Tax-efficient asset location

When creating your investment plan, you've likely considered your asset allocation. Asset allocation involves finding the right balance of different types of investments such as fixed-income, equities, and cash or cash equivalents that would be appropriate for you, given your goals and risk tolerance. But when reviewing your overall investment portfolio, have you considered asset location? Asset location is how assets are distributed between all of your accounts, such as non-registered, registered and, in some cases, corporate accounts. Asset location is important because investment returns are taxed differently, depending on what type of income you generate and where you earn it. Paying attention to the type of income each investment generates, as well as which account you hold each investment in, may have a significant effect on your after-tax return.

When creating your investment plan, you've likely considered your asset allocation. Asset allocation involves finding the right balance of different types of investments such as fixed-income, equities, and cash or cash equivalents that would be appropriate for you, given your goals and risk tolerance. But when reviewing your overall investment portfolio, have you considered asset location? Asset location is how assets are distributed between all of your accounts, such as non-registered, registered and, in some cases, corporate accounts. Asset location is important because investment returns are taxed differently, depending on what type of income you generate and where you earn it. Paying attention to the type of income each investment generates, as well as which account you hold each investment in, may have a significant effect on your after-tax return.

Family Office Services

June 14, 2025

Tax-efficient asset location

A strategy to help enhance your after-tax return on investments

When creating your investment plan, you've likely considered your asset allocation. Asset allocation involves finding the right balance of different types of investments such as fixed-income, equities, and cash or cash equivalents that would be appropriate for you, given your goals and risk tolerance. But when reviewing your overall investment portfolio, have you considered asset location? Asset location is how assets are distributed between all of your accounts, such as non-registered, registered and, in some cases, corporate accounts. Asset location is important because investment returns are taxed differently, depending on what type of income you generate and where you earn it. Paying attention to the type of income each investment generates, as well as which account you hold each investment in, may have a significant effect on your after-tax return.

Paying attention to how investment income is taxed

The type of investment income you generate, whether it's interest income, Canadian dividend income, capital gains or foreign income (for example, dividends from foreign corporations), matters when it comes to your taxes. Interest income and foreign income are generally taxed at the same rate as employment income, at your marginal tax rate. Canadian dividend income is virtually always more tax-efficient than interest income because you're entitled to a dividend tax credit that reduces your taxes payable. Capital gains can also be tax-efficient since only a portion of the capital gain is taxable.

Holding the right investments in the right accounts

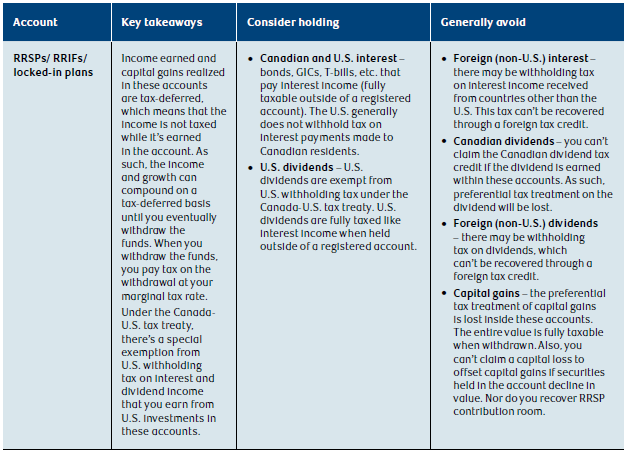

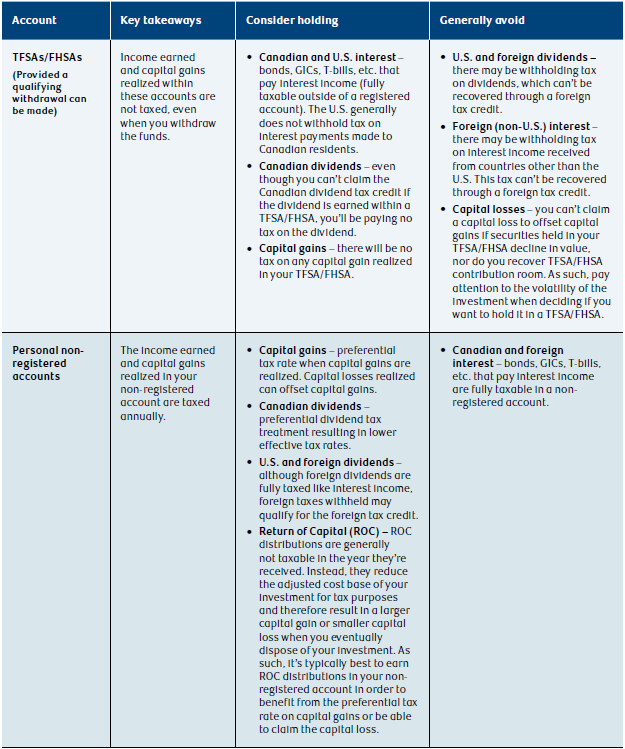

It's important to determine not only the types of investments that meet your needs, but also where to hold these investments. This is because each of your accounts, such as your registered retirement savings plan (RRSP), tax-free savings account (TFSA) and your non-registered account, are subject to different tax rules. You may be able to reduce the overall taxes on your investments just by holding your investments in the appropriate accounts.

