Saving for the purchase of your home

As the cost of owning a home continues to rise, many are prioritizing saving funds to purchase a home. With the availability of the tax-free first home savings account (FHSA) and tax-free savings account (TFSA), as well as the ability to participate in the home buyers' plan (HBP), which allows you to withdraw from your registered retirement savings plan (RRSP) to buy or build a home, you might be wondering which option is best to help you save funds for the purchase of your home. This article summarizes the key features of each savings vehicle and provides a discussion on which option, or combinations of options, may be most suitable for you, based on your circumstances.

As the cost of owning a home continues to rise, many are prioritizing saving funds to purchase a home. With the availability of the tax-free first home savings account (FHSA) and tax-free savings account (TFSA), as well as the ability to participate in the home buyers' plan (HBP), which allows you to withdraw from your registered retirement savings plan (RRSP) to buy or build a home, you might be wondering which option is best to help you save funds for the purchase of your home. This article summarizes the key features of each savings vehicle and provides a discussion on which option, or combinations of options, may be most suitable for you, based on your circumstances.

Family Office Services

January 14, 2026

Saving for the Purchase of Your Home

As the cost of owning a home continues to rise, many are prioritizing saving funds to purchase a home. With the availability of the tax-free first home savings account (FHSA) and tax-free savings account (TFSA), as well as the ability to participate in the home buyers' plan (HBP), which allows you to withdraw from your registered retirement savings plan (RRSP) to buy or build a home, you might be wondering which option is best to help you save funds for the purchase of your home. This article summarizes the key features of each savings vehicle and provides a discussion on which option, or combinations of options, may be most suitable for you, based on your circumstances. Any reference to a spouse in this article also includes a common-law partner.

