The RRSP/RRIF meltdown strategy

The RRSP/RRIF meltdown strategy may be a tax-efficient way to replace some of your excess registered assets with non-registered assets using an investment loan. This article describes the meltdown strategy and highlights some of the potential issues you should consider before incorporating this borrowing-to-invest strategy into your overall financial plan.

The RRSP/RRIF meltdown strategy may be a tax-efficient way to replace some of your excess registered assets with non-registered assets using an investment loan. This article describes the meltdown strategy and highlights some of the potential issues you should consider before incorporating this borrowing-to-invest strategy into your overall financial plan.

Family Office Services

October 14, 2025

The RRSP/RRIF Meltdown Strategy

The RRSP/RRIF meltdown strategy may be a tax-efficient way to replace some of your excess registered assets with non-registered assets using an investment loan. This article describes the meltdown strategy and highlights some of the potential issues you should consider before incorporating this borrowing-to-invest strategy into your overall financial plan.

It's important to note that using borrowed money to finance the purchase of securities involves greater risk than a purchase using cash resources only. If you borrow money to purchase securities, your responsibility to repay the loan as required by its terms remains the same, even if the value of the securities purchased declines. The information in this article is not intended to provide legal or tax advice. To ensure your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax advisor before acting on any of the information in this article.

What is the Strategy?

Every dollar that's withdrawn from your registered plan is fully taxable at your marginal rate in the year you make the withdrawal. In addition, upon your death, assuming there's no qualifying beneficiary (e.g. a spouse or common-law partner), the full fair market value of the assets in your registered retirement savings plan (RRSP) or registered retirement income fund (RRIF) must be included in your income and may be taxed at the highest marginal tax rate.

The meltdown strategy is based on the theory that it's more tax-efficient to make withdrawals from your RRSP or RRIF earlier in life, when your tax rate may be lower than the rate you expect in the year of your death. The strategy involves obtaining an investment loan and paying the interest accrued on the loan with the deregistered funds from your registered plan. The withdrawals from your registered plan should equal the interest payment on your investment loan.

What you're accomplishing from a tax perspective is offsetting the income inclusion of your RRSP or RRIF withdrawal with an interest expense deduction resulting from your investment. With the funds from your RRSP or RRIF, you can create a tax-efficient portfolio and benefit from the preferential tax rates of capital gains and dividends outside of your registered accounts.

An Example Using a RRIF

One method of implementing the meltdown strategy involves using a RRIF. This is because no tax is withheld when you withdraw the minimum amount from your RRIF. It's only when you make a withdrawal in excess of the minimum that withholding tax applies. To explain how the meltdown strategy works, let's consider a simple illustration.

Suppose you borrow $50,000 at a 6% interest rate and directly invest the borrowed money in a non-registered portfolio of income-producing assets. This means you'd have to pay $3,000 in interest per year. In order to pay the $3,000 of interest, you'd draw $3,000 from your RRIF. Let's assume $3,000 is your minimum required payment so that no withholding tax applies. Since you used the borrowed money for the purpose of earning income, the interest on the investment loan should be deductible. Therefore, by borrowing to invest, you're able to offset the $3,000 RRIF income inclusion with a $3,000 interest deduction.

In theory, you've replaced $3,000 of registered funds with non-registered funds on a tax-free basis. The funds in your non-registered account may be invested in securities that generate tax-preferred types of income such as capital gains and dividends. With less assets in your registered accounts, you may have a smaller tax liability over your lifetime.

In addition, an added benefit of withdrawing funds from a RRIF is that you may be able to claim a pension income tax credit on up to $2,000 of that income, if you're age 65 or over at any point during the year you make the withdrawal.

What About Withholding Tax?

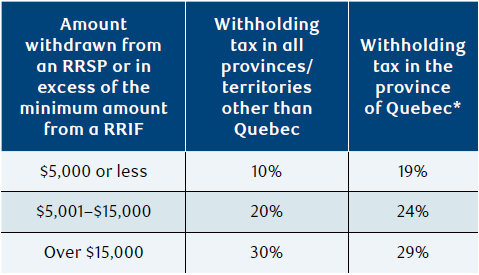

An added complexity to the meltdown strategy occurs when tax is required to be withheld. RRIF withdrawals in excess of the minimum or any RRSP withdrawals are subject to withholding taxes. The rate of withholding tax varies based on both the amount of your withdrawal and your province or territory of residence. The following table shows the percentage of withholding tax currently required when you make a single lump-sum withdrawal:

If you're withdrawing funds from your registered account where taxes are withheld, consider withdrawing a gross amount that's greater than the amount of interest owing on your investment loan. This is so the net amount you receive (after taxes are withheld) can be used to pay the interest on your investment loan. However, since the interest deduction will not be able to fully offset the gross amount you withdrew, you will owe tax on the difference. Let's look at an example of how to implement the meltdown strategy using funds from an RRSP.

