RRIF payments and withdrawals

You can think of a registered retirement income fund (RRIF) as an extension of your registered retirement savings plan (RRSP). Your RRSP is used to save for your retirement while your RRIF is used to provide you with retirement income. This article focuses on the main considerations associated with receiving income from your RRIF, including calculating your minimum amount, as well as the withholding taxes on your RRIF withdrawals.

You can think of a registered retirement income fund (RRIF) as an extension of your registered retirement savings plan (RRSP). Your RRSP is used to save for your retirement while your RRIF is used to provide you with retirement income. This article focuses on the main considerations associated with receiving income from your RRIF, including calculating your minimum amount, as well as the withholding taxes on your RRIF withdrawals.

Family Office Services

August 14, 2023

RRIF payments and withdrawals

You can think of a registered retirement income fund (RRIF) as an extension of your registered retirement savings plan (RRSP). Your RRSP is used to save for your retirement while your RRIF is used to provide you with retirement income. One of the main benefits of a RRIF is that it provides you with flexibility in establishing an income stream during your retirement. Although you're generally required to withdraw a minimum amount from your RRIF each year, there's no maximum and you can make withdrawals as often as you wish. Another major advantage of a RRIF is the assets that remain in the plan continue to grow on a tax-deferred basis until you withdraw them. This article focuses on the main considerations associated with receiving income from your RRIF, including calculating your minimum amount, as well as the withholding taxes on your RRIF withdrawals. Any reference to a spouse in this article includes a common-law partner.

Establishing your RRIF

You can establish a RRIF by transferring amounts from an RRSP, a pooled retirement pension plan (PRPP), a registered pension plan (RPP), a specified pension plan (SPP) or from another RRIF. Generally, you cannot contribute to a RRIF.

Starting in the year after the year you establish a RRIF, you have to be paid an annual minimum amount. In other words, there's no minimum payment required in the calendar year in which you convert your RRSP to a RRIF. The minimum amount is calculated based on your age at the end of the previous year. If you have a spouse, you can elect to have the minimum amount calculated based on your spouse's age. If your spouse is younger than you, this will lower your required minimum payment. You must make this election when you first establish your RRIF. Once you make the election, you can't change it on that RRIF account at a later date, even if your spouse passes away.

If you have an existing RRIF, and want to make a new election to calculate your minimum amount based on either your or your spouse's age, you are able to transfer your existing RRIF assets to a new RRIF account and make a new election. Generally, when you transfer to a new RRIF in these circumstances, you must receive the minimum payment for the year from the existing RRIF account. The minimum amount cannot be transferred to the new RRIF.

Although there are various maturity options for your RRSP, where you've decided to transfer your RRSP property to a RRIF, you can do so at any time before the end of the calendar year in which you turn age 71. The investments held in your RRSP should be transferred directly into the RRIF account to avoid any tax consequences. You're generally not required to liquidate your RRSP investments prior to transferring your RRSP property to a RRIF.

In the case where you've transferred all or part of your RRSP property to a RRIF before age 71, you are able to transfer the value of your RRIF, in excess of the required annual minimum payment for the year, back to your RRSP. You may wish to do so, for example, if your financial circumstances change and you no longer want to receive a mandatory annual payment from your RRIF.

Receiving income from your RRIF

You can withdraw more, but not less, than the annual minimum amount. Any amount above the annual minimum amount that you withdraw from your RRIF in one year cannot be applied as part of your minimum amount for the next year. You can choose to give your RRIF payments monthly, quarterly, semi-annually or annually, depending on your income requirements. If you don't require income from your RRIF to meet your financial needs, you may consider receiving the annual minimum payment at the end of the year to maximize the tax-deferral benefits of your RRIF.

Calculating your RRIF minimum amount

Your RRIF minimum amount for each year, after the year your RRIF is established, is calculated by multiplying the fair market value (FMV) of your RRIF at the end of the previous year by a prescribed percentage factor. The prescribed percentage depends on your age or your spouse's age at the end of the previous year, depending on whose age you elected at the time the RRIF was established.

