U.S. estate tax: Canadians owning U.S. real estate

Understanding your exposure and strategies to minimize it. With a warmer climate in some parts of the U.S. and Canada's close proximity to American neighbours, many Canadians spend time in the U.S. This article takes a closer look at U.S. estate tax upon death due to ownership of U.S. real estate and various ownership structures, as well as planning strategies to limit your exposure.

Understanding your exposure and strategies to minimize it. With a warmer climate in some parts of the U.S. and Canada's close proximity to American neighbours, many Canadians spend time in the U.S. This article takes a closer look at U.S. estate tax upon death due to ownership of U.S. real estate and various ownership structures, as well as planning strategies to limit your exposure.

Family Office Services

June 14, 2025

U.S. estate tax: Canadians owning U.S. real estate

Understanding your exposure and strategies to minimize it

With a warmer climate in some parts of the U.S. and Canada's close proximity to our American neighbours, it's not surprising that many Canadians spend time (especially winters) in the U.S. If you're considering purchasing your own property in the U.S., it's important to understand the tax implications of ownership during your lifetime and at death. This article takes a closer look at U.S. estate tax upon death due to ownership of U.S. real estate and various ownership structures, as well as planning strategies you may want to consider to limit your exposure.

This article is intended for Canadian resident individuals living in Canada who are not U.S. persons (i.e. U.S. citizens or U.S. domiciliaries for U.S. estate tax purposes). Any reference to a spouse in this article refers to a person to whom you're legally married. For U.S. tax purposes, a spouse does not include a common-law partner. As well, unless otherwise stated, this article only addresses U.S. federal tax considerations; some U.S. states may have their own estate/inheritance tax system, which may apply to real estate located in that U.S. state. Many of the important income tax considerations of renting out or selling your U.S. property during your lifetime are discussed in a separate article you may obtain from your RBC advisor. It's important to seek the advice of a qualified cross-border tax and legal professional before acting on any of the information in this article.

U.S. estate tax overview

U.S. estate tax may apply to your estate at the time of your death if:

• the fair market value (FMV) of your worldwide estate exceeds the U.S. estate tax exemption threshold applicable in the year of death, and

• the FMV of the U.S. real estate, together with other U.S. situs property you own (i.e. property having a U.S. location or connection), exceeds US$60,000.

U.S. estate tax is calculated based on a graduated tax rate system, where the maximum tax rate of 40% applies to the FMV of taxable U.S. situs property that exceeds US$1 million. It's important to note that even if you won't incur a U.S. estate tax liability, your estate must still file a U.S. estate tax return if the FMV of U.S. situs property included in your taxable estate is greater than US$60,000. For more information about the calculation of U.S. estate tax for Canadians, please ask your RBC advisor for a separate article on that topic.

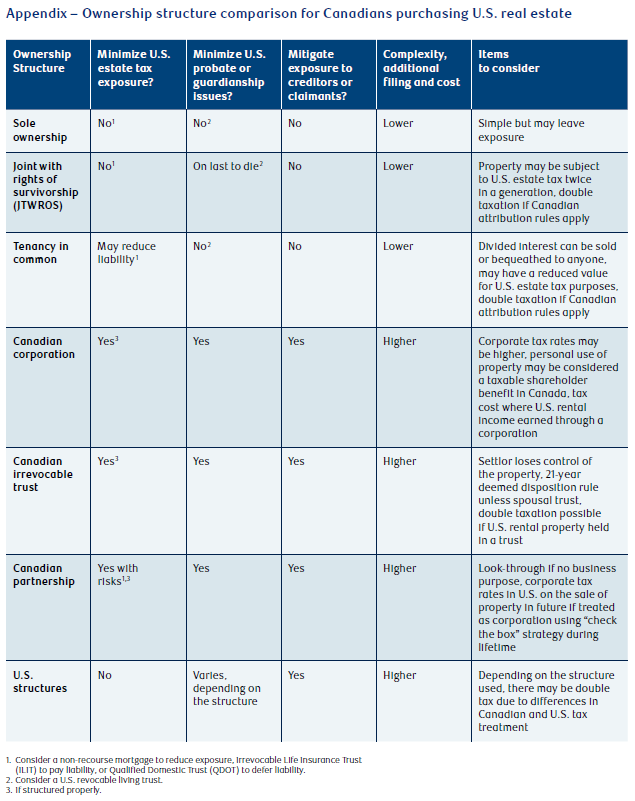

The form of ownership structure through which you hold your U.S. real estate may impact your U.S. estate tax exposure. To help you identify which form of ownership may suit your personal situation, various ownership structures and associated planning strategies are discussed in the following sections and are summarized in the appendix.

