Registered disability savings plan (RDSP)

The RDSP is designed to assist an individual with a disability in saving for their long-term financial needs. It offers tax deferral on investment growth, access to generous government grants and bonds, and an opportunity for family members to assist with the contributions. This article explains some of the intricacies of RDSPs, including who can be the holder and how the government assistance works, as well as the rules around withdrawals from an RDSP.

The RDSP is designed to assist an individual with a disability in saving for their long-term financial needs. It offers tax deferral on investment growth, access to generous government grants and bonds, and an opportunity for family members to assist with the contributions. This article explains some of the intricacies of RDSPs, including who can be the holder and how the government assistance works, as well as the rules around withdrawals from an RDSP.

Family Office Services

October 14, 2025

Registered Disability Savings Plan (RDSP)

The RDSP is designed to assist an individual with a disability in saving for their long-term financial needs. It offers tax deferral on investment growth, access to generous government grants and bonds, and an opportunity for family members to assist with the contributions. This article explains some of the intricacies of RDSPs, including who can be the holder and how the government assistance works, as well as the rules around withdrawals from an RDSP.

What is an RDSP?

The RDSP is a long-term disability savings plan that's intended to help individuals with severe and prolonged disabilities save for their future. It's a trust arrangement between an individual (the holder of the RDSP) and the RDSP issuer for the benefit of an individual with a disability. The plan is registered with the Canada Revenue Agency (CRA).

The holder makes or authorizes contributions to an RDSP. These contributions may attract government grants and bonds. The accumulated funds can be invested on a tax-deferred basis and are only taxable when withdrawn from the RDSP. All funds withdrawn from the RDSP are to be used solely for the beneficiary.

Opening an RDSP

To open an RDSP, you need both a beneficiary and a holder.

The Beneficiary

The beneficiary is the person who's entitled to the funds in the RDSP. An individual can be the beneficiary of only one RDSP and there can be only one beneficiary per RDSP. To open an RDSP, the beneficiary must meet all of the following criteria:

- Be under 60 years of age (if the beneficiary is 59, the RDSP must be opened before the end of the calendar year in which the beneficiary turns 59).

- Be a Canadian resident at the time the plan is opened.

- Have a valid Social Insurance Number (SIN).

- Be eligible for the disability tax credit (DTC).

To qualify for the DTC, a person must have a severe and prolonged impairment in physical or mental functions that is certified by a medical practitioner on Form T2201, Disability Tax Credit Certificate. The form must be approved by the CRA. A copy of the form, as well as other information on the DTC, is available on the CRA website.

The Holder

There must be at least one holder of an RDSP at all times. The holder manages the RDSP, which includes opening the plan, making or approving contributions to the plan, and authorizing withdrawals from the plan. The holder can be the beneficiary. However, if the beneficiary is unwilling or unable to be the holder, someone else may be the holder in the following circumstances:

• For beneficiaries who are under the age of majority in their province or territory of residence, a qualifying person can be the holder and open an RDSP for the beneficiary. A qualifying person can be a legal parent or a person, public department, agency or institution legally authorized to act for the beneficiary.

• Once the beneficiary reaches the age of majority, they can become the holder of the RDSP, provided they are competent.

• If the previous holder was a legal parent, the legal parent has the option to remain as the holder. The adult beneficiary can be added as a joint holder, along with their parent, if the RDSP issuer allows for joint holders. If the parent wishes change to ownership of the plan, they may choose to assign ownership of the plan to the adult beneficiary.

• If the previous holder was someone other than the legal parent, that person or body must be removed as the holder of the plan.

• For beneficiaries who've attained the age of majority but are not legally competent to enter into a contract, the holder may be a qualifying person who is a person legally authorized to act for the beneficiary.

• For beneficiaries who've attained the age of majority, but in the opinion of the RDSP issuer, the individual's contractual competency to enter into a plan is in doubt, a qualifying family member (QFM) can be a holder. A QFM includes the beneficiary's spouse, common-law partner, adult sibling or parent. A QFM can open an RDSP for a beneficiary as the holder until December 31, 2026. A QFM who becomes a plan holder before the end of 2026 can remain as the plan holder after 2026.

Provided the holder is not the beneficiary of the plan, they don't have to be a Canadian resident but will need to have a valid SIN or business number.

Replacing a Holder

If the current holder ceases to be an eligible holder, they must be replaced by someone who's eligible. Examples of when the holder can cease to be eligible would be in the case of death or loss of mental capacity. If the beneficiary doesn't have mental capacity to become the holder, the person legally authorized to act for the beneficiary will need to become the holder of the RDSP.

