Retirement compensation arrangement (RCA)

An RCA can be an effective retirement planning tool for high-income earners like business owners, executives and professionals. It may be more flexible than registered retirement savings plans (RRSPs) and registered pension plans (RPPs). RRSPs and RPPs are subject to contribution limits that may not provide you with sufficient retirement income in the future. RCAs instead have the potential of providing you with more income in your retirement years.

An RCA can be an effective retirement planning tool for high-income earners like business owners, executives and professionals. It may be more flexible than registered retirement savings plans (RRSPs) and registered pension plans (RPPs). RRSPs and RPPs are subject to contribution limits that may not provide you with sufficient retirement income in the future. RCAs instead have the potential of providing you with more income in your retirement years.

Family Office Services

April 14, 2026

Retirement compensation arrangement (RCA)

An RCA can be an effective retirement planning tool for high-income earners like business owners, executives and professionals. It may be more flexible than registered retirement savings plans (RRSPs) and registered pension plans (RPPs). RRSPs and RPPs are subject to contribution limits that may not provide you with sufficient retirement income in the future. RCAs instead have the potential of providing you with more income in your retirement years. RCAs can be used to supplement RPP benefits and other savings to better ensure you maintain your standard of living once you withdraw from active employment. An RCA could be considered in the context of your overall retirement, tax and estate planning.

What is an RCA?

An RCA is a plan or arrangement under which an employer, former employer or, in some cases, an employee makes contributions to a custodian. The custodian holds the funds in trust with the intent to eventually distribute the funds to the employee, former employee or other beneficiary upon the employee's retirement, loss of office or loss of employment, or any substantial change in the service the employee provides.

As a trust, there's a written agreement setting out the terms of the trust, such as information about the powers of the custodian, investment of the trust funds, responsibilities, rights and limitations of the parties and resignation, removal and replacement of the custodian, etc.

Why an RCA?

An employer can use an RCA to "super-size" a pension plan. This is because there's no arbitrary upper limit on the amount you or your employer can contribute to the plan, provided the amount contributed is "reasonable" (see discussion in the section, "Contributions to an RCA"). An RCA can provide you with supplemental pension benefits so you may maintain your standard of living in retirement. Typically, an RCA is part of a retirement plan, which may also include an RPP or an individual pension plan (IPP), set up by the employer. An RCA may also provide pension benefits to employees when a company doesn't have an RPP.

Advantages of an RCA

• RCA contributions don't affect RPP/IPP contributions; however, RPP/IPP contributions may reduce the amount that can be contributed to an RCA since contributions to an RCA have to be reasonable, which involves taking into account your total retirement package.

• Employer or employee contributions to an RCA don't affect your RRSP contribution room, as they don't generate a pension adjustment (PA).

• A contribution to an RCA provides a tax deduction to an employer and therefore reduces the corporation's taxable income. Contributions aren't taxable to you until you receive the benefit in a future year, potentially when you're in a lower tax bracket. However, keep in mind that the contributions to the RCA are subject to a 50% refundable tax (discussed later).

• As an owner-manager, you may be able to use an RCA to reduce the purchase price of your business (therefore reducing any capital gains taxes) prior to the sale or transfer of your business, subject to the reasonability of the contributions.

• The company may use an RCA to fund severance payments. The full amount of the contribution is deductible to the employer. You may receive the income in a later year or in installments.

• Upon the death of the employee or former employee, proceeds from an RCA aren't subject to probate fees if a beneficiary is designated on the RCA plan. If the estate is the beneficiary of the RCA, probate may be required.

• RCA contributions don't require payroll and healthcare taxes to be withheld.

• RCAs may provide a level of protection from an employer's creditors.

• Unlike RRSPs and registered retirement income funds (RRIFs), locked-in plans and RPPs/IPPs, there's no statutory requirement to start receiving income from an RCA after the year you reach age 71.

Disadvantages of an RCA

• Since contributions to an RCA and any excess of income and realized capital gains over losses and realized capital losses in the RCA are subject to a refundable tax of 50%, the amount of funds available for investment in an RCA is significantly less than if the funds are kept in the corporation to invest.

• The 50% refundable tax remitted to the Canada Revenue Agency (CRA) is non-interest-bearing.

• There are initial setup fees, and ongoing management and administration fees.

• The custodian will need to file a T3-RCA, Retirement Compensation Arrangement (RCA) Part XI.3 Tax Return, each year, even if there has been no activity in the RCA trust in the year.

Taxation of an RCA

Contributions to an RCA

The employer can generally deduct 100% of their RCA contributions. Unlike for RPPs, there's no specified threshold amount of contributions an employer can make to an RCA, as long as the amounts are "reasonable" and not excessive relative to the target retirement compensation to be provided.