Sole ownership

Direct ownership of U.S. real estate in sole name may be one of the simplest and least costly structures to implement. However, this form of ownership may leave you exposed to U.S. estate tax and/or to potential creditors or claimants (especially where you plan to earn rental income from the property). Sole ownership may also expose the property to U.S. probate tax (which may be costly and a lengthy process). And, in the event you suddenly become incapacitated, even if you have a power of attorney, there could be administrative delays due to U.S. guardianship issues.

Sole ownership may be a viable ownership structure to consider when you can't justify the costs and complexities associated with more complex structures (discussed later) because your U.S. estate tax exposure isn't significant and/or you don't plan to hold onto the property for many years. Also, if you're the only one with available funds to make the purchase, some other low-cost co-ownership structures (discussed later) may not be appropriate.

When evaluating your exposure to U.S. estate tax, keep the following in mind:

• If you're married and plan to leave your U.S. real estate and other U.S. situs property to your surviving spouse or a properly structured spousal trust, your estate may claim a marital credit, which may minimize or eliminate your exposure to U.S. estate tax.

• If the U.S. real estate is expected to appreciate in value, your estate may claim a foreign tax credit for U.S. estate tax on your Canadian return. This may reduce your Canadian tax liability on capital gains triggered upon your death. A foreign tax credit is permitted only for Canadian federal tax purposes (i.e. Canadian provinces and territories do not permit foreign tax credits for U.S. estate tax).

• There are several estate planning tools you may consider implementing to mitigate your exposure, including: a non-recourse mortgage, irrevocable life insurance trust (ILIT), and a qualified domestic trust (QDOT).

The use of a U.S. revocable living trust to purchase U.S. real estate property may be suggested by some professional tax and legal advisors; this type of estate planning tool is discussed in a following section.

Non-recourse mortgage

The U.S. estate tax laws allow a deduction for debts (such as a mortgage on U.S. real estate) in determining your U.S. estate tax liability. A non-recourse mortgage offers a greater reduction to U.S. estate tax than a conventional mortgage. Since Canadians are only subject to U.S. estate tax on U.S. situs property, only a portion of a conventional mortgage outstanding on U.S. real estate owned is deductible. However, with a non-recourse mortgage, the full amount of the outstanding mortgage is deductible. Keep in mind, as with any mortgage, only a portion of the value of the property can be mortgaged, not the entire value; therefore, you may still have some exposure to U.S. estate tax. For more information on the use of a non-recourse mortgage to minimize your U.S. estate tax exposure, please ask your RBC advisor for a separate article on this topic.

Irrevocable life insurance trust (ILIT)

Purchasing a sufficient amount of life insurance to fund the payment of your U.S. estate tax liability may be a cost-effective strategy. It can provide your beneficiaries with a tax-free death benefit that may be used to fund the payment of your U.S. estate tax liability. If you're the insured on a policy you own, the death benefit is included in determining your worldwide estate value, which in turn may increase your exposure to U.S. estate tax. However, if you purchase the life insurance through an ILIT, the ILIT will own the policy and not you, so the death benefit received in the ILIT doesn't factor into the calculation of your U.S. estate tax liability. The cost effectiveness of this strategy will depend on the amount of U.S. estate tax exposure you have, the cost to set up the trust and the cost of the premiums, which are based on the status of your health and the coverage selected. For more information on the use of an ILIT, ask your RBC advisor for a separate article on common strategies to minimize U.S. estate tax for Canadians, which contains a section on this topic.

