Registered retirement savings plan (RRSP)

Your RRSP will likely represent a key source of your retirement income. The savings you accumulate in your RRSP over the years can be converted to an income source once you retire. A thorough understanding of these rules and strategies, accompanied by effective management of your RRSP assets, may help you accumulate savings for your retirement. This article reviews the basics of RRSPs and provides an outline of potential strategies that may help you maximize your RRSP savings.

Your RRSP will likely represent a key source of your retirement income. The savings you accumulate in your RRSP over the years can be converted to an income source once you retire. A thorough understanding of these rules and strategies, accompanied by effective management of your RRSP assets, may help you accumulate savings for your retirement. This article reviews the basics of RRSPs and provides an outline of potential strategies that may help you maximize your RRSP savings.

Family Office Services

October 14, 2025

Registered retirement savings plan (RRSP)

Your RRSP will likely represent a key source of your retirement income. The savings you accumulate in your RRSP over the years can be converted to an income source once you retire. A thorough understanding of these rules and strategies, accompanied by effective management of your RRSP assets, may help you accumulate savings for your retirement. This article reviews the basics of RRSPs and provides an outline of potential strategies that may help you maximize your RRSP savings. Any reference to a spouse in this article also includes a common-law partner.

What is an RRSP?

An RRSP is a tax-sheltered investment vehicle that may help you save for retirement. Contributions to an RRSP may be tax deductible. This means you can claim the contributions as a deduction on your income tax return and reduce your taxable income in the year you claim the deduction. As well, income and capital gains earned in the plan compound on a tax-deferred basis and are taxable when you withdraw funds from the plan.

You may contribute to an RRSP up until the end of the year in which you turn age 71. If you have a spouse, you can contribute to a spousal RRSP where your spouse is the annuitant, up until the end of the year in which your spouse turns age 71.

You can wind up or mature your RRSP at any age prior to December 31 of the year you turn 71. The maturity options include:

- Converting the RRSP to a registered retirement income fund (RRIF)

- Using the funds in your RRSP to purchase an eligible annuity

- Withdrawing your RRSP funds in cash; you may also be able to make withdrawals in-kind (please check with the RRSP administrator that you can make withdrawals in-kind)

Ask your RBC advisor for an article that discusses these maturity options in detail.

The benefits of RRSP investing

The following are some of the main benefits of investing in an RRSP:

Tax deduction

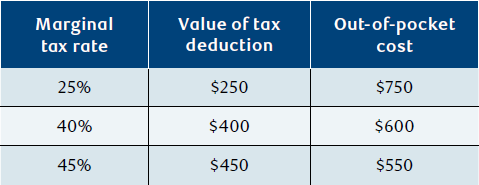

Contributions to an RRSP are deductible for tax purposes within certain prescribed limits. The deduction can be used against all sources of taxable income. This deduction reduces your amount of taxable income for the year and thus your taxes payable. The actual tax savings will depend on your marginal tax rate. The following table outlines the out-of-pocket cost of a $1,000 RRSP contribution after claiming the deduction.

RRSP contributions made in the current tax year or in the first 60 days of the following tax year are generally deductible in the current tax year. You do not have to claim the full amount of any RRSP contributions you make as a deduction in a particular year. RRSP contributions can be carried forward indefinitely and deducted in a future tax year.

If your income tends to fluctuate from year-to-year, it may be advantageous to defer the tax deduction to a future tax year when your marginal tax rate is higher, and thus, your marginal tax rate is higher. While this strategy delays the benefit of the tax deduction, choosing a year where you have a higher marginal tax rate may allow you to maximize the value of the RRSP deduction.

Tax-deferred compounding

Income and realized capital gains earned in an RRSP are generally not taxable in the year they are earned. This means income and capital gains can continue to grow and compound in the RRSP on a tax-deferred basis until you withdraw funds from the RRSP.

Income splitting

Utilizing income splitting strategies between you and your spouse can provide significant tax savings. The strategy of income splitting takes advantage of Canada's progressive tax system where as your taxable income increases, your marginal tax rate increases. Income splitting allows you to reduce your overall family tax bill by having income taxed in a lower-income spouse's hands.

