TFSA over-contributions

The tax-free savings account (TFSA) is a flexible savings vehicle, which may help you reach your financial goals more quickly. However, accidentally over-contributing to this account may result in some hefty penalties, which can erode your savings. This article explains the rules around contributing to a TFSA, the tax implications of over-contributing, and what to do if you unintentionally over-contribute.

The tax-free savings account (TFSA) is a flexible savings vehicle, which may help you reach your financial goals more quickly. However, accidentally over-contributing to this account may result in some hefty penalties, which can erode your savings. This article explains the rules around contributing to a TFSA, the tax implications of over-contributing, and what to do if you unintentionally over-contribute.

Family Office Services

November 14, 2024

TFSA over-contributions

The tax implications and your options

The tax-free savings account (TFSA) is a flexible savings vehicle, which may help you reach your financial goals more quickly. However, accidentally over-contributing to this account may result in some hefty penalties, which can erode your savings. This article explains the rules around contributing to a TFSA, the tax implications of over-contributing, and what to do if you unintentionally over-contribute.

What is a TFSA?

The TFSA was introduced in 2009 as a way for Canadian residents to save and grow their savings in a tax-free manner. The maximum amount you can contribute is limited to your TFSA contribution room. Although the contributions you make are not tax-deductible, any income (including capital gains) you earn in a TFSA is exempt from tax. In addition, withdrawals (whether from capital or income) are generally tax-free and are added to your contribution room in the following year.

How much can I contribute?

Calculating your contribution room

The maximum amount you can contribute is limited to your TFSA contribution room. You automatically accumulate contribution room each year (starting in 2009) if you were a resident of Canada at any time during the year and you were at least 18 years of age.

Assuming you were at least 18 years of age in 2009 and have never contributed to a TFSA, you would have TFSA contribution room of $95,000 in 2024. The annual TFSA dollar limits from 2009 to 2024 are as follows:

Since you automatically accumulate contribution room each year, you don't have to open a TFSA account or file an income tax return to earn the contribution room. Further, your income level has no bearing on your contribution room. Any investment income earned within your TFSA or the value of your investments held within your TFSA also will also not affect your contribution room.

If you contribute less than your annual contribution limit, you can carry forward any unused contribution room indefinitely. Unlike registered retirement savings plans (RRSPs), there's no upper age limit that restricts your ability to contribute to a TFSA. Therefore, you can contribute to a TFSA past age 71. There's also no lifetime limit on the amount you can contribute.

You can generally withdraw any amount from your TFSA at any time, without tax consequences. A withdrawal will not reduce the amount of contributions you've made for the current year. Instead, the full fair market value of the withdrawal will be added to your contribution room at the beginning of the following year.

Your contribution room decreases with any contributions you make, including re-contributions of funds you've withdrawn in previous years.

The over-contribution penalty tax

An over-contribution occurs when your contributions to your TFSA exceed your TFSA contribution room. Unlike RRSPs which give you a $2,000 buffer for over-contributions, there's no buffer for over-contributions to your TFSA. You will be subject to a penalty tax of 1% on the highest excess amount in the month, for each month you're in an over-contribution position. Even if you've only been over-contributed for a few days in a certain month, you'll be charged the 1% penalty tax for the month and the 1% penalty tax will continue to apply for each month the excess amount remains in your TFSA.

To stop the penalty tax from accruing, you need to either withdraw the excess amount from your TFSA or receive new contribution room to absorb the over-contribution, which occurs on January 1 of the following year. There's no Canada Revenue Agency (CRA) form that needs to be completed in order to withdraw the excess amount.

The over-contribution filing requirements

You will need to file Form RC243, Tax-Free Savings Account (TFSA) Return, with the CRA by June 30 of the year following the year in which you made the over-contribution and pay any penalty taxes you owe by that date. You'll also need to complete and file RC243-SCH-A, Schedule A – Excess TFSA Amounts, to help you calculate the amount of taxes you owe. You should speak with a qualified tax advisor if you're in an over-contribution position.

Situations that may generate an over-contribution

Withdrawals and re-contributions

If you withdraw from your TFSA, the full fair market value of the withdrawal will generally be added to your contribution room at the beginning of the following year. For example, an amount you withdraw in 2024 can be re-contributed to your TFSA beginning January 1, 2025. If you re-contribute an amount withdrawn in the same year (without having unused TFSA contribution room), you may have over-contributed and be subject to the penalty tax.

If your funds are invested, you may need to liquidate your positions before making the withdrawal. This may be the case if your investments are proprietary to one financial institution or if you have investments in Guaranteed Investment Certificates (GICs) or mutual funds. A GIC may need to mature before you make the withdrawal and there may be early redemption fees associated with mutual funds.