Qualified Domestic Trust (QDOT)

If you intend to transfer ownership of your U.S. real estate and other U.S. situs property to your surviving spouse upon your death, drafting your Will to provide your executor/liquidator the flexibility to transfer this property to a QDOT will allow your estate the option to defer your U.S. estate tax liability. A QDOT is an irrevocable trust for the benefit of your surviving spouse. The transfer allows a dollar-for-dollar deduction (marital deduction) against the value of the U.S. property included in your taxable estate. The deferral lasts until distributions of capital are made from the QDOT to your surviving spouse or your surviving spouse passes away. At that point, your estate is subject to U.S. estate tax based on the tax rates that existed in the year of your death and on the value of the property in the QDOT, including any growth of the property. Your estate can't claim both the marital credit (discussed earlier) and the marital deduction; it must choose to claim one or the other. Since the use of a QDOT only defers your U.S. estate tax, the QDOT could be included in your Will as a safeguard. Your estate may choose to use it only where there would still be a significant estate tax liability if your estate were to claim the marital credit. The deferral provided by using a QDOT can be especially helpful if much of the property of your estate is illiquid and not easily convertible to cash to pay for your U.S. estate tax liability. For more information about implementing a QDOT, please ask your RBC advisor for a separate article that discusses common strategies to minimize U.S. estate tax for Canadians, which contains a section on this topic.

U.S. revocable living trust

Some professional tax and legal advisors may suggest the use of a U.S. revocable trust to purchase U.S. real estate property. While this type of trust will not mitigate U.S. estate tax exposure, it may avoid U.S. probate tax and delays associated with U.S. guardianship issues due to incapacity. However, Canadians may potentially be exposed to tax and estate planning issues, for example, when they transfer property into these trusts, due to differences in the Canadian versus U.S. tax and legal treatment of U.S. revocable living trusts. For more information on U.S. revocable living trusts for Canadians, please ask your RBC advisor for a separate article on this topic.

Joint tenants with rights of survivorship (JTWROS)

JTWROS is a low-cost and simple form of co-ownership (not applicable to Quebec residents) where on the death of a joint tenant, their interest in the property passes outside of their estate directly to the surviving joint tenant(s). Like sole ownership, this form of ownership may leave you exposed to U.S. estate tax and/or to potential creditors or claimants. As your interest in the property automatically transfers to the surviving joint tenant, it may not be possible to transfer your interest to a trust, such as a QDOT, in order to defer your U.S. estate tax liability. However, the strategies involving the use of a non-recourse mortgage and ILIT may be considered for property held as JTWROS.

Owning U.S. real estate as JTWROS may be a structure to consider for Canadian spouses in cases where there's minimal to no U.S. estate tax exposure regardless of whether either spouse dies first, they die simultaneously, or the surviving spouse dies. The advantage to holding property as JTWROS, as opposed to holding it in sole name, includes minimizing U.S. probate complexities upon the death of a joint tenant, as well as not having to deal with U.S. guardianship issues in the event of incapacity. However, the risk of U.S. probate and U.S. guardianship issues will apply to a surviving spouse who will own the property in sole name when one of the joint tenants passes away. These risks also apply in the (less likely) event that both joint tenants die simultaneously. Some tax advisors may suggest that spouses use a joint U.S. revocable living trust to purchase the property in order to mitigate these risks.

When U.S. real estate property is owned as JTWROS by spouses and the contributions made by each spouse to purchase the property were not equal, there may be double taxation. This is due to differences in the Canadian and U.S. income tax treatment of the income and gains earned from the property. For example, due to the Canadian income attribution tax rules, for Canadian income tax purposes, when one spouse contributes all of the funds to purchase the U.S. real estate held as JTWROS, that spouse is subject to Canadian income tax on all income and gains earned on the jointly owned property. However, for U.S. income tax purposes, both spouses may be required to report the income and gains on the property equally, and each of them are subject to U.S. income tax. Double tax may result because, on the Canadian income tax return of the joint tenant spouse who reports all of the income and gains, a foreign tax credit can't be claimed for the U.S. income tax incurred by the other spouse.

