Tax-free first home savings account (FHSA)

A registered account to help more Canadians enter the housing market. The FHSA is a registered account to help individuals save up to $40,000 on a tax-free basis to purchase their first home. The FHSA is a mix between a registered retirement savings plan (RRSP) and a tax-free savings account (TFSA).

A registered account to help more Canadians enter the housing market. The FHSA is a registered account to help individuals save up to $40,000 on a tax-free basis to purchase their first home. The FHSA is a mix between a registered retirement savings plan (RRSP) and a tax-free savings account (TFSA).

Family Office Services

June 14, 2026

Tax-free First Home Savings Account (FHSA)

A registered account to help more Canadians enter the housing market

The FHSA is a registered account to help individuals save up to $40,000 on a tax-free basis to purchase their first home. The FHSA is a mix between a registered retirement savings plan (RRSP) and a tax-free savings account (TFSA). Like an RRSP, eligible contributions you make to an FHSA are tax-deductible; like a TFSA, qualifying withdrawals you make to purchase a first home (including the investment income earned) aren't taxable. This article provides a summary of key features of the FHSA. Any reference to a spouse in this article also includes a common-law partner.

Opening the FHSA

To open an FHSA, you must be a resident of Canada, at least 18 years of age and not turning age 72 or older in the year. If you live in a province where the age of majority is 19, you must be at least 19 years of age to open an account.

In addition, you must be a first-time home buyer, which means you and your spouse must not have owned a home (located anywhere in the world) in which you lived in as your principal residence at any time during the part of the calendar year before you opened the account or at any time in the preceding four calendar years.

To provide more clarity, you won't be considered a first-time home buyer if you lived in a home owned by your spouse during the relevant period if that person is still your spouse when you plan to open an FHSA. On the flip side, for example, if you lived in a home owned by your spouse during the relevant period but are divorced from your spouse at the time you wish to open an FHSA, you may be considered a first-time home buyer.

Financial institutions aren't required to confirm if you are eligible to open an FHSA. It's important for you to confirm your eligibility and ensure you meet the necessary criteria to avoid any negative tax implications associated with non-compliance.

Please contact us for more information about the topics discussed in this article.

Contributions

You'll be able to contribute up to a lifetime limit of $40,000 to your FHSA, with an annual contribution limit of $8,000. The full annual limit of $8,000 would be available in the year you open the account.

You can hold more than one FHSA, but the total amount you can contribute to all of your FHSAs can't exceed your annual and lifetime contribution limits.

You'll be able to claim a deduction for contributions you made to an FHSA during a calendar year. However, contributions you make to an FHSA following a qualifying withdrawal (i.e. when buying a first home) won't be deductible.

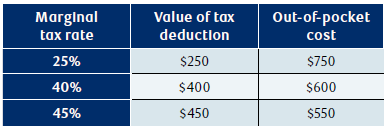

An FHSA contribution can be claimed as a deduction against all sources of taxable income. This deduction reduces your amount of taxable income for the year and therefore your taxes payable. The actual tax savings will depend on your marginal tax rate. The following table outlines the out-of-pocket cost of a $1,000 FHSA contribution after claiming the deduction:

FHSA contributions don't need to remain in the plan for a specific amount of time in order to be deductible. Also, unlike RRSPs, contributions you make within the first 60 days of a given calendar year can't be deducted in the previous tax year.

Carryforward Contributions

You'll be allowed to carry forward your unused annual contribution limit up to a maximum of $8,000. This means that if you contribute less than $8,000 in a given year, you can contribute the unused amount in a following year on top of your annual contribution limit of $8,000 (subject to your lifetime contribution limit). For example, if you contribute $5,000 to your FHSA in 2023, you'll be allowed to contribute $11,000 in 2024 (i.e. $8,000 for 2024, plus the remaining $3,000 from 2023).

Carryforward amounts only start accumulating after you open an FHSA for the first time. As such, if you're a first-time home buyer, you could consider opening an FHSA immediately, even if you don't have the funds to contribute. As an example, if you open an account in 2025 but only have the funds to contribute to the FHSA in 2026, you'd be able to contribute up to $16,000 ($8,000 annual contribution room from 2026, plus $8,000 carried forward contribution room from 2025) in 2026.