If a QFM is a holder of an RDSP, the QFM should be replaced in the following circumstances:

• If the beneficiary is determined to be contractually competent or, in the issuer's opinion, the beneficiary's contractual competence to enter into a RDSP is no longer in doubt. In this case, if the beneficiary notifies the issuer that they choose to become the holder of the plan, the beneficiary should replace the QFM as the holder.

• If a qualifying person (such as a person, public department, agency or institution) becomes legally authorized to act for the beneficiary. In this case, the qualifying person must notify the issuer of the appointment and replace the QFM as the holder.

When thinking about estate planning for incapacitated and minor beneficiaries, it's always important to consider who can become the new holder of the RDSP in the event the current holder passes away or is unable to continue being the holder.

Contributing to an RDSP

Contributions to the RDSP can only be made while the beneficiary is a Canadian resident and qualifies for the DTC. Contributions can be made until the end of the year in which the beneficiary turns age 59. RDSPs don't have an annual contribution limit, but there is a lifetime contribution limit of $200,000.

Annual contributions made to the RDSP may attract government grants, known as the Canada Disability Savings Grant (CDSG). In addition, the plan may be eligible to receive bonds, known as the Canada Disability Savings Bond (CDSB), even if no contributions are made. To be eligible for the CDSG, contributions must be made by the end of the calendar year in which the beneficiary turns age 49. If the beneficiary qualifies, the CDSB is also only paid to the plan until the end of the year in which the beneficiary turns age 49. This deadline is intended to encourage long-term savings and ensure that all grants and bonds remain in the RDSP for at least 10 years before the beneficiary turns 60. Both types of government assistance are discussed in further detail in the next section.

Any person can contribute to an RDSP. But, if the contributor is not the holder of the RDSP, they will need the holder's written consent to contribute. Requiring the holder's consent ensures the holder to manage contributions into the plan strategically in order to attract maximum grants and bonds and keep within the lifetime contribution limit.

Contributions are not tax-deductible when deposited into an RDSP, but they are also not taxable when withdrawn from the RDSP.

Government Matching Grants and Bonds

The CDSG (grant) and the CDSB (bond) are paid by the government directly into the plan and can significantly increase accumulations over time. The amount of grant and bond received depends on "adjusted net family income."

From the year the beneficiary is born until the end of the year the beneficiary turns age 18, the adjusted net family income is the income of the beneficiary's parent(s) or legal guardian(s). From the year the beneficiary turns age 19 until the RDSP is closed, the adjusted net family income is the beneficiary's income plus their spouse's or common-law partner's income.

To calculate adjusted net family income, you would start with net income (on line 2360 of the applicable individual's tax return) and adjust it to exclude certain payments received, such as payments from an RDSP. The adjustments are intended to ensure that individuals or families with low or modest income can receive the most benefits possible.

Adjusted net family income for determining eligibility for CDSG and CDSB for a particular year is based on the second previous tax year. For example, eligibility for CDSG and CDSB for 2023 is based on 2022 family income reported on your tax return. This is why it's important to file tax returns if you have an RDSP and want to qualify for the bond or to earn grants.

The CDSG

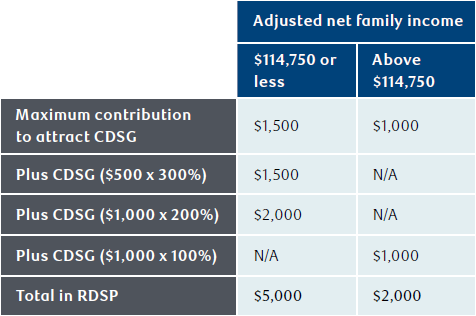

The government will pay matching grants of 100%, 200% or 300% of contributions made to the RDSP, up to an annual maximum of $3,500, and a lifetime limit of $70,000. The amount contributed, as well as the adjusted net family income, determine the amount of grant that's paid into the plan.

Where adjusted net family income is $114,750 or less (2023 threshold, indexed annually to inflation), the CDSG is 300% on the first $500 of contributions plus 200% on the next $1,000. Where family income is above $114,750, the CDSG is 100% on the first $1,000 contributed (matching dollar for dollar).