In such cases, you should consider whether it makes sense to sever the joint tenancy and hold the property as tenants in common. The U.S. gift tax rules must also be considered. For example, for spouses, U.S. gift tax does not apply at the time the property is placed into ownership as JTWROS. However, if you sever the ownership of the property other than based on each spouse's relative contribution to the purchase of the property, or if the proceeds on the sale of the property aren't distributed based on the relative contributions of each spouse, the spouse who contributed more of the funds will be considered to have transferred a portion of their ownership in the property to the other spouse. This may trigger a U.S. gift tax liability if the amount exceeds the annual exclusion. If a joint tenant is someone other than your spouse, such as another family member, U.S. gift tax (when the gift exceeds the annual exclusion) is triggered right when the U.S. real estate is placed into ownership as JTWROS and there's an unequal contribution of funds by each joint tenant.

Double U.S. estate tax exposure

When there's U.S. estate tax exposure on property held as JTWROS, there may also be double U.S. estate tax (i.e. U.S. estate tax upon your death and U.S. estate tax upon your surviving joint tenant's/tenants' death). In this case, it may not be advisable to hold property as JTWROS.

For U.S. estate tax purposes, the entire value of U.S. real estate held as JTWROS is included in the estate of the first joint tenant to pass away, unless it can be demonstrated (with appropriate records) that the surviving joint tenant(s) contributed to the purchase of the property. When this is possible, only the proportionate share of the property based on the deceased joint tenant's contributions will be included in the deceased joint tenant's estate. Note that in the event you hold U.S. real estate as JTWROS with your spouse and your spouse passes away within 10 years of your death, your spouse's estate may claim a credit relating to any U.S. estate tax paid by your estate based on your interest in the property that was held as JTWROS. This will minimize the potential for double U.S. estate tax. However, the credit is significantly reduced on a sliding scale after two years from your date of death.

There are other estate planning issues to consider. Your interest in U.S. real estate property held as JTWROS with your spouse will automatically transfer to your surviving spouse upon your death. Therefore, your executor/liquidator may be limited in their flexibility to carry out certain estate planning. For example, if a married couple owns a real estate property in Arizona as JTWROS, they will not be able to transfer their interest in the property under Canadian law on a tax-deferred basis to a testamentary spousal trust, which can be structured to protect the property from U.S. estate tax upon the surviving spouse's death. This may result in the property being subject to U.S. estate tax twice in the same generation. Also, as discussed earlier, if your U.S. estate tax liability is significant, you may not be able to transfer your interest in the property to a QDOT in order to defer your U.S. estate tax liability.

Tenancy in common

Tenancy in common is a form of co-ownership where each tenant may own an equal or unequal share of U.S. real estate. You may be exposed to U.S. estate tax, potential creditors or claimants, U.S. probate and/or guardianship issues. However, the strategies involving the use of a non-recourse mortgage, ILIT, QDOT and a U.S. revocable living trust may be considered to mitigate against exposure.

Each tenant can sell their share of the property to a third party, mortgage their interest in the property, use it as collateral for a loan, or gift their interest in the property to someone else without requiring the consent of the other tenants. On the death of a tenant, their interest in the property does not pass to the surviving tenants but rather passes through their estate according to their Will or, if they have no Will, intestacy legislation.

Holding U.S. real estate as tenancy in common may be an ownership structure to consider if two or more individuals (including married couples) will not contribute funds equally to the purchase of U.S. real estate and they have low to no exposure to U.S. estate tax. It can be a viable solution for spouses who currently have ownership of U.S. real estate as JTWROS but have made unequal contributions to purchase the property and are therefore subject to the tax issues discussed earlier.

For U.S. estate tax purposes, if U.S. real estate is owned as tenants in common, only the deceased tenant's share in the property is subject to U.S. estate tax, not the full value of the property. If the U.S. tax laws in place at the time of death permit, the value of the deceased tenant's share of property held as tenants in common may potentially be determined by applying a certain discount that would reflect a lower market value of the property because it's partially held by another tenant. A discounted market value will result in a lower U.S. estate tax liability on the property.

For married couples, each spouse's share may be transferred to a testamentary spousal trust upon their death, which may be structured to protect the property from U.S. estate tax on the surviving spouse's death. And there may be the option to transfer this share to a QDOT, thereby deferring the U.S. estate tax liability, where there is a significant U.S. estate tax liability.

