Ten strategies to pay less tax in retirement

Are you approaching retirement or have you recently retired? Maximizing your retirement income may be an important aspect of enjoying and making the most of this new phase of your life. This article discusses 10 common tax-saving retirement strategies to maximize your after-tax retirement income.

Are you approaching retirement or have you recently retired? Maximizing your retirement income may be an important aspect of enjoying and making the most of this new phase of your life. This article discusses 10 common tax-saving retirement strategies to maximize your after-tax retirement income.

Family Office Services

April 14, 2024

Ten strategies to pay less tax in retirement

Maximizing your after-tax retirement income

Are you approaching retirement or have you recently retired? Maximizing your retirement income may be an important aspect of enjoying and making the most of this new phase of your life. However, a large portion of your major sources of retirement income may be taxed at the top marginal tax rate with no preferential tax treatment.

Fortunately, there are several approaches you may want to consider to maximize your after-tax retirement income. Although not exhaustive, this article discusses 10 common tax-saving retirement strategies.

Any references to a "spouse" in this article also refers to a common-law partner.

The 10 strategies

- Strategy 1: Spousal RRSPs

- Strategy 2: Order of asset withdrawal

- Strategy 3: Tax-preferred investment income

- Strategy 4: Pension income splitting

- Strategy 5: CPP/QPP sharing

- Strategy 6: Spousal loan

- Strategy 7: Effective use of surplus assets

- Strategy 8: Prescribed life annuity

- Strategy 9: Tax-free savings account (TFSA)

- Strategy 10: Minimum RRIF/LIF/LRIF/PRIF withdrawal planning

Strategy 1 – Spousal RRSPs

Canada has a progressive tax system. The progressive nature of the system means that tax rates in Canada increase as your income increases. As a result, you could save significant amounts of tax, annually, if you and your spouse each earn $50,000 in taxable income as opposed to one of you earning $100,000, for example. In other words, a spouse with a higher income of $100,000 may end up paying more tax than if each spouse earned $50,000. With that in mind, equalizing your retirement income may help you achieve significant tax savings.

If you project your retirement income to be higher than that of your spouse, a simple way to equalize your future retirement income is by making contributions to a spousal RRSP.

If you're already retired, but you still have unused RRSP contribution room and your spouse has not yet turned age 72, you can continue to make spousal RRSP contributions even if you are over age 71. Furthermore, it's possible to create additional RRSP contribution room from rental property income or employment income, such as from part-time or consulting work, and contribute to your RRSP up to age 71.

Even with the pension income splitting rules, spousal RRSPs still have benefits. Under the pension income splitting rules, you can only reallocate a maximum of 50% of eligible pension income to your spouse. However, the full value of a spousal RRSP can be taxed in the name of your spouse.

If you and your spouse retire prior to age 65 and require income above and beyond whatever fixed sources are available (such as government income sources and a company pension), it may be beneficial for the family to be able to draw on a spousal RRSP or spousal RRIF owned by the lower-income spouse. The downside to withdrawing is that you would lose a few years of tax-deferred growth.

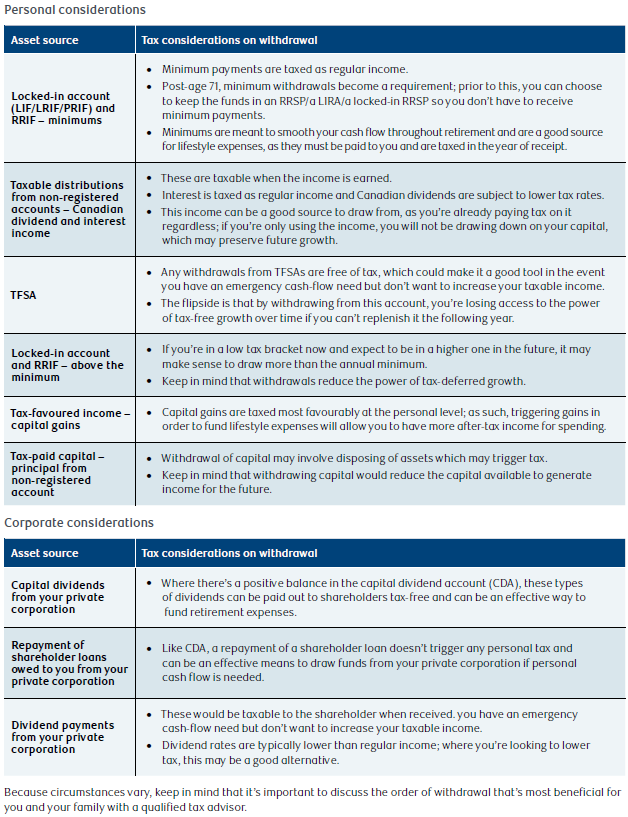

Strategy 2 – Order of asset withdrawal

In order to optimize your after-tax retirement income, it's important to determine where to withdraw assets from first to cover any income shortfalls you may have after receiving government and employer pensions. The appropriateness of each withdrawal source will be dependent on your asset types and mix during retirement.