For ages under 71, the prescribed percentage factor is calculated by the following formula:

1/ (90 – age on December 31 of the previous year) x 100

For example, if the RRIF minimum amount is based on your age, and you are age 56 as of December 31 of the previous year, the prescribed percentage factor would be 1/ (90 – 56) x 100, or 2.94%. If the value of your RRIF at December 31 of the previous year is $500,000, then your required RRIF minimum payment for the year would be $14,700.

The amount you withdraw from your RRIF determines the rate of withholding tax that will apply to your withdrawal.

For ages 71 and over, the prescribed percentage factor is found in the tax regulations. As an example, if the RRIF is based on your age, and you are age 75 as of December 31 of the previous year, the prescribed percentage factor per the tax regulations would be 5.82%. If the value of your RRIF at December 31 of the previous year is $500,000, then your required RRIF minimum payment for the year would be $29,100. Please refer to the RRIF minimum table in the appendix to this article, for the prescribed percentage factors.

Taxes on RRIF income

Your RRIF withdrawals are included in your taxable income and are subject to tax at your marginal tax rate. Your total taxable income will determine your total taxes payable. However, there are certain cases (discussed in the next section) in which financial institutions are required to withhold taxes from your RRIF payments. These amounts withheld are remitted to the Canada Revenue Agency (CRA) on your behalf and are a credit towards your total taxes payable.

Withholding taxes

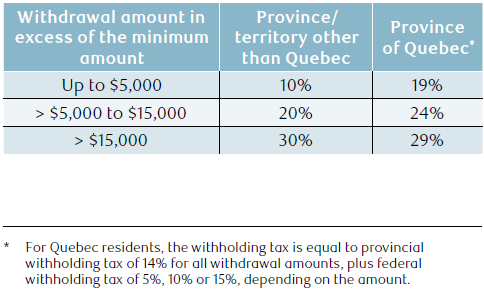

The amount you withdraw from your RRIF determines the rate of withholding tax that will apply to your withdrawal. There is no withholding tax applied to your required minimum payment from the RRIF. If you withdraw more than the required minimum payment, income tax will be withheld at source on the amount in excess of the minimum amount. The withholding tax rates for Canadian residents are the same for all provinces and territories except Quebec. Withholding tax for non-residents is discussed later in this article. The following table shows the percentage of withholding tax that applies to the amount in excess of the minimum amount when you make a single lump-sum withdrawal:

A series of payments

The withholding tax amount is generally based on the excess portion of each individual lump-sum payment, except where you make a series of pre-authorized smaller withdrawals. If you make a series of smaller withdrawals in instalments to fulfil a single request, the CRA has stated that the rate of withholding on each individual payment should be based on the total sum requested and not on each individual payment. In these situations, the CRA considers the series of payments to be blended payments (i.e. part minimum amount and part excess amount). Accordingly, the excess portion of each instalment would be subject to withholding tax at the rate that would apply had you requested to receive one lump-sum payment in the year rather than a series of payments.

For example, assume you're a resident of Saskatchewan and you decide to withdraw $600 every month from your RRIF ($7,200 on an annual basis) using a pre-authorized withdrawal program. Further, assume your annual minimum payment is $1,200. The sum of the amounts you plan to withdraw in the year in excess of the RRIF minimum is $6,000 ($7,200 – $1,200). As the total excess amount falls in the > $5,000 to $15,000 range, the portion of each individual payment that's in excess of the minimum will be subject to 20% withholding tax.

A series of payments with an additional separate request for funds

In a situation where you receive regular instalment payments and then submit a request for an additional amount during the year, the CRA will consider this to be a separate request and will only require tax to be withheld on the excess portion of that additional payment, regardless of the amount of your regular instalment payments. Building on the previous example, if you decided to withdraw an additional $4,000 as a lump-sum from your RRIF in June, this payment would be treated as a separate request. Since it's an excess amount above the minimum (already received in monthly instalments) but less than $5,000, it would be subject to a 10% withholding tax rate, and not the 20% withholding tax rate applied to the excess withdrawals in the previous example.

