Real return bonds

This article provides an overview of real return bonds (RRB). It discusses what they are, how interest and maturity values are calculated and how they are taxed. The unique characteristics of these bonds and how they are taxed may create a prepayment of tax which may make them more suitable to holding in registered accounts, such as registered retirement savings plans (RRSPs) or tax-free savings accounts (TFSA). In addition, the tax reporting and record keeping for RRBs can be complex further adding merit to holding an RRB in a registered account.

This article provides an overview of real return bonds (RRB). It discusses what they are, how interest and maturity values are calculated and how they are taxed. The unique characteristics of these bonds and how they are taxed may create a prepayment of tax which may make them more suitable to holding in registered accounts, such as registered retirement savings plans (RRSPs) or tax-free savings accounts (TFSA). In addition, the tax reporting and record keeping for RRBs can be complex further adding merit to holding an RRB in a registered account.

Family Office Services

January 14, 2021

Real return bonds

This article provides an overview of real return bonds (RRB). It discusses what they are, how interest and maturity values are calculated and how they are taxed. The unique characteristics of these bonds and how they are taxed may create a prepayment of tax which may make them more suitable to holding in registered accounts, such as registered retirement savings plans (RRSPs) or tax-free savings accounts (TFSA). In addition, the tax reporting and record keeping for RRBs can be complex further adding merit to holding an RRB in a registered account.

What are RRBs?

RRBs are issued primarily by the Government of Canada (some provinces may also issue RRBs). Unlike regular bonds, RRBs attempt to maintain your purchasing power while inflation is positive. If inflation is negative, it's possible to lose some capital and your coupon interest payments may be reduced.

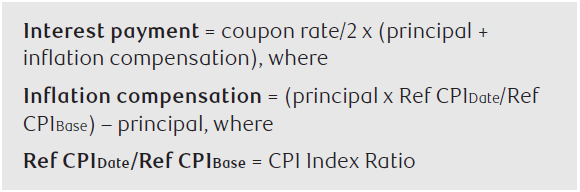

RRBs pay coupon interest semi-annually based on a fixed coupon interest rate multiplied by an inflation-adjusted principal. And at maturity, you receive the principal that is adjusted for inflation. The inflation adjustment to the principal is based on changes in the Consumer Price Index (CPI) compared to the CPI on the date the particular RRB series was first issued. The adjustment for inflation is referred to as the "inflation compensation". For this purpose, the CPI is the all-items CPI for Canada, not seasonally adjusted, which is published monthly by Statistics Canada. Inflation compensation is based on cumulative changes in the CPI since the original issue date of the specific bond.

It may be possible to buy and sell RRBs prior to maturity on a secondary market, although this market may be limited. In addition, the Government of Canada may reopen a particular series of RRBs several times. For example, the 4.25% RRBs due December 1, 2021 has been reopened ten times since the original issue date of December 1, 1991. The price you buy or sell at on the secondary market or that the RRBs are issued for on a reopening will include the market price plus accrued interest.

Calculation of RRB interest

The Government of Canada issues an RRB series with a specified coupon interest rate, maturity date and original issue date. At the original issue date, a base value of the CPI is associated with the bond, known as the "Reference CPI Base" (Ref CPIbase). The Ref CPIbase remains constant throughout the term of the bonds other than when the Official Time Base (as defined by Statistics Canada) is changed. Whenever the Official Time Base is changed, the Government of Canada will publish the conversion factor used to rebase the CPI series to the new Official Time Base. As an example, the 4% RRBs due December 1, 2031 had an original Ref CPIBase of 108.74516 which was changed in June 2007 to 91.38249. Therefore, all calculations related to the 4% RRBs due December 1, 2031 will use a Ref CPIBase after June 17, 2007 of 91.38249. Any calculations before June 17, 2007 would have used 108.74516.

When a new issue of an existing RRB series is reopened, the original Ref CPIBase for the series, or the revised Ref CPIBase, if applicable, will be associated with this new issue as well. The inflation-adjusted principal and coupon interest payments are determined in relation to the Ref CPIBase. At each coupon interest payment date the Reference CPI (Ref CPI) on this date is compared to the Ref CPIBase to determine the adjustment to the bond's principal in calculating the interest to be paid.

