Preparing your operating company for future sale (Part 1)

Owning a business presents opportunities and challenges for tax, retirement and estate planning. This article is the first in a four-part series intended to highlight key strategies to consider at different stages of your business. Part 1 introduces some tax planning strategies to consider when you're operating your business as a going concern.

Owning a business presents opportunities and challenges for tax, retirement and estate planning. This article is the first in a four-part series intended to highlight key strategies to consider at different stages of your business. Part 1 introduces some tax planning strategies to consider when you're operating your business as a going concern.

Family Office Services

October 14, 2025

Preparing Your Operating Company for Future Sale

Sale of your business - Part 1

Owning a business presents opportunities and challenges for tax, retirement and estate planning. On one hand, keeping your business structure simple makes things less complex and less costly to operate. On the other hand, a more complex structure may allow you to better minimize your tax liabilities on an ongoing basis and allow you to minimize the taxes payable in the future if you eventually sell your business to a third party.

This article is the first in a four-part series intended to highlight key strategies to consider at different stages of your business. It isn't exhaustive, but it may help you gain a deeper understanding of some strategies you're already using or that might be suggested to you. Part 1 introduces some tax planning strategies to consider when you're operating your business as a going concern. It assumes you have no immediate plans to sell but that you may consider selling in the future.

The other articles in the series are:

- Part 2: Planning the sale of your business

- Part 3: Year of sale of your business

- Part 4: Year after the sale of your business

In this article, the terms "corporation" and "company" are used interchangeably to refer to a Canadian-controlled private corporation (CCPC). In simple terms, a CCPC is a private Canadian corporation that's not controlled by a non-resident of Canada, a public corporation or a combination; in addition, no class of shares of the corporation is listed on a designated stock exchange. This four-part series does not apply to public corporations or to businesses operating as a partnership or a sole proprietorship.

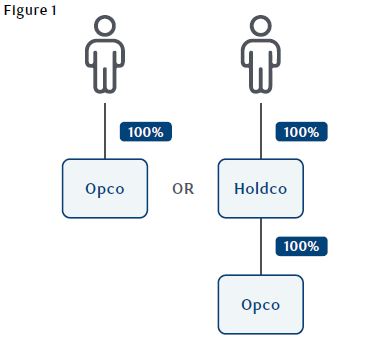

Current corporate structure

Even when selling your business is a distant event, when you're 100% owner of your operating company (Opco), or 100% owner of a holding company (Holdco) that owns 100% of your Opco, your business may not be structured in the most tax-efficient manner for a future sale. This type of structure will not easily allow for the multiplication of the lifetime capital gains exemption (LCGE) with other family members on the sale of the shares of your qualified small business corporation (QSBC).

Multiplying the LCGE could result in significant tax savings on the sale of QSBC shares, as each individual resident in Canada can claim an LCGE on the disposition of QSBC shares. The LCGE allows you to exempt capital gains up to a certain threshold on the sale of qualifying property.

Consider a more flexible structure

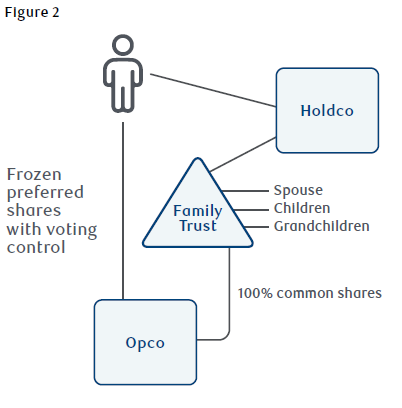

If your corporate structure looks like one of the two depicted in Figure 1, you may want to consider reorganizing your corporation so your spouse and/or children and grandchildren (or any other family member you desire) own shares of your corporation, either directly or indirectly through a discretionary family trust. This may allow you to multiply the LCGE available on the eventual sale of your business and may allow for income splitting with your family members, to the extent that the tax on split income (TOSI) rules, which restrict income splitting in certain instances, don't apply. Where the TOSI rules apply, dividends received are not eligible for many personal tax credits and tax is applied at the top marginal tax rate. Please ask your advisor for a copy of the article that discusses income splitting through private corporations for more information. The step-by-step procedures to implement this structure are beyond the scope of this article, but the major components are briefly mentioned.

