Your financial to-do list

At the beginning of every year, many of us go through an annual ritual of setting resolutions. In addition to improving your physical health, don't forget about your financial health. This article provides a list of 10 financial to-dos that may help you improve your financial well-being.

At the beginning of every year, many of us go through an annual ritual of setting resolutions. In addition to improving your physical health, don't forget about your financial health. This article provides a list of 10 financial to-dos that may help you improve your financial well-being.

Family Office Services

June 14, 2025

Your financial to-do list

At the beginning of every year, many of us go through an annual ritual of setting resolutions. Improving health is often high on many people's lists — lose weight, exercise and eat healthier. In addition to improving your physical health, don't forget about your financial health. This article provides a list of 10 financial to-dos that may help you improve your financial well-being.

Please note that any reference to a spouse in this article also includes a common-law partner.

Your financial to-do list

The following is a list of 10 items (in no particular order) you may want to consider:

1. Review your financial situation and develop a retirement projection.

2. Develop a financial plan.

3. Ensure your asset allocation is up to date.

4. Consider putting family income-splitting structures in place.

5. Ensure you have adequate life and living benefits insurance coverage.

6. Use credit effectively.

7. Review your account structures to ensure they're appropriate.

8. Make sure your Will, beneficiary designations and powers of attorney (POAs) are up to date.

9. Give back with charitable donations.

10. Simplify your financial life.

1. Review your financial situation and develop a retirement projection

In today's world of information overload, it can be refreshing to get information in an easy-to-read and simple format. A personalized financial review can help you to see the big picture by helping you gather your financial information and presenting it to you in a way that's organized and clear.

Speak to your RBC advisor about producing a financial review for you during your next meeting. This will put your financial life on paper, making it simple for you to quickly identify where you stand today. This review can be updated regularly so you can determine how you're progressing from year to year.

Once you've determined your current financial situation, think about your retirement. Will you have enough income and savings so you can retire comfortably? If you're a business owner, how will you use the equity in your business to create retirement income, and will it be enough? As life expectancies generally get longer, maintaining a comfortable standard of living throughout your retirement may become more challenging. Speak to your RBC advisor about preparing a retirement projection so you have a good indication of your overall situation and what changes, if any, need to be made to reach your retirement income goals.

2. Develop a financial plan

A financial plan addresses all aspects of your financial affairs, including cash and debt management, tax and investment planning, risk management, and retirement planning. You can use information gathered from your financial review and retirement projection to develop a financial plan that will help you achieve your financial and retirement goals. If you already have a financial plan, regularly review your plan to determine whether it's necessary to make modifications to ensure you're on track towards meeting your goals.

