Using a family trust for a prescribed rate loan

A family trust can be used to implement a prescribed rate loan income-splitting strategy to help reduce a family's tax burden. This arrangement is typically beneficial for families where one member has significantly more taxable income than the other family members.

A family trust can be used to implement a prescribed rate loan income-splitting strategy to help reduce a family's tax burden. This arrangement is typically beneficial for families where one member has significantly more taxable income than the other family members.

Family Office Services

March 14, 2025

Using a family trust for a prescribed rate loan

A family trust can be used to implement a prescribed rate loan income-splitting strategy to help reduce a family's tax burden. This arrangement is typically beneficial for families where one member has significantly more taxable income than the other family members. This article outlines the basics of using a family trust for a prescribed rate loan arrangement.

Any reference to a "spouse" in this article includes a common-law partner. Any reference to a "trustee" or "beneficiary" in this article includes the original or substituted individual, whether singular or plural.

The strategy at a glance

If structured properly, a family trust may allow a higher-income family member, such as a parent or grandparent, to split income with their lower-income family members. For example, assume you are a high-income earner. The strategy is aimed at shifting future investment income that would otherwise be taxed in your hands at a high marginal tax rate, to your lower-income spouse, children or other family members, in order to take advantage of their lower marginal tax rates.

This strategy involves you loaning funds to a family trust at the Canada Revenue Agency's (CRA) prescribed interest rate in effect at the time the loan is made. The loan is backed by a promissory note and a loan agreement which sets out the terms of the loan. The trustee will then invest the borrowed funds for the purpose of generating investment income. To the extent that the investment income can be allocated to your lower-income family members by the trustee, that income will be taxable to your family members at their lower marginal tax rate, which effectively reduces your family's overall tax bill.

You might be wondering why you can't simply gift money to your family, or to a trust for the benefit of your family, have your family or the trustee invest the funds, and have the income generated on those funds taxed in your family's own hands. The reason is because there are attribution rules designed to prevent certain types of income splitting between you and your spouse or your minor relatives. The result of triggering the attribution rules is that the income earned on funds gifted directly to certain family members, or income allocated to certain family members through a trust, will be taxed in your hands. This effectively defeats your ability to split income, resulting in no tax savings.

The attribution rules in a family trust strategy depend on the structure of the trust, who funds the trust, how it is funded, the type of investment income that is distributed from the trust, as well as who is receiving the distributions. For a refresher on these rules, please ask your RBC advisor for our article on income splitting and the attribution rules.

The attribution rules do not apply where you loan money to a properly structured trust at the CRA's prescribed interest rate in effect at the time the loan was made. The trustee must pay you annual interest on the loan by January 30 of the following year (and by January 30 of every subsequent year that the loan is in place). It is crucial to meet this deadline, because if the interest payment is late by even one day, the attribution rules will apply for that particular year, and all subsequent years until the loan is repaid.

The prescribed interest rate in effect at the time the loan is made will be locked-in for as long as the loan is outstanding, regardless of subsequent changes to CRA's prescribed interest rate. The lower the interest rate at the time the loan is made, the greater the potential tax saving opportunities for you and your family.

The components of the strategy

The following are the main components of the prescribed rate loan to family trust strategy.

Identifying potential non-registered assets

You may want to start by identifying assets you own that generate investment income and are currently exposed to your higher marginal tax rate. These may be assets that have accumulated over time in a taxable non-registered account, funds from a sudden cash windfall such as an inheritance, or proceeds from selling a business. You should also determine the amount you wish to lend to the family trust.

One method of lending these assets is converting these non-registered assets into cash if the assets are not already in cash form. Consider the tax cost of disposing of your investments since the disposition may trigger capital gains or losses. You could review your Notice of Assessment to determine if you have capital losses carried forward that could be used to offset any capital gains realized.

Establishing a family trust

A trust will need to be established. An individual (known as the settlor) creates the trust by transferring property to a trustee of their choice to be held and administered for the benefit of one or more beneficiaries. The settlor generally arranges to have the terms of the trust drafted according to their wishes. The trust agreement indicates the settlor, trustee, beneficiary, the assets being transferred to the trustee, the powers and restrictions placed on the trustee, and how and when income and capital are to be distributed to the beneficiary and to which beneficiary. For more information on establishing a trust, please refer to our article on living/family trusts.