If your income tends to fluctuate from year-to-year, it may be advantageous to defer the tax deduction to a future tax year when your marginal tax rate is higher, and thus, your marginal tax rate is higher.

One method that may help you income split with your spouse is contributing to a spousal RRSP for the spouse who has less retirement savings. For additional information, please ask your RBC advisor for the article on spousal RRSPs and RRIFs. The objective of this strategy is to provide you and your spouse with similar retirement incomes rather than having all your family's retirement income taxed in one spouse's hands.

Contributions to your RRSP

There are several rules and limits you should be aware of when making contributions to an RRSP.

RRSP contribution limit

Your annual RRSP contribution limit is based on your earned income from the previous tax year; your participation in registered pension plans (RPPs), pooled registered pension plans (PRPPs), specified pension plans (SPPs) or deferred profit sharing plans (DPSPs), as well as the prescribed contribution limit.

What is earned income?

Earned income includes the following types of income:

- Salary or wages from employment; this amount is reduced by any deducted employment-related expenses such as union or professional dues

- Disability pensions paid under the Canada Pension Plan (CPP) or Quebec Pension Plan (QPP) (you must be a resident of Canada when you receive the payments) and taxable income from a disability plan; regular CPP and QPP retirement pensions do not qualify as earned income

- Net income from a business carried on by a self-employed individual or by an active partner of a partnership

- Net rental income from real property

- Payments from supplementary unemployment benefit plans (not Employment Insurance)

- Taxable spousal and child support payments

- Royalties and net research grants

Earned income is reduced by certain deductions and losses, including the following amounts:

- Losses from a business carried on by a self-employed individual or by an active partner of a partnership

- Net rental losses from real property

- Deductible spousal and child support payments

Some common types of income not considered earned income are:

- A retiring allowance or severance payment

- Investment income from a passive portfolio

Calculating your RRSP contribution limit

If you haven't participated in an RPP or a DPSP in the previous tax year, the maximum RRSP contribution you could earn is equal to the lesser of:

- 18% of your earned income for the previous tax year, or

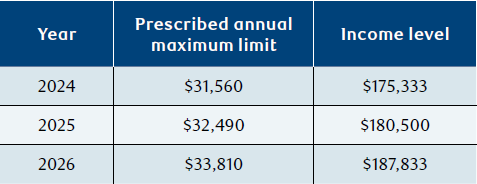

- The prescribed annual limit for the year

This table shows that to earn the maximum amount in 2026, your 2025 earned income would need to be equal to or greater than $187,833.

If you're a member of an RPP or a DPSP, your RRSP contribution limit may be reduced by the value of benefits you've accumulated in the RPP or DPSP. The value is calculated by your employer and is reported to you and the Canada Revenue Agency (CRA) as a pension adjustment (PA). The PA indicated on your prior year's T4 slip reduces your RRSP contribution limit for the current tax year.

If you're a member of a defined benefit pension plan, you may also have a past service pension adjustment (PSPA) which will reduce your RRSP contribution limit. A PSPA could result if you purchase pension benefits relating to prior years of employment (after 1989) or where the pension plan is being amended retroactively to improve the benefits for members in respect of years of pensionable service after 1989.

If you're terminating your interest in an RPP or a DPSP before retirement, you may receive a pension adjustment reversal (PAR), which can erode some of your lost RRSP contribution room. The PAR is intended to increase your RRSP contribution room where your termination benefit under the RPP or DPSP is less than the sum of all PAs that were previously reported.

Finally, if you're part of a group RRSP, it's important to remember that group RRSP contributions count towards your regular RRSP contributions for the year. If you're part of a group plan offered by your employer, be sure to take these contributions into account when determining how much you should contribute to an RRSP personally.

Here's an example that illustrates how to calculate your RRSP contribution limit.

