Ari Black

March 12, 2026

Hockey winding down. Baseball around the corner. Go Team Canada!

A few observations from markets, behaviour and everyday life that stood out this month.

This Month:

- Everyone Suddenly Has an Oil Forecast

- Private Credit: The Conversation Is Getting Louder

- Will AI Eat Software Companies?

- Detecting Bullsh*t

- The Day the Market Loses Sleep

1. Everyone Suddenly Has an Oil Forecast

Oil gets a lot of attention because it touches almost everything — inflation, interest rates, elections, and consumer spending. For countries like Canada and the United States, the story is even more complicated since both are major energy exporters.

But the reality is that oil prices are notoriously difficult to predict.

Over the past week I’ve found myself reading far too much about the situation in Iran. Social media is full of threads explaining exactly what will happen next. Some are thoughtful. Many are not. And a few clearly have an agenda. The challenge is that the range of outcomes in oil markets is enormous.

A look at history makes that clear. Over the past fifty years there have only been a handful of times when oil prices rose more than 30% in just three months. Almost every one of those spikes was tied to a major geopolitical event. Very few were caused by normal economic forces.

Source: Factset

What’s interesting is not just how rare these spikes are, but how differently they play out. Some reverse in a matter of months. Others last for years. Even the futures market, often the best forecast of forward-looking oil prices, frequently overshoots during shocks. When prices spike, future curves tend to imply high prices will persist. In reality, prices often normalize much sooner.

That’s exactly why forecasting oil prices is so difficult. In real time it’s nearly impossible to know whether a spike represents a temporary disruption or the beginning of a broader cycle.

Fortunately, most investors already have some exposure to energy whether they realize it or not. Energy companies represent roughly 17% of the TSX Composite and about 4% of the S&P 500, meaning diversified portfolios already tend to own a slice of the sector.

The broader lesson here isn’t really about oil. It’s about balance and capital allocation. The biggest mistakes investors tend to make happen when they start chasing whatever theme is dominating the headlines. As a rule of thumb, I tend to assume the market is right most of the time. Trying to outsmart it constantly rarely works.

What tends to work better is something much less exciting: staying diversified, thinking long term, and avoiding big portfolio decisions based on the latest geopolitical forecast. The goal isn’t to predict oil prices. It’s to build a portfolio that doesn’t depend on getting that prediction right.

Because if history teaches anything, it’s that the biggest moves in oil are usually the ones nobody saw coming.

2. Private Credit: The Conversation Is Getting Louder

(Private credit is when investment funds lend money directly to companies instead of banks, which historically handled most corporate lending. These loans are private and don’t trade in public markets like regular bonds.)

Back in December I wrote about risks building in private credit and high-yield markets. The concern wasn’t that the asset class would suddenly collapse. The issue was entry point, as spreads (or the return over government bonds) had become unusually tight after years of enormous capital inflows.

Since then, the conversation has become noticeably louder.

Recently, large banks such as JPMorgan Chase have reportedly tightened lending to some private credit funds, highlighting concerns around leverage and underwriting standards.

Public markets may already be sending a signal. Shares of alternative asset managers including Blue Owl Capital, KKR, Blackstone and Brookfield Asset Management have declined meaningfully in recent months, reflecting concerns about future fundraising and asset growth.

Some private credit vehicles have also limited investor withdrawals as redemption requests increased.

Because private assets are not marked to market daily, valuations can move more slowly than public markets. At times like this, public markets may offer more attractive entry points.

Which brings me back to the same conclusion I had in December: liquidity matters.

Credit cycles tend to reward investors who still have capital available when opportunities appear.

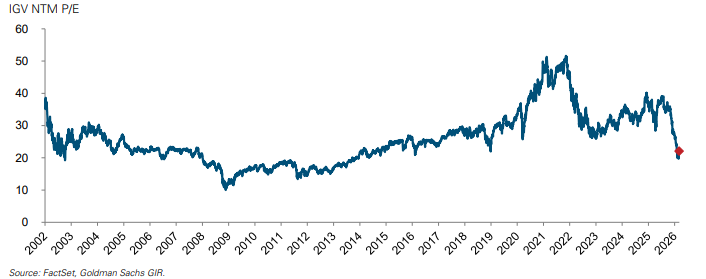

3. Will AI Eat Software Companies?

Software represents roughly 6% of the TSX and about 9% of the S&P 500, and the group is down roughly 20% year-to-date.