Ownership as tenants in common should be based on each spouse's contribution made to purchase the property. If one spouse contributes all of the funds to purchase U.S. real estate held as tenants in common, then the same income tax issues (double taxation) with respect to owning U.S. real estate as JTWROS may apply. Also, U.S. gift tax may apply at the time one spouse funds the purchase of the property and places the property in ownership as joint tenants in common with the other spouse. Even if one spouse buys the entire property and then provides additional funds to the other spouse for that spouse to purchase a portion of the property to hold as tenants in common, U.S. gift tax may apply. The same U.S. gift tax issues will apply if these transactions occur with other individuals, including a child or other family members.

Canadian corporation

U.S. situs property such as shares of a U.S. corporation or U.S. real estate held in a bona fide Canadian corporation (i.e. a company incorporated in Canada) are generally not subject to U.S. estate tax. However, if U.S. real estate held inside a Canadian corporation is a vacation property, it's possible that the Internal Revenue Service (IRS) may be of the view that the corporation is insulating the property (that's intended for personal use) from U.S. estate tax. As a result, the IRS may disregard the structure and consider the property to be a U.S. situs property that you own directly. The risk is greater if the corporation doesn't follow all legal requirements and formalities, and the finances of the company are intermingled with personal accounts. This may be the case, particularly if you've transferred the property to the corporation, the real estate is the corporation's only property, the property is only used by you and your family, and/or corporate formalities are not followed. The risk of the IRS disregarding the structure is lower for U.S. rental property held in the corporation, provided the corporate formalities are followed.

U.S. real estate owned by a corporation is not generally subject to U.S. probate and U.S. guardianship issues, although there could be delays in dealing with property in a corporation absent any planning. For example, if the corporation has a sole shareholder and no other company directors are able to immediately act on behalf of the corporation, there may be delays in dealing with the property should the sole shareholder suddenly die or become incapacitated. A corporate structure may help to mitigate exposure to potential creditors or claimants, which may be especially desirable if you will own U.S. real estate that will be used to earn rental income. Purchasing U.S. real estate in a Canadian corporation may be considered in situations where the funds needed to make the purchase are in the corporation and there would be significant Canadian tax triggered if funds from the corporation are withdrawn to make the purchase personally. However, there are costs to implement a corporate structure and income tax and estate tax implications to consider, which could make this structure less desirable for holding U.S. real estate than other forms of ownership.

For U.S. income tax purposes, the entire capital gain triggered on the sale of U.S. real estate is taxable. For property held in a corporation, the capital gain would be subject to the U.S. federal corporate tax rate, currently at a flat rate of 21%. However, in some states which do not levy a personal income tax, such as Florida, there is a state corporate income tax that may result in some additional percentage points to your overall corporate tax rate. In comparison with ownership by individuals, trusts, estates and partnerships, if the property is held for at least one year, there are flat preferential long-term capital gains tax rates (based on your income tax bracket) which may result in a lower flat tax rate on the capital gain compared to the overall capital gains tax rate it would be subject to in the corporation.

Also, from a Canadian income tax perspective, if you own U.S. vacation property in a Canadian corporation, the Canada Revenue Agency (CRA) may assert that the use of such property rent-free represents a taxable shareholder benefit to you. This benefit would be included as taxable income on your personal income tax return. There is an administrative exception to this CRA policy only if you had established the Canadian corporation on or before December 31, 2004, for the sole purpose of holding U.S. vacation property for use by you and your family and certain other criteria is met.

While the Canadian shareholder benefit rules may not apply where the property held is income producing, there's still generally a tax cost to earning passive income inside a Canadian corporation. This means your overall combined tax rate, for both corporate and personal, may be higher than if the rental property is held personally. If the corporation doesn't earn a profit from the rental income due to expenses and allowable depreciation, these income tax issues may not apply.

Lastly, a separate corporate income tax return would be required for both U.S. and Canadian income tax purposes.

It's important to seek advice from a qualified cross-border tax and legal professional to understand both the income tax and estate planning implications with this structure.

Canadian trust

A properly structured Canadian irrevocable inter vivos trust for U.S. real estate may mitigate against U.S. estate tax exposure. It may also help to reduce exposure to potential creditors or claimants and minimize U.S. probate and U.S. guardianship issues due to incapacity. However, there are significant costs to implement a trust and both U.S. and Canadian tax implications need to be considered, particularly if you already own U.S. real estate property. For example, there's a disposition for Canadian income tax purposes for transfers of property to a trust (except for transfers to certain types of trusts, such as a qualified spousal trust). There may also be U.S. gift tax as a result of a transfer to a trust. Since the Canadian tax rules don't allow a foreign tax credit to be claimed for U.S. gift tax, there may be double taxation.

