The cash damming strategy

You may realize potential tax savings by converting personal debt (non-deductible) into tax-deductible debt through the cash damming strategy. If you own an unincorporated business or a rental property, this approach may help you reduce your overall tax liability and support your wealth-building goals.

You may realize potential tax savings by converting personal debt (non-deductible) into tax-deductible debt through the cash damming strategy. If you own an unincorporated business or a rental property, this approach may help you reduce your overall tax liability and support your wealth-building goals.

Family Office Services

January 14, 2024

The cash damming strategy

Reduce your taxes by restructuring debt

You may realize potential tax savings by converting personal debt (non-deductible) into tax-deductible debt through the cash damming strategy. If you own an unincorporated business or a rental property, this approach may help you reduce your overall tax liability and support your wealth-building goals. This article describes the cash damming strategy and highlights some of the potential issues you should consider before implementing this strategy.

The strategy

If you have personal debt, such as a mortgage against your home, the interest on that debt is likely not tax-deductible. Interest will only be deductible if the money you borrow is used for the purpose of earning income from business or property. Business income includes income you earn from a profession or trade, or any activity you carry on for profit. Property income generally includes interest income, dividends, rents and royalties. As an unincorporated business owner, the cash damming strategy allows you to use your business income to pay down personal (non-deductible) debt and then re-borrow to invest in your business, making the interest payments on your loan deductible for tax purposes.

To get started, you will need a line of credit or other loan facility. You'll borrow the funds from the line of credit and use them to pay your business expenses or to purchase investment assets. You'll pay down your personal debt using the funds received from your business operations.

If you own rental property, you may also employ the cash damming strategy. In this case, you pay your personal expenses directly out of rental income while you borrow money to finance expenses related to your rental property. Eligible expenses may include, but are not limited to, mortgage interest, property taxes, management fees, administration fees, and maintenance and repair costs. Please consult with a qualified tax advisor to confirm which other expenses relating to your rental property are eligible.

Maintaining interest deductibility

The cash damming strategy generally involves using separate accounts to segregate funds received from borrowed money and funds received from other sources, such as your business operations. This strategy centres on ensuring interest on the borrowed money remains tax-deductible. Therefore, it's very important to be able to directly link your borrowed funds to an income-earning purpose. Using a separate bank account to track borrowed funds and business expenses may help you keep track of which funds were used for each purpose.

Although cash damming using two separate bank accounts allows you to trace the use of your borrowed money more readily, it's not mandatory to have separate accounts. In situations where you deposit and commit the borrowed money into one account with other funds, the Canada Revenue Agency (CRA) allows you to allocate, on a dollar-for-dollar basis, the borrowed money to a specific identifiable use. In other words, you're permitted to look at all of the uses of the money in the account and link the borrowed funds to a specific use. However, you are required to place the borrowed funds into the account prior to or on the same day the funds were used.