Loaning to the family trust

Once the family trust is established, you can make a demand loan to the family trust. The loan is backed by a promissory note and a loan agreement which sets out the terms of the loan. It's essential that you consult with a qualified legal advisor in drafting these documents.

Ensure that any legal documentation, such as the trust documents and loan agreements, are filed away safely.

Investing trust assets

The trustee can then invest the borrowed money in a portfolio. Generally, a prescribed rate loan strategy will only be effective if the annual income generated from the portfolio is greater than the interest rate on the loan. The lower the prescribed rate, the easier it is to ensure that the family trust earns sufficient income to cover the interest cost and maximize the tax savings.

If you disposed of your securities at a loss before loaning the cash to the family trust, and the trust intends on repurchasing the same securities, you should be aware of the superficial loss rules. The superficial loss rules may deny your immediate use of the loss where the trust repurchases and owns the identical security on the 30th day after the settlement date of the loss transaction. To prevent the superficial loss rules from applying, the trustee can consider waiting 30 days before repurchasing the security or purchase a different security with similar exposure to the markets.

Decisions relating to the investment of the assets in the family trust will depend on the purpose and goals of the trust, as well as the investment powers contained in the trust agreement. In general, a trustee must be guided by the prudent investor standard in selecting the trust's investments, unless the trust agreement grants the trustee broader investment powers, and reasonably assess the risk and return of each investment.

Making annual interest payments

The trustee must pay you the annual interest, as set out in the loan agreement, no later than January 30 of the following year. If the interest payment is not made, the income earned by the trust on the borrowed funds that is allocated out to beneficiaries may be attributed back to you and taxable in your hands. Documentation showing that interest payments are made should be retained for the relevant tax year.

Allocating trust income

In general, investment income earned in the trust from a prescribed rate loan is usually subject to tax in the trust at the top marginal tax rate in the trust's province or territory of residence. However, if the trust is properly structured, the trustee may be able to pay or "make payable" the investment income, to a beneficiary. This way, the income can be taxed in their hands at their marginal tax rate.

Income is considered paid to the beneficiary if the amount is distributed to them or used to pay for expenses that directly benefit them. The trustee of the trust should confirm with a qualified legal advisor whether it's possible to use trust income to pay for the expenses of a beneficiary. Depending on the terms of the trust, some types of expenses that may qualify include private school tuition, lessons, camp and childcare expenses.

Income or capital gains "made payable" to the beneficiary are not paid out to them but are retained in the trust. These funds are legally owed to the beneficiary and is typically supported by a promissory note to substantiate that the beneficiary can enforce payment of these amounts.

Filing annual returns

The trustee needs to ensure that an annual tax return is filed for the trust, if required. They also need to provide the resulting T3 tax slips to the beneficiary for any income that was paid or made payable to them. The beneficiary will use these T3 slips when filing their annual personal income tax return.

In addition, the trustee may need to file an annual T5 information return to report the interest paid to the lender and provide the lender with a T5 slip detailing the interest paid.

Calculating the annual tax savings

Ensure that the strategy remains effective by reviewing your tax savings with a qualified tax advisor every year. The end goal of this prescribed rate loan strategy is to shift investment income earned on non-registered assets to your family members with a lower marginal tax rate to achieve family tax savings. The required interest payment on the loan must be accounted for when determining the investment return. You should also factor in the taxes owing on the interest payments you receive from the trust.

Keep in mind that this strategy should be implemented as part of a long-term financial plan. It's possible that over the lifetime of the loan, as a result of market fluctuations, you may not achieve income splitting and the expected tax savings at certain points in time. However, the longer the loan remains in place, the more potential there is for greater savings.

Ensuring the loan is enforceable

You should ensure that the demand loan remains legally enforceable. Some legal advisors believe that making the annual interest payments on the prescribed rate loan is sufficient action to avoid the loan from becoming unenforceable. Making the interest payment annually is an acknowledgement by the borrower that the loan is still outstanding and enforceable. An alternative is to renew the promissory note on an annual basis or to have the borrower acknowledge in writing that the promissory note is still valid. You should consult with a qualified legal advisor to determine what is required to keep the loan enforceable in your jurisdiction.