This ownership structure may be beneficial if you haven't yet purchased the U.S. real estate property, you intend to buy and own the property for many years, and you expect throughout your lifetime that you or your family will have a significant amount of U.S. estate tax exposure. This trust structure can be particularly beneficial for a married couple where one spouse who has the funds to make a purchase creates a Canadian trust and funds it with the required amount of cash for the purchase. The trust may be structured to allow the other spouse to be a trustee and beneficiary. Children may also be included as beneficiaries now or upon the beneficiary spouse's death. To provide U.S. estate tax protection to the beneficiaries, the trust must be structured to ensure the beneficiaries don't have a general power of appointment. Also, the trust must be structured so the spouse who creates and funds the trust does not have a retained interest. This means they can't be a trustee of the trust nor have an interest in the property of the trust. In essence, this spouse must be willing to no longer have control of the funds transferred to the trust. The spouse who's a beneficiary of the trust may allow the other spouse to use the property. However, if the spouse who's a beneficiary of the trust dies first, the surviving spouse will need to pay market rent to the trust to demonstrate that they don't have a retained interest.

The use of this trust structure avoids some of the negative Canadian tax consequences associated with owning U.S. real property inside a Canadian corporation. However, the annual income tax filing requirements and the loss of control of the funds contributed to the trust may not make this structure desirable to everyone. In addition, all of the capital property in a Canadian trust is generally subject to a deemed disposition every 21 years of the trust's existence (unless the trust qualifies as a certain type of trust, such as a qualified spousal trust).

In addition to increased income tax filings required and associated compliance costs, rental income or capital gains (from the sale of the property) will be subject to income tax. U.S. rental income and capital gains in some instances may be subject to Canadian income attribution rules or Tax On Split Income (kiddie tax) rules. This may result in higher or even double taxation. For example, if there's inadequate planning, the income attribution rules would apply if rental income and capital gains on the sale of the property are allocated by the terms of the trust to your spouse as a beneficiary of the trust. This would result in the rental income and capital gains being taxable on your personal Canadian income tax return as the settlor of the trust. However, the rental income and capital gains would be taxable in the U.S. on your spouse's personal U.S. income tax return. This would result in double tax because you can't claim a foreign tax credit for the U.S. income tax incurred by your spouse. Double tax would not apply if the income and capital gains are taxed in the trust, but the Canadian tax rate of a trust is the top marginal tax rate, which could result in a higher overall tax.

Canadian partnership

There is a level of risk associated with the use of a Canadian partnership to provide U.S. estate tax protection. The IRS provides little guidance regarding the application of U.S. estate tax to a non-U.S. person with an interest in a Canadian partnership that owns U.S. situs property such as U.S. real estate. The risk is that the IRS might look through the partnership and consider you to own the underlying U.S. property as opposed to looking at the situs of the partnership itself based on the country where the partnership was organized. Also, while a Canadian partnership is generally not subject to U.S. probate and may be structured to mitigate exposure to potential creditors or claimants, it does not protect you from exposure to U.S. guardianship issues. The strategies that involve the use of a non-recourse mortgage, ILIT, QDOT and U.S. revocable living trust may potentially be considered.

Due to these risks, it's important to seek advice from a qualified cross-border tax and legal professional regarding the use of this structure to mitigate U.S. estate tax exposure. This structure may be considered where you already own U.S. real estate directly (solely or jointly with someone else), there's a significant exposure to U.S. estate tax, you've determined with advice from a qualified tax advisor that the use of a corporate structure does not make sense and there would be a significant U.S. gift tax that prevents the use of a trust structure to mitigate U.S. estate tax exposure.