To help determine the order that may be the most suitable for you to draw assets, consider the following asset withdrawal tables as a general reference guide. These tables are based on the understanding that it may be best to use your least-flexible sources of income first. After that, it's generally best to draw down on assets that trigger the least amount of taxation. Please note that this hierarchy is not fixed or set in stone and applicability will vary based on your personal circumstances.

Strategy 3 – Tax-preferred investment income

Consider holding your fixed-income or interest-bearing investments, such as bonds and guaranteed investment certificates (GICs), in your registered accounts (RRSP/RRIF and locked-in). Further, foreign dividends are not subject to the preferential tax treatment available to dividends received from Canadian corporations. Instead, this income is taxed as ordinary income, like interest. For this reason, high dividend-paying foreign stocks where capital appreciation is expected to be minimal may be better off held in a registered account.

Again, these are general guidelines only; depending on your total investable assets, contribution room and overall asset allocation, following these guidelines may not be feasible.

In a non-registered investment account, Canadian dividends, capital gains and return of capital are taxed at a lower rate than interest income. For this reason, you may be able to maximize your after-tax retirement income by holding investments that generate Canadian dividends, capital gains or return of capital income in your non-registered account. However, these investments typically carry higher risk than more conservative fixed-income investments and may offer greater returns or losses.

Strategy 4 – Pension income splitting

If you're in a higher tax bracket than your spouse, you may be able to reduce your family's total tax bill by allocating up to 50% of eligible pension income to your spouse. The tax savings can occur both federally and provincially where eligible pension income is allocated from a spouse in the higher marginal tax bracket to the spouse in the lower marginal tax bracket. The tax savings depend on a number of factors, including the amount of eligible pension income available to be split with your spouse, the difference in your marginal tax rates, and the impact the reallocation could have on certain government benefits and tax credits. For example, if you're subject to the old age security (OAS) clawback, splitting your eligible pension income with your lower-income spouse will reduce your net income, which may in turn reduce or eliminate your clawback.

If you're under age 65 during the entire tax year, you'll generally be able to split only the income that's paid to you directly from a defined benefit pension plan. Alternatively, if you're at least age 65 during the tax year, there are more types of income that can be split with your spouse, including RRIF/LIF/LRIF/PRIF income. Please note that RRSP withdrawals and CPP/QPP and OAS are not considered eligible pension income for income splitting purposes.

The decision of how much income to split, if any, is made when you prepare your income tax returns for the year in which the income was received. Remember that pension income splitting does not involve actually transferring the money to your spouse. You're only splitting the income on your tax return by completing a joint election with your spouse.

Strategy 5 – CPP/QPP sharing

Although the CPP/QPP pension is not considered eligible pension income for the purpose of pension income splitting (described in Strategy 4), you may achieve tax savings by sharing your CPP/QPP with your lower-income spouse. This may be a particularly viable strategy if you have a spouse with a limited working history, with minimal contributions to the CPP/QPP. This approach may lower your family tax bill and reduce OAS clawback where applicable.

To be eligible for sharing your CPP/QPP with your spouse, keep in mind that you must fulfill certain conditions. One requirement is that your spouse must be at least age 60 and receiving CPP/QPP pension benefits (unless they never contributed to CPP/QPP).

The pension sharing calculation process involves combining the CPP/QPP pension entitlement you and your spouse earned during the time you lived together (either as married/civil union or common-law/de facto spouses) and then allocating 50% of the combined total to each of you. Any individual entitlements you and your spouse earned prior to the time you lived together cannot be shared. Although pension sharing can reallocate up to 50% of your CPP/QPP pension to your spouse, it will not increase or decrease the overall combined pension benefit paid.

Strategy 6 – Spousal loan

Generally, you achieve no tax advantage when you simply give funds to your lower-income spouse to invest — this is because of "attribution". Where attribution applies, any investment income earned on gifted funds is attributed back to you, as if you had earned it yourself. This is where the spousal loan strategy may help you reduce your taxes payable.

By making a bona fide loan to your lower-income spouse at the Canada Revenue Agency (CRA) prescribed interest rate, you can avoid triggering the income attribution rules. Your spouse must make the annual interest payments. The prescribed rate in effect at the time your loan is established remains in effect for the lifetime of the loan. Your spouse can then invest the loan proceeds, and the investment income and capital gains earned will be taxed at your spouse's lower rate.

The benefit of this strategy comes down to the difference between the prescribed rate and the investment return. The lower the prescribed rate relative to the return on investments, the greater the opportunity to benefit from this strategy and have income taxed in your lower-income spouse's hands. Other factors that may impact the degree of tax savings you can potentially reap from this strategy include the types of investments (i.e. investment asset mix) your spouse purchases with the loan proceeds and the difference between your tax rate and your spouse's tax rate. For more information, please ask your RBC advisor for the article on spousal loans.

