Retiring allowances

If you're leaving your employer, you may be offered a retiring allowance. This article discusses what a retiring allowance is, the taxation of a retiring allowance and the rules that may allow you to defer tax by contributing your retiring allowance to your registered retirement savings plan (RRSP).

If you're leaving your employer, you may be offered a retiring allowance. This article discusses what a retiring allowance is, the taxation of a retiring allowance and the rules that may allow you to defer tax by contributing your retiring allowance to your registered retirement savings plan (RRSP).

Family Office Services

October 14, 2025

Retiring allowances

If you're leaving your employer, you may be offered a retiring allowance. This article discusses what a retiring allowance is, the taxation of a retiring allowance and the rules that may allow you to defer tax by contributing your retiring allowance to your registered retirement savings plan (RRSP).

What is a retiring allowance?

A retiring allowance (also called severance pay) is an amount your employer pays to you, an employee, upon retirement or upon loss of employment. A retiring allowance can be paid to you in a lump sum or over one or more years. The amount paid is usually based on your length of service and position within the organization.

A retiring allowance is often just one component of a severance package, which may also include other payments, benefits, and incentives.

A retiring allowance can include:

- A payment for unused sick leave credits on termination; and

- An amount received when employment is terminated, including an amount for damages (such as wrongful dismissal) when the employee does not return to work.

A retiring allowance does not include:

- Salary, wages, bonuses, overtime and reimbursement of legal fees;

- Salary continuance;

- A superannuation or pension benefit;

- An amount received as a result of death;

- A benefit derived from certain counselling services;

- A payment for unused vacation;

- A payment in lieu of termination notice; and,

- Damages for violations or alleged violations of an employee's human rights awarded under human rights legislation that are not taxable.

The eligible versus non-eligible portion

Your retiring allowance may include an eligible and a non-eligible portion.

Your retiring allowance may include an eligible portion if you had years of service before 1996. The eligible portion is calculated as the lesser of:

i. The actual amount you receive as a retiring allowance; and

ii. The sum of:

a. $2,000 for each year or part of a year you worked for the employer (or person related to the employer) before 1996; and

b. $1,500 for each year or part of a year you worked for the employer (or person related to the employer) before 1989 in which you had earned no pension or deferred profit sharing plan (DPSP) benefit from employer contributions that were vested in you at the time of the retiring allowance payment. Generally, if you were not a member of a pension plan or DPSP for years prior to 1989, you're likely eligible for this additional $1,500 per year.

Any part of your retiring allowance that isn't eligible is considered non-eligible.

How are retiring allowances taxed?

Generally, a retiring allowance must be included in your income and taxed at your marginal tax rate. However, there are situations where you can transfer all or part of a retiring allowance to a registered pension plan (RPP) or an RRSP to defer the tax. A direct transfer of a retiring allowance to an RPP is uncommon since it may result in a pension adjustment that would affect your RRSP deduction limit for the following year. As such, this article focuses on transfers of a retiring allowance to an RRSP.

You can transfer or contribute all or part of the eligible portion of a retiring allowance to your RRSP, without using your unused RRSP contribution room. You may also be able to transfer or contribute all or part of the non-eligible retiring allowance to your RRSP, provided you have sufficient unused RRSP contribution room. Transferring or contributing your retiring allowance to your RRSP allows you to defer taxes on the amount transferred, as you'll only be taxed on the amount once you receive a payment or withdrawal from your RRSP or RRIF.

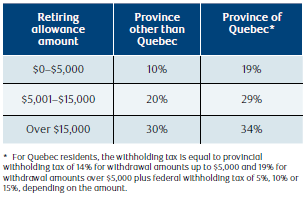

Withholding tax

If you don't transfer all or part of your retiring allowance to an RRSP, your employer will need to deduct income tax from any amounts contributed to your RRSP by your employer but not deduct Canada Pension Plan (CPP) or Employment Insurance (EI) premiums from any retiring allowance payment. The amount of tax your employer needs to withhold depends on the amount of the taxable payment, as follows:

The tax withheld on your retiring allowance payment is not your final tax liability

Your total taxable income determines your total taxes payable. The tax withheld acts as a credit towards your total taxes payable. If the amount of tax withheld is greater than your total tax liability, you'll receive a refund when you file your tax return for the year.

Your options for the eligible portion

The eligible portion of your retiring allowance may be transferred to your RRSP or paid to you, in whole or in part, directly.

Transferred to your RRSP

If you transfer the eligible portion of the retiring allowance to your RRSP, you can transfer it without using your unused RRSP contribution room. Your employer is not required to withhold tax when they transfer the eligible portion to your RRSP.

You must transfer the eligible portion of your retiring allowance to an RRSP for which you are the annuitant. You can't transfer any part directly to a spousal RRSP. Also, you can't transfer any amount to an RRSP if you're over age 71 at the end of the year since you no longer have an RRSP.

Paid to you directly

If the eligible portion of the retiring allowance is paid to you directly, the amount is taxable as income in the year you receive it. Your employer will be required to withhold income tax from the payment.

