Registered retirement savings plan (RRSP) maturity options

Understanding your options when your RRSP matures. Although you may wind up your RRSP at any time, you're required to mature your RRSP by December 31 of the year you turn age 71. This article discusses the RRSP maturity options available to you, as well as some considerations in determining when to wind up your RRSP.

Understanding your options when your RRSP matures. Although you may wind up your RRSP at any time, you're required to mature your RRSP by December 31 of the year you turn age 71. This article discusses the RRSP maturity options available to you, as well as some considerations in determining when to wind up your RRSP.

Family Office Services

September 14, 2025

Registered retirement savings plan (RRSP) maturity options

Understanding your options when your RRSP matures

Although you may wind up your RRSP at any time, you're required to mature your RRSP by December 31 of the year you turn age 71. This article discusses the RRSP maturity options available to you, as well as some considerations in determining when to wind up your RRSP.

Any reference to a spouse in this article also includes a common-law partner.

RRSP maturity options

You must collapse your RRSP by the end of the year you turn age 71, after which you have the following three options:

1. You can directly transfer your RRSP assets to a registered retirement income fund (RRIF).

2. You can use the funds in your RRSP to purchase an eligible annuity.

3. You can withdraw your RRSP funds (less withholding tax) in cash or in-kind.

You can choose any one of the options available or you may choose a combination of the options. You can also collapse your RRSP using these options before the age of 71.

RRIFs

A RRIF is an arrangement between you (the annuitant) and an administrator (a financial institution authorized to offer RRSPs/RRIFs) under which payments of at least a minimum amount are made to you each year.

You can have more than one RRIF. Once your RRIF is established, you cannot make contributions to the plan. You can only directly transfer certain amounts from other registered plans, such as an RRSP, another RRIF or a registered pension plan, into your RRIF. Like an RRSP, earnings in a RRIF are tax-deferred and amounts paid out of a RRIF are taxable to you at your marginal tax rate when received.

Under the tax rules, there are only two types of RRIFs — ones that are self-directed and ones that aren't. You may favour a self-directed RRIF if you want to select and manage your own investments. RRIFs, whether self-directed or not, are subject to qualified and prohibited investment restrictions.

When you convert your RRSP to a RRIF, the investments held in your RRSP should be transferred directly into your RRIF account. You are generally not required to liquidate your RRSP investments prior to transferring your RRSP to a RRIF. If you convert all or part of an RRSP to a RRIF before age 71, you're not committed to the RRIF forever. You can transfer the value of your RRIF that exceeds the required minimum payment back to your RRSP any time before December 31 of the year you turn age 71.

RRIF minimum payments

You can withdraw more, but not less, than the annual minimum amount from your RRIF. You can choose to receive your RRIF payment as a lump sum at any time during the year or periodically on a monthly, quarterly, semi-annual, or annual basis, depending on your preference. If you don't require income from your RRIF to meet your financial needs, you may consider receiving the annual minimum payment at the end of the year to maximize the tax-deferral benefits of your RRIF.

While some institutions allow you to receive RRIF payments in-kind (i.e. receive securities rather than cash as a minimum payment), this is not always the case and you may have to sell securities in your RRIF to generate cash to satisfy the minimum payments.

Your RRIF minimum payment for each year, after the year your RRIF is established, is calculated by multiplying the fair market value (FMV) of your RRIF at the end of the previous year by a prescribed percentage factor. The prescribed percentage depends on your age or your spouse's age (if applicable) at the end of the previous year, depending on whose age you elected at the time the RRIF was established. For more detailed information on RRIF minimum payments, please ask your RBC advisor for the article on RRIF payments and withdrawals.

Advanced life deferred annuities (ALDA)

An ALDA is a life annuity where the annuity payment must be started before the end of the year in which you turn age 85. You can transfer up to 25% of your RRSP or RRIF (subject to a maximum of $800,000 in 2025) to purchase an ALDA. The purpose of an ALDA is to reserve a portion of your registered assets for later in retirement and reduce your longevity risk. Also, since the portion of the registered assets that are invested in the ALDA are not used to calculate your annual RRIF minimum, this lowers your required minimum payment and the associated taxes. A lower required minimum payment from a RRIF may also help reduce the recovery of certain government benefits such as old age security (OAS).

Tax implications of receiving RRIF income

Your RRIF withdrawals are included in your taxable income and are subject to tax at your marginal tax rate. In some cases, the RRIF administrator will charge withholding tax on your RRIF payments. Amounts withheld are remitted to the Canada Revenue Agency (CRA) on your behalf and are a credit towards your total taxes payable.

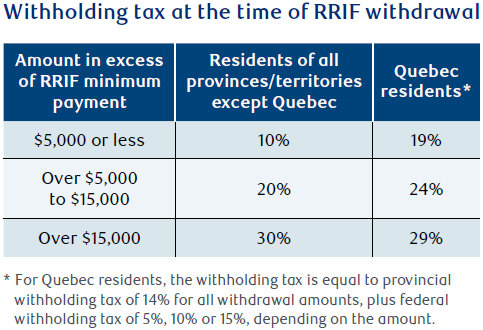

Withholding tax is not required on minimum payments from the RRIF. If you withdraw more than the required minimum payment, income tax will need to be withheld at source on the amount in excess of the minimum amount. The withholding tax rates applied to RRIF withdrawals above the minimum amount are identical to the withholding tax rates applied to RRSP withdrawals.