How much you can re-contribute the following year depends on how much you withdrew from your TFSA. For example, let's say you invested $10,000 five years ago and your investment increased to $25,000 in the current year. If you withdrew the full $25,000 in the current year, then starting January 1 of the following year, you can re-contribute $25,000, plus the $7,000 of new contribution room earned for that year, for a total of $32,000 (plus any unused TFSA contribution room you carried forward from previous years). On the other hand, suppose you'd invested $10,000 but the investment decreased to $2,000. If you withdrew this amount in the current year, then starting January 1 of the following year, you can re-contribute only $2,000, plus the $7,000 of new contribution room earned for that year, for a total of $9,000 (plus any unused TFSA contribution room you carried forward from previous years).

Certain withdrawals are not added back to your contribution room for the following year. These include withdrawals of deliberate over-contributions, prohibited investments, non-qualified investments, amounts attributable to swap transactions, and any income or capital gains earned on any of these items.

Transfers between multiple TFSAs

You can maintain more than one TFSA, but you'll need to ensure the total contributions across your multiple TFSAs don't exceed your contribution limit.

If you wish to transfer funds from one TFSA account to another, or from one TFSA issuer to another, without tax consequences, ensure your issuer completes a direct transfer for you. If instead of a direct transfer, you withdraw funds from one of your TFSAs to contribute to another, it will be treated as a withdrawal and a contribution, which will affect your contribution room for the year. If you don't have sufficient contribution room, you will be over-contributed and may be subject to the penalty tax.

Transfers upon breakdown of a relationship

If you experience a breakdown in marriage or common-law partnership, you can directly transfer an amount from one spouse's TFSA to the other's TFSA without affecting either spouse's contribution room.

If you directly transfer TFSA assets to your former spouse's TFSA, your contribution room will not be reinstated at the beginning of the following year. This is because the transfer is not considered a withdrawal. Your former spouse will not need contribution room to accept the transfer. Also, the transfer will not remove any excess TFSA amount, if applicable, in your TFSA.

Alternatively, instead of transferring the amount directly, you may choose to withdraw assets from your TFSA and give these assets to your former spouse. In this case, the amount of the withdrawal will be added back to your contribution room in the following year. Your former spouse will only be able to contribute these assets to their own TFSA if they have unused TFSA contribution room. For further clarity, in this situation, your withdrawal will be considered a regular withdrawal and the former spouse's contribution will be considered a regular contribution which will reduce their TFSA contribution room.

Becoming a non-resident of Canada

Your TFSA contribution limit is not pro-rated for the year you move from or to Canada. You're entitled to the full amount of contribution room in either of those years. However, if you're a non-resident for an entire calendar year, you will not accrue contribution room for that year.

You can make a TFSA contribution up until the date you become a non-resident of Canada; if you make a contribution to your TFSA while you're a non-resident (whether or not you have the contribution room), you'll be subject to a 1% penalty tax for each month the contribution stays in your account. The penalty will continue to apply until you withdraw the full amount of the contribution from your account (and designate it as a withdrawal of non-resident contributions) or re-establish Canadian residency. Note that a partial withdrawal of a non-resident contribution will not proportionately reduce the penalty tax otherwise payable. It is necessary for you to withdraw the full amount of a non-resident contribution in order for the penalty tax to stop accruing.

If the contribution you made while you were a non-resident is also in excess of your TFSA contribution room, you may be subject to an additional penalty tax of 1% per month.

If the 1% penalty tax applies to you as a non-resident, you'll need to file Form RC243, Tax-Free Savings Account (TFSA) Return, and Form RC243-SCH-B, Schedule B – Non-Resident Contributions to a Tax-Free Savings Account (TFSA). If the contribution you made while you were a non-resident is also in excess of your TFSA contribution room, you may be subject to an additional tax of 1% per month and have to file Form RC243-SCH-A, Schedule A – Excess TFSA Amounts.

Generally, withdrawals (that are not excess contributions or contributions made while a non-resident) you make while you're a non-resident will be added back to your TFSA contribution room for the following year. Keep in mind that this contribution room will not be available to you until you re-establish Canadian residency.

Tracking your contribution room

The CRA will keep track of your contribution room and determine your available unused TFSA contribution room based on information provided annually by your TFSA issuer. However, TFSA issuers are only required to send TFSA information to the CRA once a year (by the last day of February of the following year). As such, it's important to remember that the CRA may have incomplete information about your TFSA contribution room, especially if you made contributions during the current year.

Using the CRA's services

Your TFSA contribution room information can be found by using one of the following CRA services:

• My Account for Individuals at canada.ca/my-cra-account

• MyCRA at Mobile apps at canada.ca/cra-mobile-apps

• Tax Information Phone Service (TIPS) at 1-800-267-6999

In addition, if you want to receive a TFSA Room Statement, you can call the CRA. You can also ask for a TFSA Transaction Summary which shows the information the CRA received from your TFSA issuer about your contributions and withdrawals. You can also view your TFSA Transaction Summary online by going to My Account for Individuals.