The Income Tax Act (ITA) also allows tax-deductible contributions by you. However, your personal contributions can't exceed those of the employer, and you must be required, under the terms of employment, to contribute to the RCA. Your contributions will reduce the amount that may be contributed by the employer since total contributions to the RCA must be reasonable.

The CRA may disallow the employer's deduction for contributions to an RCA if the amount is not "reasonable". While the ITA doesn't define what's considered reasonable contributions to an RCA, the CRA stated in an Income Tax Technical News No. 34 that:

The CRA takes the view that benefits will not be reasonable if, for example, they are more generous than benefits that would be commensurate with the employee's position, salary and service or they do not take into account benefits that are provided through one or more registered plans.

Instead, the RCA should provide a normal level of benefits, which the CRA describes as follows:

A normal level of benefits would be the same benefit provided under a registered pension plan without regard to the limits. This would be 2% x years of service x final average earning or about 70% of pre-retirement income of an employee with 35 years of service.

In other words, the CRA allows the formula generally used for defined benefit pensions to be used for the purposes of determining RCA retirement benefits but ignoring the tax maximum imposed on defined benefit pension plans by the ITA. This continues to be CRA's position with respect to reasonable contributions to an RCA. A qualified actuary can help you determine a reasonable RCA contribution.

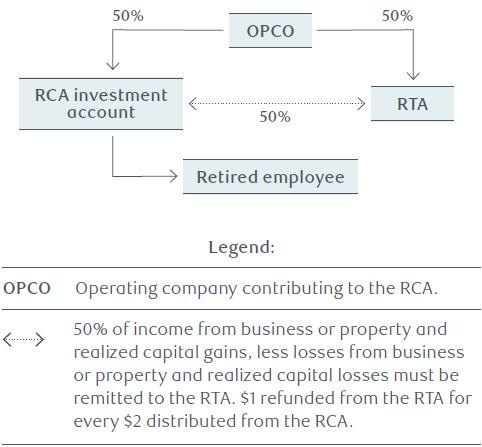

Refundable tax account (RTA)

When a contribution is made to an RCA, only half of the contribution is deposited with the custodian of the RCA trust. The other half is deposited with the CRA into the RTA as a payment of the 50% refundable tax. The RTA is a non-interest-bearing account. It accumulates the refundable tax remitted to the CRA until distributions are made out of the RTA. When a distribution is made out of the RTA, the CRA will refund some of the tax to the RCA.

In addition, 50% of all income earned and capital gains realized, less losses incurred and capital losses realized in the RCA trust must be remitted to the RTA on an annual basis. Unlike investment income earned in a personal non-registrant investment account or regular trust account, Canadian dividends and capital gains don't receive preferential tax treatment in an RCA. In other words, the entire capital gain is subject to the 50% refundable tax and the RCA doesn't receive a dividend tax credit on taxable Canadian dividends.

When the RCA makes distributions to the employee, former employee or other beneficiary, $1 is refunded from the RTA to the RCA trust for every $2 distributed.

There's an alternative method, via an election, for computing the refundable tax of an RCA when the property held by the RTA at the end of the year consists only of cash, debt obligations or shares listed on a designated stock exchange, or a combination of these. The election is designed to allow the RCA to recover an amount equal to the refundable tax at the end of the previous year on termination of the RCA or a portion of such refundable tax when the RCA trust has suffered a loss in the value of its investments. In other words, this election may make it possible to recover 100% of the RTA balance if the RCA is completely paid out, even where the value of the investments in the RCA is less than the balance of the RTA. A detailed discussion of the election is beyond the scope of the article.

Anti-avoidance rules

The 2012 Federal Budget introduced a penalty tax regime on "prohibited investments" and "advantages" for RCAs, effective after March 28, 2012. These measures are similar to the anti-avoidance rules applicable to registered plans, such as RRSPs, RRIFs and tax-free savings accounts (TFSAs), where a 50% tax on the fair market value (FMV) of a "prohibited investment" and a 100% tax on the FMV of an "advantage" are payable by RCA custodians. A detailed discussion of these rules is beyond the scope of this article, but you may want to review the rules with a qualified tax advisor.

Distributions from an RCA

All distributions out of an RCA trust are fully taxable and subject to withholding tax at source. The RCA custodian has to provide you with a T4A-RCA slip, Statement of Distributions from a Retirement Compensation Arrangement (RCA), showing the amount of distributions and the income tax deducted. You have to report the RCA income on your income tax return in the year it's received. It's taxable at your marginal tax rate.

Distributions to non-residents

The custodian may withhold 25% when making payments to a non-resident employee, former employee or other beneficiary from the RCA, unless this rate is reduced by a tax treaty. If the payments qualify as "periodic pension payments," the withholding tax rate may be reduced if the individual is a resident of a country that has a tax treaty with Canada and the treaty allows for a reduced rate.