Here are some aspects to keep in mind when considering which account is right for various investment types. The investments discussed here are categorized based on the typical types of income they generate. For example, fixed-income investments mainly generate interest income while dividend-paying stocks generally produce dividend income and capital gains when sold. There are many other types of investments (e.g., mutual funds, ETFs and REITs), but since they can produce a variety of income types including interest, dividends, capital gains and return of capital, you may need to analyze these types of investments on an individual basis. For example, a particular mutual fund may be more likely to generate interest income because that specific fund mainly invests in fixed-income instruments.

Also, keep in mind that finding the optimum asset allocation across accounts is a complex task, and in some cases, the following suggestions may not be applicable to your situation. Further, in addition to the type of income generated by the investment, you'll want to consider your investment time horizon, account contribution limits, personal tax rates and expected return and yields. For example, where you'd typically avoid holding a foreign-paying dividend stock in your TFSA to avoid the non-recoverable foreign withholding taxes, you might consider holding it in your TFSA if you expect that security to quadruple in value in order to pay no tax on a large capital gain.

Note that the following asset location considerations are for Canadian residents who are not U.S. persons (including U.S. citizens, residents or green-card holders).

In summary, from a tax perspective, it may be worthwhile to focus on holding equity investments such as Canadian dividend-paying stocks in your non-registered account to benefit from the preferred tax treatment of capital gains and dividends. Also, where possible, you can consider holding fully taxed income investments such as interest inside your registered accounts to defer or eliminate the tax on income that's fully taxable. As for foreign income, you'll have to pay close attention to what type of income the investment generates, as well as the source country of the investment. For example, for U.S. dividend-paying securities, it may be better to hold them inside an RRSP, as there will generally be no withholding tax versus holding them inside a TFSA where there will be withholding tax on the investment payments. Of course, if the after-tax return on the U.S. security is better than any other investment you believe you should hold, you may still consider holding it in your TFSA.

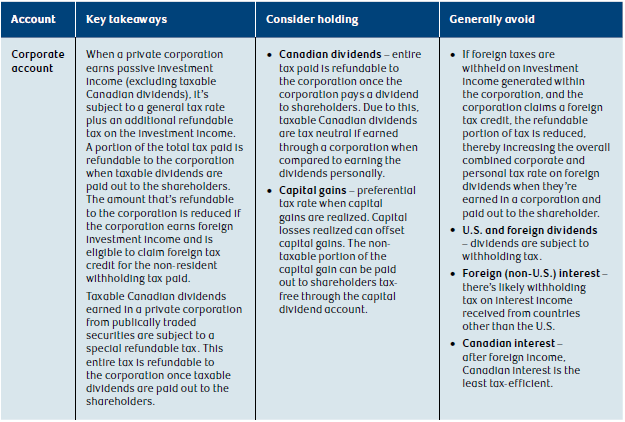

If you have a corporation

If you own a corporation, you may want to include your corporate investment account into your asset location decisions. Generally, the income and capital gains earned on investments within your corporation will be considered passive investment income. This is regardless of whether you're investing in an operating company or holding company. This is also assuming that the income generated from investing is not pertaining to and incidental to your business or practice (if you have one).

The taxation of passive investment income earned in a corporation is far from straightforward. If you'd like a more detailed review of how each type of income is taxed, please refer to our article on the taxation of investment income in a corporation. From a high level, the Canadian tax system was designed so that, theoretically, there should be no material tax advantage or disadvantage to earning passive income through a corporation. However, the Canadian tax system is not perfect and may be a tax cost to earning investment income through a corporation where the income is earned in the corporation and distributed out to the shareholders. Despite this, there are still some guiding principles to consider when deciding whether a particular type of investment is suitable for your corporation from a tax-efficiency perspective.

Paying attention to your other objectives

While tax-efficiency is important when creating your investment portfolio, it should only be considered after you've decided on the appropriate asset allocation for your risk tolerance and time horizon. If you're a conservative investor, you may typically invest in principal-protected investments such as GICs. Since you're aware that interest doesn't benefit from tax-preferred treatment, you may consider investing in other products that generate Canadian dividends or capital gains. However, given your investor profile, high-risk equities with large capital gains or capital growth may not make sense in your circumstances.

You should also consider your needs and objectives, your time horizon and so on. For example, if you have surplus cash, before investing, you should first determine if you have an immediate need for the cash. Do you have the cash to pay immediate installments on your major capital expenditure? If so, it might not make sense to invest the funds. If there's no immediate need, but you may need the funds in the short or medium term, you'll want to ensure the investments you choose can be easily liquidated when the time comes. Alternatively, are your long-term objectives your main priority? Perhaps you want to boost your retirement savings or enhance the value of your estate. In this case, you may want to consider investments that feature tax-sheltered growth and tax-free payouts.

Conclusion

It's not always what you earn, it's what you keep. If you want to keep more of what you earn as an investor, then investing tax-efficiently, and considering asset location, may help you build and protect your wealth. Working with your RBC advisor and qualified tax advisor can help you make informed decisions on which tax-efficient investments or strategies may be most appropriate for you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.