Spousal RRSP and RRIF

A registered retirement savings plan (RRSP) is a powerful retirement planning tool. In some cases, setting up a spousal RRSP can provide additional advantages. This article provides an overview of spousal RRSPs and includes a discussion of some of the potential benefits and considerations of such RRSPs.

A registered retirement savings plan (RRSP) is a powerful retirement planning tool. In some cases, setting up a spousal RRSP can provide additional advantages. This article provides an overview of spousal RRSPs and includes a discussion of some of the potential benefits and considerations of such RRSPs.

Family Office Services

July 14, 2024

Spousal RRSP and RRIF

A registered retirement savings plan (RRSP) is a powerful retirement planning tool. In some cases, setting up a spousal RRSP can provide additional advantages. This article provides an overview of spousal RRSPs and includes a discussion of some of the potential benefits and considerations of such RRSPs. Any reference to spouse in this article also includes a common-law partner.

What is a spousal RRSP?

With a regular RRSP, you contribute to a plan registered in your own name. You are both the annuitant and the contributor. A spousal RRSP is a plan where you are the plan annuitant and your spouse can make contributions to the plan. Some financial institutions offer spousal RRSPs where you are the annuitant, but both you and your spouse can make contributions. This may allow for easier administration and reduction of administrative costs.

Any RRSP that you are the annuitant of (including spousal RRSPs) must mature by December 31 of the year you turn 71. Before that time, you must either transfer your RRSP to a registered retirement income fund (RRIF), use the funds to purchase an eligible annuity or withdraw your RRSP funds in cash or in-kind. When you convert your spousal RRSP to a RRIF, the RRIF is considered a spousal RRIF.

How much can you contribute to a spousal RRSP?

To contribute to a regular RRSP or a spousal RRSP, you must have sufficient unused contribution room. Contributions you make to a regular RRSP or a spousal RRSP reduce your RRSP contribution room. In other words, even when you make a spousal contribution, it affects your own RRSP contribution room, not the annuitant's.

When you contribute to a spousal RRSP, the tax receipt should identify you as the contributor and your spouse as the annuitant of the RRSP. You can claim a deduction on your income tax return when you make contributions to either your own RRSP or a spousal RRSP. The total amount of RRSP contributions you can deduct cannot be more than your RRSP deduction limit for the year.

Potential benefits of a spousal RRSP

If you're deciding between contributing to your own RRSP or a spousal RRSP, some factors to consider include your tax brackets both now and in retirement, your spouse's tax brackets, and the difference in your ages. Taking these factors into consideration, here are a few common situations where a family may benefit from having a spousal RRSP.

Income splitting

A spousal RRSP may enable your family to split income. Income splitting takes advantage of Canada's progressive tax system where, as your taxable income increases, your marginal tax rate increases. You may be able to reduce your family's overall tax bill by shifting income from the higher-income spouse to the lower-income spouse.

By contributing to a lower-income spouse's RRSP, the contributor, who is typically the higher-income earner, can deduct the contribution at their higher marginal tax rate and the lower-income spouse will likely pay tax at a lower marginal tax rate when they withdraw from the spousal RRSP or RRIF. Please keep in mind that the income attribution rules (discussed later in this article) may affect this strategy.

Pension income splitting

If you or your spouse receives eligible pension income during the year, you and your spouse may split or allocate the eligible pension income for tax purposes. RRIF income is considered eligible pension income if you are at least age 65 in the year you receive it.

Given that there are these income splitting provisions, you may be wondering whether it still makes sense to contribute to a spousal RRSP. The following are some of the reasons a spousal RRSP may still be useful, even with the pension income splitting rules in place.

Enhanced income splitting

Under the pension income splitting provisions, up to 50% of eligible pension income can be allocated to a spouse. But there are cases where a couple cannot achieve the optimum tax result from splitting income through these provisions alone. For example, if a higher-income spouse has a significant amount of non-registered investment income, this income is not considered eligible pension income and cannot be split under these provisions. If this higher-income spouse had only made regular contributions to their own RRSP, in retirement they will only be able to allocate up to 50% of their RRIF income, and not their non-registered income, to their lower-income spouse. This allocation alone may not be sufficient to equalize the couple's total taxable income.

If, instead, the higher-income spouse had made regular contributions to a spousal RRSP, the lower-income spouse would have the option of withdrawing funds from the spousal RRSP or RRIF in retirement, which may help to equalize their incomes. This allows the higher-income spouse to pay tax on their non-registered investment income and the lower-income spouse to pay tax on the spousal RRSP or RRIF withdrawals.

