Taxation of options transactions

Options can provide you with flexible investment choices. Depending on the contract, options can protect or enhance your portfolio in rising, falling and neutral markets. As flexible as options are, they're quite complex to understand and aren't appropriate for all investors. The purpose of this article is to provide a general overview of options transactions, as well as how to report them for tax purposes.

Options can provide you with flexible investment choices. Depending on the contract, options can protect or enhance your portfolio in rising, falling and neutral markets. As flexible as options are, they're quite complex to understand and aren't appropriate for all investors. The purpose of this article is to provide a general overview of options transactions, as well as how to report them for tax purposes.

Family Office Services

November 14, 2025

Taxation of options transactions

Options can provide you with flexible investment choices. Depending on the contract, options can protect or enhance your portfolio in rising, falling and neutral markets. As flexible as options are, they're quite complex to understand and aren't appropriate for all investors. The purpose of this article is to provide a general overview of options transactions, as well as how to report them for tax purposes.

Description of an option

Options are contracts that allow buyers (holders of the option) and obligee sellers (writers of the option) to buy or sell an underlying financial product (such as shares, ETFs, indices, foreign currency, etc.) at a specific price (referred to as the strike price), on or before a certain date (referred to as the expiration date). Throughout the article we will refer to the underlying financial product as shares. The cost of an option is called the premium, which is paid by the buyer to the seller of the option. The premium is determined by factors including the price of the underlying share, strike price, time remaining until expiration and price volatility of the share.

Buyers and sellers

The important distinction between buyers and sellers is that buyers have the right, but not the obligation, to buy or sell the underlying shares. Buyers can always let the expiration date pass without exercising their right. Sellers, on the other hand, have the obligation to buy or sell the underlying shares at the strike price on or before the expiration date. This obligation arises if a buyer exercises their right to buy or sell the underlying shares and the option is randomly assigned by the industry clearing house to an investment firm who then assigns it to a seller. Buyers and sellers of options can also close out options by trading their options in the market.

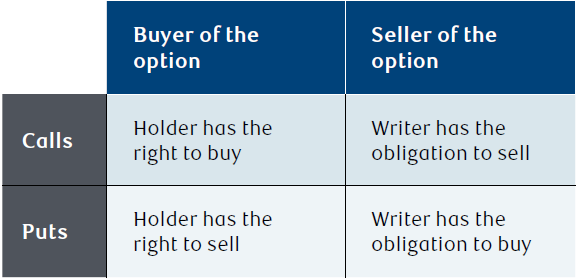

Calls and puts

Calls

Calls give the holder the right to buy shares at the strike price on or before the expiration date. Buyers of calls hope that the shares will increase substantially before the option expires. If you are a buyer, it makes sense to exercise a call option if the share price is above the strike price. This option position is referred to as being "in the money."

In order for a buyer to buy a call, a seller needs to write a call option. Sellers of calls generally expect that the price of the underlying shares will fall and they will not need to deliver the underlying shares to the buyer.

Puts

Puts give the holder the right to sell shares at the strike price on or before the expiration date. Buyers of puts hope that the price of the shares will fall before the option expires. A put option is in the money when the share price is below the strike price.

In order for a buyer to buy a put, a seller needs to write a put option. Sellers of puts generally expect that the price of the underlying shares will increase and they will not have to buy the underlying shares from the buyer.

Types of options transactions

There are four types of options transactions you can enter into:

Options with life spans longer than one year, often referred to as Long Term Equity Anticipation Securities (LEAPS), are not addressed in this article.

Covered and naked options

If an option is covered, this means the seller owns the corresponding amount of the underlying shares. Conversely, if an option is naked, the seller doesn't own any, or enough, of the underlying shares. Trading naked options is only suitable for experienced traders since it's a risky endeavour and the potential for losses is unlimited. For example, say the seller writes a call option and expects the price of a particular share to fall. Instead of falling, the price of the share increases substantially. The seller, who doesn't already own the share regardless of how high the price is, and then sell it to the option buyer at the strike price.