It's important to note that your FHSA carryforward amount can't exceed $8,000 in a given year. Therefore, you can't contribute more than $16,000 to an FHSA in a particular year. For example, let's assume you open an FHSA in 2024 but don't make any contributions for 2024 and 2025. In 2026 you will be able to contribute $16,000 ($8,000 for 2026 plus $8,000 maximum carryforward balance). Even though you opened an FHSA in 2024 but didn't contribute for two years, you'll only have $8,000 of FHSA carryforward for use in 2026. Your FHSA carryforward will be zero for subsequent years (e.g. your contribution room will be $8,000 for 2027) unless you contribute less than the annual maximum of $8,000 in a later year.

Undeducted Contributions

If you make a contribution to your FHSA, you don't have to claim a deduction for that year. Like RRSP deductions, you'll be able to carry forward undeducted contributions indefinitely and deduct them in a later year. For example, if you contribute $3,000 to your FHSA in 2025, you can carry forward some or all of your deduction in 2026 or subsequent tax years. You may want to consider this approach if you want access to tax-free growth immediately, but you expect to be in a higher tax bracket in a future tax year and would benefit more from a deduction in that year.

Income Earned

Income as well as capital gains (and capital losses) earned in an FHSA aren't included in your annual income (or deductible) for tax purposes. This means income and capital gains can continue to grow and compound in the FHSA on a tax-free basis. Income, capital gains and capital losses will also not be taken into account in determining your eligibility for income-tested benefits or credits delivered through the income tax system such as the Canada child benefit and the goods and services tax (GST) credit.

Withdrawals

There are qualifying withdrawals (non-taxable) as well as non-qualifying withdrawals (taxable). When any withdrawals are made, you'll receive an information slip from your financial institution stating the amount of the withdrawal and, for non-qualifying withdrawals, the amount of income tax withheld.

Qualifying Withdrawals

In order for an FHSA withdrawal to be a qualifying withdrawal (i.e. non-taxable), the following conditions must be met:

• You must be a first-time home buyer at the time you make a withdrawal. The first-time home buyer definition for the purposes of making a qualifying withdrawal is different than the first-time home buyer definition for the purposes of opening an FHSA. Specifically, you couldn't have owned a home in which you lived at any time during the calendar year before the withdrawal is made or at any time in the preceding four calendar years. If you make a withdrawal within 30 days of acquiring your home, it'll still be considered a qualifying withdrawal; and

• You must have a written agreement to buy or build a qualifying home before October 1 of the year following the year of withdrawal and intend to occupy the qualifying home as your principal residence within one year after buying or building it. A qualifying home is a housing unit located in Canada.

If an FHSA withdrawal is qualifying, you may withdraw the entire amount of available FHSA funds on a tax-free basis either as a single withdrawal or a series of withdrawals. No taxes will be withheld on qualifying withdrawals. Qualifying withdrawals will also not be taken into account in determining your eligibility for income-tested benefits or credits such as the Canada child benefit and the GST credit.

Non-qualifying Withdrawals

If you make a withdrawal that's not qualifying, the withdrawal will be included in your income. Taxes will be withheld on non-qualifying withdrawals, in a manner consistent with taxable RRSP withdrawals.

Transfers

You can transfer funds from an FHSA to another FHSA, an RRSP or a registered retirement income fund (RRIF) on a tax-free basis.

If you transfer funds from an FHSA to an RRSP or a RRIF, the transfer won't reduce, or be limited by, your available RRSP contribution room, nor would the transfer reinstate your FHSA annual or lifetime contribution limit. Once transferred, the funds will be subject to the rules applicable to RRSPs and RRIFs, including that the funds will be taxable when you withdraw them from the account.

You're also allowed to transfer funds from your RRSP to your FHSA on a tax-free basis, subject to the FHSA annual and lifetime contribution limits. This transfer isn't deductible and doesn't reinstate your RRSP contribution room. Once transferred, the funds will be subject to the rules applicable to FHSAs, including that the funds will be taxable if you make a non-qualifying withdrawal.

Interaction With the Home Buyers' Plan (HBP)

Under the HBP it's possible to withdraw up to $60,000 from your RRSP to buy or build a home without triggering immediate tax consequences. Generally, you must repay any amounts withdrawn to your RRSP within 15 years, starting the second calendar year following the year in which you made the withdrawal. The funds must be repaid but as there's no interest charged, it's like an interest-free loan to yourself.

