RRSP deduction limit and available contribution room statement

Shortly after you've filed your 2025 tax return, you should have received a Notice of Assessment (NOA) from the Canada Revenue Agency (CRA). Here's an overview of the registered retirement savings plan (RRSP) deduction limit and available contribution room statement on your NOA to help you determine the amount you can contribute, how much you can deduct on your income tax return and whether you're in an over-contribution position.

Shortly after you've filed your 2025 tax return, you should have received a Notice of Assessment (NOA) from the Canada Revenue Agency (CRA). Here's an overview of the registered retirement savings plan (RRSP) deduction limit and available contribution room statement on your NOA to help you determine the amount you can contribute, how much you can deduct on your income tax return and whether you're in an over-contribution position.

Family Office Services

January 14, 2026

RRSP deduction limit and available contribution room statement

Shortly after you've filed your 2024 tax return, you should have received a Notice of Assessment (NOA) from the Canada Revenue Agency (CRA). Here's an overview of the registered retirement savings plan (RRSP) deduction limit and available contribution room statement ("statement") on your NOA to help you determine the amount you can contribute, how much you can deduct on your income tax return and whether you're in an over-contribution position.

Keep in mind that while this article focuses on your RRSP, your RRSP deduction limit also shows the maximum amount that you and/or your employer may contribute to a Pooled Registered Pension Plan (PRPP), or a Voluntary Retirement Savings Plan (VRSP) in Quebec, for the year. All PRPP or VRSP contributions by you and/or your employer will reduce your RRSP contribution room for the year.

The RRSP deduction limit and available contribution room statement

The following is a sample of an RRSP deduction limit and available contribution room statement:

References to RRSP contributions also include contributions to your pooled registered pension plan (PRPP) and to your and your spouse's or common-law partner's specified pension plan (SPP). For more information, go to canada.ca/rrsp or see Guide T4040, RRSPs and Other Registered Pension Plans for Retirement.

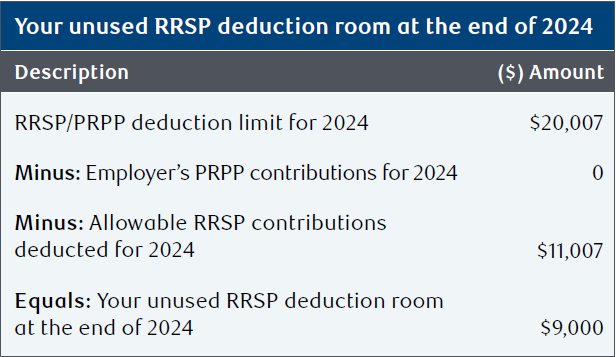

Your unused RRSP deduction room at the end of 2024

The sample statement shows the calculation of your unused RRSP deduction room at the end of 2024:

- RRSP/PRPP deduction limit for 2024: $20,007

- Minus: Employer's PRPP contributions for 2024: $0

- Minus: Allowable RRSP contributions deducted for 2024: $11,007

- Equals: Your unused RRSP deduction room at the end of 2024: $9,000

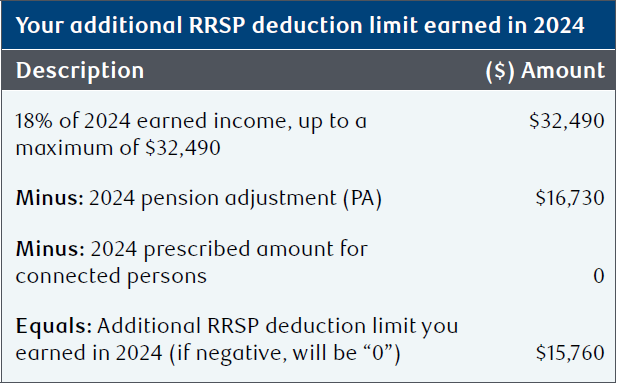

Your additional RRSP deduction limit earned in 2024

The sample statement shows the calculation of your additional RRSP deduction limit earned in 2024:

- 18% of 2024 earned income, up to a maximum of $32,490: $32,490

- Minus: 2024 pension adjustment (PA): $16,730

- Minus: 2024 prescribed amount for connected persons: $0

- Equals: Additional RRSP deduction limit you earned in 2024 (if negative, will be "0"): $15,760

