Superficial loss rules

Tax rules to remember when triggering capital losses. You may realize a capital gain or loss when you sell a non-registered investment for more (gain) or less (loss) than the cost base of the investment. Income tax is payable on the net capital gains you realize in a year. While this may sound straightforward, some capital losses are considered "superficial" and can't be used to offset capital gains. This article discusses the superficial loss rules and how they are applied.

Tax rules to remember when triggering capital losses. You may realize a capital gain or loss when you sell a non-registered investment for more (gain) or less (loss) than the cost base of the investment. Income tax is payable on the net capital gains you realize in a year. While this may sound straightforward, some capital losses are considered "superficial" and can't be used to offset capital gains. This article discusses the superficial loss rules and how they are applied.

Family Office Services

June 14, 2024

Superficial loss rules

Tax rules to remember when triggering capital losses

You may realize a capital gain or loss when you sell a non-registered investment for more (gain) or less (loss) than the cost base of the investment. Income tax is payable on the net capital gains you realize in a year. While this may sound straightforward, some capital losses are considered "superficial" and can't be used to offset capital gains. This article discusses the superficial loss rules and how they are applied.

Any reference to a spouse in this article includes a common-law partner.

Please contact us for more information about the topics discussed in this article.

What is a superficial loss?

When you sell your investment at a loss and reacquire the identical property, in some cases, the loss may be a superficial loss. When you realize a superficial loss, you can't claim the loss and therefore, you can't use it to offset capital gains. Instead, the loss is added to the adjusted cost base (ACB) of the identical property reacquired.

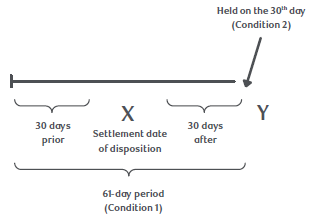

The superficial loss rules will apply when the following conditions are met:

Condition 1

During the period that begins 30 days before and ends 30 days after the settlement date of the disposition (e.g. when you sell the property), you or a person "affiliated" with you acquires the identical property that was disposed of at a loss. Although the rules may be complex, affiliated persons include you, your spouse, a corporation controlled by you and/or your spouse, and a trust where you and/or your spouse are majority interest beneficiaries.

Therefore, when you dispose of your investment at a loss, you need to consider the 61 days that includes the 30 days before, the day of and the 30 days after the settlement date of the disposition.

Condition 2

At the end of that period (i.e. on the 30th day after the settlement date of the disposition), you or a person affiliated with you owns or has a right to acquire the identical property.

In other words, identical property can be acquired at any time during the 61-day period without triggering the superficial loss rules, as long as you or someone affiliated with you does not own that identical property on the 30th day following the settlement date of the disposition of the original investment.

Identical property

The superficial loss rules only apply if you acquire "identical property". A similar but not identical property may be acquired at any time without triggering the superficial loss rules.

What is an identical property? The Canada Revenue Agency (CRA) has stated the following: "identical properties are properties that are the same in all material aspects, so that a prospective buyer would not have a preference for one as opposed to another. To determine whether properties are identical, it is necessary to compare the inherent qualities or elements which give each property its identity." If you're unsure of whether a property is an identical property, you should seek advice from a qualified tax professional.

Generally, two different classes of shares of a corporation would not be considered identical if they do not have the same interests, rights and privileges. For example, if class A shares of CompanyCo have voting rights but class B shares do not, they would not be considered identical. However, the CRA takes the position that if one class of shares is convertible into another class of shares, the two classes of shares may be considered identical.

This is because the right to convert from one class of shares (e.g. Class X) to another (e.g. Class Y) is considered a right to acquire property, and that right attached to Class X is identical to Class Y shares for the purposes of the superficial loss rules.

The CRA has also provided guidance on mutual funds. The CRA stated in a Technical Interpretation that a TSX 300 index-based mutual fund from one financial institution would generally be considered identical to a TSX 300 index-based mutual fund of another financial institution. However, in the same document, the CRA stated it would generally not consider a TSX 300 Index Fund to be identical to a TSX 60 Index Fund.