You can make both an FHSA withdrawal and a HBP withdrawal for the same qualifying home purchase. If you maximize withdrawals from both programs, you'll be able to access $100,000 in capital plus any growth in the FHSA to use towards a purchase of a home.

If you don't have enough funds to contribute to both an FHSA and an RRSP, here are some points to consider:

• With the HBP, you're essentially borrowing money (interest-free) from your own RRSP, as you have to repay the funds to your RRSP within 15 years. With the FHSA, you can make a qualifying withdrawal (tax-free) and you don't have to repay the funds.

• If you don't buy a home within 15 years, you can transfer the funds accumulated in your FHSA to your RRSP, where you can then withdraw under the HBP.

• If you start contributing to an RRSP and then transfer the funds into your FHSA, you'll have lost that RRSP room. On the other hand, if you start contributing to an FHSA and then transfer the funds to your RRSP, the transfer won't reduce your RRSP room. Since a transfer of funds from an FHSA to an RRSP won't reduce your available RRSP contribution room, you can effectively create more RRSP room by starting to contribute to your FHSA.

Spousal Considerations for the FHSA

Spousal Contributions

As the FHSA holder, only you can claim a deduction for contributions made to your own FHSA. You won't be able to contribute to your spouse's FHSA and claim a deduction. You can, however, gift funds to your spouse and have them contribute those funds to their own FHSA. Normally, if you gift funds to your spouse, the attribution rules apply so that all of the income earned, and capital gains realized on those funds will be attributed back to you and taxed in your hands. However, there is an exception and the attribution rules won't apply to income earned and capital gains generated within an FHSA that's derived from such contributions.

To illustrate, let's assume you gifted funds to your spouse, and they contributed those funds to their own FHSA. If, in the future, your spouse makes a qualifying FHSA withdrawal, the entire amount withdrawn will be tax-free. If instead, your spouse makes a non-qualifying withdrawal, attribution doesn't apply and your spouse will have a taxable income inclusion.

Relationship Breakdown

If you experience a breakdown of your marriage or common-law partnership, you may transfer funds directly from your FHSA to your former spouse's FHSA, RRSP or RRIF. These transfers wouldn't reinstate any FHSA contribution room for you and wouldn't use any contribution room of your former spouse.

Over-contributions

Over-contributions occur when you contribute more than your FHSA contribution room. You'll be subject to a tax of 1% on the highest excess amount in the month, for each month (or part of a month) that you're in an over-contribution position.

The 1% tax will continue to apply for each month the excess amount remains in your FHSA. The tax will stop accruing when:

1. You withdraw the excess amount from your FHSA; or

2. You receive new contribution room to absorb the over-contribution, which occurs on January 1 of the following year.

You'll be allowed to deduct an over-contributed amount in the year in which it ceases to be an over-contribution but not earlier. However, if a qualifying withdrawal is made before an over-contribution ceases to be an over-contribution, no deduction would be provided for the over-contributed amount.

An Example:

Zoey contributes $10,000 on November 15, 2025, and keeps the full amount of the funds in her FHSA. This contribution exceeds Zoey's annual FHSA contribution limit by $2,000. Zoey will be subject to an over-contribution tax of $40 (1% × $2,000 × 2 months) when filing her 2025 tax return. The $2,000 amount would cease to be an over-contribution on January 1, 2026, as a new annual limit of $8,000 would be available.

Zoey will be allowed to deduct $8,000 from her 2025 net income. Presuming Zoey didn't make a qualifying withdrawal between November 15, 2025, and January 1, 2026, she would be allowed to claim a deduction of $2,000 on her 2026 tax return.

Closing the FHSA

You'll need to close your FHSA by December 31 of the year you turn age 71. You'll also need to close your FHSA by December 31 of the 15th anniversary of first opening the account, if you haven't used the funds to purchase a qualifying home.

If you aren't able to use the funds in your FHSA to purchase a qualifying home, you can transfer any savings in the account on a tax-deferred basis to your RRSP or a RRIF. Future withdrawals from your RRSP or RRIF will be taxable.