A series of separate requests

Despite what's mentioned in the previous section about the withholding tax rate on an additional separate request for funds, if it appears you're making a series of separate requests in order to minimize the withholding tax, the CRA's position is that the withholding tax rate should be determined as if there was one request equal to the total of all amounts requested; therefore, a higher withholding rate may apply. This could be the case where you make a series of requests within a short period of time. Continuing with the same example, assume that in addition to the $4,000 withdrawal in June, you request another $4,000 the next day. Because the requests are within a short period of time, the withholding tax rate should be determined as if there was one request equal to $8,000 rather than two separate requests. Since the entire $8,000 will be an excess amount above the minimum (already received in monthly instalments), it will be subject to a 20% withholding tax rate rather than each $4,000 withdrawal being subject to a 10% withholding tax rate.

Quarterly tax instalments

It is possible that the amount of withholding tax on your RRIF withdrawals may not be sufficient to cover your actual tax liability. This could contribute to you having to pay additional tax when you file your income tax return for the year. If your net tax owing (your total tax liability less all amounts withheld at source) for the current year and either one of the two immediately preceding years exceeds $3,000 ($1,800 in Quebec), you will be asked by the CRA to pay tax instalments in subsequent years.

Increasing your withholding tax

To minimize the possibility of having to make future quarterly tax instalments, you may request that a larger amount of tax be withheld on your RRIF withdrawals by completing CRA's Form TD1, Personal Tax Credits Return (TD1 Form). Quebec residents should also complete Form TP-1017-V, Request to Have Additional Income Tax Withheld at Source. The form(s) must be completed and provided to your financial institution.

Reducing your withholding tax

There may be situations where the required amount of tax withheld on your RRIF payments would be more than sufficient to cover your final tax liability. This may be the case where your RRIF withdrawals are subject to the highest rate of withholding tax and those payments make up most of your income for the year.

In order to reduce or waive the withholding tax, your financial institution may require you to provide them with either a completed TD1 Form or authorization from the CRA. To obtain approval from the CRA, you will need to send the CRA a completed Form T1213, Request to Reduce Tax Deductions at Source. Quebec residents must use Form TP-1016, Application for a Reduction in Source Deductions of Income Tax, to request reduced withholding tax from Revenu Québec.

Tax reporting slips

All amounts that are paid out of your RRIF in a calendar year are reported to you on a T4RIF. This tax slip is issued by the end of February of the calendar year following the year of withdrawal. The T4RIF reports the gross income paid out to you, as well as any federal and provincial taxes (with the exception of Quebec) that have been withheld and remitted to the government. For Quebec residents, the T4RIF will show the gross income and only the federal withholding tax. This is because residents of Quebec also receive a Relevé 2 slip for provincial income tax purposes. The Relevé 2 reports the gross income withdrawn from the RRIF, as well as the Quebec withholding tax.

Spousal RRIFs and income attribution

RRIF minimum payments aren't subject to the income attribution rules, so if you withdraw only the minimum amount from a spousal RRIF, no income will be attributed to the contributing spouse. Keep in mind that in the year you establish the RRIF, the required minimum payment is zero. If you withdraw more than the minimum payment from your spousal RRIF, the excess will attribute back to the contributing spouse, to the extent there were any spousal RRSP contributions made in the year of the withdrawal or the two previous calendar years. Please refer to the article on spousal RRSPs and RRIFs for an example on how the income attribution rules apply when you make a withdrawal from a spousal RRIF.

RRIF transfers

In-kind withdrawals

It may be possible to take a RRIF payment by transferring investments in-kind from your RRIF directly into your non-registered account. Check with your RRIF plan administrator to verify that in-kind withdrawals are permitted. If you make an in-kind withdrawal, and the withdrawal exceeds the minimum amount, you must pay the withholding tax on the excess amount. The withholding tax is calculated based on the amount of your in-kind withdrawal that exceeds the minimum amount. There must be sufficient cash available in the RRIF to cover the withholding tax, so you may have to sell a portion of the investments to satisfy the withholding tax requirement.

The amount of your RRIF withdrawal will equal the FMV of the investments at the time of the transfer plus any cash used to cover withholding tax, if applicable. The FMV of the investments at the time of the transfer will also become the new adjusted cost base of those transferred securities.