Income splitting before age 65

If you and your spouse retire before age 65 and you need to withdraw from your RRSP or RRIF to supplement your retirement income, it may be beneficial to withdraw from a spousal RRSP or RRIF owned by the lower-income spouse. This is because you cannot split RRIF income before the RRIF annuitant reaches age 65 and you cannot split RRSP income at all. If all the RRSP or RRIF assets are in the higher-income spouse's name, any withdrawals they make before age 65 will be taxed in their hands at their higher marginal tax rate.

Low-income years

You don't have to use a spousal RRSP solely for retirement purposes. You may be able to use a spousal RRSP to pay for expenses during a period of low earnings. This may happen before retirement, for example, during a sabbatical, a period of unemployment or parental leave.

Generally, contributing to a spousal RRSP in these cases will make sense if the value of the RRSP deduction in the contributor's hands is greater than the taxes the RRSP annuitant will pay on the withdrawal. Of course, you'll also need to consider how the income attribution rules (discussed later) will affect withdrawals you make using this strategy. Lastly, remember that when you withdraw funds from an RRSP, you're losing the benefit of continued tax-deferred growth.

Participating in the HBP and LLP

To participate in the home buyers' plan (HBP) or lifelong learning plan (LLP), you must be an annuitant of an RRSP. If only one spouse in your family earns income that generates RRSP contribution room, setting up a spousal RRSP can allow both of you to potentially participate in the HBP and/or LLP programs.

Making contributions past age 71

If you've reached the year in which you turn 72, you cannot contribute to your own RRSP even if you have unused RRSP contribution room. However, if you have a spouse who has not yet reached the year in which they turn 72, you can make RRSP contributions to a spousal RRSP if you have unused RRSP contribution room.

Making contributions after death

You cannot make contributions to a deceased individual's RRSP. If the deceased person has unused RRSP contribution room, their legal representative can arrange for a contribution to be made to a spousal RRSP where the surviving spouse is the annuitant. This contribution can be done in the year of death or during the first 60 days after the end of that year if the surviving spouse is under age 72. The contributions can be claimed on the deceased individual's final tax return.

Spousal RRSP or RRIF attribution

When attribution applies, income that's normally taxed in the hands of one person is instead taxed in the hands of another. The income is not actually paid to the other individual.

Generally, when you withdraw funds from your RRSP or RRIF (including your spousal RRSP or RRIF), you're subject to tax on the withdrawal. But if you withdraw from a spousal RRSP or RRIF and the attribution rules apply, some or all of the withdrawal will instead be taxed in the contributor's hands.

When attribution applies

Attribution may apply when:

• The plan annuitant's spouse has contributed in the year of the withdrawal; or

• The plan annuitant's spouse has contributed in one of the two taxation years immediately preceding the withdrawal.

The amount of the RRSP withdrawal that's subject to attribution is limited to the total amount of spousal RRSP contributions made during the three-year period described above. For example, assume Bob contributes $3,000 in each of years 1, 2 and 3 (totalling $9,000) to Debbie's spousal RRSP. Debbie then withdraws $10,000 from her spousal RRSP in year 3. In this case, $9,000 will attribute back to Bob, while the remaining $1,000 will be taxable to Debbie.

If multiple spousal RRSP contributions have been made during the three-year period, there is an ordering rule that helps determine how the contributions are attributed. This rule provides that contributions are included in income in the same order they were made (if the contributions have not already been previously attributed to the contributor). Revisiting the same example, if Debbie instead only withdrew $5,000 in year 3, the ordering rule provides that $3,000 of Bob's contribution from year 1 and $2,000 of Bob's contribution from year 2 will be attributed to Bob.

RRIF withdrawals and attribution

RRIF minimum payments are not subject to the attribution rules. Any withdrawal made from a spousal RRIF in excess of the minimum RRIF withdrawal is attributed to the contributor, to the extent of any spousal RRSP contributions made in the year of withdrawal or in the two previous years.

Keep in mind that in the first year of converting an RRSP to a RRIF, there is no minimum payment. You may want to take this into account in deciding when to convert your spousal RRSP to a RRIF.

Spousal RRIF withdrawals that are attributed to the contributor are not considered eligible pension income for the purpose of pension income splitting. This means the attributed amounts will be fully taxed in the hands in the contributor, even if the contributor is age 65 or older.