The following chart illustrates the amount of contributions necessary, depending on your adjusted net family income, to attract the maximum CDSG for a year:

If you make an RDSP contribution of less than the amount required to attract the maximum CDSG for the year, you can carry forward the remaining CDSG amount, which is referred to as "unused grant entitlements." Claiming unused grant entitlements is discussed in a later section.

On the other hand, since there's no annual contribution limit for RDSPs, it is possible to contribute the lifetime maximum of $200,000 up front. The main benefit of doing so would be the ability to have the investments grow on a tax-deferred basis within the RDSP. The drawback is that you'll forfeit the ability to receive future CDSG, which may otherwise be available if you made regular annual contributions. In deciding which option may be best, consider the following:

- The ability to make a larger up-front contribution.

- The age and health of the beneficiary, as that will generally dictate the time horizon for tax-deferred growth as well as the timing of future withdrawals.

- The marginal tax rate on non-registered investment income that would otherwise be earned in the RDSP.

- The expected rate of return on investment income (both inside and outside the RDSP).

- The beneficiary's expected marginal tax rate when the funds are withdrawn.

The CDSB is paid to low-income individuals or families, regardless of whether contributions are made to an RDSP. Once the plan has been opened, the government will pay bonds of up to $1,000 annually, to a lifetime maximum of $20,000. The adjusted net family income determines the amount of bond that's paid.

Where adjusted net family income is $37,487 or less (2025 threshold), the maximum annual CDSB of $1,000 is paid. Where adjusted net family income is above this threshold, the CDSB is gradually phased out, reaching zero if adjusted net family income is more than $57,375 (2025 threshold). These thresholds are adjusted annually for inflation.

Claiming Unused Grant and Bond Entitlements

Qualifying RDSP beneficiaries are entitled to claim previously unused CDSG and CDSB from the past 10 years, starting from 2008 (the year RDSPs became available). To qualify for past grant and bond entitlements, you must meet all of the following criteria:

• Be qualified for the DTC in each year of entitlement.

• Be a Canadian resident when the contribution is made and for each year of entitlement.

• Have a valid SIN.

• Be age 49 or under at the end of the calendar year when the contribution is made.

• Not have used up your $200,000 lifetime contribution limit.

The amount of the unused grant and bond that can be paid into the plan will be calculated automatically based on the beneficiary's adjusted net family income for those past years. The matching rate on unused grant entitlements is the same as what would have applied if the contribution had been made in the calendar year in which the entitlement was earned. Grants are paid on contributions that use up any grant entitlements at the highest available matching rate first from oldest to newest, followed by any grant entitlements at lower rates.

The maximum annual amount of unused entitlements that can paid out in a calendar year is $10,500 for grants and $11,000 for bonds. These amounts include any grant or bond entitlement paid for the current year.

Creditor Protection

The federal Bankruptcy and Insolvency Act provides creditor protection for assets held in RDSPs in the event of bankruptcy. This protection applies for all provinces and territories of Canada. There's no cap on the amount of assets that are protected, with the exception of any RDSP contributions made in the 12 months before the date of bankruptcy.

Withdrawing from an RDSP

Generally, to make a withdrawal from the RDSP, the holder's consent is required. There is an exception when the private contributions made to the RDSP are less than the amount of grants and bonds in the RDSP, and the beneficiary is aged 28 to 58 (inclusive) during the calendar year. In this case, the holder's consent is not needed for withdrawals, up to a specified maximum. This exception is especially important for an adult beneficiary with an RDSP that was opened by, for example, their parent, while they were a minor. It allows the adult beneficiary to request and receive some assistance from the plan, even if their parent, as the holder of the plan, refuses to allow a payment.

There are two types of payments a beneficiary can receive from an RDSP:

Disability Assistance Payments (DAPs): These are lump-sum or unscheduled single payments to the beneficiary or their estate after death. Some RDSP issuers may not allow DAPs; as such, it's important to check if your RDSP issuer allows DAPs before opening an RDSP. If DAPs are allowed, the holder can request a DAP at any time. Receiving a DAP before age 60 may trigger a proportional repayment of grants and bonds to the government, as described later in this article.

Lifetime Disability Assistance Payments (LDAPs): These are regularly scheduled periodic payments to the beneficiary. Once they begin, they continue at least annually until the plan is terminated or the beneficiary passes away. LDAPs must begin by the end of the year the beneficiary turns age 60, but the holder may request for them to begin at an earlier time. Receiving an LDAP before age 60 may trigger a proportional repayment of grants and bonds to the government, as described later in this article.