There are U.S. income tax rules that may potentially mitigate the risk of U.S. estate tax. For example, for U.S. income tax purposes, it is possible for a partnership to make an election (referred to as a "check the box" election) to be treated as a corporation. Therefore, if a Canadian partnership makes this election, the partnership would be treated as a Canadian corporation for U.S. income tax purposes. As a partner, you would be considered to own shares of a Canadian corporation for U.S. tax purposes. However, the IRS would only recognize this election for U.S. income tax purposes, if the partnership is a business entity separate from its owners. The election could be disregarded if the partnership doesn't have a business purpose. Holding some business or investment property in the partnership and respecting the legal partnership structure may reduce the risk of the election being disregarded. Where a valid election is made, it's possible that U.S. real estate held by a Canadian partnership that is treated as a corporation for U.S. tax purposes may mitigate U.S. estate tax exposure.

What makes ownership through a partnership appealing is that it may be structured to provide similar creditor protection benefits afforded by a corporate structure without the negative income tax implications. For example, it's possible for a Canadian partnership to be structured to provide partners with limited liability by including a corporation as a general partner that holds a 1% partnership interest, while you as a limited partner would hold the other 99% limited partnership interest. Also, this structure will continue to be a partnership for Canadian income tax purposes even though it may make an election to be treated as a corporation for U.S. income tax purposes. As a partnership, some of the negative Canadian income tax consequences of owning U.S. real estate inside a corporation (e.g. shareholder benefit rules for vacation property) would not apply.

It's important to note that when a Canadian partnership elects for corporate status, for U.S. income tax purposes, there's a deemed disposition of the U.S. real estate owned by the partnership and you're subject to U.S. income tax on the accrued gains. The gain would be subject to preferential long-term capital gains tax rates if held for at least one year. Under the Canada-U.S. Income Tax Treaty, there may potentially be relief that would allow a disposition of the property for Canadian income tax purposes, which would allow you to avoid double tax by claiming a foreign tax credit to reduce or eliminate the Canadian tax on the deemed disposition of the U.S. property. Without the election, this capital gain may not be triggered for Canadian tax purposes until the property is sold or deemed disposed of upon the death of the partner. This could result in double tax since a foreign tax credit for U.S. income tax triggered in prior years can't be claimed on your Canadian income tax return in a future year.

As the property could potentially be sold during your lifetime, you may wish to preserve the availability to claim preferential long-term U.S. capital gains tax rates (which are not available for property held in a Canadian corporation) and avoid the risk of double taxation, by waiting and having your estate make a retroactive election upon your death. A retroactive election may be made within 75 days following your death. This would result in the matching of both the timing of Canadian and U.S. income tax, the ability to claim a foreign tax credit to minimize double taxation, and the potential to avoid U.S. estate tax.

U.S. structures

There are a number of U.S. structures such as a U.S. limited partnership, a U.S. limited liability company (LLC), a U.S. C corporation and other similar structures in the U.S. that U.S. persons residing in the U.S. (i.e. U.S. residents) may use to own U.S. real estate. Canadians who own U.S. real estate directly in these structures are exposed to U.S. estate tax and potentially negative income tax implications such as double taxation due to differences in the Canadian versus U.S. income tax treatment of some of these structures. For example, U.S. residents are often advised to hold U.S. rental properties in a U.S. LLC structure; however, there are double tax issues for Canadian residents. As a result, this structure is not recommended for Canadian residents. A detailed discussion of the potential tax and estate planning issues that apply when using certain U.S. structures is beyond the scope of this article. The key message is that Canadians must seek advice from a qualified cross-border tax and legal professional who will review both the Canadian and U.S. tax and estate planning implications (including U.S. state implications) that may apply.

Evaluating your options

There are many factors, including Canadian and U.S. income tax implications, U.S. gift and estate tax exposure, and U.S. probate and guardianship issues, that must be considered when determining the most appropriate ownership structure for you to own U.S. real estate. You should also consider your long-term intentions for the property, giving thought to how long you want to own the property, whether the property will be used to earn income, and whether you want the property to be maintained for the benefit of future generations of your family.

There's no single approach that's right in all circumstances and, as with many complex decisions, there will be trade-offs. For example, you may not want to deal with the administration and cost required by some of the more complex strategies to reduce or minimize your U.S. estate tax exposure. In any case, it's very important to consult with a qualified cross-border tax or legal professional who can help you review your specific situation to determine an appropriate approach that you're comfortable with.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified cross-border tax, legal and/or insurance advisor before acting on any of the information in this article.