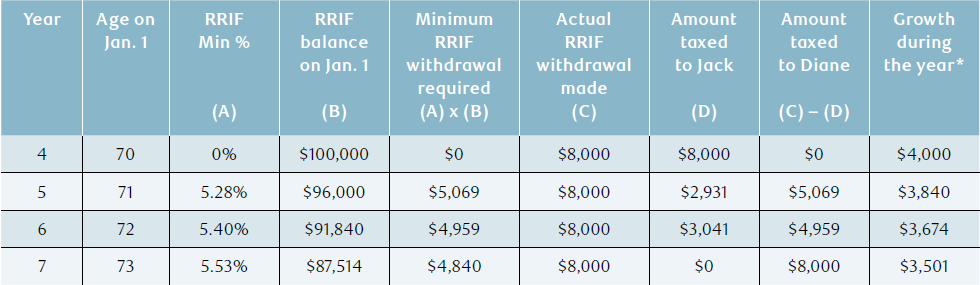

The following example illustrates the application of the attribution rules in the case of a spousal RRIF. Let's assume Jack contributes to a spousal RRSP for his spouse, Diane, in years 1, 2, 3 and 4, in the amount of $5,000 each year. Diane turns 71 in year 4 and she decides to convert her $100,000 spousal RRSP into a spousal RRIF that year. After converting, she withdraws $8,000 from the spousal RRIF on December 15, every year from year 4 to year 7. The following table outlines how attribution works in relation to the RRIF withdrawals:

Note that attribution will not apply to spousal RRIF withdrawals, regardless of the amount withdrawn, beginning in year 7. This is because Jack cannot make spousal contributions after the end of the year in which Diane, the RRSP annuitant, turns 71. So, withdrawals made in year 7 and later won't be taxed in Jack's hands since three years have passed since the last spousal contribution.

Exceptions to the attribution rules

In addition to the RRIF minimum payment, the attribution rules for spousal RRSPs/RRIFs don't apply in the following circumstances:

- Withdrawals made during and after the year of death of the contributing spouse;

- When an amount from the spousal RRSP/RRIF is deemed to have been received by the annuitant because of the annuitant's death;

- Withdrawals made when either spouse is a non-resident of Canada;

- Withdrawals made when the spouses are living separate and apart due to relationship breakdown;

- A withdrawal that is a commutation payment (this is generally a lump-sum payment from your RRSP annuity that's equal to the current value of your future annuity payments from the plan) transferred directly from the plan to another RRSP, to a RRIF, or to an issuer to buy an eligible annuity you cannot cash in for at least three years.

- Withdrawals made under the HBP or LLP. It is the annuitant's responsibility to make the minimum repayments required under these plans. If the annuitant does not make the required repayment, the repayment amount is taxable to the annuitant, regardless of any recent spousal RRSP contributions; and

- If you transfer an amount from your spousal RRSP directly to a defined benefit pension plan of which you are a member to buyback past service.

Commingling a spousal RRSP with a regular RRSP

If you combine a spousal RRSP and a regular RRSP, the combined account will be identified as a spousal RRSP. The same applies to combining spousal RRIFs with regular RRIFs. The attribution rules apply if the annuitant withdrawals from a spousal RRSP or withdrawals more than the minimum from a spousal RRIF and the contributing spouse has contributed in the year of the withdrawal or in either of the two immediately preceding taxation years. The attribution rules apply even if the annuitant has also made contributions to the RRSP. The spousal contributions are considered to have been withdrawn first.

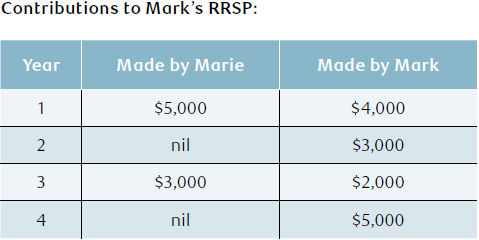

In the following example, Mark contributes to his RRSP in years 1, 2, 3 and 4. His spouse, Marie, makes spousal RRSP contributions to his plan in years 1 and 3.

In year 5, Mark wishes to withdraw $9,000 from his RRSP. Since both Marie and Mark have made contributions to the account, $3,000 of the $9,000 withdrawal will attribute back to Marie. To prevent this, Mark could wait until year 6 to make the withdrawal, assuming Marie does not make any more spousal RRSP contributions. Alternatively, if Mark and Marie each contribute to separate accounts (Mark to his own RRSP and Marie to a spousal RRSP for Mark), the attribution rules will not apply if Mark withdrawals from his own RRSP.