RCA payments are considered periodic unless they're specifically excluded from the definition of periodic, in which case they're considered lump-sum payments. Generally, the following RCA payments will be considered lump-sum payments and wouldn't benefit from reduced tax treaty rates:

• Payments that aren't part of a series of payments to be made annually or more frequently over the lifetime of the recipient or over a period of at least 10 years

• Payments that aren't made to a recipient by reason of a disability of the recipient

• Payments that aren't the continuation of payments to a beneficiary of a deceased person who was receiving "periodic pension payments" and whose "pension payments" were guaranteed for a minimum number of years

The tax treatment of RCA income and RCA payments in the individual's country of residence depends on their local tax rules. If you don't live in Canada and you're entitled to benefits out of an RCA, speak with a qualified tax advisor in your country of residence for more information.

There are special planning considerations when setting up an RCA for a Canadian resident who's also a U.S. person (U.S. citizen or green card holder). If you're a U.S. person, speak to a qualified cross-border tax advisor.

Pension income splitting

In some cases, you may be able to split your RCA income with your spouse or common-law partner. The following conditions must be met:

• You must be at least 65 years of age, and

• The RCA payments must be in the form of life annuity payments and be supplemental to benefits received out of an RPP, other than an IPP

The RCA payments that are eligible for pension income splitting are subject to a limit. The limit is calculated as the "defined benefit limit" multiplied by 35, minus your other eligible pension income. If the calculated amount is greater than your actual RCA payments, you are limited to your actual RCA payments. The "defined benefit limit" changes annually and can be found on the CRA website.

RCA distributions eligible for pension income splitting should be reported in box 17 of the T4A-RCA slip. If you're at least age 65 in the year, you may be able to elect to split this income with your spouse.

Termination of RCA or death of employee or former employee

The custodian holds the RCA funds with the intent of eventually distributing them to the employee, former employee or other beneficiary on or after an employee's retirement, loss of office or employment, or any substantial change in the services the employee provides. When one of these triggering events occurs, depending on the design of the RCA plan, distributions can be made either periodically or in a lump sum. RCAs are generally more flexible than RPPs and other types of registered plans in terms of when and how much can be paid out of the plan. For example, you don't necessarily have to start taking payments out of an RCA when you turn a certain age, especially if you're still working for your employer and there hasn't been a substantial change in the services you provide to them. Compare this to an RPP, IPP or an RRSP, which must start an income stream to the plan member or annuitant after the year in which they turn 71.

Examples of some situations where the RCA may be terminated, in accordance with the RCA agreement, is when you sell your business before your planned retirement age and your business sponsored an RCA for you, if you leave Canada to a low- or no-tax jurisdiction, or in the event of death of the employee or former employee. Of course, the recipient is taxed as funds are distributed, and the RCA receives the refundable tax from the CRA at that time. If you decide to wind up the RCA, and the RCA agreement allows for early termination, the whole RTA may be refunded to the RCA plan.

The entitlement to the RCA benefits on the death of the plan member is determined by the terms of the RCA agreement. The sponsoring company may impose certain terms and conditions which will vary by plan. For example, if the plan designates the spouse as the beneficiary after the death of the RCA member, the RCA benefits may be transferred to the member's surviving spouse on a tax-deferred basis. In this case, the surviving spouse will be taxable on distributions made to them from the RCA in the year the distributions are received. If there's no surviving spouse, the plan member's RCA entitlement may have to be included as income on their final return (or on a "rights or things" return). The RCA benefits can then be distributed to the deceased's estate.

The terms of an RCA agreement dealing with the death of the RCA member aren't specifically restricted or governed by law. The terms can be determined by negotiation between the RCA member and the RBC Wealth Management Company. Therefore, it's important to consult with a qualified tax and/or legal advisor to understand the RCA benefits at death and the tax implications.

U.S. estate tax

Generally, Canadian residents, who are non-U.S. persons, are only subject to U.S. estate tax on death on their U.S. situs assets. U.S. securities held in an RCA could potentially be included as the RCA plan member's U.S. situs assets on death for the purposes of calculating their U.S. estate tax liability, depending on the design and terms of the RCA. You should consult with a qualified cross-border tax advisor to determine whether your U.S. assets held in your RCA would be included as part of your estate for U.S. estate tax purposes.

Conclusion

Given the advantages and disadvantages of RCAs, you may want to consider an RCA in the following scenarios:

- If you're a business owner, to reward long-term employees and retain top executives; an RCA contract provides flexibility in setting the terms of payment participation

- If you're an owner-manager contemplating moving and retiring outside of Canada, in a lower-tax jurisdiction, or in a province or territory with a lower tax rate; setting up an RCA in this case may allow you to reduce your personal taxes ultimately paid in retirement in the lower-tax jurisdiction

- If you plan to sell your business, to reduce the value of your business and the resulting capital gain

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is intended for informational purposes only and is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on your own circumstances, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.