You're still able to contribute the eligible portion to your RRSP without using contribution room, provided you make the contribution within 60 days from the end of the year in which you received it. However, since your employer is required to withhold tax when the payment is made to you directly, you may need to supplement your contribution with additional funds from other sources. In other words, you're to contribute the gross amount of the eligible retiring allowance to your RRSP to get an offsetting deduction that matches your income inclusion. Contributing the gross amount of your eligible retiring allowance enables you to maximize the amount contributed to your RRSP, without using RRSP contribution room.

Your options for the non-eligible portion

The non-eligible portion of your retiring allowance may be transferred to your RRSP, provided you have unused RRSP contribution room, or paid to you in whole or in part directly.

Transferred to your RRSP

If you want to defer the taxes payable on the non-eligible portion of your retiring allowance, you can contribute the amount to your own RRSP or to a spousal RRSP, provided you have sufficient unused RRSP contribution room and you make the contribution within 60 days from the end of the year in which you received it. Your unused RRSP contribution room will be reduced by the amount of your contribution.

Your employer may be willing to contribute the gross amount of the retiring allowance (without withholding tax) directly to your RRSP or to a spousal RRSP but will likely require reasonable proof that you have the available unused RRSP contribution room. Your employer may ask for a copy of your Notice of Assessment for the previous year showing your RRSP deduction limit or they may require you to complete the Canada Revenue Agency (CRA) Form T1213 – Request to Reduce Tax Deductions at Source and have it certified by the CRA.

Even if you have sufficient unused RRSP room (and proof to confirm it), your employer may exercise their discretion to not make a direct transfer to your RRSP. You should contact your employer to determine which options are available to you.

Paid to you directly

If the non-eligible portion of the retiring allowance is paid to you directly, the amount is taxable as income in the year you receive it. Your employer will be required to withhold income tax from the payment.

Tax reporting

Although your employer may not initially inform you of the breakdown of the eligible and non-eligible portion of your retiring allowance, they are required to make the determination on your T4 slip. Your employer must issue you the T4 slip by the last day of February following the year your allowance is paid. You will need to report both the eligible and non-eligible portions of the retiring allowance as income on your tax return.

If you directly transferred all or part of the retiring allowance (either the eligible or non-eligible portion) to your RRSP, you'll receive a contribution receipt for the amount transferred. If you were paid the retiring allowance and then contributed all or part of it to your RRSP or spousal RRSP, you'll receive a contribution receipt for the amount contributed. The RRSP contribution receipts can be used to claim a deduction to offset the income reported from the retiring allowance.

If you're taking advantage of the tax rules that allow you to contribute an eligible retiring allowance to your RRSP without using RRSP contribution room, be sure to report it as a transfer on Schedule 7 on your personal income tax return in order to ensure the contribution does not use your RRSP contribution room.

Financial planning considerations

For your eligible retiring allowance

If you receive an eligible retiring allowance, you don't have to take advantage of the tax rules that allow you to contribute it to your RRSP without using RRSP contribution room. You may have other uses for those funds. For example, you may require money to fund your expenses while you search for a new job or you may wish to pay off debt. If you have an immediate need for the funds, you can request that all or part of the eligible retiring allowance be paid out in cash, subject to withholding tax. Keep in mind that your final tax liability may be greater than the taxes withheld, so be sure to set aside some funds for your taxes.

For your non-eligible retiring allowance

Deferring payment

If you receive a non-eligible retiring allowance, your employer may be willing to defer payment to a future tax year. This option may be preferable if you don't have unused RRSP contribution room or if you choose not to contribute the payment to your RRSP. Deferring receipt of the payment can be beneficial if your total income in the future tax year will be lower than the year in which you were supposed to receive the payment. However, if the company you're leaving is having financial difficulty or if there's any other reason to question whether payment will be received, it may be advisable to receive the whole payment now to avoid any risk of non-payment in the future.

Other considerations to keep in mind

• Your eligible retiring allowance must be contributed to your RRSP in the year you received the allowance or within the first 60 days of the following tax year. If you don't contribute the retiring allowance to your RRSP before this deadline, your ability to make the contribution without using RRSP contribution room will be lost.

• Since your RRSP must mature by the end of the year you turn age 71, contributing your eligible retiring allowance to your RRSP is not possible in the year you turn 72 or older. If you have a younger spouse and have unused RRSP contribution room, you can contribute the retiring allowance to a spousal RRSP.

• Amounts you receive as a retiring allowance, whether eligible or non-eligible, are taxable to your estate income for the purpose of calculating your RRSP contribution limit for the following year.

• The retiring allowance you receive, whether contributed to an RRSP or not, may be used for charitable purposes.

• Employment Insurance (EI) benefits, if you qualify for them, and claimed as deduction for the contribution, you can't designate that contribution as a repayment under the home buyers' plan or lifelong learning plan.

Consider your options and plan accordingly

Careful planning can help maximize the use of your retiring allowance and may minimize the tax impact. Remember to consider your cash-flow needs (both immediate and long-term) and maintain flexibility, as your circumstances may change. Your RBC advisor can assist in determining your cash-flow and other financial needs while a qualified tax advisor can assist with your overall planning for your retiring allowance.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal or insurance advisor before acting on any of the information in this article.