The structure in Figure 2 is usually achieved by doing an estate freeze where you exchange the shares you currently own for fixed-value preferred shares and your corporation issues new common shares, either directly or indirectly through a discretionary family trust, to other family members. The use of a family trust may allow for more flexibility in terms of tax planning and increased control. A family trust may be necessary if minors are involved. In addition, you may want to include a Holdco as a beneficiary of the family trust. Having a Holdco as part of the structure may allow you to keep your operating business as a QSBC by paying out excess funds in the Opco to the Holdco, rather than directing the excess funds to the other beneficiaries of the trust. This structure may also provide better creditor protection; however, you should speak to a qualified legal advisor about the extent of creditor protection provided from the structure illustrated in Figure 2.

If you're implementing an estate freeze, you should be aware of the corporate attribution rules. Corporate attribution applies when property is loaned or transferred by an individual to a corporation, and their spouse or minor child can benefit from this transfer. A typical estate freeze is viewed as a transfer to a corporation. Corporate attribution applies to corporations other than a small business corporation (i.e. 90% or more of its assets are used in an active business). Therefore, as long as the Opco continues to be a small business corporation, these rules do not apply.

Ongoing purification techniques

You may be able to structure your business so that you can purify the company by keeping both the purification refers to maintaining your Opco's status as a QSBC by removing surplus assets that are not part of its active business. There are a number of possible structures available and you may be able to set up the structure by using an estate freeze. The following is an example of one alternative that may allow for ongoing purification using a trust with a corporate beneficiary. Here are the typical steps to implement this structure:

1. Mrs. A establishes Holdco and subscribes for super voting special shares to maintain control of the company

2. A family trust is settled and the trust subscribes for the common shares of Holdco; Holdco is also named as one of the beneficiaries of the family trust

3. Mrs. A exchanges her common shares of Opco for frozen non-voting preferred shares for the fair market value of Opco and nominal special voting shares

4. The family trust subscribes for non-voting common shares of Opco

5. When Opco generates after-tax surplus funds that are not needed by the business, dividends can be paid on the common shares held by the family trust, the dividends can then be allocated by the trust to either the family members who are beneficiaries of the trust or Holdco (or both), it is important to seek advice before allocating dividends to family members, as they could be subject to the TOSI rules

6. Dividends allocated to the family member beneficiaries are taxed in their hands at their marginal tax rates (assuming the trust is properly structured and none of the attribution rules or TOSI rules apply)

7. Dividends allocated to Holdco may be considered a tax-free inter-corporate dividend from a connected corporation, assuming they're not re-characterized by any anti-avoidance provisions in the Income Tax Act; it's important to consult with a qualified tax advisor before paying inter-corporate dividends to ensure they don't fall into the anti-avoidance provisions

Tax strategies to consider at this stage of your business

- The LCGE available on the disposition of QSBC shares can be multiplied if you and your family members own shares of your corporation, directly or indirectly. The definition of QSBC shares is beyond the scope of this article. For more information, ask your RBC advisor for the article on the capital gains exemption on private shares. The structure in Figure 2 puts you in a better position to multiply the LCGE in the future. Each beneficiary of the trust who's an individual may be able to claim an LCGE when the shares of your qualifying business are sold. For your family members to qualify for the LCGE, the trust in Figure 2 must hold the shares for at least 24 months before the sale because the shares were issued from treasury. You would not be able to set this structure up immediately before a sale to multiply the LCGE because of this 24-month holding period test. This is why implementing a suitable structure to meet your objectives or provide flexibility at this stage is important. In addition, the value of the business must increase after the estate freeze to allow the beneficiaries' interest to grow so they can take advantage of their LCGE.