Example:

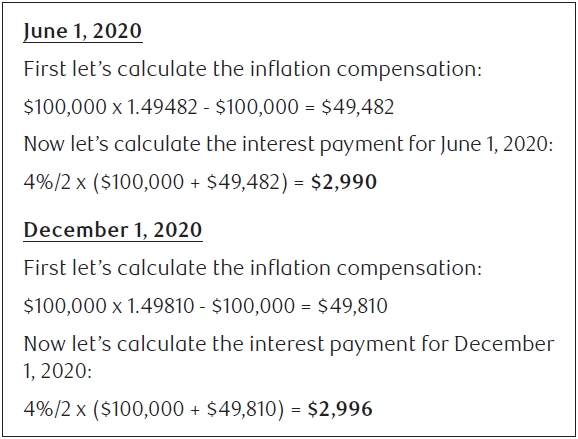

You have an RRB with a 4% coupon rate and a maturity date of December 1, 2031. Interest is paid semi-annually on June 1 and December 1. For these bonds, the principal is $100,000 (each bond is issued at $1,000). What is the interest paid on the bonds for the calendar year ended December 31, 2020?

The semi-annual interest payments are calculated as follows:

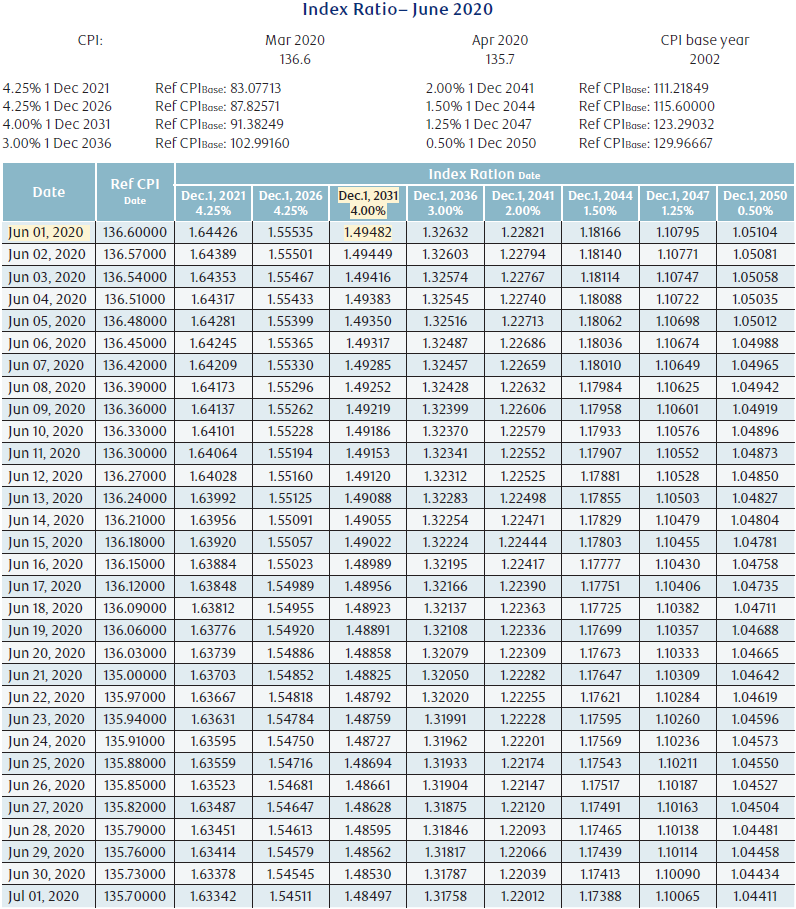

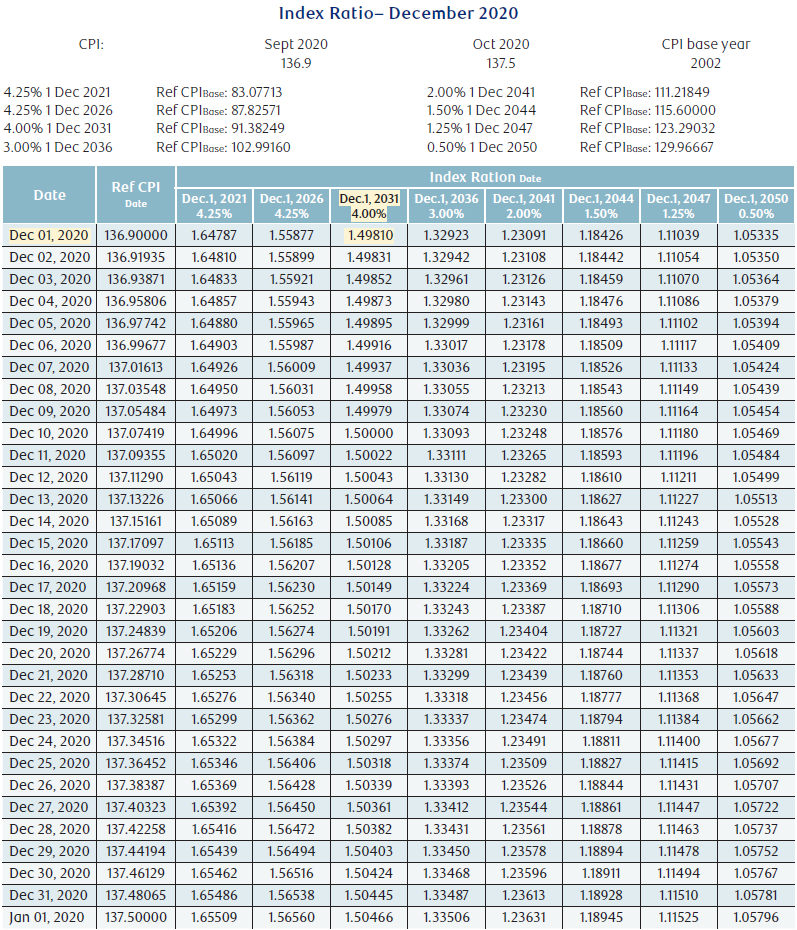

The CPI Index Ratio for June 1, 2020 and for December 1, 2020 can be found on the Bank of Canada (BoC) website under "Real Return Bonds – Index Ratio". The CPI Index Ratio for June 1, 2020 and December 1, 2020 is 1.49482 and 1.49810, respectively. See Appendix A for the CPI Index Ratio schedule for June 2020 and December 2020.

So, the total coupon interest payments received in 2020 is $5,986

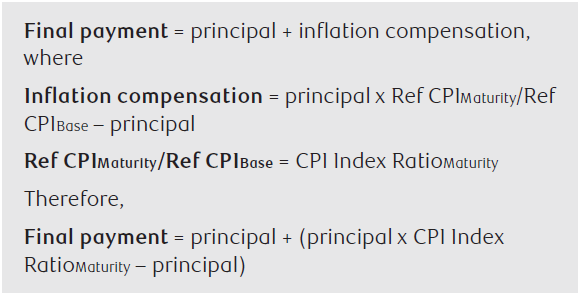

Calculation of final payment at maturity

At maturity you will receive, in addition to a coupon interest payment, a final payment equal to the sum of the principal amount and the inflation compensation accrued from the original issue date. Here's how the final payment at maturity is calculated:

Since in our example the bond matures in the future, we will need to make an assumption so that we can illustrate the calculation of the final payment at maturity. We will assume that the CPI Index Ratio at maturity on December 1, 2031 will be 1.50000.

Therefore, based on our assumption that the CPI Index Ratio at maturity will be 1.50000, the final payment is $150,000.

Taxation of RRBs

Taxation of coupon interest

You will be required to include in income any coupon interest you receive or that becomes receivable in the taxation year, depending upon the method of tax reporting you regularly follow. RRBS interest is taxed as ordinary income at your marginal tax rate. The calculation of the coupon interest payment received in 2020 was illustrated in the section on, "Calculation of RRBS interest". The coupon interest paid in a calendar year is reported to you on a T5, Statement of Investment Income.

The amount of coupon interest reported is the interest which has accrued since the immediately preceding coupon payment date for the particular series of RRBS; however, to the extent that coupon interest accrued prior to the date of issuance of the bonds, a deduction will be available to you. Any amount which is deductible reduces the adjusted cost base (ACB) of the bond.