Money withdrawn from the RDSP can be used for any purpose.

Taxation of Withdrawals

A DAP or an LDAP may consist of contributions, grants, bonds, payments from designated provincial programs, proceeds from rollovers and income earned in the RDSP. As such, a portion of a DAP or an LDAP may be nontaxable and a portion may be taxable. The non-taxable portion is made up of contributions made to the RDSP. The taxable portion includes grants, bonds, investment earnings, payments from designated provincial programs, and proceeds from the rollover of a retirement savings plan or an education savings plan. The taxable portion of the RDSP withdrawal is included in the beneficiary's income in the year the payment is made.

Income tax is withheld on the taxable portion of RDSP payments that exceeds the sum of the beneficiary's basic personal amount and the DTC amount. These tax credit amounts are both indexed annually.

There are complicated steps involved in calculating the taxable and non-taxable portion of a DAP or an LDAP and are beyond the scope of this article.

Repayments of Grants and Bonds

Since the RDSP is intended to promote long-term savings, there are specific rules designed to discourage early withdrawals from an RDSP. In most cases, an early withdrawal from an RDSP will trigger a repayment of the "assistance holdback amount" (AHA). The AHA is the total of all grants and bonds that were paid into the RDSP within the past 10 years (less any grants and bonds that were already repaid to the government during that period).

To ensure there are sufficient funds in the RDSP to meet any potential repayment obligations, RDSP issuers must set aside an amount equal to the AHA. As such, a payment can't be made from an RDSP if the fair market value (FMV) of the plan, after the payment, will be less than the AHA.

Proportional Repayments

As mentioned earlier, receiving a DAP or an LDAP before the year the beneficiary turns age 60 may trigger the proportional repayment rules. Under these rules, for every $1 withdrawal, $3 of any grants or bonds that were paid into the plan in the 10 years preceding the withdrawal will have to be repaid, up to a maximum of the AHA. The grants and bonds are repaid to the government in the order they were paid into the RDSP, from oldest to newest.

Requesting a DAP or starting LDAPs in the year the beneficiary turns 60 will not trigger a repayment, as grants and bonds stop being paid into the plan by the end of the calendar year in which the beneficiary turns age 49.

Full Repayments

The following events will trigger a full repayment of the AHA:

- The RDSP is closed.

- The RDSP is no longer compliant.

- The beneficiary passes away.

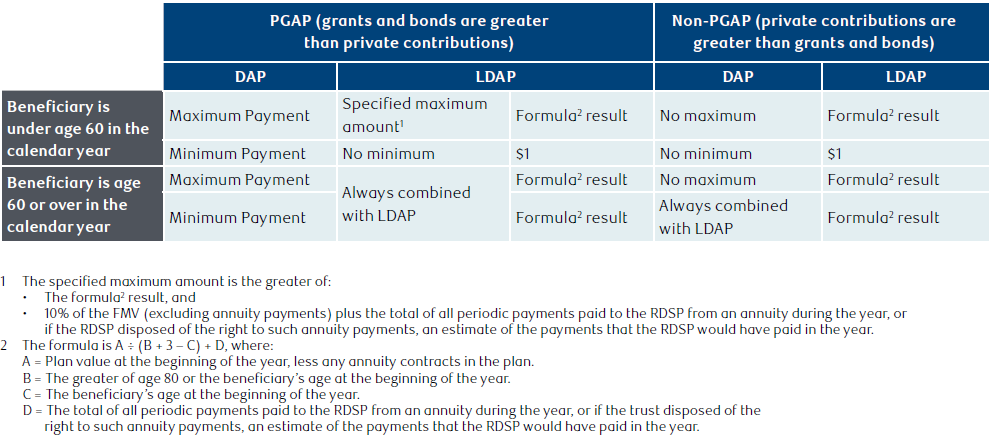

Withdrawal Limits

DAP or LDAP limits are calculated depending on the proportion of private contributions to government assistance (grants and bonds) held in the RDSP. When an RDSP contains more government assistance than private contributions, it's considered a Primarily Government Assisted Plan (PGAP). When the amount of private contributions is greater than the amount of government assistance, the RDSP is considered a non-PGAP.

If you withdraw money from a PGAP, there are limitations on how much you can withdraw, whereas if you withdraw from a non-PGAP, there are fewer limitations. The following chart outlines the annual minimum and maximum withdrawal limitations:

Shortened Life Expectancy

Where a beneficiary of an RDSP has a life expectancy of five years or less (as certified, in writing, by a medical doctor or nurse practitioner), the holder has two options that offer greater flexibility in withdrawing money from the RDSP. The holder can either choose to keep the plan as an RDSP or make an election, in prescribed form, to designate the plan as a specified disability savings plan (SDSP).