The withholding tax rates for Canadian residents are the same for all provinces and territories except Quebec. The following table shows the percentage of withholding tax that applies to the amount in excess of the minimum amount when you make a single lump-sum withdrawal:

If you receive RRIF income and are age 65 or over, you may be eligible for the pension income tax credit on the first $2,000 received. This credit translates into a maximum federal annual tax savings of $280 (based on the federal tax credit rate of 14% for 2026 and subsequent tax years). The amount of additional provincial/territorial tax savings varies depending on where you reside. Also, if you are age 65 or over, you can consider splitting up to 50% of your RRIF income with your spouse. By splitting your RRIF income, the income can be taxed in your spouse's hands at their lower marginal tax rate; you may also help reduce the potential impact on certain income-tested government benefits such as the OAS. For more information on RRIF income splitting and the pension income tax credit, please ask your RBC advisor for the articles on these topics.

Tax considerations at death

As a general rule, when you pass away, the FMV of your RRIF, and all other amounts you received from your RRIF in the year, are included as income on your final tax return. Any income earned in your RRIF after the date of death and until December 31 of the year after the year of death will be taxed in the hands of the beneficiary named on your plan or your estate (if no beneficiary is named on the plan) as income in the year it's paid.

There are a few exceptions to this general rule when you designate certain persons as the successor annuitant or beneficiary of your RRIF. In these circumstances, the tax on your RRIF proceeds may be deferred and/or taxed in your beneficiary's hands. For a discussion on some of the advantages and disadvantages of naming certain beneficiaries of your RRIF and the associated tax implications on death, please ask your RBC advisor for the article on estate planning for your RRSP/RRIF.

Annuities

An annuity is a financial contract that binds an issuer to deliver a steady stream of income payments in return for a lump-sum deposit. These payments can be set up to last an entire lifetime (a life annuity) — or for a set period of time (a term certain annuity).

If you purchase a life annuity, you effectively transfer all of the risk of investing to the expertise of the insurer. The annuity will provide a guaranteed income for as long as you live. The main drawback of annuities, in general, is that once you purchase an annuity, the funds used for that purchase are no longer accessible to you. Generally speaking, the decision to annuitize is a permanent decision which cannot be reversed and must be considered carefully.

The amount of the regular income payments from an annuity depends on many factors including your age, your sex and the current rate of interest at the time of purchase. Other factors include the guarantee period, the time between the annuity being purchased and the first payment being made, and the frequency of payments.

There are also many different features that can be added to an annuity that can affect the income amount payable, for example, joint life or inflation protection.

A description of the various types of annuities and options available are beyond the scope of this article. For more information about annuities, you should seek the assistance of an advisor licensed to sell annuities.

Tax implications of receiving income from an annuity

All payments received in a calendar year from an annuity purchased with registered funds (a registered annuity) must be reported as income and are fully taxable. The payments from a registered annuity are generally not subject to withholding tax at the time they're paid to you.

If you receive income from an annuity and are age 65 or over, you may be eligible for the pension income tax credit on the first $2,000 received. Also, if you're age 65 or over, you can consider splitting up to 50% of your annuity income with your spouse. For more information on income splitting and the pension income tax credit, please ask your RBC advisor for the articles on these topics.

Tax considerations at death

On passing, all payments you received during the year, up to the time of death, must be included as income on your final income tax return.

If you named a spouse as the beneficiary of a single life annuity, and the guarantee period has not expired, or the annuity is a joint life annuity, subsequent payments will be made to your surviving spouse and taxed in their hands.

If you named anyone other than your spouse as a beneficiary and the guarantee period has not expired, the death benefit will be paid to your beneficiary as a lump-sum payment. The death benefit is equal to the present value of the remaining payments in the guarantee period from the date of death. The death benefit will be taxable to you in the year of death.

Cash in or deregister your RRSP

The simplest, but usually least tax-efficient, maturity option is to cash in or deregister your RRSP. When you cash in your RRSP, the full value of the RRSP is included in your taxable income in the year of withdrawal. Given that Canada has a progressive tax system, if you have a large RRSP, you may be taxed at the highest marginal tax rate on at least a portion of the amount withdrawn.

If you don't convert your RRSP to an annuity or RRIF by the end of the year you turn age 71, your RRSP may be deregistered in the following year and you'll have to include the full FMV of the RRSP as taxable income in the year of deregistration.

You will be subject to withholding tax at the time of withdrawal or deregistration. When you file your tax return, the withholding tax is used as a credit towards any taxes due.

Before choosing to withdraw or deregister all or a portion of your RRSP, you should consider the following:

• It's a one-time decision that can't be reversed;

• You forgo the opportunity to grow your investments in a tax-deferred environment;

• Payments from your RRSP do not qualify for the pension income tax credit;

• There may be substantial income taxes owing;

• You lose access to certain estate planning opportunities such as leaving your RRSP to a spouse or a financially dependent child or grandchild; and

• The resulting increase in income can potentially impact income-tested government benefits such as OAS.