Therefore, if you sold a security at a loss and then you (or a person affiliated with you) repurchased the identical security at some point during the 61-day period, you may be able to prevent the application of the superficial loss rules by ensuring you (and any person affiliated with you) do not own the security on the 30th day.

For example, you own 1 share of CompanyCo with an ACB of $100. You sell the share of CompanyCo today for $90 and realize a capital loss of $10. You decide that you do not want to be out of the position and a week later, you repurchase a share of CompanyCo for $103. You hold this share of CompanyCo for longer than 30 days from the settlement date of the original disposition. In this case, you will be denied from claiming the $10 capital loss on the initial sale. The $10 loss will be added to the ACB of the security you repurchased so that the ACB of the CompanyCo share you currently hold will be $113 ($103 + $10).

If you had sold the repurchased security and the settlement date of the sale was on the 29th day (or any time before the 29th day) after the settlement date of the original disposition, you would be able to claim the $10 loss you realized on the original sale of the security. You could even acquire the position again a few days later. Of course, if the second sale settling 29 days after the original disposition was also at a loss, you would then have to pay close attention to whether the superficial loss rules would apply to that loss, too.

Please note that the preceding strategy is more aggressive than simply waiting until the 30 days have passed to re-acquire the position; therefore, please discuss this strategy with a qualified tax advisor if you are considering implementing it.

Settlement date

For the purpose of the superficial loss rules, the 61-day period is from settlement date to settlement date and not from the transaction date. Therefore, it's important to know how long it will take a particular transaction to settle.

In general, it takes 1 business day for a transaction involving a Canadian equity to settle. Mutual funds transactions also take 1 business day to settle.

For example, assume you sell 100 shares of CompanyCo with a trade date of September 3, 2024. This trade settles on September 4, 2024. Factoring in weekends and holidays when determining the settlement dates, this means you can acquire new CompanyCo shares with a trade date on or before August 1, 2024, or on or after October 4, 2024, if you wish to avoid triggering the superficial loss rules. Alternatively, since both conditions need to be met to trigger the superficial loss rules, you can simply ensure you do not own any CompanyCo shares on October 4, 2024 (see previous section for details on the conditions).

[CHART: 61-Day Period Timeline - Visual representation showing the period beginning 30 days before settlement date through 30 days after settlement date, with notations for Condition 1 and conditions for acquisition. Please clip and insert the timeline chart from page 2 of the PDF.]

Proportionate superficial loss formula

When you've triggered a superficial loss, you may still be able to claim some of the capital loss in the year of sale if you own fewer identical shares or units at the end of the 61-day period than the number of shares or units you sold at a loss. You may calculate the amount of the denied loss using the following formula:

Denied loss = capital loss determined x (least of S, P and B) ÷ S

Where:

- S = the number of shares disposed of;

- P = the number of shares bought in the 61-day period referred to in Condition 1 described earlier; and

- B = the number of shares left at the end of the 61-day period.

For example, you purchased 1,000 shares of CompanyCo in January 2024 for a total ACB of $10,000. On October 2, 2024, you sold the 1,000 shares of CompanyCo for total proceeds of $4,000, resulting in a capital loss of $6,000. However, you decided to buy back 300 shares of CompanyCo on October 16, 2024, for $1,500 and continue to hold these 300 shares with no plans to sell them. How much of your $6,000 capital loss is denied? Based on the formula, your denied loss is calculated as follows:

Denied loss = $6,000 x (least of 1,000, 300 and 300) ÷ 1,000 = $6,000 x 300 ÷ 1,000 = $1,800

As a result, you can still claim a capital loss of $4,200 ($6,000 – $1,800), and $1,800 of the capital loss is denied due to the superficial loss rules. This denied loss of $1,800 is added to the ACB of your remaining 300 CompanyCo shares, giving you a new ACB of $3,300 ($1,500 + $1,800).