Exiting an option

As a buyer, when you buy a put or a call option, there are three potential outcomes:

1. The option is in the money and you may choose to exercise the option.

2. The option is out of the money and worthless, so you let the option expire.

3. You sell the option contract on the market prior to expiration (sell to close).

As a seller, when you sell a put or a call option, there are three potential outcomes:

1. A buyer exercises the option and you get assigned.

2. The option expires.

3. You buy back the option contract prior to expiration (buy to close).

Tax consequences of options transactions

To determine the tax consequences of an options transaction, you need to establish whether the transaction is considered on account of income (business income or loss) or capital (capital gain or loss). This determination depends on your specific circumstances and the nature of the transaction.

If it's determined that the options transaction is on account of income, the full amount of any gain must be included in your income and taxed at your marginal tax rate. The full amount of any loss is deductible against income from any source (such as business income, employment income or taxable capital gains). If the loss cannot be deducted within the year, it may be carried back three years or carried forward 20 years.

If it's determined that the options transaction is on account of capital, a portion of the capital gain is taxable (based on the capital gains inclusion rate) and must be included in income. Similarly, a portion of any capital loss is deductible, but the loss can only be used to offset capital gains. If the loss cannot be deducted within the year, it may be carried back three years or carried forward indefinitely.

Gains and losses on account of income or capital

Although there's no definitive rule to determine if a particular transaction is on account of income or capital, the Canada Revenue Agency (CRA) has provided some guidance in their Interpretation Bulletin IT-479R.

The CRA has stated that the proceeds of sale will normally be considered to be on income account where in security transactions the person is disposing of securities in a way capable of producing gains and with that intention, and the transactions are of the same kind and carried on in the same way as those of a "trader or dealer in securities." A trader or dealer in securities generally means a taxpayer who participates in the promotion or underwriting of a particular issue of shares, bonds or other securities or a taxpayer who holds themselves out to the public as a dealer in shares, bonds or other securities. Some factors that the CRA may consider when determining whether you are carrying on security transactions in the same way as those of a trader or dealer in securities are: The frequency of transactions, the ownership period of the securities, your knowledge of the securities market, the time spent studying the securities market and investigating a potential purchase, and whether you intended to acquire the securities for resale at a profit.

If you're not a non-resident of Canada, a trader or dealer in securities, a bank, a credit union or another excluded corporation, you may make an irrevocable election in your income tax return that deems all Canadian securities you own in that year and in any subsequent year to be treated as capital property. This means the disposition of every Canadian security in that year and all subsequent years will be treated as a capital gain or loss. The election is made by filing form T123 – Election on disposition of Canadian securities. For any such election made after December 19, 2006, Quebec residents are also required to notify Revenu Québec in writing about the election and include a copy of any document that was filed with the CRA in respect of the election. However, it appears that recently Revenu Québec administratively doesn't require this notice for individuals.

However, an option isn't a Canadian security within the applicable definition in the Income Tax Act. As a result, options transactions cannot qualify for the guaranteed capital gains treatment under this election.

For options transactions, it's a question of fact whether gains or losses are on income account or capital account. The CRA generally presumes that the gain or loss realized by a buyer of options or a seller of covered options is on the same account as the underlying shares. This means if the gain or loss on the sale of the underlying shares would be treated as a capital gain or loss, the gain or loss on the call or put option transaction could also be treated as a capital gain or loss. This presumption may not apply where the facts clearly indicate otherwise.

The CRA states that the gain or loss realized by a seller of naked options is normally on account of income. However, the CRA will allow these gains and losses to be reported on account of capital, provided this method is followed consistently from year to year.

As the determination of the tax treatment can be subject to interpretation, it's always recommended that you seek advice from a qualified tax advisor whenever you realize gains or losses on options transactions. Using a consistent approach year over year may help reduce the risk of a challenge by the CRA.