Throughout 2025, Susan was employed by a company that sponsors a pension plan for its employees. Her employer reported a 2025 PA of $6,000 on her 2025 T4 slip. Susan's employment income in 2025 was $50,000. She has always made her maximum RRSP contribution each year. Susan's 2026 contribution limit would be calculated as follows:

Unused contribution from prior years: NIL (a)

PLUS the lesser of:

18% of earned income from prior year ($50,000 x 18% = $9,000) OR the maximum annual 2026 contribution ($33,810): $9,000 (b)

LESS pension adjustment from prior year: $6,000 (c)

TOTAL: (a + b) - c: $3,000 (d)

LESS past service pension adjustment (PSPA): NIL (e)

PLUS pension adjustment reversal (PAR): NIL (f)

Allowable deductible contribution: d - e + f: $3,000 (g)

Each year, the CRA sends out, along with your Notice of Assessment for your tax return, a calculation of what your RRSP deduction and contribution limits are for the year. For a better understanding of how to interpret your RRSP deduction limit and available contribution room statement, please ask your RBC advisor for an article on this topic.

Carrying forward unused RRSP contribution room and unused contributions

If you don't contribute your maximum available contribution limit to your RRSP, you can carry forward the unused portion and make the contribution in a future year. This unused portion can be carried forward indefinitely.

If you contribute to your RRSP, you do not have to claim a deduction for that year. For example, if you contribute $5,000 to your RRSP in 2026, you can carry forward some or all of your deduction to 2027 or subsequent tax years. You may wish to use this strategy if you want immediate access to tax-deferred growth but expect to be in a higher tax bracket in a future tax year and would benefit more from a deduction in that year. Contributions that you've already made but not yet deducted will appear on your RRSP deduction limit and available contribution room statement as unused contributions previously reported. Please note that even if you have not yet claimed the deduction, your RRSP contribution room will still be reduced.

Excess contributions

You can make a contribution to your RRSP in excess of your RRSP contribution limit up to an amount of $2,000 without being subject to a penalty tax. This $2,000 excess contribution limit is intended as a buffer in the event you inadvertently exceed your actual limit for the year.

Making a $2,000 excess contribution may appear to be advantageous, as you're not subject to the penalty tax, and you're able to benefit from tax-deferred growth on this amount. However, you cannot deduct the excess contribution from your taxable income. If you don't deduct the $2,000 from your income, you may be subject to double taxation: once, as you never deducted it when it was contributed to the RRSP (you would have generally paid tax on this amount when it was earned), and a second time when you withdraw it from the plan. If possible, you may wish to consider treating this excess contribution as part of a future year's contribution limit and ensure to deduct it in the future.

If your contributions do exceed your available contribution limit by more than $2,000 at the end of any given month, you will be subject to a 1% tax on the excess amount for each month that the excess amount remains in the plan or until the excess amount is absorbed by new RRSP contribution room.

In-kind contributions

Instead of contributing cash to your RRSP, you can choose to contribute eligible investments from your non-registered account to your RRSP at their fair market value (FMV). For tax purposes, investments contributed to an RRSP (i.e. in-kind contributions) are treated as if they are actually sold. Therefore, this contribution may trigger a taxable capital gain or loss. Unfortunately, if the FMV of the transferred investment is less than its original cost, the resulting capital loss cannot be claimed.

For example, on the transfer of two securities to an RRSP, one with an unrealized gain of $1,500 and the other with an unrealized loss of $500, the gain of $1,500 is included in income, but the loss cannot be used to reduce the gain to $1,000. You will need to report $1,500 of capital gains on your tax return as a result of this contribution. If you'd like to be able to claim the loss, you can sell the securities in your non-registered account and then contribute cash to your RRSP. To ensure you can claim the loss, you may want to wait at least 30 days after the sale before buying back the identical security.

Finally, any accrued interest on the investment up to the transfer date (i.e. interest that has been earned but not paid) must be reported as income by you on your tax return for the year of the transfer.

Transfers into your RRSP

Certain amounts may be transferred into your RRSP without requiring unused RRSP contribution room. For example, when an employee retires or terminates their employment, they may be offered a taxable lump-sum payment, classified as a retiring allowance. It may be possible to transfer the eligible portion of a retiring allowance to an RRSP on a tax-deferred basis without using RRSP contribution room. For further information about retiring allowances, ask your RBC advisor for an article on this topic.

RRSP assets can also be transferred on a tax-deferred basis between RRSP accounts. A common reason for transfers between RRSPs is to consolidate your RRSPs into one plan. This may simplify the administration of your RRSPs, making it easier to maintain a proper asset mix and evaluate performance. It may also reduce expenses to you relating to the administration of your RRSPs.

