Prescribed rate loan annual interest payments due by January 30

To ensure that the prescribed rate loan you made to a spouse, or a family trust, continues to meet the requirements to split income, the required annual interest payment must be made to you by January 30 of the following year. If the annual interest payment is not made by January 30, the attribution rules may be triggered for that particular year and every subsequent year that the loan is in place.

To ensure that the prescribed rate loan you made to a spouse, or a family trust, continues to meet the requirements to split income, the required annual interest payment must be made to you by January 30 of the following year. If the annual interest payment is not made by January 30, the attribution rules may be triggered for that particular year and every subsequent year that the loan is in place.

Family Office Services

June 14, 2025

Prescribed rate loan annual interest payments due by January 30

To ensure that the prescribed rate loan you made to a spouse, or a family trust, continues to meet the requirements to split income, the required annual interest payment must be made to you by January 30 of the following year. If the annual interest payment is not made by January 30, the attribution rules may be triggered for that particular year and every subsequent year that the loan is in place, effectively defeating your ability to income split. Any reference to spouse in this article also includes a common-law partner.

The attribution rules

There are attribution rules in the Income Tax Act designed to prevent family income splitting in certain circumstances. For example, if you transfer assets directly to your spouse, then income and capital gains derived from those assets may be attributed back to you and taxed in your hands. Similarly, if you transfer the assets indirectly to your spouse, for example, through a family trust, the income and capital gains paid out or made payable to your spouse may be attributed back to you.

In addition, if you transfer assets to a trust for the benefit of your minor child (including your niece or nephew), then interest and dividends derived from those assets and paid out or made payable to the beneficiaries will be attributed back to you, effectively defeating your ability to income split.

There are exceptions to the attribution rules. One exception is where you loan money at the Canada Revenue Agency (CRA) prescribed interest rate in effect at the time the loan was made, instead of simply transferring the assets to your spouse or trust for the benefit of your family members. To ensure that the income earned is not attributed back to you, the interest on the loan should be paid by January 30 of the following year (and by January 30 of every subsequent year that the loan is in place). It's crucial to meet this deadline, because if the interest payment is late by even one day, the attribution rules may apply for the year the interest payment is related to, and all subsequent years, until the loan is repaid.

Making the interest payment

Where you make a loan to your spouse, your spouse should pay you the interest using their own funds. The payment of interest from a joint account may be problematic, as your spouse would need to clearly demonstrate that the interest payment is made using their own funds. Your spouse should also document that the payment is for interest owed on the loan for the relevant tax year.

Where you make a loan to a family trust, the trust should also pay you the interest using the trust funds. The trust should maintain sufficient records and receipts to evidence that an annual interest payment was made.

Calculating the amount of interest

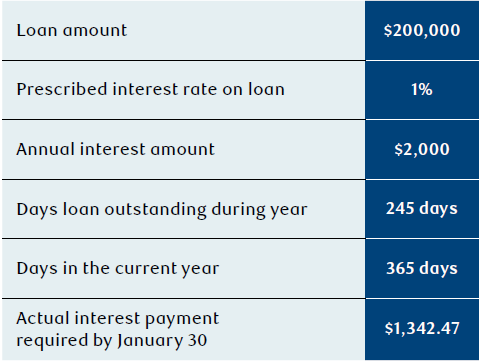

Let's assume you want to split income with your spouse and minor child. You loan $200,000 to a family trust on May 1 of Year 1 at the prescribed interest rate of 1%. The following table illustrates the elements needed to calculate the interest amount.

The interest owing for Year 1 is prorated based on the number of days the loan was outstanding during the year (245 out of 365 days). To avoid attribution of any income earned on the $200,000 loaned to the family trust that was paid or made payable to your spouse or minor child, the trust would have to pay you interest of $1,342.47 for Year 1 by January 30 of Year 2.

Note that even if the prescribed rate increases or decreases during the year or subsequent years, the rate that was in effect when the loan was established is the rate that is used to calculate the interest that is payable on the loan.

Tax reporting for interest paid and received

If you lend money to a family trust, the trustee may need to file an annual T5 information return to report the interest paid to you, the lender, and provide you with a T5 slip detailing the interest paid. If you lend money to an individual family member, that family member is not required to file a T5 return or issue you a T5 slip for the interest paid.

Regardless of whether a T5 slip is issued or not, the lender is required to include the interest received or receivable on their income tax return.

Generally, the timing of the income inclusion or deduction on the prescribed rate loan depends on the year the interest is related to, when the interest is received or paid, and the method (cash vs. accrual) the individual regularly follows in computing their income.

Ensuring the demand promissory note is enforceable

Depending on the governing legislation of your loan agreement, making the annual interest payments on the prescribed rate loan may be sufficient action to avoid the promissory note from becoming unenforceable. In other words, making the interest payment annually can be seen as an acknowledgement by the borrower that the loan is still outstanding and enforceable. Alternatives are to renew the note on an annual basis or to have your spouse and/or the trust acknowledge in writing that the promissory note is still valid. You should consult with a qualified legal advisor to ensure that your promissory note remains legally enforceable.

Conclusion

If you have loaned funds to your spouse or a family trust for the purpose of income splitting, it's important to ensure that the interest payments are made to you by January 30 of the following year. For each year the loan is outstanding, this allows income and capital gains to be taxed in the hands of your spouse or your other family members and not be subject to the attribution rules.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.