Strategy 7 – Effective use of surplus assets

With a growing senior population in Canada and generally longer life expectancies, many Canadians may be facing potentially escalating healthcare and long-term care costs. It's imperative that you're prepared for these contingencies before redirecting your surplus assets. Preparing a financial plan may help you determine your cash-flow needs and identify any surplus assets.

If your financial plan determines that you have surplus non-registered assets that you'll likely not need during your lifetime, even under very conservative assumptions, then consider directing these excess assets to other more effective uses. The following are three options which may be of interest.

Tax-exempt life insurance

If you're planning to leave some of your assets to your heirs upon your death and you won't need to use these assets during your lifetime, you may be paying high amounts of tax on the income generated on these assets. If this is the case, consider directing these highly taxed assets towards a tax-exempt life insurance policy, where the investment income can grow tax-free. This way, the taxes that would have been payable on these surplus assets during your lifetime could instead be paid directly to your beneficiaries in the form of a tax-free death benefit. Speak with a licensed life insurance representative to see if insurance makes sense for you.

Lifetime gifts

You may have surplus assets you won't need during retirement and beneficiaries, such as children and grandchildren, that you'd like to support. You may want to assist them with buying a home, paying for education costs, starting a business or paying for their wedding. If this is the case, it may not make sense to continue exposing the income from these surplus assets to your higher marginal tax rate. Instead, consider gifting some of these surplus funds now as an outright cash lump-sum gift. Before pursuing this option, keep in mind that gifting in this way means you'll no longer have control of these assets.

Establish a family trust for adult children or grandchildren beneficiaries

If you don't want to give your adult children or grandchildren control over your surplus funds, you may want to consider using the funds to establish a family trust. You can direct your surplus funds to the family trust through either a gift (irrevocable) or a demand loan (revocable). Your children and/or grandchildren beneficiaries can be beneficiaries of the trust. If structured correctly, the family trust can allow you to allocate income to your children or grandchildren and ensure it's taxed in their hands at their lower marginal tax rate. Be sure to speak with a qualified tax and legal advisor to ensure your trust is properly structured and meets your needs.

Strategy 8 – Prescribed life annuity

If you're retired, a conservative investor and not satisfied with your fully taxable cash flow from traditional non-registered fixed-income assets (e.g. GICs and government bonds), consider using some of these fixed-income assets to purchase a prescribed life annuity. The prescribed life annuity will provide a guaranteed income stream for your lifetime with the advantage of partial tax deferral.

If you're concerned your annuity will not provide any payout to your beneficiaries upon your death, an insured annuity may be an option. With an insured annuity, part of your annuity payment is used to pay the premiums on a life insurance policy to ensure that a death benefit is paid to your beneficiaries. You may also consider an annuity with survivorship for your spouse or a guaranteed payment term (e.g. five years, 10 years) that will pay the residual to your estate. Speak with a licensed life insurance representative to determine if a prescribed annuity makes sense in your circumstances.

Strategy 9 – Tax-free savings account (TFSA)

In retirement, you continue to be able to contribute money to a TFSA, up to your contribution limit. Although TFSA contributions are not tax-deductible, remember that the income and capital gains generated in the TFSA grow tax-free. Additionally, any money withdrawn from a TFSA is not taxable.

To the extent you have excess cash flow, contributing to your TFSA annually will help you to maximize your tax-free growth. Further, TFSA withdrawals have no impact on income-tested benefits like OAS, nor do they limit entitlement to other government plans like the guaranteed income supplement and the age credit.

Strategy 10 – Minimum RRIF/LIF/LRIF/PRIF withdrawal planning

If your pension income and non-registered assets sufficiently meet most of your retirement expenses, you'll likely need to withdraw only the mandatory minimum amount from your RRIF or from your locked-in plans each year.

The following are some strategies to maximize the tax deferral within your RRIF/LIF/LRIF/PRIF in order to maximize your after-tax retirement income:

- If your spouse is younger than you, you may be able to base your minimum annual RRIF/LIF/LRIF/PRIF withdrawal on your spouse's age in order to minimize the amount of the annual withdrawal, thereby keeping more assets in the registered environment to grow on a tax-deferred basis. Many of the provinces and territories have locked-in plan legislation that permits you to base your mandatory minimum payment on your spouse's age.

- Convert your RRSP/LIRA/locked-in RRSP to a RRIF/LIF/LRIF/PRIF as required by the end of the year in which you turn age 71, but don't make your first withdrawal until the end of the year in which you turn age 72; this may allow for increased tax-deferred growth.

- Withdraw the annual required minimum from your RRIF/LIF/LRIF/PRIF as a lump-sum at the end of each year. This may allow for more tax-deferred growth on your minimum payment.

Summary

Although the majority of retirement income sources are taxed at a high rate with no preferential tax treatment, there are some common strategies that may help you to maximize your after-tax income in retirement. Speak with a qualified tax advisor to see if any of the strategies discussed in this article can help you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.