Ari Black, CFA

Investment Advisor

June 16, 2026

Congratulations to the Hurricanes, Knicks - and Anyone Who Bet on Them

Source: NBA.com

It was more fun when the Knicks were a dysfunctional franchise, helping clear a path for my Raptors (now the Leafs are on their own). At the start of the season, betting markets gave Carolina and New York each about a 10% chance of winning it all. Predicting champions - or individual stocks - is hard, which is part of the fun. Long-term investors can instead be the house: the S&P 500 has historically been positive in roughly 94% of rolling 10-year periods.

A few things that caught my attention this month – markets, behaviour, and a couple that say more about where things are heading than where they’ve been.

This Month:

- Tax-Loss Harvesting on Steroids?

- Index Funds Have a SpaceX problem

- What SpaceX’s $2 Trillion Valuation Says About This Market

- Why Your Vet Might Be Pushing More Tests

- The Demographic Shift That Could Change Everything

1. Tax-Loss Harvesting on Steroids?

A new category of tax-aware long/short funds is starting to arrive in Canada, and the pitch sounds almost too good: create tax losses while keeping your market exposure.

That distinction matters. The goal is not simply to “stay invested.” It is to maintain similar beta exposure - exposure to the same broad market or sector risk - while using long and short positions in related securities to create more opportunities for tax-loss harvesting.

In plain English: the strategy tries to keep the portfolio economically exposed to the market, while realizing losses along the way that may be useful against capital gains elsewhere.

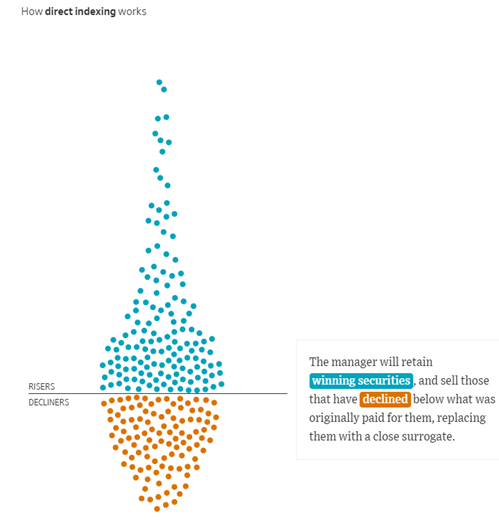

This is similar in spirit to tax-loss harvesting with individual stocks or direct indexing, but potentially more powerful. A manager can own one security while shorting a similar one, allowing losses to be realized on one side of the trade even when the overall market or sector exposure remains largely intact.

It’s worth separating the marketing pitch from the math.

A realized loss today often means a larger embedded gain later. That doesn’t make the strategy bad - it just means the benefit isn’t a free lunch. The real value comes from timing, compounding, flexibility, and the ability to use losses when they’re most valuable.

Over a full investment horizon, the tax component may be worth roughly 60–70 basis points annually over 15 years, depending on market conditions, tax rates, implementation, and the investor’s ability to use the losses. Any excess return (or underperformance) from the underlying investment strategy would be separate from the tax benefit - and this is where it’s important to select the right manager and structure.

My takeaway: this is a genuinely interesting category, particularly for taxable investors with large realized or unrealized gains, a long time horizon, and the discipline to actually use the losses generated. It’s worth looking at the full life cycle - including the eventual capital gain - rather than just the annual tax-savings chart. But for the right investor, even accounting for that deferred gain, the combination of flexibility and compounding can make this a meaningful addition to a taxable portfolio.

Further Reading

This Wall Street Journal article is also a really good tutorial of how direct investing and tax-aware long/short investing works.