Investment options for your RRSP

The investment options for your RRSP are wide ranging, but there are specific restrictions on what you can invest in. Your investment options will also vary depending on the type of RRSP account you have and at which financial institution you choose to hold your RRSP. A self-directed RRSP will provide the widest range of possible investment options. See the appendix for more information on the types of investments you can hold in your RRSP and the potential penalties that might apply if you were to hold a non-qualified investment in your RRSP.

Strategies to maximize your RRSP

There are several strategies available that may help you maximize the value of your and your spouse's RRSPs.

Spousal RRSPs

If you have a spouse who will be in a lower tax bracket than you on retirement, you may wish to consider contributing to a spousal RRSP rather than your own RRSP. This may help maximize your retirement benefits and minimize taxes payable.

A spousal RRSP is an RRSP that has received contributions from the plan annuitant's spouse. By contributing to a spousal RRSP that the lower-income spouse is the annuitant of, the contributor, who is typically the higher-income earner, gets a deduction at their marginal tax rate; the lower-income spouse will pay tax at their marginal tax rate when withdrawals are eventually made from the RRSP (subject to the attribution rules if funds are withdrawn in the year of contribution or in the two following calendar years).

For additional information on this strategy, please ask your RBC advisor for the article on spousal RRSPs and RRIFs.

Contribute early

By making your RRSP contribution at the beginning of the year or by making regular monthly contributions, you may be able to maximize the tax-deferred growth in the RRSP and avoid the stress of trying to meet a last-minute deadline.

Borrowing to make an RRSP contribution

The interest on a loan used to make an RRSP contribution is not tax deductible. Deciding whether or not to borrow to contribute to your RRSP is also complicated by the fact that you can carry forward your unused contribution limit to a future tax year when you may have the funds available to make the contribution. While carrying forward your contribution room will avoid borrowing costs, the potential for tax-deferred growth will be forfeited. In general, if you expect to be able to repay an RRSP loan within a short period of time, this strategy may prove advantageous. For additional information on this strategy, please ask your RBC advisor for the article on borrowing to contribute to your RRSP.

Withdrawals from an RRSP

Although RRSPs are intended to provide funds during retirement, there may be occasions when a withdrawal is necessary. It's possible to withdraw or deregister funds from your RRSP before age 71. The amount withdrawn is taxable to you in the year of withdrawal.

Income and capital gains withdrawn do not retain their original tax treatment. Thus, when funds are withdrawn, the withdrawal is not broken down into interest, capital gains, dividends earned or contributions; all amounts are treated as regular taxable income and are subject to tax at your marginal tax rate.

Withdrawing from an RRSP before age 71

You may wonder when the best time is to begin withdrawing the funds you've built up in your RRSP. You may ask whether you should wait until age 71, when it's mandatory to wind up your RRSP, and get more tax-deferred growth, or whether you would be better off making early withdrawals from your RRSP even if you don't need the money.

In general, if you require your RRSP funds for your day-to-day living expenses and you have no other sources of income (e.g. non-registered assets, employer pension income, CPP/QPP and old age security (OAS)), there may be no other choice but to start early RRSP withdrawals. If the need is recurring, consider maturing all or a portion of your RRSP to a RRIF or annuity.

In circumstances where you have both non-registered and registered assets, a common rule of thumb is to use your non-registered assets first before using funds from your RRSP. The argument is that if you're withdrawing from an RRSP earlier than necessary, you're prepaying the tax on your RRSP withdrawal, and you'd lose the potential tax-deferred compounding in the plan.

There are, however, some situations where it may make sense to consider withdrawing from your registered assets before using your non-registered assets. Here are some examples:

• You're getting close to age 71 (therefore, fewer years remaining for tax-deferred compounding)

• You're in a lower tax bracket now than you expect to be when you start drawing on your RRSP assets

• You're concerned about a potential OAS clawback or impact on other income-tested government benefits such as the guaranteed income supplement (GIS) when you have to receive mandatory payments from registered savings in the future

• You're concerned about a high tax liability on RRSP assets that may remain after death

Another situation where you might want to consider withdrawing from your registered assets is when you are 65 or over and would like to take advantage of the $2,000 pension income tax credit. In such a case, you may want to convert a portion of your RRSP to a RRIF to generate eligible pension income that qualifies for this tax credit. If you're in the lowest marginal tax bracket, this credit may allow you to receive $2,000 of RRIF income tax-free for federal tax purposes. The value of this credit should be compared to the loss of the tax-deferred growth in the registered plan. You should also note that if you're 65 or over and withdraw funds from a RRIF, you can split up to 50% of the RRIF payment with your spouse. This may allow you to transfer some of the income that would otherwise be taxable at your high marginal tax rate to your lower-income spouse.