Benefits of the strategy

By loaning the money to a family trust, instead of gifting money, you retain access to the capital loaned. Another potential benefit of using a family trust for a prescribed rate loan strategy is the ability to maximize your family's after-tax investment income by lowering your family's overall tax liability.

Income or capital gains allocated to a beneficiary from the trust retain their character. This means that interest, dividends and capital gains that are allocated to the beneficiary from the trust will be taxed as if the beneficiary earned these types of income personally.

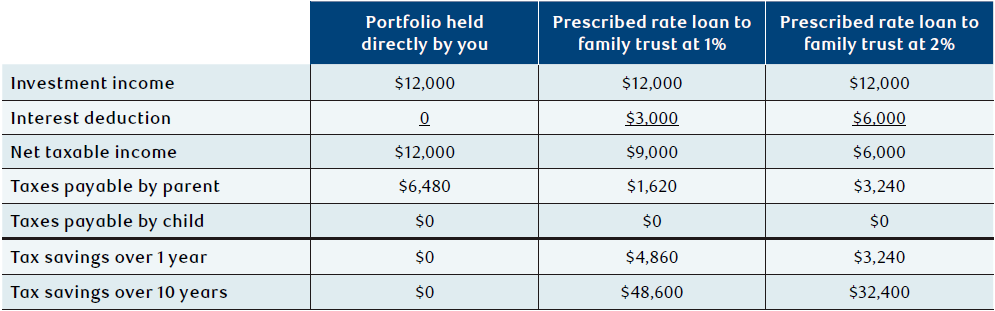

An example

The table below illustrates the potential tax savings you and your family could achieve by making a prescribed rate loan to a family trust for the benefit of your minor child, compared to investing the portfolio directly and paying for your child's expenses with the after-tax returns. Let's assume you have a $300,000 portfolio with an annual rate of return of 4.0% interest. Let's also assume that your marginal tax rate is 54% and that your child has no taxes payable since the total taxable income they receive is less than their basic personal exemption. The interest paid in this scenario is deductible to the trust as the borrowed funds are used to invest in a portfolio with the purpose of earning income.

The tax savings are the result of the investment income being taxed in your lower-income child's hands, as opposed to your own. The family's net tax benefit of having a prescribed rate loan at 1% is $4,860 in one year alone. If this loan remains in place for 10 years with similar returns, the savings become significantly greater. These savings are further compounded if the return on the investment increases.

As shown in the illustration above, it's more beneficial when the CRA prescribed rate is lower. However, even with a higher CRA prescribed rate, there may still an advantage to implementing a prescribed rate loan strategy, where the annual income generated from the portfolio is greater than the interest rate on the loan. The benefit is just not as pronounced.

Considerations of the strategy

Interest deductibility

The interest paid by the trustee on the loan is generally tax-deductible where the proceeds from the loan are used to purchase income producing assets, such as a bond that pays interest or a stock that pays dividends. The income earned on the portfolio can be paid or made payable to beneficiaries without affecting the interest deduction, as long as the original borrowings remain invested in income producing assets.

Where the trustee disposes of all or a portion of the investments, they will need to identify the current use of borrowed money to determine the extent to which interest remains deductible. If in doubt, the trustee should speak with a qualified tax advisor to determine the amount of interest that remains deductible.

Alternative minimum tax (AMT)

AMT is designed to ensure that certain taxpayers, including most trusts, pay at least a minimum amount of tax. Trusts are required to compute their tax liability by calculating their regular tax and AMT. The AMT calculation allows fewer deductions, exemptions, and tax credits than the regular income tax rules. Trusts pay either the regular tax or the AMT, whichever is highest.

Due to recent tax changes, AMT may now be a concern for most prescribed rate loans set up through a family trust. For AMT purposes, the trust can only deduct 50% of its deductible interest expense and carrying charges instead of 100% for regular tax purposes. This means that a family trust that was funded by a prescribed rate loan may now have to pay AMT even if it didn't in the past.

To read more about how AMT may impact your trust, please ask your RBC advisor for the article on this topic.

Due to the potential impact of AMT, the effectiveness of prescribed rate loan trusts may not be as great as it once was, and you should speak with your qualified tax advisor about ways to mitigate the effects of AMT.