Illustration

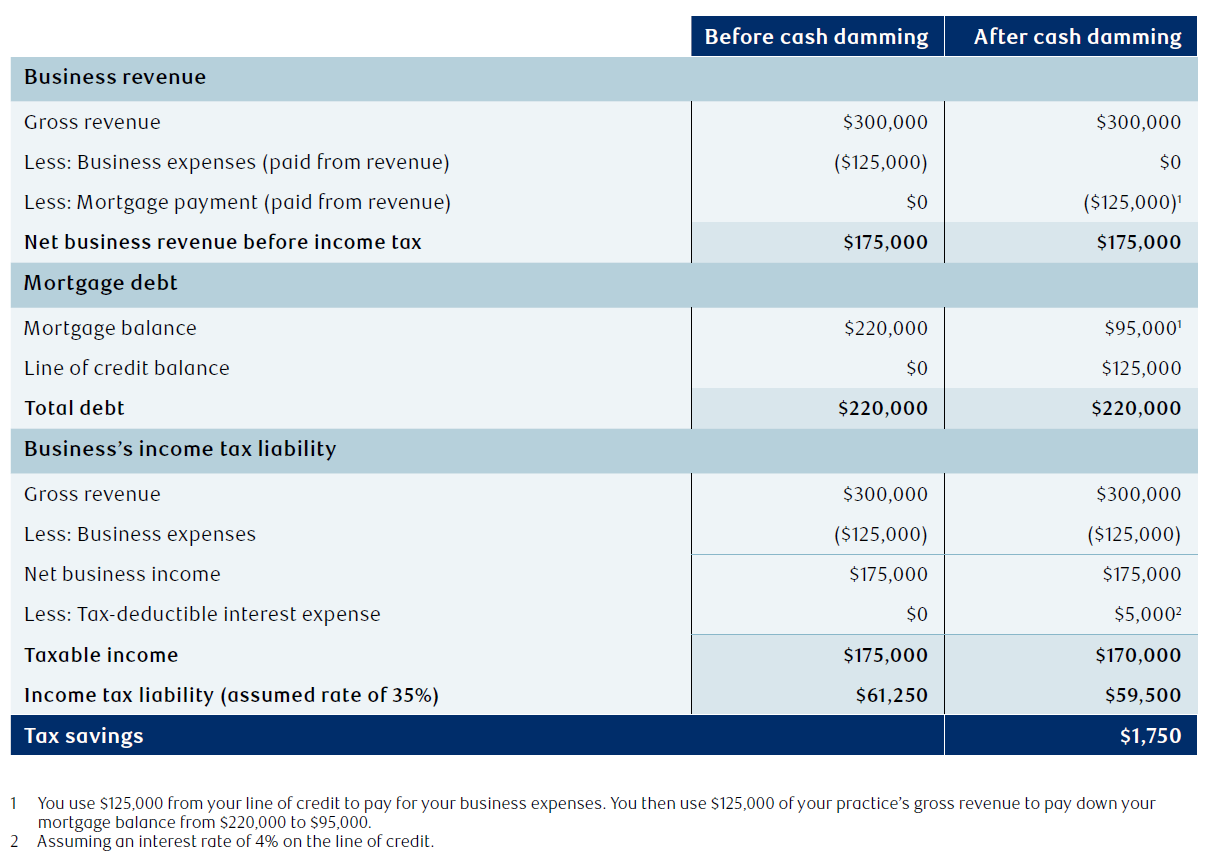

Let's say you're the owner of an unincorporated dental practice with two employees. You own a house with a $220,000 open mortgage, which gives you the freedom to pay down your mortgage without incurring penalties. In the current year, the gross annual income from your dental practice is $300,000, and your business expenses total $125,000. You decide to implement the cash damming strategy and use a line of credit to pay for ongoing business expenses while using your practice's gross revenue to pay down your personal non-deductible mortgage.

The key to this strategy is that interest paid on borrowed amounts used for business expenses is tax-deductible. Although your overall debt before and after using the cash damming strategy is the same (your mortgage decreased by as much as your line of credit increased), you effectively converted the non-deductible debt with tax-deductible debt. This conversion translated into tax savings of $1,750 for the year. If you continue to use your tax savings to make extra mortgage payments, you may be able to pay down your mortgage at a much faster pace than if you hadn't used the cash damming strategy. In the end, you will have no mortgage and a large tax-deductible business loan.

Alternatively, you could consider using the tax savings to reinvest in your business, pay down some of the business line of credit, save for retirement, or treat yourself to a vacation — the savings are yours to do as you see fit.

Is this strategy right for you?

Have you discussed financing options with your lender?

Paying off your mortgage or other debt ahead of schedule may trigger a prepayment penalty. Make sure you discuss your prepayment options with your lender well in advance. In addition, you may have difficulty securing a large business line of credit if you don't have sufficient collateral. Also, if the interest rate on your line of credit is higher than your mortgage rate, you'll need to determine if the income tax savings outweigh the incremental borrowing cost.

Do you have a long investment time horizon?

In the example illustration, the cash damming strategy is effectively converting your mortgage, which is a debt with a set time horizon, to an investment loan, which has an indefinite time horizon. Since the investment loan doesn't have set repayment dates, you'll need to have the discipline to repay the debt.

Do you have surplus cash flow?

It's important to understand the terms of the investment loan that you'll use to pay for your business expenses. Some loans require a monthly repayment that's a combination of interest and principal while other loans require interest-only payments. Ensure you have adequate surplus cash flow (i.e. after-tax income less expenses) from sources in addition to your business to pay the applicable monthly payments.

Your source of cash flow should also be sufficient to respond to the effects of changing economic conditions. An economic downturn might have a negative effect on your business's cash flow. An increase in interest rates may potentially increase your borrowing costs. If your borrowing costs increase, it's prudent to have enough cash flow to cover any interest increases as well as any potential demands for repayment.

What's your risk tolerance?

Your risk tolerance is a measure of how comfortable you are with taking on risk. Borrowing to invest, in your case in your business, may add an additional level of risk to your overall financial situation.

Will the tax-deductible interest cause alternative minimum tax (AMT)?

AMT is a parallel tax calculation that applies to certain high-income taxpayers who may otherwise pay little or no tax because of the deductions, exemptions and credits they claim under the regular tax system. AMT is designed to ensure these taxpayers pay at least a minimum amount of tax. Consequently, you're required to compute your tax liability by calculating your regular tax and AMT for federal tax purposes. You pay either the regular tax or the AMT, whichever is the highest. If you're required to pay AMT, it may be recoverable over the next seven years. As such, it's often seen as a prepayment of taxes.

The AMT rules limit the deduction of interest and carrying charges. For AMT purposes, you can only deduct 50% of the interest and carrying charges you would typically claim as a 100% deduction for regular tax purposes. If you're subject to AMT due to the interest expense claimed, you may need to re-evaluate the tax effectiveness of the cash damming strategy. For a detailed discussion on how the interest deduction would impact your AMT, please ask your RBC advisor for an article on AMT and the impact on individuals.

Conclusion

The cash damming strategy may allow you to convert your non-deductible debt into tax-deductible debt to create tax savings and build long-term wealth. Your RBC advisor, along with a qualified tax advisor, can help you evaluate whether this strategy and its associated benefits and risks make sense for you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.