3. Ensure your asset allocation is up to date

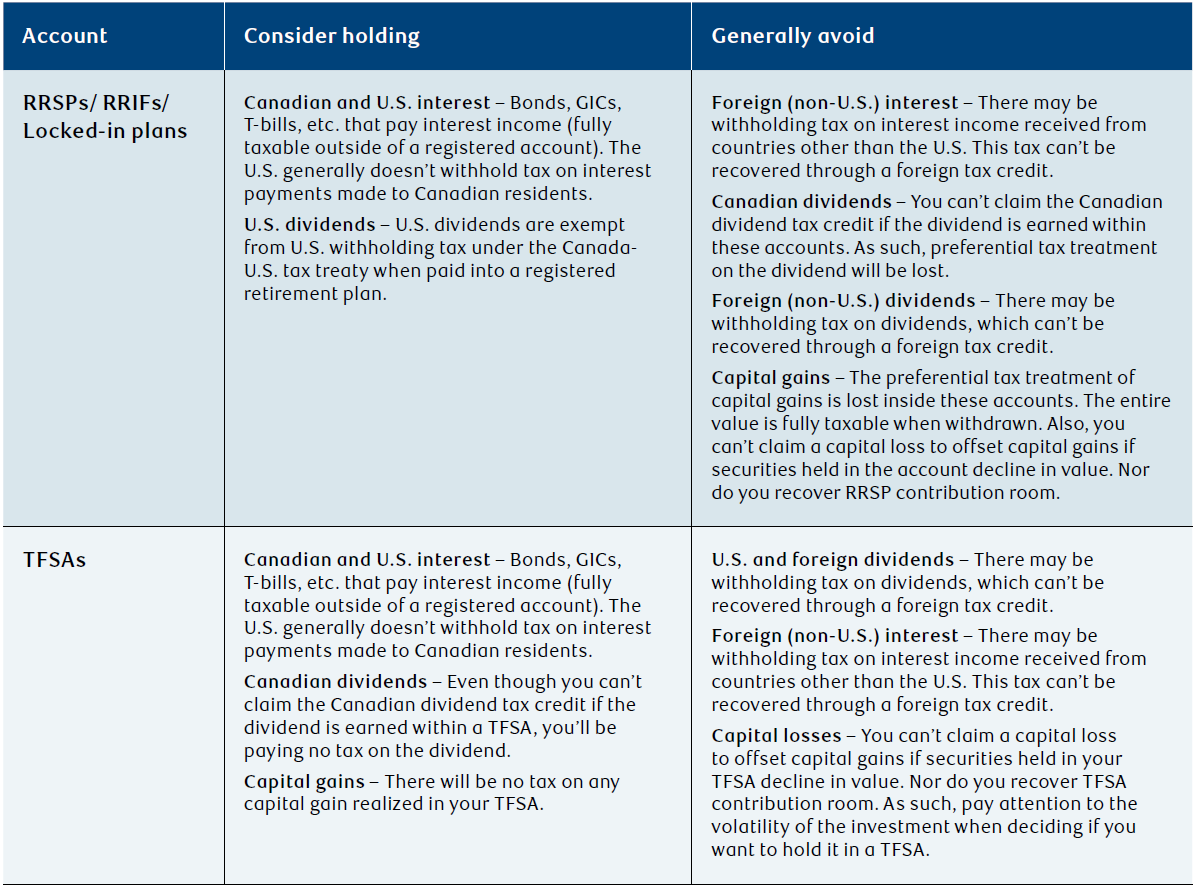

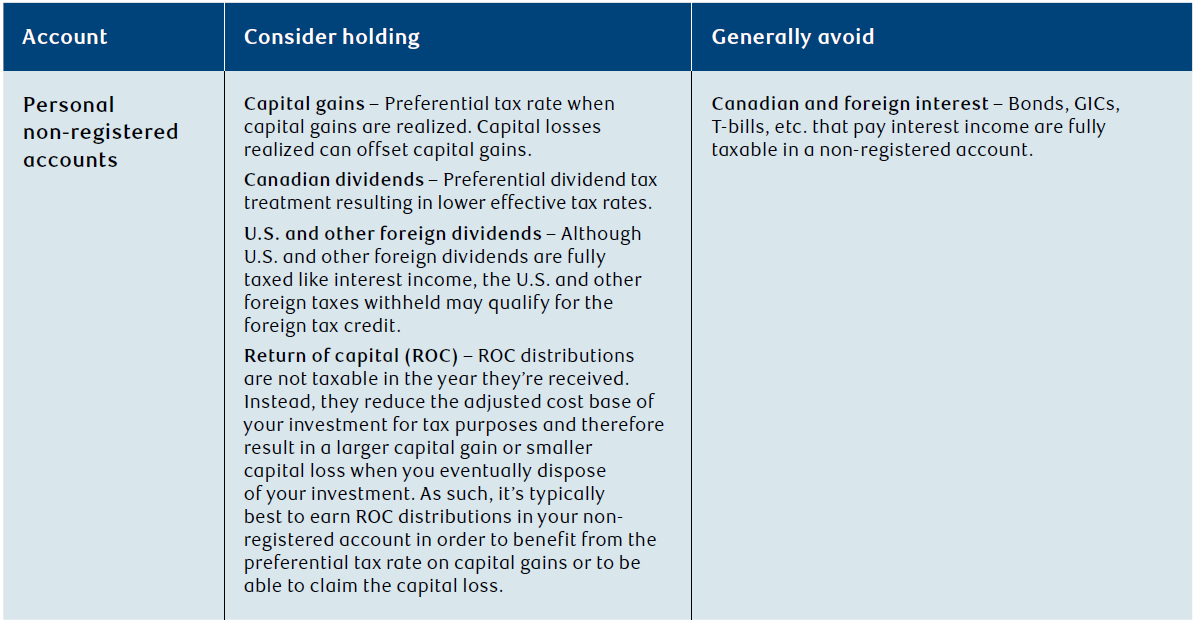

It's important to review the asset allocation of your investments (cash, fixed income and equities), as well as their currency and geographic split (Canada, U.S., international) on a regular basis. Is your asset allocation appropriate based on your risk tolerance, as well as your financial and retirement goals? Have your circumstances or goals changed? Review your asset allocation with your RBC advisor to see if any changes need to be made.

In addition to reviewing your asset allocation, consider the tax efficiency of your investments and their place within your registered and non-registered accounts. To help maximize your after-tax returns, here are some general investment guidelines you may want to incorporate into your overall investment strategy.