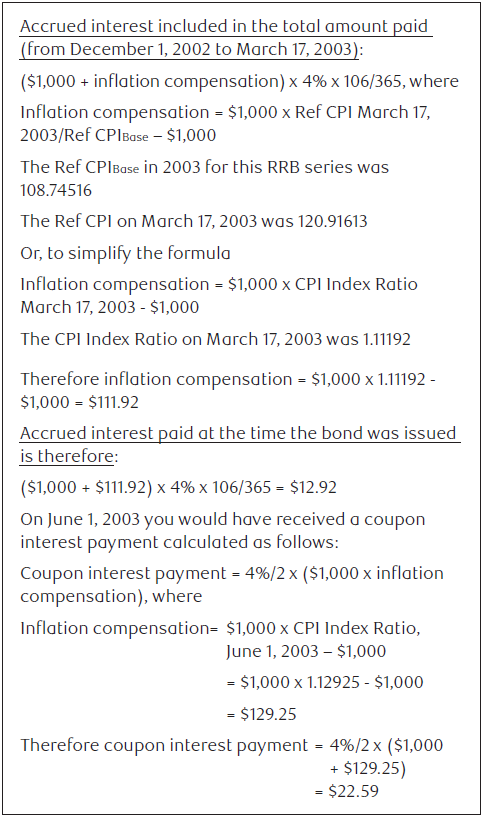

To illustrate this concept, let's look at the Government of Canada 4% RRBS due December 1, 2031. The first issue date of the 4% RRBS due December 1, 2031 was March 8, 1999. After this date the Government of Canada reopened this issue seventeen times from March 1999 to March 2003. The last reopening was March 17, 2003 at a price of 124.267 plus accrued interest from December 1, 2002. So you would have paid $1,242.67 plus accrued interest for a $1,000 bond. Although the bond you purchased was never issued before, you would have to pay, in addition to the purchase price, accrued interest from December 1, 2002 (the last interest payment date for this RRBS series) to March 17, 2003. The total amount you would have paid for this bond would be made up of the price of the bond, which includes inflation compensation, plus accrued interest. Inflation compensation accrues from the original issue date of March 8, 1999. Interest accrues from the last interest payment date. In this example, on June 1, 2003, you would have received the full amount of coupon interest on your $1,000 bond.

Although you would have had to include $22.59 as interest income on your 2003 income tax return for the June 2003 coupon interest payment, you could have claimed a deduction for the $12.92 of interest that accrued before the bond issue date that you paid when you purchased the bond. The ACB of your bond should not include the $12.92 of accrued interest.

Any time an RRBS is purchased on a secondary market between coupon interest payment dates, the same analysis and calculations of accrued interest will apply.

Taxation of inflation compensation

While the market value of an RRBS does increase to reflect the inflation compensation on your principal amount, cash is not received until the RRBS matures or is sold. However, you are required to include in income, for each taxation year you hold the bond, the amount by which inflation compensation has increased for any inflation adjustment period that ends in the taxation year. This amount is also reported as interest on your T5, and must be included in your income. The amount of any increase required to be included in your income increases the ACB of the RRB.

If instead, accrued inflation compensation has decreased for any inflation adjustment period that ends in a taxation year, you can deduct this amount in computing your income for the year. This is reported in your tax reporting package as "paid by you". The amount of any decrease permitted to be deducted in computing your income reduces the ACB of the RRB.

The first inflation adjustment period for a series of bonds acquired in an offering by the Government of Canada will be the period starting on the date of issuance of the bonds. Where you purchased the RRB on the secondary market, your first inflation adjustment period will start on the date of purchase. Each subsequent inflation adjustment period will start on a coupon payment date for the series. An inflation adjustment period will end on the earlier of the next coupon payment date for the series and the date of disposition of the bond.