Switching financial institutions

If you're transferring all of your RRIF assets from one financial institution to another, the transferring financial institution is generally required to pay you your annual minimum before transferring your RRIF. For example, if your annual minimum payment is $8,000 and you have only withdrawn $1,000 from your RRIF to date, the transferring financial institution will pay you $7,000 before transferring your remaining RRIF balance.

Separation or divorce

Where RRIF property is transferred from your RRIF to your current or former spouse's RRIF under a decree, court order, or written separation agreement relating to a division of property resulting from the breakdown of your marriage or common-law partnership, the property can be transferred on a tax-deferred basis. These transfers have to be done as a direct transfer from your RRIF to your current or former spouse's RRIF using CRA Form T2220, Transfer from an RRSP, RRIF, PRPP or SPP to Another RRSP, RRIF, PRPP or SPP on Breakdown of Marriage or Common-law Partnership.

Your financial institution is not required to retain or pay out the minimum amount to you before the transfer. A full or partial minimum payment would only be required if there are remaining funds in the RRIF after the transfer. In this case, the transferring financial institution must pay you the lesser of the minimum amount or the FMV of your RRIF's remaining property after the transfer.

The attribution rules previously mentioned for spousal RRIFs will not apply where you are divorced or living separate and apart from your spouse because of a breakdown of your marriage or common-law partnership.

Pension income splitting

If you are age 65 or over during the year and receive RRIF income, you can split up to 50% of this income with your spouse. By reallocating a portion of your RRIF income to your lower-income spouse, the income will be taxed in their hands at their lower marginal tax rate and reduce your family's overall tax bill. Further, by reallocating your RRIF income, you may also avoid having your old age security (OAS) or other income-tested government benefits reduced.

To split RRIF income, you and your spouse have to make a joint election on CRA Form T1032, Joint Election to Split Pension Income. The form must be signed and attached to both your and your spouse's income tax returns.

When you allocate RRIF income that was subject to withholding tax to your spouse, a proportionate amount of the withholding tax is also allocated to your spouse.

Pension income tax credit

If you are age 65 or over during the year and received RRIF income, you may be eligible for a federal pension income tax credit of up to $2,000. If your spouse is also age eligible pension income but your spouse is not, you may wish to allocate $2,000 of your pension income to your spouse. This will allow both you and your spouse to claim the pension income tax credit. If your spouse is also age 65 or over, if your spouse does not need to claim all of the credit in order to reduce their federal taxes to zero, they may transfer any unused amount to you, for you to claim on your tax return.

Non-residents of Canada

If you're a non-resident of Canada, generally a withholding tax of 25% applies to your RRIF payments, even if you only receive the minimum amount. The rate of withholding tax that applies may be lower if Canada has a tax treaty with the country where you are resident. For non-residents of Canada, you may have a tax treaty with Canada, including the United States, withdrawals from a RRIF are subject to a 15% non-resident withholding tax, provided payments are considered periodic pension payments. A RRIF withdrawal would be considered a periodic pension payment if the total payments made during the calendar year do not exceed the greater of:

- Twice the RRIF minimum amount for the year; or

- 10% of the FMV at the beginning of the year.

For calculating the periodic pension payment, where property or funds are transferred to a RRIF in a particular year, both the minimum amount and the FMV of the RRIF are determined on the assumption that the transfer took place immediately before the beginning of the particular year. This is so that, for this purpose, in the year the RRIF is established, the minimum amount is not NIL. In calculating twice the RRIF minimum amount and 10% of the FMV in the first year, the FMV at the time of the transfer to the RRIF is used.

A notable withholding tax exception is periodic pension payments made to residents of the United Kingdom (UK) based on the Canada-UK Tax Treaty. The treaty eliminates the condition non-resident withholding tax applies for periodic pension payments made to residents of the UK. RRIF payments and taxes withheld are reported to non-residents on an N44 slip.

Conclusion

A RRIF provides you with continued tax-deferred growth and flexibility in planning for your retirement. Ensuring you have a good understanding of how RRIF withdrawals work will allow you to better plan for your retirement cash flow. You should reach out to your RRIF advisor if you have questions on any of the topics discussed in this article.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide tax, legal, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal, or insurance advisor before acting on any of the information in this article.