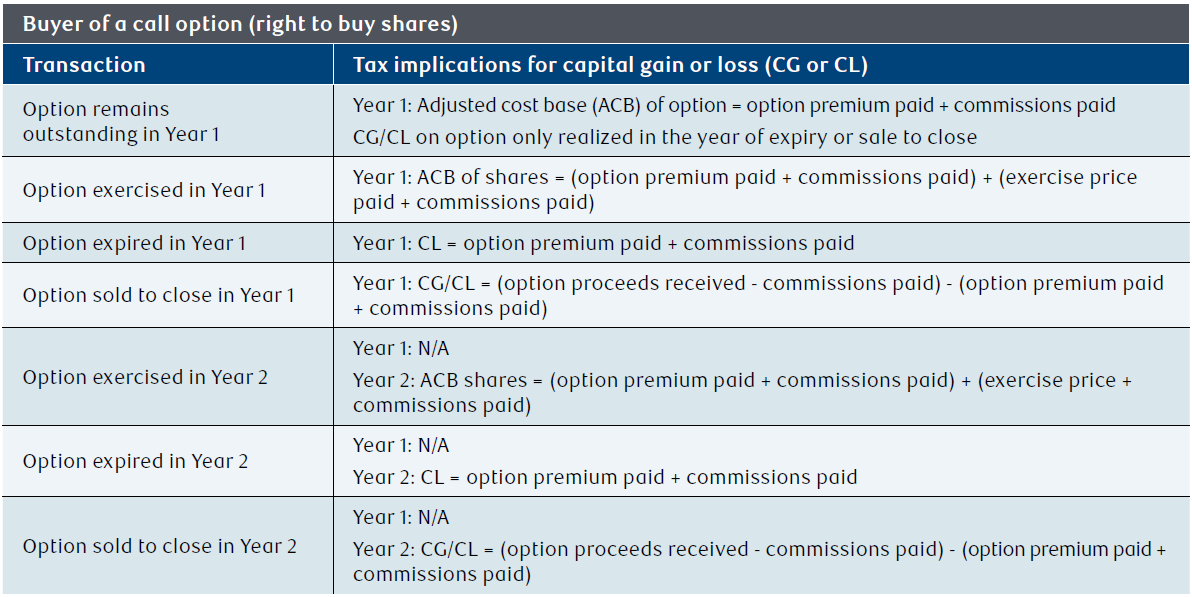

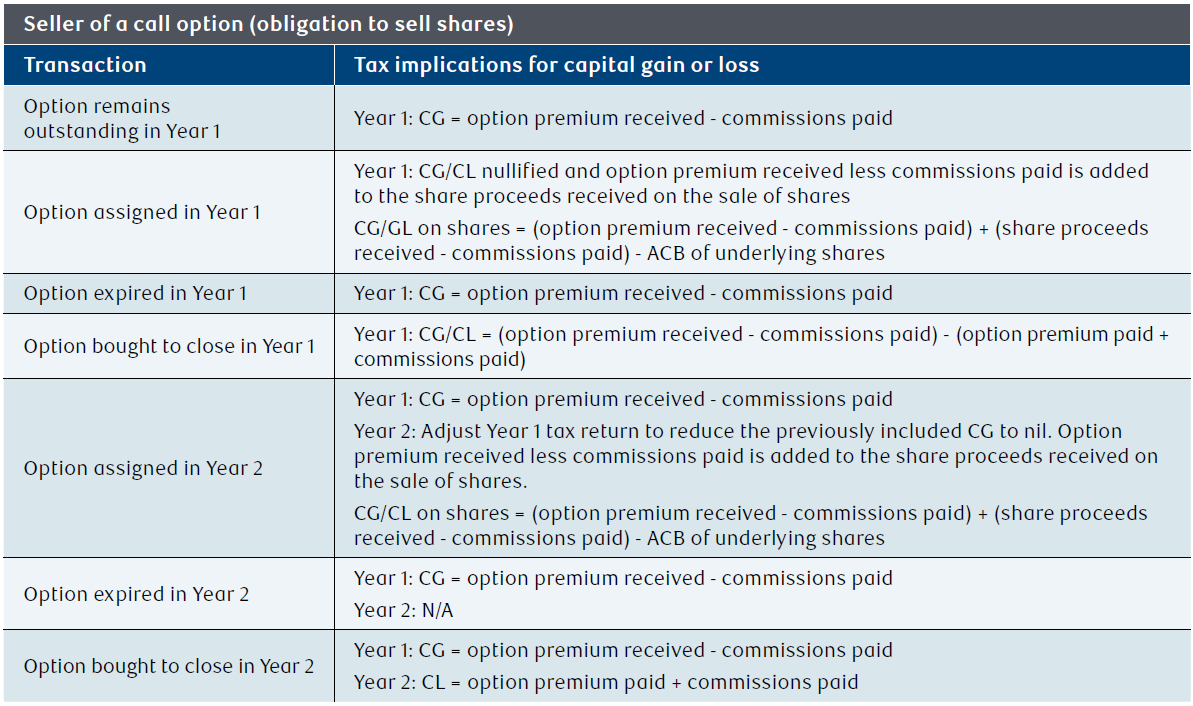

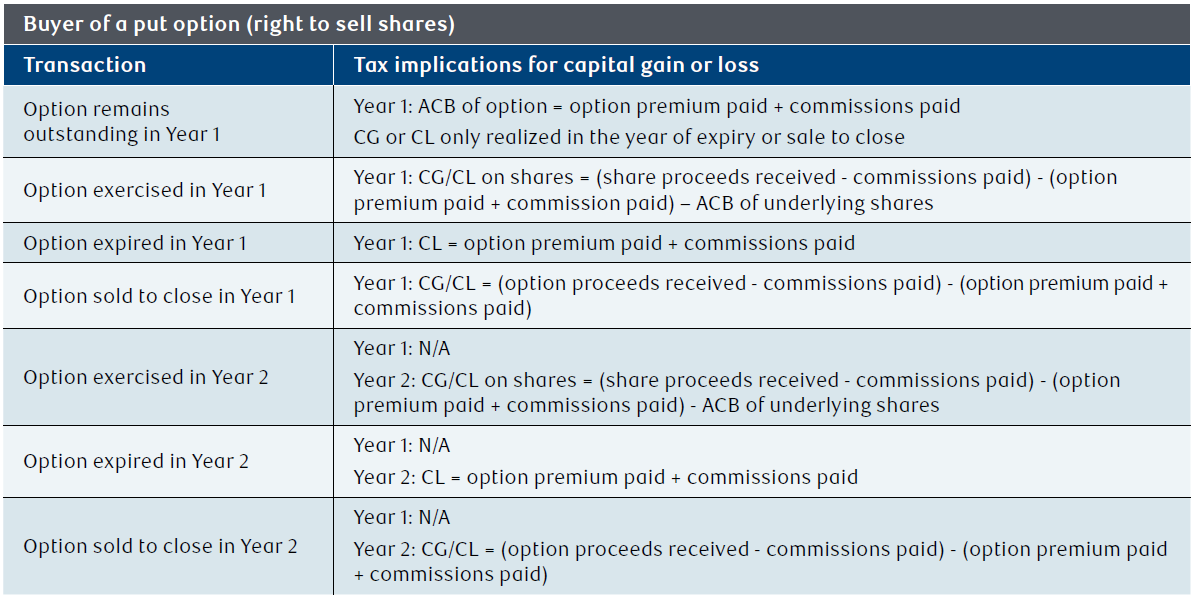

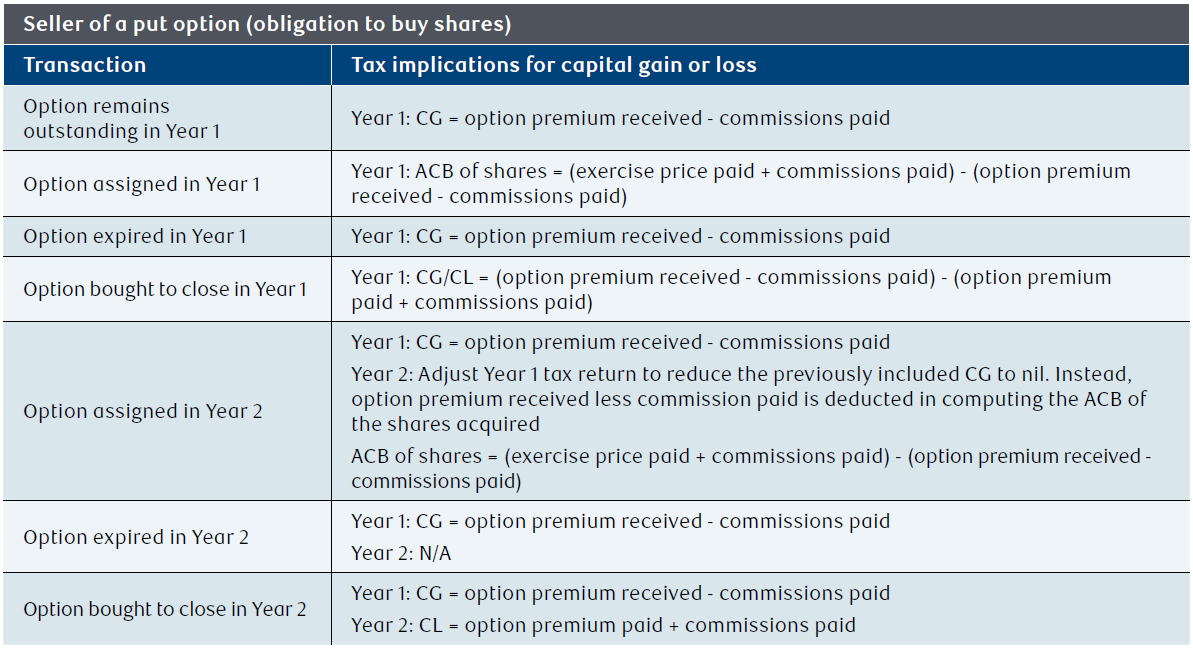

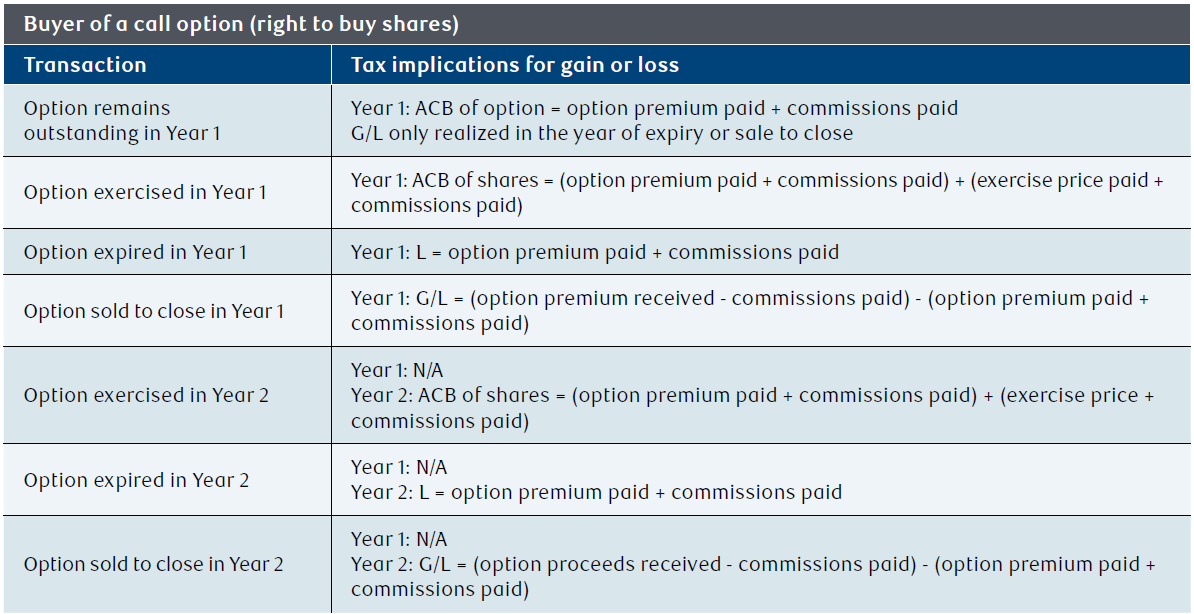

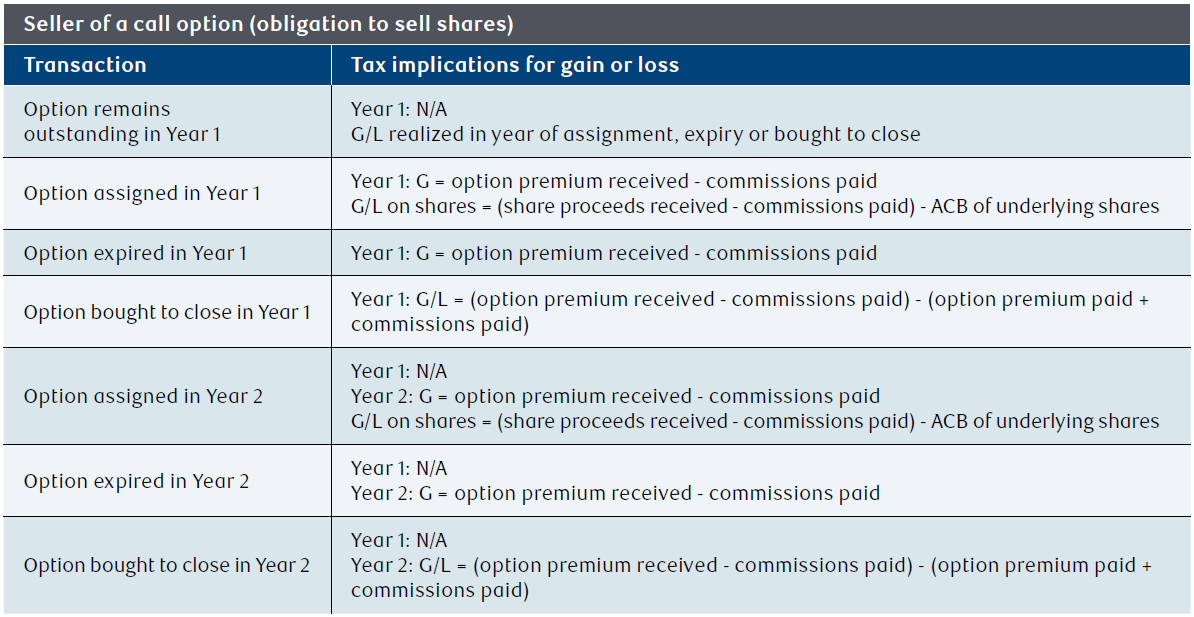

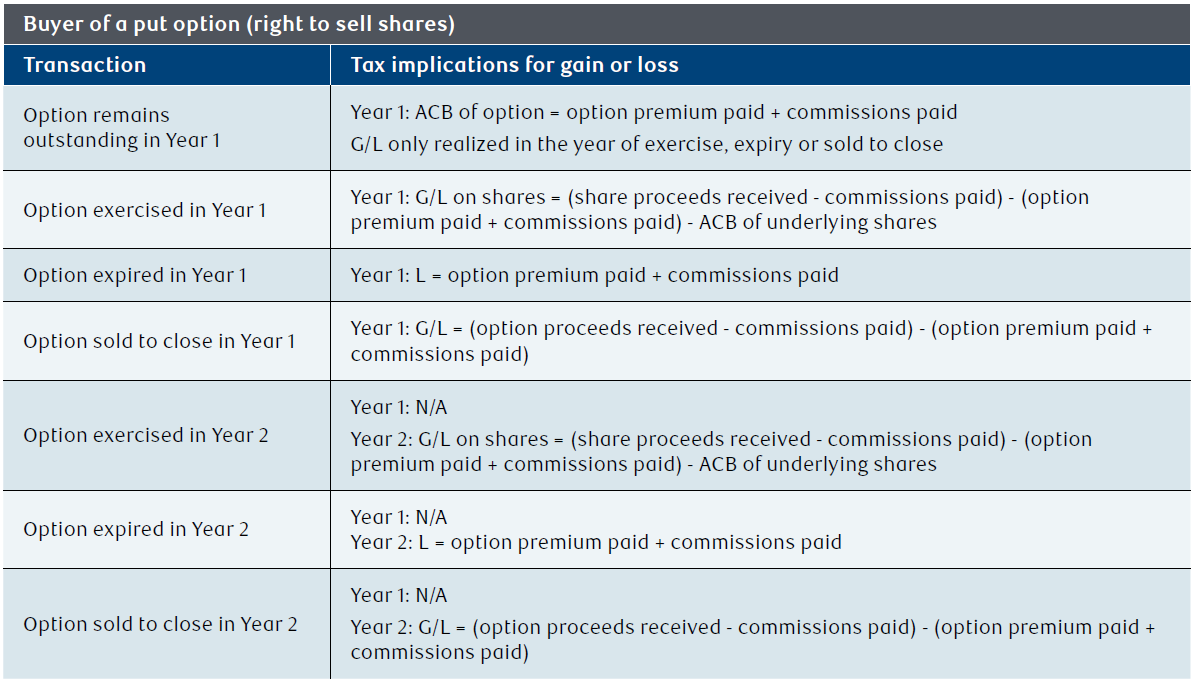

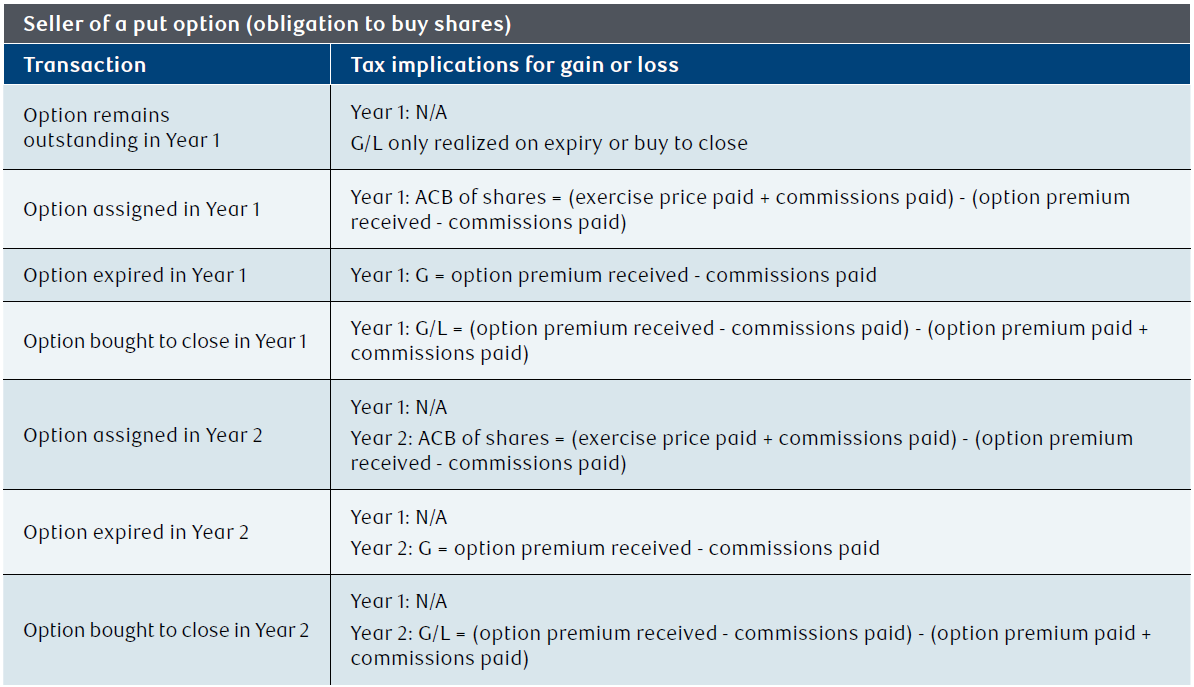

Timing of tax reporting of gains and losses on account of capital

The following tables describe the timing of tax reporting and calculation of gains and losses for call and put options transactions from the buyer's and the seller's perspective that are on account of capital. For the purposes of the table, it's assumed that the disposition of shares related to the options transactions will also be treated on account of capital. In more complex situations, this may not be the case, so it's important to seek professional tax advice.

Timing of tax reporting of gains and losses on account of income

The following tables describe the timing of tax reporting and calculation of gains and losses for call and put options transactions from the buyer's and the seller's perspective that are on account of income. For purposes of the table, it's assumed that the disposition of shares related to the options transactions will also be treated on account of income. In more complex situations, this may not be the case, so it's important to seek professional tax advice.

Conclusion

The tax treatment of options transactions is very complex. You first need to determine if the options transactions should be reported on account of income or capital. You then need to determine when the gains or losses are realized for tax purposes. To ensure your own circumstances are properly considered, it's strongly recommended that you seek advice from a qualified tax advisor before buying or selling options.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.