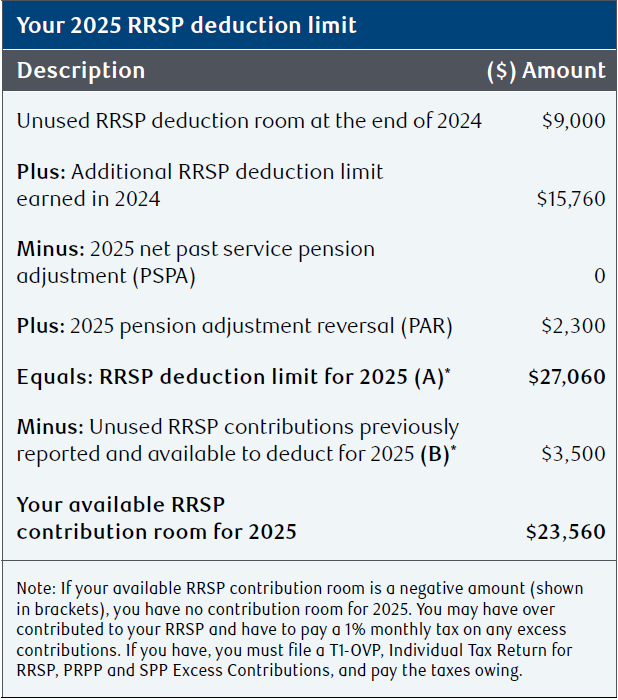

Your 2025 RRSP deduction limit

The sample statement shows the calculation of your 2025 RRSP deduction limit:

- Unused RRSP deduction room at the end of 2024: $9,000

- Plus: Additional RRSP deduction limit earned in 2024: $15,760

- Minus: 2025 net past service pension adjustment (PSPA): $0

- Plus: 2025 pension adjustment reversal (PAR): $2,300

- Equals: RRSP deduction limit for 2025 (A): $27,060

- Minus: Unused RRSP contributions previously reported and available to deduct for 2025 (B): $3,500

- Your available RRSP contribution room for 2025: $23,560

Note: If your available RRSP contribution room is a negative amount (shown in brackets), you have no contribution room for 2025. You may have over contributed to your RRSP and have to pay a 7% monthly tax on any excess contributions. If you have, you must file a T1-OVP, Individual Tax Return for RRSP, PRPP and SPF Excess Contributions, and pay the taxes owing.

Please note that the letters (A) and (B) are not actually shown on your statement but have been included in this sample for ease of reference and to provide continuity with past statements.

How much can I contribute to my RRSP?

The maximum amount you can contribute to your RRSP without triggering penalty tax is equal to (A) – (B) + $2,000 where:

- (A) is your RRSP deduction limit for 2025;

- (B) is your unused RRSP contributions; and

- $2,000 is the cumulative lifetime allowable amount of over-contribution you can make without being subject to penalty tax.

Using the information from the sample statement, you may contribute $25,560 ($27,060 – $3,500 + $2,000) to your own RRSP or to a spousal RRSP without triggering penalty tax. If you would like to deduct the contribution on your 2025 tax return, the contribution needs to be made by the 2025 RRSP deadline of March 2, 2026.

Consider contributing to your RRSP early in the year. By contributing early, your RRSP assets will have more time to benefit from tax-deferred compound growth.

Your RRSP contribution room will be reduced by certain pension transactions calculated by your employer. For example:

- If you or your employer contributes to a registered pension plan or your employer contributes to a deferred profit-sharing plan, your employer will report a PA on your T4 slip for the benefits accruing to you under the plan(s). If your employer reported a PA on your 2024 T4 slip, your 2025 RRSP room will be reduced.

- If you purchased past years of pension service or your benefits relating to a previous period of pensionable service are improved, a PSRA is reported to you. If your employer or pension administrator issued you a PSRA in 2025, your 2025 RRSP room will be reduced.