It’s far too early to know who the ultimate winners and losers from AI will be. For now, markets appear to be taking a simple approach: sell first and sort it out later, particularly given the above-average multiples many companies in the sector commanded coming into the year.

A recent report from Goldman Sachs offers a useful framework for thinking about this risk. The firm highlights the possibility that AI tools could increasingly perform tasks that users currently do inside traditional applications. Instead of opening multiple programs, a user can simply ask an AI assistant to gather information, run analysis, and complete tasks across several systems. There may still be a need for traditional software programs, but their role could become much smaller.

Goldman suggests companies with the following characteristics may prove more durable:

· System of record — where companies have stored important information for years and moving it somewhere else would be a major headache.

· Core workflow — software people rely on every day to actually do their jobs.

· Proprietary operational data — valuable information that builds up inside the system over time from actually using the software.

The idea is that AI may change how people interact with software, but the platforms that store the data and run the underlying processes may remain central even if the interface shifts.

The space is evolving quickly, so it’s worth being mindful of portfolio exposure as the competitive landscape develops.

4. How to Detect Bullsh*t

(For anyone who hasn’t seen the clip from How to Lose a Guy in 10 days link)

Carl Sagan’s “baloney detection kit” may be 30 years old, but it feels even more relevant now. In a world flooded with social media takes, headlines, clips, and confident opinions, the ability to slow down and think critically matters more than ever. Big Think’s recent piece revisits Sagan’s ideas from The Demon-Haunted World and shows how timeless they still are.

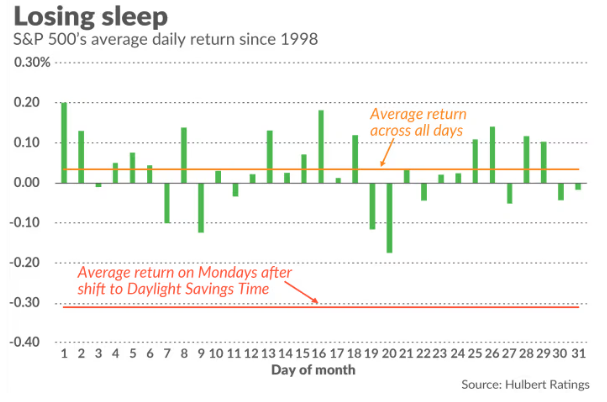

5. The Day the Market Loses Sleep

It’s amazing how passionate people get about daylight saving time.

It’s blamed for everything from sleep disruption to stock market volatility. Interestingly, the Monday after the spring time change has historically been one of the weaker days for markets. That doesn’t necessarily mean daylight savings time causes it, but it’s a fun piece of market trivia. One analysis shows the S&P 500 has averaged about a -0.30% return that day since 1998, compared with roughly +0.03% on a typical day.

One possible explanation is that the one-hour shift disrupts our circadian rhythms, leaving millions of slightly sleep-deprived people - including investors - making decisions at the same time.

On a related note, my seven-year-old son asked me a great question that I suspect many adults can’t answer (and I failed): What does “a.m.” actually stand for?

(Answer: ante meridiem — Latin for “before midday.”)

At this point my personal solution might just be to move to the equator.

Closing Thoughts

Markets right now continue to reward quality, liquidity, disciplined duration, and thoughtful tax planning. They’re far less forgiving of stretched yield, illiquidity, or narratives that rely more on optimism than fundamentals.

Ari Black, CFA, HBA | Investment Advisor

RBC Dominion Securities Inc.

| T: 416-756-8886 | 2 St. Clair Ave West, Suite 1900, Toronto, ON M4V 1L5 | Personal Website | LinkedIn

If you ever want an objective second opinion, not a sales pitch, I’m always happy to help where appropriate