4. Consider putting family income-splitting structures in place

Implementing a family income-splitting strategy may help you lower your family's overall tax bill, allowing you to keep more of your investment income.

If you have a spouse or children or grandchildren with little or no income, and financial conditions are favourable, you may want to consider setting up a prescribed rate loan for income splitting. The lower the CRA prescribed interest rate is at the time you set up the prescribed rate loan, the more efficient the strategy will likely be. The prescribed rate loan strategy involves making a formal loan to a family member or family trust at the CRA prescribed rate. Your family members or the family trust can then invest the loaned funds and earn investment income. If this strategy is executed properly, the net income earned can be taxed in your family member's hands at their lower marginal tax rate, thereby allowing you to shift investment income from your hands to lower-income earners.

If a prescribed rate loan doesn't currently make sense for you (for example, the current CRA prescribed rate is too high), there are other strategies you can consider such as:

• Gifting funds to adult children. Although gifting assets with an accrued gain will trigger immediate capital gains tax, future income generated by the funds held by your children will not be attributed back to you.

• Having the higher-income spouse pay the household expenses. This allows a lower-income spouse to save their funds and invest at their lower tax rates.

• Consider setting up tax-free savings accounts (TFSA) for family members who are at least 18 years of age (or at least 19 if you live in a province where the age of majority is 19). You can gift money that would generate income, that may otherwise have been taxable in your hands, to a family member to contribute to their own TFSA. Since all of the investment income in the TFSA grows tax-free, there will be no income attribution, even if you gifted the money that funded the account.

For more income-splitting ideas, ask your RBC advisor for an article on income splitting.

5. Ensure you have adequate life and living benefits insurance coverage

Are you confident that on your passing or if you became ill or incapacitated, you and your family would have adequate assets and income to maintain your standard of living? If the answer is "No" or "I don't know," consider speaking to a licensed insurance representative to determine if your current insurance coverage is adequate or if you require new or additional coverage. Give yourself and your family peace of mind by taking immediate action today to help secure your family's financial future in the event of an unforeseen occurrence.

Life insurance benefits are typically paid when the insured party passes away. The tax-free death benefit received can be used to pay off your debts and expenses or be used to create a legacy. At death, your assets often trigger significant tax obligations, which are frequently met by liquidating the assets of your estate. A life insurance benefit can help cover your tax obligations and leave your estate intact.

It's also important to consider the financial repercussions of recovering from a serious accident or illness, in particular if you require long-term care. You may be left without regular income and your savings may be depleted. Living benefits insurance can provide you with a benefit if you're unable to work, have to pay additional recuperative costs due to your medical condition or are unable to care for yourself.

To ensure that you, your family, and your savings are financially protected against disability or illness, speak to your licensed insurance representative about these types of insurance.

6. Use credit effectively

Are you maximizing opportunities on both sides of your balance sheet? Interest rates fluctuate, so it may be prudent to review your debt obligations regularly and see if you can benefit from a low interest rate environment by refinancing your high-cost debt, including your student loans, your car loan or even your mortgage. For example, if you bought a home while interest rates were higher, you may be able obtain a new mortgage at a lower rate. You'll need to consider whether refinancing is beneficial while factoring any applicable penalties.

If you have different sources of debt, consider paying off the debt with the highest interest rate first, to reduce interest costs. You may also want to consider consolidating your debt, as this may allow you to access a lower interest rate. If you already have a competitive rate on your debt, is the interest on the debt tax-deductible? If not, speak with your RBC advisor to see if there's a way you can restructure your loan and your assets to reduce your interest costs, or make the interest on the loan tax-deductible to save you taxes.

7. Review your account structures to ensure they're appropriate

Prepare a list of all of your bank and investment accounts and determine how the account is owned and whether the ownership structure is appropriate. For example, many people own non-registered assets jointly with their spouse, for convenience or possible probate minimization. However, owning assets jointly may not always be appropriate, such as when assets in the joint account are required to fund a spousal testamentary trust. Also, using joint accounts may be undesirable, as the joint owner may have the ability to potentially deal with the assets without your knowledge. As well, the assets in the account may be exposed to the joint owner's creditors.

You may also want to consider whether your account structures make sense from a tax perspective. For example, if you hold most of your assets in a non-registered investment account, consider whether it may be appropriate to contribute assets from this account to your RRSP and/or TFSA to benefit from tax-deferred/tax-free growth.