Continuing with our example of the 4% RRB due December 1, 2031:

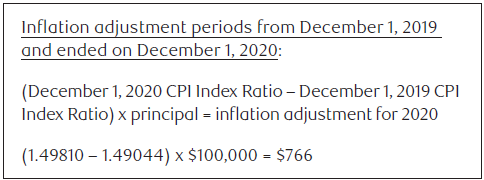

If you owned the bond before December 1, 2019, there are two inflation adjustment periods that end in the 2020 taxation year; one that begins on December 1, 2019 and ends on June 1, 2020 and one that begins on June 1, 2020 and ends on December 1, 2020. The inflation compensation required to be reported for the 2020 year would be calculated as follows:

Therefore, the total inflation adjustment that accrued in the 2020 taxation year is $766. In addition to the coupon interest payments received in 2020 of $5,986, you would also have to include the inflation adjustment of $766 in income as interest even though you will not receive it until maturity.

The inflation adjustment of $766 should be added to the ACB of your RRBs.

Purchased or sold between coupon interest payment dates

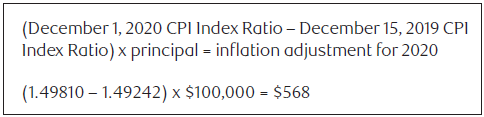

If you purchase RRBs between coupon interest payment dates, the calculation of the inflation adjustment must reflect this. So continuing with our example using the 4% December 1, 2031 RRBs, let's assume that you purchased these bonds on a secondary market on December 15, 2019. Your first inflation adjustment period starts on December 15, 2019. Since there are no inflation adjustment periods that end in 2019, there would be no inflation compensation adjustment for 2019. The calculation of the inflation adjustment for the period up to December 1, 2020 is as follows:

A similar calculation is required if an RRB is sold between coupon interest payment dates. For example, if you sell your 4% December 1, 2031 RRBs on December 21, 2020, the inflation adjustment must be calculated to December 21, 2020 and be included in your income as interest. This amount should be added to your ACB, so that the correct capital gain or loss on the sale of your RRBs can be calculated. Assuming you owned the bond before December 1, 2019, in addition to the inflation adjustment from December 1, 2019 up to December 1, 2020, the calculation of the inflation adjustment to December 21, 2020 would be:

So the total interest related to the inflation compensation in 2020 up to December 21, 2020 would be $1,189 ($766 + $423). This should be added to your ACB in determining your capital gain or loss on the sale of the bond.

Taxation on disposition

On the disposition or a deemed disposition of an RRB, you may realize a capital gain or capital loss. If the total amount received, less the portion that represents accrued interest from the last coupon interest payment date to the date of disposition, is greater than your ACB then you will have a gain. The tax treatment of changes in the inflation compensation for inflation adjustment periods ending in the taxation year of disposition is described above under the heading "Taxation of inflation compensation".

Any accrued coupon interest to the date of disposition must also be included in your income. To the extent that the amount received on the disposition of an RRB in respect of the coupon interest is less than the accrued coupon interest on the bond, you may be entitled to a deduction.

Taxation if held to maturity

At maturity, you will receive the coupon interest up to the date of maturity and the principal plus or minus the inflation compensation from the original issue date of the RRB series. Although this was previously discussed in the section, "Calculation of final payment at maturity", here is the formula again:

Any coupon interest to the date of maturity must be included in your income. In addition, the inflation compensation adjustment from the last coupon date to the date of maturity must also be included in your income as interest. This amount is then added to your ACB. The tax treatment of changes in the inflation compensation for inflation adjustment periods ending in the taxation year of disposition is described above in the section "Taxation of inflation compensation".

If you did not purchase your bond at the original issue date of the RRB series, you may realize a capital gain or capital loss at maturity. The final payment (not including the coupon interest paid at maturity) less your ACB is equal to your capital gain or loss.

Summary

If you own an RRB, you likely bought it because you hope to be protected from the effects of inflation and you like the relative safety of bonds. Keep in mind that RRBs are subject to risks similar to regular bonds including interest rate risk, re-investment risk and market risk.

Even if you like the investment features of an RRB, you have to be aware that you do not receive the inflation adjusted principal until maturity or sale even though you are paying the taxes annually on the inflation adjustments. Due to this tax disadvantage, it may be best to hold RRBs in registered accounts. In addition, the record keeping for RRBs is complex. You should track the changes in the inflation compensation and the effect on your ACB every year. These calculation and bookkeeping complexities may merit holding an RRB in a registered account.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

Appendix A – CPI Index Ratios for June and December 2020