An Example Using an RRSP

Using the information from our earlier example, let's again assume you borrowed $50,000 at a 6% interest rate and directly invested the borrowed money in a non-registered portfolio of income-producing assets. Your interest liability would be $3,000 per year. This time, in order to pay the $3,000 of interest, you want to withdraw from your RRSP. For withdrawals from an RRSP, there's generally a 10% withholding tax on amounts less than $5,000. Therefore, to cover the required interest expense of $3,000, you'll need to withdraw a gross amount of $3,333.33 from your RRSP. The additional amount of $333.33 withdrawal will be fully taxable and will not have a corresponding interest deduction.

Alternatively, if you withdraw only $3,000 from your RRSP, you'll receive a net amount of $2,700. You'll need to come up with an additional $300 to pay the $3,000 interest liability.

If the additional funds don't come from your RRSP or RRIF, you'll need to reduce your current cash flow in order to fund the difference. This will increase the tax cost of this meltdown strategy since you will be using after-tax dollars.

Given the consequences of either an increased tax liability or reducing your current cash flow to fund the difference, the meltdown strategy may not be suitable for you if you're withdrawing from your RRSP or withdrawing more than the RRIF minimum amount due to the taxes withheld.

Your Investment Mix

When implementing the meltdown strategy, you'll want to be mindful of creating an overall tax-efficient portfolio and benefitting from the preferential tax rates of certain investments when held outside of your registered accounts. For example, capital gains and Canadian dividends are taxed at more favourable rates than interest and foreign income. As such, from a tax perspective, it might make sense to focus on holding equity investments outside your registered accounts to benefit from the preferred tax treatment of capital gains and dividends. On the other hand, since interest income is fully taxable at your marginal tax rate, you may want to continue holding fixed income investments that generate interest income inside your registered plan to defer the tax.

While evaluating investments based on after-tax return is important, you should also consider other factors such as the investment's risk, diversification, the opportunity for capital appreciation and liquidity.

Determining if This Strategy is For You

What's Your Marginal Tax Rate?

The choice to withdraw funds early from your registered plan is a trade-off between the benefit of lower tax rates when the funds are withdrawn and the benefit of the years of tax-free growth within the registered plan. If your marginal tax rate today is not significantly less than it will be at death, this strategy may not make sense for you.

What's Your Time Horizon?

This strategy requires a time commitment to be effective. A long investment time horizon increases the probability that your investments will appreciate in value such that your total investment assets will exceed your loan plus interest costs.

On the other hand, this strategy becomes less efficient the longer you live after taking out the early withdrawals. This is because you're giving up the tax deferral that comes from leaving the assets in your registered plan. If you suspect you have a very long-term deferral time horizon, it will generally be more advantageous to leave the funds in your registered plan.

Do You Have Surplus Cash Flow?

Investment loans may require a monthly payment that's a combination of interest and principal. The withdrawal from your registered accounts should cover the interest payment on the loan, but you should ensure you have adequate surplus cash flow to make the principal repayments on your debt as well. If you don't have sufficient non-registered funds that can be used to make the principal repayments, you might need to use more registered funds. These registered funds will be taxed as income when withdrawn without any offsetting tax deduction.

Your source of cash flow should also be sufficient to absorb the effects of a market downturn. A market downturn could result in a potential increase in your borrowing costs as well as a decrease in the value of your investments. If borrowing costs increase, you should have enough cash flow to cover any loan interest payment increases. If the value of the investments within your RRSP decreases, your yearly withdrawals will not last as long as you intended them to. In addition, the investments you purchased with borrowed money will also have decreased in value, resulting in significant unrealized losses. In this situation, it's prudent to have enough cash flow to cover any potential demands for repayment. Lastly, if you decide to sell your investments at a loss, you'll need to come up with extra cash to pay off the difference between the outstanding loan balance and your investment proceeds.

What's Your Investment Risk Tolerance?