Considerations when selecting an RRSP maturity option

Determining which maturity option is best for you depends mainly on your financial and personal situation. For instance, a life annuity may not be ideal for you if you have a lower life expectancy or a well-funded defined benefit pension plan. On the other hand, a life annuity may make sense if you're worried about investment risk or longevity risk, as it provides you with a fixed income stream even if there's a market downturn or you live longer than your life expectancy.

It's important to note that you don't have to choose one option exclusively over another. It's quite possible — and often preferable — to combine different options to create a retirement income plan that meets your individual needs. As an example, you may wish to use a portion of your RRSP funds to purchase an annuity and transfer the other portion to a RRIF. Combined, these options will provide you with not only a guaranteed income stream but also some flexibility in managing your retirement funds.

The following sections discuss some of the factors worth considering when selecting the maturity option that is right for you.

Your retirement income needs

First, consider whether your other sources of retirement income (such as an employer pension, the Canada Pension Plan (CPP)/Quebec Pension Plan (QPP), OAS, and other investment income) will be sufficient to maintain your lifestyle in retirement. If you'll require little or no additional income from your RRSP in the near future, transferring your RRSP funds to a RRIF may provide you with the maximum tax deferral. Alternatively, if you're worried your sources of income in retirement may not be enough if you have greater longevity, purchasing an annuity may give you the peace of mind you need.

Your estate objectives

If you wish to leave an estate for your heirs, a RRIF is likely the best option for preserving your registered retirement assets. A RRIF allows you to continue to accumulate your registered funds on a tax-deferred basis while enjoying the benefits of a retirement income. Upon your death, the assets remaining in your RRIF can be transferred to a beneficiary or form part of your estate.

A life annuity also offers options to provide for your family after your passing. For instance, you can choose a joint life annuity with a guaranteed period that will provide payments for as long your spouse lives. However, if the annuity has no guarantee period or the guarantee period has expired, the annuity will terminate upon your death (or your spouse's death in the case of a joint life annuity) and no further payments will be made.

The current rate of return and inflation

By purchasing an annuity, you're locking in a fixed interest rate for life. As such, purchasing annuities are generally preferable when interest rates are high. In a low interest rate environment, you may want to consider the various investment alternatives available within a RRIF that can achieve a higher rate of return.

When purchasing an annuity, it's especially important to consider the effect of inflation on your purchasing power. Although a fixed income arrangement may seem ideal for some, an average inflationary trend could easily erode that income. Annuities can be indexed to keep pace with inflation and other increasing fixed lifestyle costs, but annuities that offer protection against inflation may start providing payments at a lower rate.

Flexibility and control versus guarantees

Depending on your situation, you may want to maintain flexibility with respect to your retirement funds, in case your financial or personal circumstances change.

You generally can't cash in a life annuity once it's been purchased. In that sense, annuities are relatively inflexible and give you little control. However, an annuity provides you with a guaranteed stable retirement income stream for the rest of your life. To provide further security for your family, life annuities may be issued with guarantee periods in the event you pass before the guaranteed period is over.

In terms of flexibility, a RRIF provides you with the ability to vary the annual amount you receive, as long as you meet the minimum payment requirements. This flexibility may be useful, for example, if you wish to manage your marginal tax rate or your income needs may vary from year to year. In addition, some federal non-refundable tax credits and benefits, such as the age amount (a non-refundable tax credit) and OAS benefits are reduced or eliminated when your net income exceeds certain thresholds. By varying the level of income you receive, you may be able to minimize or avoid OAS clawback or keep your income level below certain thresholds.

You can maintain control over the assets in your RRIF and can choose from a wide range of investments. But, keep in mind that with that control comes risk, and the value of your RRIF and income you receive from it will vary depending on the rate of return of your investments.

You have the ability to convert your RRIF to a life annuity at any time in the future. You may want to consider doing so when interest rates increase or you find you no longer wish to manage your own RRIF assets as you age and prefer to transfer the investment risk to the insurer.

Timing considerations

Although your RRSP must mature by the end of the year you turn age 71, it may make sense to mature your RRSP at an earlier age. For example, if you're age 65 or over and not receiving an employer pension, you may want to convert a portion of your RRSP to a RRIF or annuity in order to create an income stream and take advantage of the pension income tax credit or pension income splitting with a lower-income spouse. This may allow you to take funds out of your RRSP with little or no tax liability.

If you later decide you no longer want or need the income stream, you can transfer the value of your RRIF that exceeds the required minimum payment back to your RRSP any time before December 31 of the year you turn age 71.

Conclusion

Since the best RRSP maturity option for you depends mainly on your financial and personal situation, it's important to speak with a qualified tax advisor to ensure you have fully considered your specific circumstances in creating a retirement income plan that meets your individual needs. Remember, choosing the timing and the right option for you involves considering a variety of factors. It's important to consider all options and your personal needs and objectives before selecting an RRSP maturity option as some decisions may not be reversable.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.