If the holder chooses to keep the plan as an RDSP, there's no annual payment limit. The holder could request DAPs and start LDAPs, withdraw the funds in the RDSP over the next five years, or even withdraw all funds in one lump sum. That said, with this option, the full AHA or a portion of the AHA may need to be repaid.

Alternatively, designating the RDSP as an SDSP allows the holder to withdraw assets without repaying any of the AHA. When the plan is designated as an SDSP, payments from the plan must start by December 31 of the following calendar year. The holder could request a DAP or start LDAPs or withdraw up to $10,000 of a taxable amount. On occasion, the formula for the DAP or LDAP results in a taxable amount greater than $10,000. In this case, the limit does not apply.

Although designating the plan as an SDSP provides greater withdrawal flexibility, once the plan becomes an SDSP, contributions to the plan are no longer permitted and no further grants or bonds will be paid into the plan. Furthermore, beneficiaries will not be able to carry forward any grant and bond entitlements for the years the plan is an SDSP (except for the calendar year in which the election is made).

This article discusses rollovers of retirement and education plans to an RDSP in a later section, but for the purpose of SDSPs, only rollovers of retirement savings proceeds to an SDSP are permitted. A rollover of an education savings plan to an SDSP is not allowed.

In the event the beneficiary's health improves, the holder can request, in writing, that the SDSP designation be removed and then the plan becomes an RDSP again. If the beneficiary survives for more than five years, the plan is unaffected and remains an SDSP until the holder requests the designation be removed or one of the SDSP conditions is no longer met.

In the event of the beneficiary's death, any grant or bond paid into the plan over the 10 years preceding the time of death will have to be repaid to the government.

RDSP Withdrawals and Income-Tested Benefits

Payments from an RDSP do not affect eligibility for federal government benefits such as the old age security, the guaranteed income supplement, the Canada child benefit, and the goods and services tax/harmonized sales tax credit. Although it's not the case for most provinces and territories, RDSP payments may affect eligibility for some provincial or territorial disability benefits or other disability benefits that are means-tested. Please consult the specific benefit provider for further information if you're considering opening an RDSP.

Transfers Between Institutions

If all holders agree, a transfer from one institution to another can be made from a beneficiary's current RDSP to a new RDSP for the same beneficiary. The transfer must be done directly for the full amount of the funds in the plan. Financial institutions that offer RDSPs will provide the necessary forms to transfer the plan.

Becoming a Non-Resident

If the beneficiary of an RDSP becomes a non-resident, contributions to the plan must stop. Contributions can begin again if the beneficiary regains Canadian residency. If a contribution is made to the RDSP while the beneficiary is a non-resident, the plan will be non-compliant. In this case, a DAP is deemed to have been paid to the beneficiary equal to the amount in the RDSP less any AHA. As such, it's important that no contributions are made to an RDSP while the beneficiary is a non-resident of Canada.

Losing DTC Eligibility

The condition of an individual with a disability may improve. This may result in a beneficiary losing their eligibility for the DTC.

Effective January 1, 2021, an RDSP does not need to be closed if the beneficiary becomes DTC-ineligible. The plan is permitted to remain open and there's no requirement to provide medical certification that the beneficiary is likely to become eligible for the DTC in the future.

For any period during which the beneficiary is ineligible for the DTC, commencing with the first full calendar year throughout which the beneficiary is no longer eligible for the DTC, the following rules apply:

• No contributions to the RDSP are permitted.

• The beneficiary is not eligible to receive grants or bonds, and no new entitlements accrue in respect of any year throughout which the beneficiary is ineligible for the DTC.

• A rollover of registered education savings plan (RESP) investment income is not permitted.

• A rollover of proceeds from a deceased individual's registered retirement savings plan (RRSP) or registered retirement income fund (RRIF) to the RDSP of a financially dependent infirm child or grandchild is permitted only if the rollover occurs by the end of the fourth calendar year following the first full calendar year throughout which the beneficiary is ineligible for the DTC.

• Withdrawals from the RDSP are permitted. Withdrawals will be subject to the proportional repayment rule and the AHA will be modified, depending on the beneficiary's age. These modifications are beyond the scope of this article.