Further, for each beneficiary to be able to claim their LCGE, the qualifying capital gain must be taxable in their hands. This can only be done by paying (or making payable) the taxable capital gain on the sale of the QSBC shares to the beneficiaries. Therefore, you must be comfortable with each beneficiary receiving their portion of the sale proceeds that's taxable in their hands.

There is a 21-year deemed disposition rule for trusts, so you may not want to implement this strategy too early if you intend to have your business for that long. If your children are very young and 21 years from now, you wouldn't be comfortable transferring the shares of your business directly to them, you may want to wait.

- As part of the reorganization to implement a structure like Figure 2, you may consider crystallizing your LCGE at that time. When your existing common shares of Opco are exchanged for frozen preferred shares, you can elect to transfer your shares at a value somewhere between your adjusted cost base (ACB) and the fair market value (FMV) of your common shares. This allows you to elect an amount so that you can trigger a capital gain sufficient enough for you to claim your LCGE. In doing this, the ACB of the preferred shares received will be bumped up to the amount you elected.

- The structure illustrated in Figure 2 may also allow for ongoing purification of Opco. In particular, to qualify as a QSBC, in the 24 months immediately before the sale of the shares, the corporation must have more than 50% of its assets used in an active business carried on primarily in Canada. Since you may not know when an interested party may offer to buy your company, it may be prudent to always keep your Opco ready so that if you decided to sell, you have the most tax-efficient structure. The structure in Figure 2 may allow excess funds not needed for the operating business to be paid as a dividend to the family trust. The trustee(s) of the discretionary family trust can then pay the dividend to Holdco. As long as Holdco is properly structured, the dividend may be considered an inter-corporate dividend and may not be taxable to Holdco. In recent years, the income tax rules with respect to inter-corporate dividends have been severely restricted. It's important to discuss with a qualified tax advisor whether your operating company will be able to pay a tax-free inter-corporate dividend to the holding company. Assuming you are able to pay tax-free inter-corporate dividends to Holdco, the added benefit of this structure is that it may provide creditor protection for Opco since all excess assets are removed from Opco without immediately triggering tax. You should consult with your qualified legal advisor with respect to the extent of the creditor protection provided.

- At this stage of your business (i.e. when there's no pending sale or plan to sell your business in the near future), it may be easier to purify Opco for LCGE purposes and to increase its attractiveness to buyers. This may be the best time to transfer redundant assets held in Opco, such as real estate, an investment portfolio and life insurance, etc. either to a Holdco or a sister company.

- You may want to extract surplus assets from your corporations in order to maintain your small business deduction. Active business income up to the business limit benefits from the small business deduction, which lowers the corporate tax rate on such income. The federal business limit as well as the business limit for most provinces is $500,000. If your corporation and any associated corporation(s) earns more than $50,000 of passive income in a given year, your corporation's ability to claim the small business deduction may be affected. Where passive income is earned in excess of $50,000 in the previous year, access to the business limit is ground down on a straight-line basis by $5 for every $1 of passive income above $50,000. This may result in higher corporate taxes being paid on your corporation's active business income. Speak with your RBC advisor for the article on withdrawing surplus cash from a corporation.

Factors affecting company value

At this stage of operating your business, you'll want to understand the various factors that affect your company's value to ensure you continue to build on your strengths, work on your weaknesses, take advantage of opportunities and mitigate risks so you can continue to grow your business. In addition, some of the strategies discussed earlier will require you to properly value your business. Here are some factors that influence the value of your company:

• Consistent, recurring, growing cash flow

• Certainty of cash flow

• Favourable industry dynamics

• Management team

• Growing diversified customer base

• Sustainable competitive advantage

• Price-sensitive commodity product/proprietary offering

• Barriers to entry

• Public/private/scale

Some of the factors noted are discussed briefly in Part 2 of this series, "Planning the sale of your business."

Conclusion

The strategies discussed in this article are complex both from a tax and legal perspective but have the potential to save significant amounts of tax. Consequently, it's important to get qualified legal and tax professionals involved to ensure you accomplish your goals and avoid unnecessary challenges.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.