If you make a qualifying withdrawal from your FHSA, the account must be closed by December 31 of the following year. You can transfer any unwithdrawn savings on a tax-deferred basis to an RRSP or a RRIF until December 31 of the year following the year of your first qualifying withdrawal. You won't be able to open a new FHSA in the future even if you once again meet all the qualifications to be considered a first-time home buyer.

After the date it loses its FHSA status, the FHSA will become a taxable trust and will have to pay tax on any income earned. You'll have to include in income the fair market value (FMV) of the FHSA immediately before it lost its status as an FHSA. The CRA will issue you a reminder when your FHSA ceases to have tax-advantaged status.

Treatment Upon Death

You may be able to designate your spouse as the successor account holder on your FHSA. If named as the successor holder, your surviving spouse would become the new holder of the FHSA immediately upon your death, provided your surviving spouse meets the eligibility criteria to open an FHSA. The FHSA in this case can maintain its tax-exempt status.

Inheriting an FHSA in this way wouldn't impact your surviving spouse's contribution limits. Inherited FHSAs would assume your surviving spouse's closure deadlines. If your surviving spouse isn't eligible to open an FHSA, amounts in the FHSA could instead be transferred on a tax-deferred basis to your surviving spouse's RRSP or RRIF, or withdrawn on a taxable basis.

If you name anyone other than your spouse as the beneficiary of your FHSA, the funds will need to be withdrawn following your death and paid to your named beneficiary. Amounts paid to your beneficiary will be included in your beneficiary's income for tax purposes and subject to withholding tax. If you didn't name a beneficiary, your estate will have the income inclusion. The income won't be included in your final tax return.

The FHSA will cease to be an FHSA at the end of the year following the year of death.

Non-resident Issues

If you move from Canada, you'll be allowed to contribute to your existing FHSA after becoming a non-resident, but you won't be able to make a qualifying withdrawal as a non-resident. In order to withdraw funds from an FHSA, you must be a resident of Canada at the time of withdrawal and up to the time a qualifying home is bought or built. If you make a non-qualifying withdrawal as a non-resident, the withdrawal will be subject to withholding tax.

Qualified Investments

You'll be able to hold a broad range of investments, including mutual funds, publicly traded securities, government and corporate bonds, and GICs in your FHSA. Essentially, any investment that's allowed to be held in an RRSP or a TFSA can be held in your FHSA.

Prohibited Investment, Non-qualified Investment and Advantage Tax Rules

There are prohibited investment, non-qualified investment and advantage tax rules that are applicable to other registered plans, and these rules will also apply to FHSAs. These rules are intended to disallow investments in entities or transactions with parties that you don't deal at arm's length with. Further, these rules prevent investments in certain other assets such as land, shares of private corporations and general partnership units.

Carrying On a Business

FHSAs are generally intended to hold passive investments. If the CRA determines that an FHSA is "carrying on a business" of trading securities, the income from that business may be taxable. Whether the FHSA is carrying on a business depends on many different factors, including how frequently the securities are traded, the length of time the securities are owned, the holder's knowledge or experience in the securities markets and whether the securities are considered speculative in nature.

If the CRA determines that an FHSA is carrying on a business of trading in securities, taxes are imposed on the income earned by the FHSA. The FHSA holder and the trustee of the FHSA are jointly and severally liable with the FHSA for any tax payable on income earned from carrying on a business in the FHSA.

Other Features

Interest Deductibility

Like RRSPs and TFSAs, interest on money borrowed to invest in an FHSA isn't deductible for tax purposes.

Income Splitting

You can gift money to your adult children to contribute to their own FHSA. Income earned on that gift isn't subject to attribution, but keep in mind that the gift becomes your child's property.

Collateralization

If you pledge the assets in the FHSA as collateral for a loan, you'll have to include the full value of those assets in your income.

Bankruptcy

FHSAs aren't creditor protected under the Bankruptcy and Insolvency Act.

Conclusion

Eligible first-time home buyers can consider opening an FHSA and taking advantage of the tax-deductible contributions, plus the tax-free compounding growth on any income earned and capital gains realized within the account. This account may help you save tax-efficiently towards the purchase of a home. And if you don't end up buying or building a qualifying home, you can direct the funds towards your retirement by transferring any unwithdrawn savings on a tax-free basis to an RRSP or a RRIF. Speak with your RBC advisor and a qualified tax advisor to see how the FHSA may help you meet your financial goals.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.