The question of whether to begin withdrawing from an RRSP prior to age 71 is not easy to answer. Your personal situation, including your goals, objectives, tax rates, asset allocation and risk tolerance, must be analyzed before a recommendation can be made.

Withholding tax

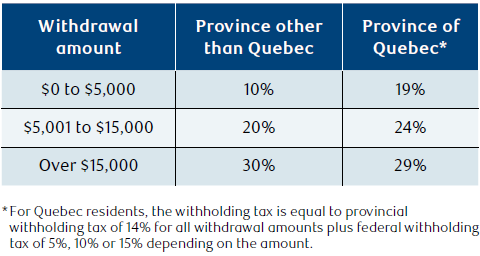

Most withdrawals you make from an RRSP are subject to withholding taxes. The amount you withdraw determines the rate of withholding tax that will be applied at the time of the withdrawal. The withholding tax rates for Canadian residents are the same for all provinces except Quebec. Withholding tax for non-residents is discussed later in this article. The following table shows the percentage of withholding tax that applies when you make a single lump-sum withdrawal.

Certain amounts you withdraw from your RRSP are not subject to withholding taxes. They include:

- An RRSP withdrawal under the home buyers' plan

- An RRSP withdrawal under the lifelong learning plan

- The removal of unused RRSP contributions where you have an approved CRA Form T3012A — Tax Deduction Waiver on the Refund of Your Unused RRSP, PRPP, or SPP Contributions from your RRSP

It's important to note that the withholding tax applied to your RRSP withdrawal does not necessarily represent your final tax liability with respect to your RRSP income. Your RRSP income is subject to tax at your marginal tax rate. If your marginal tax rate is greater than the rate of withholding tax applied, you may have to pay more tax on the RRSP withdrawal. If your marginal tax rate is less than the withholding tax applied, you may receive a refund after you file your tax return for the year.

Impact of a series of withdrawals

You may wish to make a series of withdrawals from an RRSP rather than taking one lump-sum payment. This may have an impact on the withholding tax rate that will apply on your withdrawals.

If you make a series of smaller withdrawals from an RRSP (i.e. instalments to fulfil a single request), the rate of withholding on each individual payment should be based on the total sum requested and not on each individual payment. For example, if you were to make a withdrawal request for $12,000 at the beginning of the year and ask that it be split into monthly payments, each payment would be considered a portion of a single request. Because the total amount of the withdrawal for the year is known in advance, the withholding tax rate that applies to each payment is based on the total payment. In this example, the withholding tax rate that applies to each monthly payment of $1,000 would be 20% in provinces other than Quebec. If, later in the year, you request an additional amount, over and above the instalment payments, this will be considered a separate request and the withholding tax rate that will be applied will be based on that payment only.

If it appears you're making a series of separate requests in order to minimize the withholding tax, it is the CRA's position that the withholding tax rate should be determined as if there was one request equal to the total of all amounts requested and a higher withholding rate could apply. This could be the case where you make a series of requests in a short period of time (e.g. on the same day or over five consecutive days).

Quarterly tax instalments

It is possible that the amount of withholding tax on your RRSP withdrawals may not be sufficient to cover your actual tax liability. You may have to pay additional tax on your RRSP withdrawals when you file your income tax return, and this may result in you having to make tax instalments in subsequent years.

If your net tax owing (your total tax liability less all amounts withheld at source) for the current year and either one of the two immediately preceding years exceeds $3,000 ($1,800 in Quebec), you may need to make tax instalments in subsequent years.

For more information regarding tax instalments, ask your RBC advisor for the article on quarterly tax instalments.