If you have a regular RRSP and are thinking of setting up a separate spousal RRSP to receive spousal contributions, consider any additional costs that may result from having more than one RRSP.

More than one spousal plan

If you have more than one spousal RRSP, the attribution rules will still apply if you withdraw from one of your spousal RRSPs and a spousal RRSP contribution is made to another spousal RRSP in the year of the withdrawal or either of the two immediately preceding tax years. This means even if you withdraw from a specific spousal RRSP that would normally not be subject to attribution, the attribution rules may apply if you hold another spousal RRSP with recent spousal RRSP contributions.

If you have a regular RRSP that's not a spousal plan, you can withdraw from that plan without triggering the attribution rules, even if you hold a spousal RRSP where spousal contributions have been made in the year of withdrawal or either of the two immediately preceding tax years.

Tax reporting when attribution applies

When you're the plan annuitant and withdraw from your spousal RRSP/RRIF, a tax slip is issued to you even when attribution applies. You will need to calculate the amount of income that's subject to attribution and properly report the income on your and your spouse's tax returns.

The taxes withheld on the withdrawal are also reported on this tax slip. Only you will receive a tax slip and only you can claim the taxes withheld on your tax return. Even if your spouse contributed to the spousal RRSP and is reporting attributed income, they cannot claim the taxes withheld.

If the attribution rules apply to your withdrawal, you will need to complete CRA Form T2205 Amounts from a Spousal Or Common-law Partner RRSP, RRIF or SPP to Include in Income to calculate how much of the withdrawal to include in your and your spouse's income tax return.

When can't you make a spousal RRSP contribution?

Transferring the commuted value of your pension benefits

When you leave your employer or retire, you may be able to transfer all or a portion of the commuted value of your pension benefits to a locked-in RRSP. You can transfer these assets to your own locked-in RRSP but not to a spousal RRSP. If part of the commuted value cannot be transferred to a locked-in plan and is taxable to you, you may be able to reduce the tax payable by contributing the non-locked-in portion to a spousal RRSP if you have unused RRSP contribution room.

Transferring retiring allowances

If you receive a retiring allowance from your employer and you have years of service with that employer prior to 1996, all or a portion of that retiring allowance may be considered "eligible". You can transfer an eligible retiring allowance to your own RRSP without using any RRSP contribution room. In contrast, you are only able to contribute an eligible retiring allowance to a spousal RRSP if you use your RRSP contribution room.

The portion of your retiring allowance that does not qualify as eligible is the "non-eligible" portion. You can contribute the non-eligible portion of the retiring allowance to either your own RRSP or a spousal RRSP, but you will need unused RRSP contribution room to do so.

Transferring foreign pension plans

Under certain conditions, Canadian tax rules allow residents of Canada to contribute benefits withdrawn from foreign-based retirement plans to an RRSP without using RRSP contribution room. Under these rules, the contribution must be made to your own RRSP. If you would like to contribute the benefits to a spousal RRSP, you will need RRSP contribution room.

HBP and LLP repayments

If you are the annuitant of a spousal RRSP and you make a withdrawal from the spousal plan under the HBP or LLP, you must be the one to make the repayment. The repayment can be made to any one of your RRSPs where you are the annuitant. The repayment cannot be made to your spouse's RRSP. Where the required repayment is not made, attribution does not apply and you will have a taxable income inclusion.

Removing the spousal designation on a spousal plan

It may be possible to remove the spousal designation on a spousal RRSP or RRIF if your relationship with your spouse breaks down. To remove the spousal information, the following conditions must be met:

• You (the annuitant) and your spouse (the contributor) must be living separate and apart due to relationship breakdown;

• There must be no spousal contributions to any of the annuitant's RRSPs in the year of request or any of the two previous years; and

• There must be no withdrawals from the spousal RRSP during the year of request. In the case of a spousal RRIF, no more than the minimum must have been withdrawn during the year of request.

If the contributor passes away, it may also be possible to remove the spousal designation on a spousal RRSP or RRIF. Speak with your spousal RRSP or RRIF plan administrator for more information regarding removing the spousal designation on your plan in the event of relationship breakdown or on the death of the contributor.

Summary

Making spousal RRSP contributions can be useful, depending on your circumstances. Speak to your qualified tax advisor to determine if setting up a spousal RRSP may make sense for your family.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.