Pension income tax credit

If you're receiving eligible pension income, you may be entitled to claim both a federal and a provincial/territorial tax credit. The federal non-refundable pension income tax credit is on the first $2,000 of eligible pension income, which translates to a maximum federal annual tax savings of $280 (for 2026 and subsequent tax years). The amount of additional provincial/territorial tax savings varies depending on where you reside. This article addresses the types of pension income that qualify for the tax credit and what to consider if you'd like to structure your retirement holdings to take advantage of this credit.

If you're receiving eligible pension income, you may be entitled to claim both a federal and a provincial/territorial tax credit. The federal non-refundable pension income tax credit is on the first $2,000 of eligible pension income, which translates to a maximum federal annual tax savings of $280 (for 2026 and subsequent tax years). The amount of additional provincial/territorial tax savings varies depending on where you reside. This article addresses the types of pension income that qualify for the tax credit and what to consider if you'd like to structure your retirement holdings to take advantage of this credit.

Family Office Services

October 14, 2025

Pension Income Tax Credit

Potential tax credit on $2,000 of your pension income

If you're receiving eligible pension income, you may be entitled to claim both a federal and a provincial/territorial tax credit. The federal non-refundable pension income tax credit is on the first $2,000 of eligible pension income, which translates to a maximum federal annual tax savings of $280 (for 2026 and subsequent tax years). The amount of additional provincial/territorial tax savings varies depending on where you reside. This article addresses the types of pension income that qualify for the tax credit and what to consider if you'd like to structure your retirement holdings to take advantage of this credit. Any reference to a spouse in this article also includes a common-law partner.

What is the Pension Income Tax Credit?

If you receive income from sources such as an employer pension plan, certain annuities or a registered retirement income fund (RRIF), you may be able to claim a tax credit on up to $2,000 of that income. The federal tax credit rate is based on the lowest personal marginal tax bracket (14% for 2026 and subsequent tax years). This results in maximum federal tax savings of $280 ($2,000 x 14%). You may also be eligible for a provincial/territorial pension income tax credit.

The federal pension income tax credit is non-refundable, which means you only benefit from the credit if you owe federal income tax. It reduces your federal taxes payable. If you don't need to claim all of the credit in order to reduce your federal taxes to zero, you may transfer any unused amount to your spouse. Any unused amount can't be carried forward or back to other tax years.

What Types of Income Qualify for the Credit?

65 years of age or over during the year

If you're age 65 or over at any point during the year, you can claim the pension income tax credit if you receive the following types of income:

1. Life annuity payments from a superannuation or employer pension plan (including the Saskatchewan Pension Plan)

2. Annuity payments from a registered retirement savings plan (RRSP)

3. Payments from a pooled registered pension plan (PRPP)

4. Payments from a RRIF, LIF, an RLIF, LRIF or prescribed RRIF

5. Annuity payments from a deferred profit-sharing plan (DPSP)

6. Payments (including the income portion) from a regular annuity or an income averaging annuity contract

7. Payments from certain foreign pension plans (including U.S. Social Security), or

8. Elected split pension income reported on your tax return

Under 65 years of age for the entire year

If you've not reached age 65 by the end of the year, you can claim the pension income tax credit if you receive the following types of income:

1. Life annuity payments from a superannuation or employer pension plan (including the Saskatchewan Pension Plan)

2. Payments described in points 3 to 7 in the previous section that you received as a consequence of the death of your spouse

3. Payments from certain foreign pension plans (including U.S. Social Security), or

4. Elected split pension income reported on your tax return that your spouse received from a life annuity payment from a superannuation or employer pension plan

What Types of Income Do Not Qualify for the Credit?

The following are some types of income you may receive at retirement that do not qualify as eligible pension income for the purposes of the pension income tax credit:

• Old age security (OAS) benefits

• Canada Pension Plan (CPP) benefits

• Quebec Pension Plan (QPP) benefits

• Death benefits

• Retiring allowances

• RRSP withdrawals other than annuity payments from an RRSP

• Amounts from a RRIF that are transferred to an RRSP, another RRIF or an annuity

• Any foreign source pension income that's tax-free in Canada

• Income from a U.S. Individual Retirement Account (IRA)

• Amounts received from a salary deferral arrangement

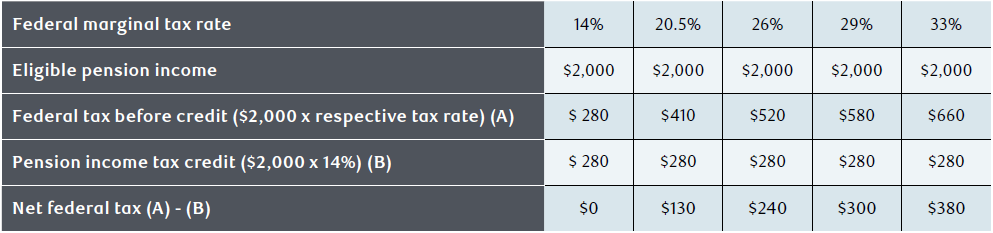

How Much Tax Do You Save With This Credit?

If you're in the lowest federal marginal tax bracket, you can essentially receive the first $2,000 of eligible pension income tax-free for federal tax purposes. This is because the federal tax credit and the lowest federal marginal tax rate on personal income are both 14% (for 2026 and subsequent tax years). If you're in a higher tax bracket, you will pay tax on the first $2,000 of eligible pension income, but at a reduced rate.

The pension income amount that's eligible for the provincial/territorial tax credit varies by jurisdiction. The rate that's used to calculate the tax credit also varies by jurisdiction. The rate generally mirrors the tax rate of the lowest marginal tax bracket. Therefore, the actual tax benefit of the pension income tax credit differs across all provinces/territories. For example, the maximum pension income amount in British Columbia is $1,000 with the tax credit at a rate of 5.06%, while the maximum pension income amount in Ontario is $1,762 (for 2025) with the tax credit at a rate of 5.05%.

Should You Structure Your Retirement Holdings to Qualify for the Credit?

If you're between the ages of 65 and 71 with no pension income, you might want to consider converting all or a portion of your RRSP funds to a RRIF and drawing $2,000 per year from the RRIF, subject to RRIF minimum payment requirements. This will allow you to claim the pension income tax credit. Before implementing this strategy, consider the following.

The maximum amount of the federal annual tax savings is limited to $280 (for 2026 and subsequent tax years). If you're in a higher tax bracket, the $2,000 of eligible pension income you receive will not be tax-free. You'll have to pay the incremental tax at your marginal tax rate. Any pension income you receive for the year above $2,000 will also be taxed at your marginal tax rate.

Additionally, depending on your province/territory of residence, it may be the case that you will owe provincial/territorial taxes on the $2,000 of pension income since the provincial/territorial pension income tax credit amount may be less than the federal income tax credit amount of $2,000.

Lastly, the choice to withdraw funds early from your registered plan is a trade-off between the benefit of lower taxes due to the pension income tax credit and the potential benefit of tax-deferred growth within your registered plan. You may want to compare the benefit of the annual tax savings due to the pension income tax credit with the value of the forgone future tax-deferred income due to the early receipt of your RRIF income.

Your RBC advisor, along with a qualified tax advisor, can help you evaluate whether structuring your investments to qualify for the pension income tax credit makes sense for you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.