If a beneficiary regains eligibility for the DTC, the regular RDSP rules will apply, beginning with the year in which the beneficiary becomes eligible for the DTC again. For example, contributions to the RDSP will be permitted and new grants and bonds may be paid into the RDSP.

Closing an RDSP

When an RDSP is closed, the beneficiary or the beneficiary's estate receives the invested contributions and all earnings from the RDSP. However, all grants and bonds that have been paid into the RDSP during the 10 years preceding the closure must be repaid to the government. The RDSP must be closed in the following situations:

The Beneficiary's Death

When a beneficiary passes away, the holder must close the RDSP by December 31 of the year following the calendar year of the beneficiary's death. Any grants or bonds that were paid into the RDSP in the 10 years preceding the beneficiary's death must be repaid to the government. Any funds remaining in the RDSP will be paid to the beneficiary's estate and may be subject to probate taxes.

Upon the Holder's Request

At the holder's request, an RDSP can be closed if there's no property left in the RDSP or if only the AHA is left (i.e. no earnings or contributions).

At any time during which the beneficiary is ineligible for the DTC, the holder may request the RDSP be closed. The general rules in the event of an RDSP closure will apply, with the exception that the amount required to be repaid upon closure will be equal to the AHA at that time, modified depending on the beneficiary's age.

Rollovers

Rollovers of Retirement Savings Plans to an RDSP

A parent or grandparent of a financially dependent child or grandchild can transfer some or all of their retirement savings on a tax-deferred basis to their child's or grandchild's RDSP when they pass away. The retirement savings plan must be one of the following:

• A registered retirement savings plan (RRSP).

• A registered retirement income fund (RRIF).

• A registered pension plan (RPP).

• A pooled retirement pension plan (PRPP).

• A specified pension plan (SPP).

To be eligible for the rollover, the RDSP beneficiary must be alive at the time of the transfer, a resident of Canada, and age 59 or younger at the end of the calendar year in which the transfer takes place. In addition, the RDSP holder must give permission for the rollover to occur. Lastly, the beneficiary of the RDSP must have been entitled to receive the retirement savings amount either because they were designated as a beneficiary on the plan or entitled to some or all of the retirement savings proceeds by virtue of being a beneficiary of the estate.

The rollover of retirement proceeds will be considered a private contribution. There are no tax implications when the proceeds are rolled over into the RDSP, although the rollover will not attract grants. The amount of the rollover counts towards the $200,000 RDSP lifetime contribution limit. For example, if the holder had already contributed $60,000 to the RDSP, the amount rolled over from the retirement plan can't exceed $140,000.

If the beneficiary of the RDSP is not eligible for the DTC, it's still possible to roll over the proceeds from a deceased individual's registered savings plan to the RDSP if the rollover occurs by the end of the fourth calendar year following the first full calendar year throughout which the beneficiary is ineligible for the DTC.

Rollovers of an RESP to an RDSP

If the beneficiary of an RDSP is also the beneficiary of an RESP, it is possible to roll over an accumulated income payment (AIP) on a tax-deferred basis from the RESP to the RDSP. The AIP consists of investment income earned in the RESP and excludes any government assistance such as grants and bonds.

The subscriber of the RESP and the holder of the RDSP must jointly elect, in writing, for the rollover to take place. To be eligible for the rollover, the RDSP beneficiary must be eligible for the DTC at the time of the transfer, a resident of Canada, and age 59 or younger by the end of the calendar year in which the transfer takes place. In addition, one of the following conditions must be met:

• The beneficiary is, or will be, unable to pursue post-secondary education because of a severe and prolonged mental impairment.

• The RESP has existed for more than 35 years.

• The RESP has existed for at least 10 years and each beneficiary of the plan is at least age 21 and is not pursuing post-secondary education.

When the RESP rollover occurs, original contributions made into the RESP are returned to the subscriber on a tax-free basis, the original contributions will be applied to the government, and the RESP must be closed by the end of February of the year after the rollover year.

The rollover of RESP proceeds will be considered a private contribution. There are no tax implications when the proceeds are rolled over into the RDSP, although the rollover will not attract grants. The amount of the rollover counts towards the RDSP lifetime contribution limit.

Conclusion

The RDSP is designed to assist persons with disabilities in saving for their long-term financial needs. If you qualify for the disability tax credit or you're supporting a family member who qualifies, speak with a qualified tax advisor to determine if setting up an RDSP may make sense in your circumstances.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.