income. If the form is being completed after the date of death, the surviving spouse and the legal representative of the deceased spouse's estate must sign the form.

How Much Will the Tax Savings Be?

The amount of tax savings will depend on a number of factors, including the amount of eligible pension income you or your spouse receive and the difference between you and your spouse's marginal tax rates. Once the lower-income spouse's taxable income is the same as the higher-income spouse's taxable income, there's generally no further tax savings from allocating more income from the higher-income spouse to the lower-income spouse. For example, you may only need to allocate 20% of the higher-income spouse's pension income to the lower-income spouse to equalize their incomes. You do not need to allocate the full 50%.

You should also be aware that pension income splitting may impact certain government benefits and tax credits such as OAS.

Although it's obvious that it makes the most sense to split your eligible pension income when you and your spouse are in different tax brackets, there are some lesser-known reasons for splitting eligible pension income.

The following sections outline some aspects you may want to consider when determining whether to pension income split.

Pension Income Tax Credit

If you're receiving eligible pension income, you may be entitled to claim both a federal and a provincial/territorial tax credit. The federal non-refundable pension income tax credit is available on the first $2,000 of eligible pension income. This translates into a maximum federal annual tax savings of $280 (based on the federal tax credit rate of 14% for 2026 and subsequent tax years). The amount of additional provincial/territorial tax savings varies depending on where you reside.

While the age of the receiving spouse doesn't matter when pension income splitting, the spouse's age is relevant in determining whether they qualify for the pension income tax credit. If the spouse receiving the eligible pension income is at least age 65 during the tax year, they'll be able to claim the pension income tax credit on any type of pension income allocated to them by the transferring spouse. If the spouse receiving the eligible pension income is younger than 65 during the entire tax year, they'll only be able to claim the pension income tax credit on pension income that's eligible for individuals under age 65 allocated to them by the transferring spouse. For more information on the pension income tax credit, please ask your RBC advisor for a copy of the article on that topic.

If only one of you is currently receiving eligible pension income, you and your spouse may want to split that eligible income so you can both claim the pension income tax credit (assuming other relevant conditions are met).

Clawback of OAS Benefits

If you're receiving OAS benefits, you will be subject to a 15% OAS clawback for every dollar of your net income that exceeds the OAS clawback threshold. Allocating eligible pension income from a higher-income spouse can reduce their taxable income and bring it below the OAS clawback threshold. This will not only reduce the family's income taxes but may also increase the OAS funds the family receives.

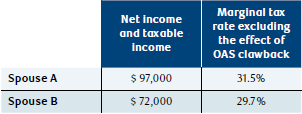

For example, consider a couple living in Ontario. Spouse A is receiving a company pension while Spouse B's primary source of retirement income is investment income. The amount of pension Spouse A is receiving is sufficient to enable the couple to equalize their incomes under the pension income splitting rules.

Also, assume Spouse A is currently receiving OAS benefits. Some of their OAS benefits will be subject to clawback since Spouse A's net income exceeds the OAS clawback threshold for the year.

While the income tax savings for the couple will be minimal, the allocation of $5,000 under the pension income splitting rules will result in an elimination of OAS clawback and, therefore, provide this couple with additional savings.

Summary

The pension income splitting rules affect both the retirement savings and retirement income planning strategies of many Canadian families. In many cases, the opportunity to reduce your family's tax bill during retirement may be meaningful.

Generally, you'll calculate your family's tax savings at the time you prepare your income tax return. After you know your and your spouse's total income, you can determine if and how you should split your eligible pension income.

Since everyone's tax situation is different, it's important to discuss your circumstances with a qualified tax advisor in order to make the best decisions possible for you and your family.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.