Source: WSJ.com

2. Index Funds Have a SpaceX Problem

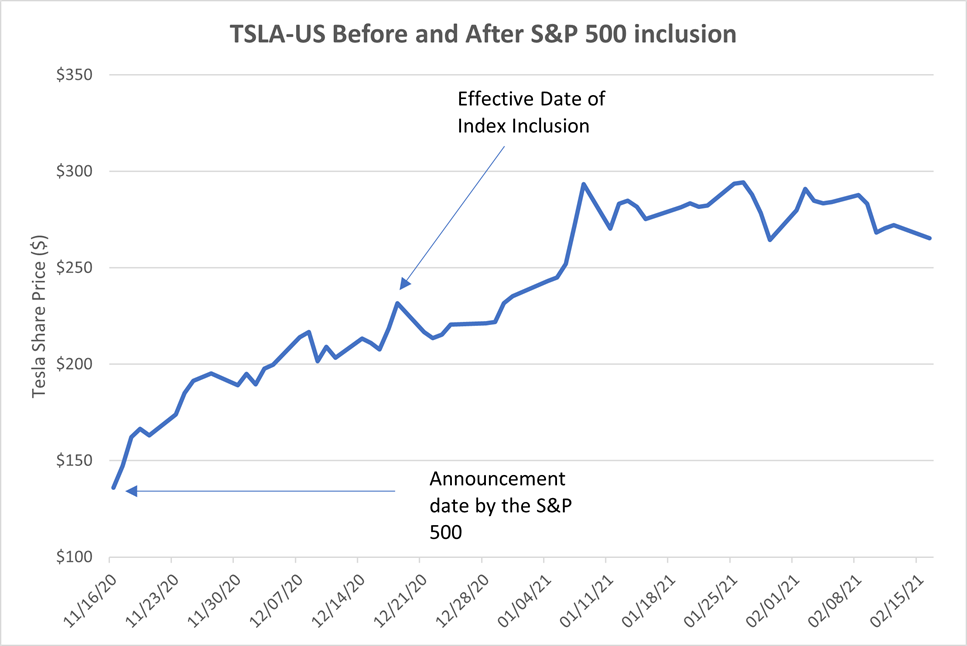

The chart below shows Tesla’s performance between its S&P 500 inclusion announcement and its eventual addition to the index.

If a company like SpaceX eventually goes public at a valuation measured in trillions, index providers, active managers, and passive funds will all face the same question: when should it be added to major benchmarks.

I explore the debate in more detail here:

Source: Factset

3. What SpaceX’s $2 Trillion Valuation Says About This Market

The short version: SpaceX’s reported $2 trillion valuation is not only a story about one exceptional company. It also shows how much of the distant future investors are willing to pay for today - and why the reopening IPO market deserves attention.

SpaceX may be one of the few companies where a credible argument can be made that a valuation of roughly $2 trillion is only the starting point.

As discussed recently on the All-In Podcast, the bullish case is not based on launch revenue alone. It rests on a vertically integrated platform spanning reusable rockets, Starlink’s global communications network, defence applications, potential computing infrastructure and perhaps an entirely new space economy. Lower launch costs support a larger satellite network, Starlink generates recurring revenue, and that cash flow can fund further technological development. SpaceX’s exceptional record of execution makes that vision easier to believe.

But the valuation also says something about the market in which it is emerging.

To justify a number like this, investors must assume SpaceX preserves its technological advantage, successfully commercializes capital-intensive projects and earns attractive returns despite competition, regulation and technological change. That may prove correct. But markets are most willing to underwrite outcomes a decade or more away when confidence is high, capital is plentiful and perceived risk is low.

That is why the reopening IPO market deserves attention.

IPOs identify the stage of the cycle

One major IPO does not reliably mark a market top. The stronger signal appears when many companies recognize that public investors are offering attractive valuations and begin issuing equity at the same time.

Academic research has found that IPO waves tend to follow strong market returns and elevated valuations and have historically been associated with weaker subsequent returns. Broader research on corporate financing finds a similar pattern: when companies issue unusually large amounts of equity relative to debt, future market returns have generally been lower.