Your investment risk tolerance is a measure of how comfortable you are with taking risk in the hopes of earning greater returns on your investments. Most investments have some degree of risk associated with them, and borrowing to invest adds an additional level of risk to your investing. Borrowing to invest will magnify your returns when your investments are appreciating in value. This is due to the larger pool of investment capital that can benefit from investment growth. However, the downside is that if your investments start to decrease in value, your losses will be magnified as well.

How Will Your Retirement be Affected?

This strategy involves replacing registered assets that you'd intended on using during retirement with non-registered assets. You'll need to consider whether this strategy may jeopardize your ability to cover your expenses during retirement. Also, once you withdraw funds from your registered accounts, you're not able to recontribute the money back to your RRSP. That contribution room is lost forever.

Lastly, keep in mind that taking money out of your registered plan early may affect your income-tested benefits such as old age security.

Keeping Your Interest Tax-Deductible

One major attraction of this borrowing-to-invest strategy is the ability to deduct your interest expense for tax purposes. This deductibility allows you to increase the after-tax rate of return on your investment. In order to keep your interest deductible, here are some important points you should bear in mind:

What Can You Invest In?

If you want to deduct your interest expense, the borrowed money must be used for the purpose of earning income from a business or property. Business income includes any activity you carry on for profit or with a reasonable expectation of profit. Property income includes interest income, dividends, rents and royalties.

If you borrow money to purchase securities, the interest expense will generally be deductible if there's a reasonable expectation at the time you acquired the securities that you will receive income, such as interest or dividends.

If your investment generates a return of capital (ROC), the ROC must be reinvested to ensure all of the interest continues to be tax-deductible. Otherwise, a pro-rated interest expense calculation is required to determine the amount that may be deductible.

What if the Interest Expense Exceeds the Investment Income Earned?

The amount of income earned (or expected to be earned) does not affect the amount of interest you can deduct. For example, if you borrowed money at 8% to invest in something that earns 5%, you can generally deduct the full 8%.

Please note that if you live in Quebec, the provincial tax laws limit the interest you deduct in any given year to the investment income you earn in that year. For Quebec tax purposes, unused interest expense can be carried back three years and carried forward indefinitely to be deducted against investment income in other years.

Alternative Minimum Tax (AMT)

AMT is a parallel tax calculation designed to prevent individuals and certain trusts from paying little or no tax by limiting the tax advantages they could receive in a year through certain tax preferences, such as claiming certain deductions or earning tax-preferred income. You pay either the regular tax or the AMT, whichever is highest. In recent years, the government has introduced a number of changes to the AMT that may have broadened the impact it may have to high-income earners and most trusts.

For AMT purposes, you can only deduct 50% of deductible interest expense instead of 100% for regular tax purposes. This rule may have a significant impact on borrowing to invest and interest deductibility. To read more about the AMT, please ask your RBC advisor for an article on this topic.

What if You Dispose of Your Investments?

When you dispose of all or a portion of your investments, you'll need to identify the current use of borrowed money to determine the extent to which the interest remains deductible.

For example, if you invest the proceeds from the sale into a new income source, the entire interest expense should continue to be deductible. If you sell your investments at a loss, it's likely that the proceeds will only cover a replacement investment of lesser value. As long as you can trace the cost of the replacement investment to the entire original borrowed amount, the full amount of the interest expense should be deductible.

If you dispose of a portion of your investments and decide to pay down your investment loan with the proceeds from the sale, then the interest expense on the remaining portion of the loan will generally continue to be deductible. In the case where you dispose of all of your investments at a loss, the proceeds from the sale may not be adequate to pay off the entire outstanding loan balance. In this case, the interest expense on the remaining portion of the loan will generally continue to be deductible as long the original loan was used to purchase income-producing assets.

If you instead decide to use the sale proceeds for personal purposes (such as travel, renovating your home or paying down your mortgage), the interest on that portion of borrowed money can be deductible. Likewise, if you sell your investments at a loss, you'll need to identify what portion of the originally purchased investments has been disposed of, and a pro-rated interest expense calculation is required to determine the amount that remains deductible.

Conclusion

The RRSP/RRIF meltdown strategy may be a tax-efficient way to replace some of your excess registered assets with non-registered assets using an investment loan. However, it's an advanced planning strategy with associated risks.

This strategy is usually implemented once a sizeable amount of funds have accumulated in your registered plan, which is usually close to or at retirement. If you're either approaching retirement age or are already in retirement, you'll generally tend to have a lower risk tolerance, a shorter investment time horizon and possibly less potential surplus cash flow. Be sure to work with a qualified tax advisor to evaluate whether or not this borrowing-to-invest strategy makes sense for you.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.