On the other hand, your RRSP contribution room will be increased by any PARs calculated by your employer. For example:

- If you received the commuted value from a defined benefit pension plan, you may have a PAR. A PAR restores your RRSP deduction limit if the amount received from the plan is less than the total PAs and PSPARs that were previously reported to you. If your employer or pension plan administrator issued you a PAR in 2025, your RRSP contribution room for 2025 will increase.

It's important to note that your RRSP deduction limit for 2025 may not be the same amount as your available RRSP contribution room for 2025. This is the case in the example previously shown.

How much can I deduct on my tax return?

The amount of RRSP contributions you can deduct for 2025 is your 2025 RRSP deduction limit, which is the amount next to the letter (A) in the sample statement. The CRA determines your 2025 limit using information from your 2024 tax return, plus any unused RRSP contribution room carried forward from previous years.

Your RRSP deduction limit is calculated in part by determining your earned income. Earned income includes net income from employment, business and rentals, as well as other income, such as alimony received, but it doesn't include portfolio investment income.

Have I over-contributed to my RRSP?

In order to determine if you've over-contributed to your RRSP, you'll need to account for the amount next to the letter (B) (as shown on the earlier sample statement) on your statement. This amount represents your unused contributions, which are also known as undeducted contributions. Unused contributions are RRSP contributions you made in previous years, or in the first 60 days of the current year, that were not deducted on a prior year income tax return. Based on the information from the sample statement, you made $3,500 of RRSP contributions in previous years that you did not deduct for income tax purposes.

You may have chosen not to deduct these contributions because your taxable income was low in the previous year(s) or you expected your income to rise significantly in a future year(s). It's also possible that you didn't deduct these contributions because you didn't have sufficient RRSP deduction room.

Note that any RRSP contributions you made during the first 60 days of 2025 (i.e. on or before March 3, 2025) should have been reported on Schedule 7 of your 2024 income tax and benefit return, even if you didn't deduct them. If you didn't deduct them, the CRA will report these as unused RRSP contributions (next to where the letter (B) is on the sample statement) on your 2025 RRSP deduction limit statement. Any amounts contributed to your RRSP after March 3, 2025 will not be reflected in your 2025 statement.

The relationship of amount (B) to amount (A) will determine if you have an RRSP over-contribution. This relationship can be classified in one of the following three ways:

1) If (B) – (A) is less than or equal to $0, you have not over-contributed to your RRSP. This means you still have additional room to make contributions to your RRSP. This additional room is equal to (A) – (B) + $2,000.

2) If (B) – (A) is greater than $0 but less than $2,000, you're within the allowable over-contribution limit. You are allowed to over-contribute a cumulative lifetime total of $2,000 to your RRSP without incurring a penalty tax. This limit is designed to provide a buffer in case of accidental over-contributions. You can use the $2,000 over-contribution to have your funds grow on a tax-deferred basis in the RRSP, but keep in mind that the additional over-contribution amount will not be deductible.

As you get closer to retirement, make sure that you eventually claim the $2,000 as part of your RRSP contribution deductions to avoid double taxation. The double taxation occurs because you must include the amount in income and may pay tax on the amount when you withdraw it, even though the amount was not deductible when you contributed it. This is important to consider when determining the amount you should contribute to your RRSP when you're nearing retirement.

3) If (B) – (A) is greater than $2,000, you have over-contributed to your RRSP and may be accruing a penalty. Generally, over-contributions in excess of $2,000 are subject to a 1% per month over-contribution tax calculated from the month you first exceeded your contribution limit. The tax will continue to apply until the month you remove the excess or until new contribution room that's sufficient to absorb the over-contribution may become available to you on January 1 of the following year.

If you're in an over-contribution position in excess of $2,000 in any year, you are required to file a T1-OVP, Individual Tax Return for RRSP Excess Contributions. This return is used to calculate the penalty you owe. You are required to pay the penalty and submit the completed return to your tax centre no later than 90 days after the end of the year. If you're in an over-contribution position, you should notify a tax advisor to discuss your options and ensure that the T1-OVP is completed and submitted in a timely fashion.

What if I can't find my NOA?

If you're unable to locate your NOA, you can determine your RRSP contribution room by contacting the CRA directly by phone, using the MyCRA mobile app or visiting the "My Account" page of the Government of Canada website.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.