8. Make sure your Will, beneficiary designations and POAs are up to date

Did you know that many Canadians don't have a Will and that in some provinces, marriage revokes your Will? If you do have a Will, is it up to date? Does it reflect your wishes given your current situation? Does it include provisions that will allow your executor/liquidator to implement strategies which may help to minimize taxes and disharmony among family members upon your death?

A Will is one way to ensure your property is distributed according to your wishes after your death. Give your family and yourself peace of mind by working with a qualified legal advisor who specializes in Will and estate planning to get a thorough and up-to-date Will.

As part of your Will and estate plan review, determine whether there are alternate methods to distribute your assets on death. This may include naming beneficiaries on registered plans, such as RRSPs/RRIFs, pension plans and life insurance policies. By naming a beneficiary on the plan or policy documentation, you may be able to reduce probate taxes on death, as the proceeds are paid directly to your beneficiary outside of your estate. Consider whether this option is available to you in your province of residence and whether designating beneficiaries on your registered plans and life insurance policies is appropriate.

If you've already named a beneficiary on your registered plan or life insurance policy, is the designation current and does it still reflect your wishes? Have you designated any minor beneficiaries? Be aware that naming a minor as the beneficiary of your registered plans or life insurance policy may cause difficulty in settling the plan or policy proceeds after your death.

Prior to meeting with a qualified legal advisor to review and update your Will and estate plan, it may be helpful to put together a list of your assets, including your registered assets and insurance policies, and any beneficiary designations.

Also, don't underestimate the importance of having a POA, or Mandate in Quebec, for both your financial affairs and health care. These documents are crucial in the event you become mentally incapacitated and require the help of another to manage your affairs.

Consider storing a copy of your Will and POAs in a fireproof safe (where your executor/liquidator and attorney know the combination number or how to access it) or with your legal advisor.

Additionally, whenever you have a change in circumstances or wishes, remember it's always a good idea to revisit your Will, beneficiary designations and POAs.

9. Give back with charitable donations

If you have charitable intentions, give some thought to the size and timing of your gift, as well as the type of gift you're going to make. As an individual, you're entitled to a donation tax credit if you donate to a qualified donee, such as a registered charity. The donation tax credit can reduce your taxes significantly.

As an alternative to cash, you may also be able to donate publicly listed securities in-kind to qualified donees without being subject to tax on any accrued capital gain on the securities. In addition, you may receive a donation tax receipt equal to the fair market value of the securities at the time of the donation, allowing you to claim a donation tax credit. Speak with the organization you're intending to make a gift to prior to the donation to confirm whether they can accept in-kind donations.

10. Simplify your financial life

Keeping your finances simple can help you in saving both time and money. The following are some strategies you can consider.

• Consolidate your finances. Many people, over time, open several accounts at various financial institutions to chase the highest interest rates or to diversify. This could result in additional administration time that arises from having to deal with multiple statements and meetings with different advisors, duplication of fees and possibly different investment strategies that don't suit your circumstances. Consider the benefits of consolidating your accounts with a trusted, qualified advisor. Ensure they can offer you a wide array of solutions at a competitive fee structure, as well as personalized expert advice and planning to meet your financial and life goals.

• Bank online. Banking online allows you to view your financial accounts, transfer funds, add to savings and pay bills conveniently and at your fingertips.

• Pre-authorize your bill payments. Pre-authorizing your bill payments can save you considerable time. It can ensure your bills are paid when due, thereby maintaining and strengthening your credit score and helping you avoid late fees.

• Set up a pre-authorized contribution (PAC) plan. One of the ways to create wealth is to "pay yourself first." Setting up a PAC plan may be a good way to help ensure you make annual contributions for accounts such as RRSPs, TFSAs and RESPs. It's also a great way to control your lifestyle spending and ensure you're setting aside funds for the future.

• Keep your financial documents and a list of relevant contacts in a designated, secure area. This process involves gathering documents such as financial statements, tax slips, financial reviews, retirement projections, insurance policies, Will and POAs and keeping them in a safe place. Doing so will help you stay organized and help ensure your family members can easily access this information if needed.

Conclusion

Although some of the tips and strategies in this article may require you to spend additional time and commit additional resources to managing your affairs, it's important to keep sight of the benefits. By getting your financial life in order, you give yourself the opportunity to help maximize your returns and preserve your wealth. Consider going through this list, noting the items that are applicable to your circumstances, and speaking with a qualified tax/legal advisor about any strategies you want to implement.

This article may contain strategies, not all of which will apply to your particular financial circumstances. The information in this article is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been properly considered and that action is taken based on the latest information available, you should obtain professional advice from a qualified tax, legal and/or insurance advisor before acting on any of the information in this article.