In summary, if you own fewer identical shares or units at the end of the 61-day period than the number of shares or units you sold at a loss, then the proportional loss formula should be used to determine if some of the capital loss can still be claimed in the year of sale.

Pre-Authorized Contribution (PAC) Plans

Mutual funds may allow pre-authorized contributions on a weekly, bi-weekly, monthly or annual basis. They are a form of regular savings that are quite popular; however, you may be affected by the superficial loss rules if you decide to sell some of the funds at a loss. For example, selling some units in one month where the fund is in a loss position and then rebuying more in the same or the next month could trigger the superficial loss rules, and the loss may be denied. To avoid the superficial loss rules, you may need to stop the PAC in the month following a sale.

Superficial loss strategies that may work

The following are some transactions that may enable you to sell your investment that's in a loss position and realize the capital loss while possibly avoiding the application of the superficial loss rules.

All securities

- Repurchasing the same security after 30 days from the settlement date of the original sale.

- Purchasing an identical security at least 31 days prior to buying the original security. This may be a strategy you want to consider if you don't want to be out of the market at any time. Keep in mind the weighted average cost rules will impact the size of the loss that can be claimed in this situation.

- Ensuring you don't own the security on the 30th day following the settlement date.

- Transferring the security to an adult child, parent or sibling (i.e. anyone unaffiliated with you).

- Purchasing only a portion of the identical security back within the 61-day superficial loss period (see earlier 'proportionate superficial loss formula' example).

Shares

- Selling shares of one company and purchasing shares of a different company that provides similar exposure to the markets.

- Selling an exchangeable share and purchasing a non-exchangeable share of the same company (but not the other way around).

Mutual funds

- Switching from one mutual fund trust to a different mutual fund trust in a similar asset class.

- Switching from one mutual fund trust to a similar mutual fund corporation in a similar asset class or vice versa.

Superficial loss strategies that may not work

The following transactions involving investments in loss positions may result in the application of the superficial loss rules or similar rules where the capital loss is denied:

- Making an in-kind transfer of a security from your non-registered account to your RRSP/RRIF/TFSA of which you are the annuitant/holder. Although not considered a superficial loss, these losses would be permanently denied under another section of the Income Tax Act and the loss can never be claimed.

- Making an in-kind transfer of a security from your non-registered account to your RESP of which you are the subscriber.

- Selling a security in your non-registered account and immediately repurchasing the identical security in your RRSP/RRIF/TFSA/RESP.

- Selling a security in your non-registered account and immediately repurchasing the identical security in a managed non-registered account or vice versa.

- Selling a security in your non-registered account and repurchasing the security in a corporation controlled by you.

- Selling a security held by one of the corporations controlled by you and repurchasing the same security in a different corporation also controlled by you.

Exceptions to the superficial loss rules

In some cases, even if the two earlier noted conditions are met, the superficial loss rules will not apply. Some of the more common situations include:

- You are deemed to have sold the capital property because you became or ceased to be a resident of Canada.

- You are considered to have sold the property because you changed its use.

- The property is considered to have been sold because the owner passed away.

- The disposition results from the expiry of an option.

- You dispose of the property and, within 30 calendar days after the disposition, you became or ceased to be exempt from income tax.

Using superficial loss rules to transfer a capital loss to your spouse

It may be possible to use the superficial loss rule to transfer your unrealized capital losses to your spouse. You may be interested in this strategy if you have unrealized capital losses that you can't use personally and your spouse has taxable capital gains that would otherwise be subject to tax (or vice versa). Even if you or your spouse can use the losses personally, you may still want to transfer capital losses to the spouse in the higher tax bracket, if that spouse has taxable capital gains. For more information on this strategy, ask your RBC advisor for the article on this strategy.

Conclusion

By considering some of the strategies outlined in this article, you may be able to avoid the negative consequences associated with superficial loss transactions so you can maximize your tax-loss selling opportunities. However, it's important to keep in mind that the decision to dispose and acquire investments should be based on investment merits and not strictly the tax implications.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.