Debt forgiveness

In certain circumstances, the funds loaned to a trust may be invested in a portfolio that declines in value. Where there is insufficient capital for the trustee to repay the loan and you decide to forgive the loan, or part of the loan, the debt forgiveness rules may apply.

The debt forgiveness rules are complex, but in general, the amount not repaid will be deemed to be forgiven and first used to reduce certain tax attributes of the trust, if available. The tax attributes that will be reduced include non-capital losses, farm losses, restricted farm losses, allowable business investment losses, and net capital losses carried forward, in that order.

If the trust's losses are insufficient to absorb the forgiven amount, the trustee can then choose to reduce other specified tax attributes, such as the adjusted cost base of certain capital property held by the trust. If there is still a forgiven amount remaining, a portion of the forgiven amount may be taxable in the year the unpaid amount is forgiven.

Upon death

If you, the lender, were to pass away and no specific instructions are given to the executor/liquidator of your estate with respect to the loan, the trustee may need to repay the loan to your estate. If the trustee is unable to repay the loan and the loan is considered forgiven, the debt forgiveness rules may apply. Alternatively, if the loan is forgiven in your Will, the debt forgiveness rules would not apply.

Due to these complexities, be sure to address the loan in your estate plans.

Portfolio make-up

The prescribed rate loan strategy may be tax-effective for your family if you currently invest in a very tax-efficient portfolio (i.e. deferred capital gains, return of capital, etc.). In this case, the taxes payable by you on the loan interest received may exceed any tax savings that result from shifting the investment income to your lower-income family members.

Recordkeeping duties

There are several recordkeeping duties that the trustee must adhere to on an annual basis to ensure that the trust is properly administered and the income splitting benefits of the trust are sustained. These duties include, but are not limited to:

- Signing a resolution before year-end to allocate the trust's income to a beneficiary.

- Documenting payments made to a beneficiary or a third party for the benefit of the beneficiary.

- Keeping receipts for any payments made to a third party or a parent as a reimbursement for an expenditure.

- Maintaining promissory notes for any income that has been made payable to the beneficiary.

- Ensuring the timely and accurate filing of the trust's tax return and providing the T3 tax slips to the beneficiary.

- Ensuring the timely and accurate filing of an annual T5 information return and providing the lender with a T5 slip.

- Documenting and maintaining source documents for the interest payments on the prescribed rate loan and any repayments of principal.

It's recommended that the trustee consult with qualified tax and legal advisors to discuss their recordkeeping responsibilities related to a family trust and the prescribed rate loan.

Costs of implementing the strategy

The cost of implementing a prescribed rate loan may include the legal fees associated with drafting the loan agreement and promissory note. You may also incur legal fees associated with reviewing your documentation to ensure that the loan remains enforceable. The trustee may incur additional accounting fees related to filing the trust's income tax return and other administrative issues such as calculating the required interest payment on the loan. You should take these costs and fees into consideration when determining whether using a family trust for a prescribed rate loan makes sense in your circumstances.

U.S. securities in a family trust

Depending upon how the family trust is structured or funded, the value of the trust assets may be included in the settlor, lender and/or beneficiary's worldwide estate for U.S. estate tax purposes on their death. If the trust is in existence at the time of the settlor, lender and/or beneficiary's death, and the trust owns U.S. securities, the settlor, lender and/or beneficiary may be subject to U.S. estate tax on the value of these U.S. situs assets. Note that Canadian mutual funds or Canadian pooled funds that invest in U.S. securities are not considered to be U.S. situs assets for U.S. estate tax purposes.

If the value of the settlor, lender and/or beneficiary's worldwide estate (including the trust assets) is below the U.S. estate tax exemption in place in the year of their death, U.S. estate tax will not be payable.

If you are the settlor, lender and/or beneficiary of a trust that holds U.S. situs assets, it's important to review the trust agreement as well as how the trust was funded to determine whether you have U.S. estate tax exposure. If you're considering setting up a family trust, you may want to consider seeking advice from a qualified cross-border tax advisor about how to structure the trust to minimize U.S. estate tax exposure.

Conclusion

Although a prescribed rate loan in a family trust can provide significant tax savings, ensure you have considered all costs, prevailing interest rates and market conditions before setting up a family trust. Speak to a qualified tax and legal advisor to determine if this strategy makes sense for you and your family.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax, or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal, and/or insurance advisor before acting on any of the information in this article.