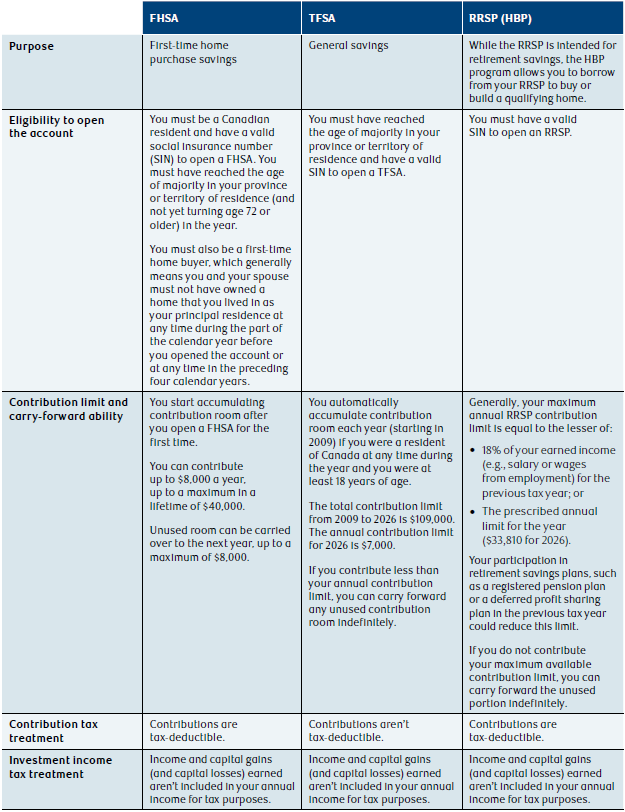

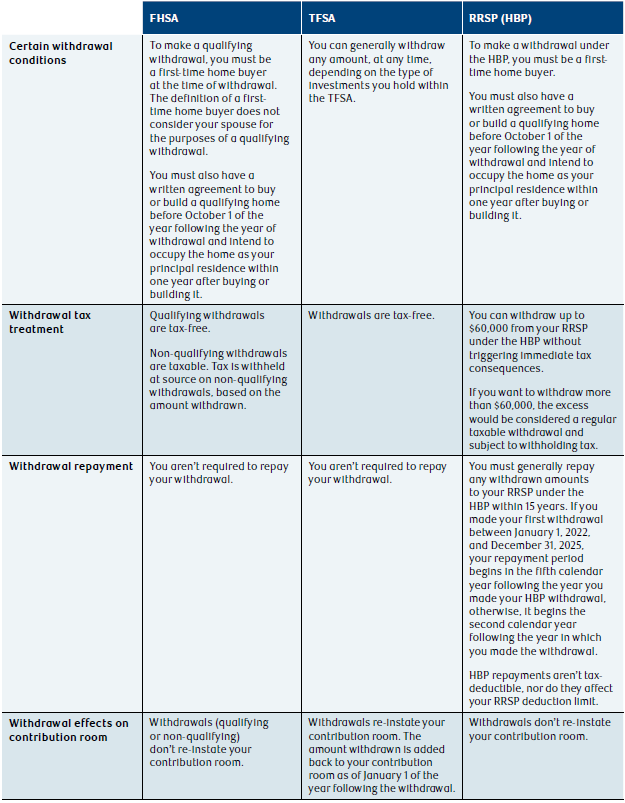

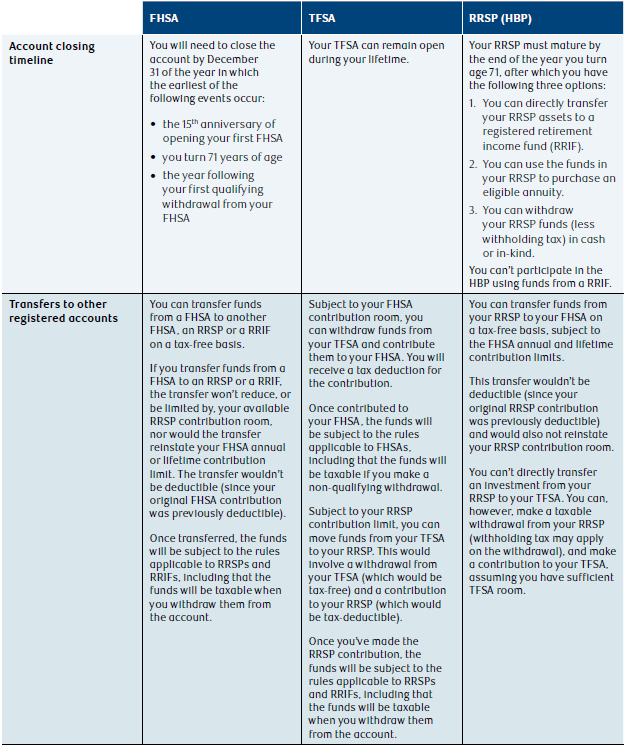

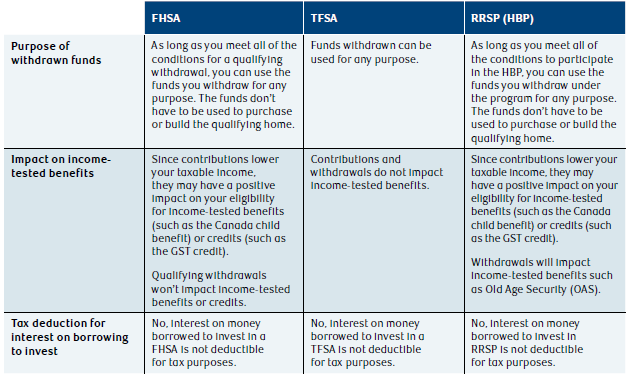

Comparing the FHSA, TFSA and RRSP

Evaluating Your Options

Determining which account would best help you save towards purchasing a home depends on your own specific circumstances — there is no single or absolute answer. Instead, there are many considerations that may make a particular savings vehicle more suitable for you.

The FHSA

If you plan on purchasing your first home in the near future, you may want to open a FHSA and start accumulating room. The FHSA has many advantages, as it combines the attractive features of both the RRSP and the TFSA. The earlier you're able to open the account, the longer you have to take advantage of the 15-year limit for tax-free growth. If you can't contribute the full $8,000 of annual contribution room this year, you carry contribution room, up to a maximum of $8,000, will carry forward and you can contribute up to your available room in the following year. Further, if you expect to be in a high marginal tax bracket for the next few years, the FHSA is particularly tax-efficient because it allows for a tax deduction on your contributions as well as tax-free growth and qualifying withdrawals.

Since undeducted FHSA contributions can be carried forward indefinitely, if you have relatively low income this year and expect to have higher income in the next few years (perhaps you're just starting out in your career), you can contribute to your FHSA this year and wait to claim the tax deduction in a future year when you have higher income. With this approach, you gain access to tax-free growth immediately and you also get to benefit more from a tax deduction in a later year when you're paying tax at higher marginal income tax rates.

Although the same carryforward rules apply for undeducted RRSP contributions, it may make sense to first start contributing to your FHSA, as opposed to your RRSP. This is because if you don't end up buying a home within 15 years, you have the flexibility of transferring the funds accumulated in your FHSA to your RRSP, where you can later make a withdrawal under the HBP. This transfer won't reduce your available RRSP room; therefore, you can create more RRSP room by first contributing to your FHSA. On the other hand, if you start by contributing to an RRSP and then transfer the funds into your FHSA (which you're allowed to do), you don't get an additional deduction and you will have lost that RRSP room.

The RRSP

If you're in a high marginal tax bracket, you may want to consider contributing to the RRSP, as it may allow for larger tax-deductible contributions (based on your RRSP contribution room) and therefore provide you with access to a larger amount that can be withdrawn (up to $60,000) than from a FHSA in the early years of the FHSA program.

Keep in mind that by participating in the HBP through your RRSP, you're essentially borrowing money (interest-free) from your own RRSP, as you do have to repay the funds to your RRSP within 15 years. You may pay those funds at your marginal tax rate eventually when you make a regular withdrawal.

The TFSA

If you're not considered a first-time home buyer and therefore aren't eligible to open a FHSA or participate in the HBP program, you may still be able to open a TFSA to save for your home. If you're considered a first-time home buyer, you can also use the TFSA to supplement a FHSA and/or HBP withdrawal. The TFSA is designed to help you meet a wide range of financial goals, as it offers tax-free growth and enhanced flexibility. You can contribute to a TFSA at any time, as long as you have contribution room. You can also withdraw from a TFSA at any time, for whatever purpose, and the amount of the withdrawals can be added back to your contribution room for the following year. There are no income restrictions for contributing to a TFSA, meaning that regardless of your income level or type of income, you can contribute to a TFSA. As such, the TFSA can be an attractive option if you're in a lower income tax bracket and looking to save for the purchase of your home.

The Interplay

If you have enough funds to be able to contribute to all three accounts, and assuming you meet the eligibility criteria to open and contribute to all of these accounts, you are able to use all of them in conjunction with each other. You can save in all three accounts and make a FHSA, using HBP, and a TFSA withdrawal for the same qualifying home purchase.

Alternatively, if you don't currently have the cash flow but you have already saved funds in a TFSA and anticipate purchasing a home within the next few years, you may want to consider withdrawing funds from your TFSA and contributing them into your FHSA in order to receive a tax-deduction (either now or in a future year).

Conclusion

If you're thinking of buying a home in the near future, it's important to be aware of the options available to help you save for this major purchase. The more you know about these options, the better informed you'll be able to make about the right savings vehicle for you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly reviewed, you should always act on your own advice. If you are unsure of the advice that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal or insurance advisor before acting on any of the information in this article.