If the information the CRA has about your TFSA transactions is incomplete or if you've made contributions to your TFSA in the current year, you can use Form RC343, Worksheet – TFSA contribution room, to calculate your TFSA contribution room for the current year.

If you disagree with any of the information on your TFSA Room Statement, or TFSA Transaction Summary, including dates or amounts of contributions or withdrawals, you may wish to contact your TFSA issuer to verify the transaction details. If the information about your TFSA account is incorrect, the issuer can send the CRA a revised record so that the CRA can update their files.

Keep accurate records

Due to the delayed receipt of information by the CRA, you should also maintain accurate records to keep track of your own TFSA room. Your total TFSA contributions for the year should be shown on your statements from your TFSA issuer. You are ultimately responsible for determining your TFSA contribution room. If you over-contribute, you'll still be responsible for the penalty tax even if you rely on the CRA's records.

How will you know if you've over-contributed?

The CRA may send out an "excess amount letter" or a "proposed TFSA return" if you've over-contributed to your TFSA.

The excess amount letter

If you receive an excess amount letter and you've already removed the excess TFSA amount, you do not have to do anything else. If you haven't removed the excess, you should remove it immediately.

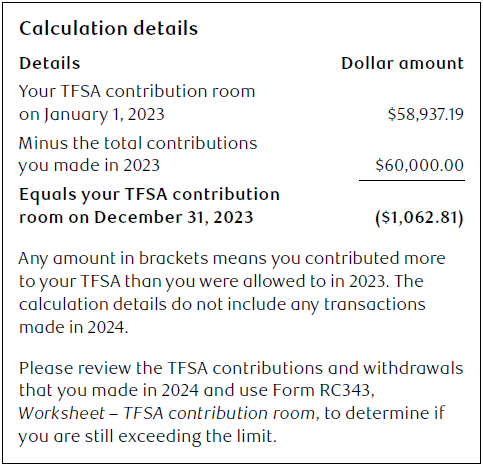

Here's an example of what the CRA's excess amount letter may look like:

You contributed more to your TFSA than you were allowed to in 2023. We determined this using the following information, which was provided by your financial institution(s):

The proposed TFSA return

If you receive a "proposed TFSA return" (i.e. RC243-P, Proposed Tax-Free Savings Account (TFSA) Return), it should show the penalty taxes you owe, based on the CRA's calculations. It also normally contains a cover letter, giving you instructions on how to respond to the proposed return.

If you agree with the information on the TFSA return, you can sign and date it, and make your payment per the instructions in the letter. The CRA will issue you an assessment based on this return.

If you do not agree with the TFSA return, you can send a letter to the CRA, including a detailed explanation and any supporting documentation you have about the excess contributions along with proof that your excess TFSA amount has been removed. The CRA will review your request and send you a letter explaining their decision. Even if you disagree with the TFSA return, consider whether to pay the penalty tax assessed. If the CRA accepts your appeal, they will reimburse you the tax paid.

In either case, you should respond to the CRA's proposed TFSA return. If they do not receive a response from you, they will issue an assessment based on the information on file which will include any applicable penalties and interest.

What to do once you've received your assessment?

You will receive formal assessment or reassessment from the CRA of your TFSA tax payable. If you disagree with the assessment or reassessment, you can make a formal objection by sending the CRA a completed Form T400A, Notice of Objection – Income Tax Act, or a signed letter to the Chief of Appeals at your tax services office or tax centre within 90 days of the date of the notice of assessment or notice of reassessment. For more information, see CRA's Pamphlet P148, Resolving your Dispute: Objections and Appeal Rights under the Income Tax Act.

Waiving or cancelling the TFSA taxes

You can ask the CRA to waive or cancel the TFSA penalty taxes by sending them a written letter, with supporting documents, explaining why the tax arose and why it would be fair to cancel or waive all or part of the tax. The CRA will review all factors including whether the tax arose because of a reasonable error. Being unaware of the tax rules is not considered a reasonable error. The CRA has clarified that a reasonable error means you didn't intentionally make excess contributions and that an impartial person would deem the over-contribution more likely than not to have occurred based on your specific circumstances.

In addition, to waive the penalty tax, the CRA will need to see that you've made one or more withdrawals without delay to reduce or eliminate the excess contributions to your TFSA. The CRA is unwavering on this condition. If you're unable to withdraw any amounts from your TFSA because the value of your investments has decreased to zero, the CRA will not waive the 1% penalty tax. Your excess TFSA will only be reduced once new TFSA contribution room becomes available in future years.

Conclusion

It's important for you to maintain and keep track of your available TFSA contribution room. If you over-contribute, you may be subject to penalty taxes. If you think you may have over-contributed to your TFSA, it's important to seek advice from a qualified tax advisor to determine the next steps that are most appropriate for you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.