History offers two recent illustrations. The 1999 IPO boom, nearly 400 listings in a single year, arrived just as the dot-com bubble was peaking and was followed by a brutal multi-year drawdown for many of those companies. The 2021 wave of IPOs and SPAC listings, with more than 250 deals, came near the top of a different cycle; a large share of those companies traded well below their offer prices within a year or two. In both cases, the surge in issuance wasn’t the cause of the downturn, but it coincided with the point of maximum optimism - exactly when investors were most willing to pay up for future growth.

This is not because executives can consistently time the market. Companies simply tend to sell more shares when public markets are offering especially favourable terms.

The underwriting itself is also part of the signal. Hot IPO markets show that investors are increasingly willing to extrapolate rapid growth, assume today’s leaders will retain their advantages and look beyond near-term losses or heavy capital requirements. That does not make every highly valued IPO irrational, but it leaves less room for disappointment.

Why this cycle may have more room to run

There are reasons to believe the current wave has not yet reached an extreme.

Goldman Sachs expects roughly 100 US IPOs in 2026 - close to the historical average, compared with more than 250 in 2021 and nearly 400 in 1999. Even if IPO proceeds reach a dollar record, total corporate equity issuance is forecast at only about 1% of the US equity market, below its long-term average.

Goldman also projects approximately $1.3 trillion in corporate buybacks this year, enough to outweigh new issuance and the potential supply from expiring lockups. Limited initial floats, faster index inclusion and strong demand for scarce technology exposure could therefore allow major IPOs to extend the rally rather than end it.

The harder test may come later.

Large IPOs with small initial floats have historically seen their publicly tradable share count rise from roughly 7% at launch to 28% after six months and 46% after one year. Goldman estimates that recent and upcoming IPOs could make roughly $500 billion of additional shares eligible for sale in 2026, with more potentially becoming available in 2027.

That does not mean all those shares will be sold. But as founders, employees and early investors gain liquidity, the market may eventually have to absorb substantially more supply.

The likely sequence may therefore be: enthusiasm and scarcity first, followed by broader issuance, insider liquidity and a tougher valuation test.

Back to SpaceX

A potential SpaceX IPO at a valuation approaching $2 trillion would be one of the clearest examples yet of investors underwriting an extraordinary future far in advance.

That future may be realized. A limited initial float and strong demand from active, passive and retail investors could even help extend the current cycle.

But IPOs are more useful for identifying the stage of a market cycle than the exact date of its peak. A growing wave of ambitious companies coming public at demanding valuations may be telling us that investors have entered the part of the cycle when they are most willing to believe in the distant future - and pay for it in advance.

4. Why Your Vet Might Be Pushing More Tests

If you have a dog or a cat, it is natural to trust your veterinarian’s advice on preventative medication, diagnostic tests and other services. Most vets undoubtedly have their patients’ best interests at heart, but the incentives within the industry may still deserve closer scrutiny, particularly as vet service prices have risen sharply over the past decade.

This is an interesting look at how vertical integration and industry consolidation may be affecting the cost and delivery of veterinary care.

Source: My dog!

5. The Demographic Shift That Could Change Everything

Fascinating blog post on why global birth rates are falling – and why the social consequences may be bigger than most people realize. The most interesting part isn’t that birth rates are falling – it’s that the decline appears persistent across countries with very different cultures, policies and income levels.

There are investing implications too: slower labour-force growth, pressure on pension systems, more demand for automation/AI, and bigger questions around immigration and housing.

Source: John Burn-Murdoch

If you have any issues opening these articles reach out to me.

Closing Thoughts

The common thread this month is that structure matters. Whether it’s taxes, index construction, demographics, or IPOs, investors often spend too much time predicting outcomes and too little time understanding the incentives and systems behind them.

Ari Black, CFA, HBA | Investment Advisor

RBC Dominion Securities Inc.

| T: 416-756-8886 | 2 St. Clair Ave West, Suite 1900, Toronto, ON M4V 1L5 | Personal Website | LinkedIn

If you ever want an objective second opinion, not a sales pitch, I’m always happy to help where appropriate.