Increasing your withholding tax

To avoid the possibility of having to make future quarterly tax instalments, you may request that a larger amount of tax be withheld on your RRSP withdrawals by completing CRA's Form TD1, Personal Tax Credits Return (TD1 Form). Quebec residents will also need to complete Form TP1017-V, Request to Have Additional Income Tax Withheld at Source. The form(s) must be completed and provided to the financial institution holding your RRSP.

Reducing your withholding tax

In order to reduce or waive the withholding tax, your financial institution may require you to provide them with either a completed TD1 Form or authorization from the CRA. To obtain approval from the CRA, you'll need to send the CRA a completed Form T1213, Request to Reduce Tax Deductions at Source. Quebec residents must use Form TP-1016, Application for a Reduction in Source Deductions of Income Tax, to request reduced withholding tax from Revenu Québec.

Tax reporting slips

You will receive a T4RSP slip for any amounts you withdraw from your RRSP during the year. This tax slip is issued by the end of February of the calendar year following the year of withdrawal. The T4RSP reports the gross income paid out to you, as well as any federal and provincial taxes (except for Quebec) that have been withheld and remitted to the government. For Quebec residents, the T4RSP will show the gross income and only the federal withholding tax. This is because residents of Quebec also receive a Relevé 2 slip for provincial income tax purposes. The Relevé 2 reports the gross income withdrawn from the RRSP, as well as the Quebec withholding tax.

Non-residents

Withdrawals from RRSPs made by non-residents of Canada are subject to different withholding tax rules. In general, RRSP withdrawals are subject to a 25% withholding tax. The rate of withholding tax that applies may be lower if Canada has a tax treaty with the country where you are resident. Payments and taxes withheld are reported to non-residents on an NR4 slip.

Conclusion

RRSPs are one type of savings vehicle that can be used for retirement. Understanding the rules specific to RRSPs can help you incorporate this savings vehicle in your retirement plan. Speak with a qualified tax advisor to ensure you've considered your circumstances before contributing to or making a withdrawal from your RRSP.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.

Appendix: Anti-avoidance rules

The qualified investments you're permitted to hold in your RRSP include (but are not limited to): cash, mutual funds, securities listed on a designated stock exchange, GICs and certain shares of small business corporations.

Non-qualified investments are investments that do not meet the definition of a "qualified investment" under the Income Tax Act. Examples of non-qualified investments include shares in private investment holding companies or foreign private companies, shares that become delisted from a designated stock exchange and real estate.

Prohibited investments include debt of the annuitant and investments in entities in which the RRSP annuitant or a non-arm's length person has a "significant interest" (generally 10% or more ownership) or entities with which the RRSP annuitant does not deal at arm's length.

The consequences of holding a non-qualified or prohibited investment inside your RRSP can be quite harsh. In the year you purchase the non-qualified or prohibited investment inside your RRSP or in the year an investment becomes non-qualified or prohibited, you may incur a penalty tax of 50% of the FMV of the investment.

If you did not know and could not have known, at the time the investment was obtained, that the investment was or would become non-qualified or prohibited, and you dispose of the investment from the RRSP or the investment ceases to be non-qualified or prohibited by the end of the year following the year in which the tax applied (or at a later time as permitted by the Minister of National Revenue), you may be able to obtain a refund of this penalty tax.

Any income or capital gains that a prohibited investment earns will be considered an "advantage" and is subject to a 100% penalty tax.

In addition to restrictions on what you can hold in your RRSP, there may be certain transactions that can result in negative tax consequences. One example is a "swap transaction." This type of transaction involves a transfer of assets (other than a contribution or withdrawal) between your RRSP and yourself (or a person with whom you do not deal at arm's length). If you engage in a swap transaction, the increase in the total FMV of the RRSP as a result of the swap transaction is considered an advantage and is subject to a 100% penalty tax. In addition, all future increases in the RRSP that are reasonably attributable to the initial swap transaction will be considered an advantage. Therefore, any dividends, interest or other amounts paid on the swapped security, any appreciation in value of the swapped security or on any substituted property, and any income earned on income would be subject to the 100% advantage tax.

There is an exception to these rules. You may be able to swap a non-qualified or prohibited investment from your RRSP with cash or other property of equal value that you hold outside of your RRSP. After 2022, you will only be eligible to do this type of swap if you're entitled to the refund of the 50% penalty tax on the non-qualified or prohibited investment.