Ari Black, CFA

Investment Advisor

May 18, 2026

A Lesson in Economics? Or Something Else…

We were at Disney this month and my son decided to start trading pins.It turned into a surprisingly good lesson in supply and demand, negotiation, behavioural finance and even regret. What I didn’t expect was discovering dozens of vendors like the one in the picture, each carrying hundreds of pins on a Tuesday morning (along with meeting some very interesting characters who weren’t dressed in costume). I’ll come back to that in the final section.

A few things that caught my attention this month – markets, behaviour, and a couple that say more about where things are heading than where they’ve been.

This Month:

- Are You Inheriting Someone Else’s Tax Bill?

- Covered Call ETFs: Why They’ve Exploded in Popularity

- Anything About Costco Usually Gets My Attention… And 30% of Americans

- Like We Needed More Reasons to Drink Coffee

- Hi, My Name is Ari and I’m a Disneyaholic

1. Are You Inheriting Someone Else’s Tax Bill?

I recently came across another example of a fund event that triggered a large capital gains distribution for investors.

That is the strange part: you can receive a taxable capital gains distribution even if you personally never sold anything, and even if you have not made much money in the fund yourself.

This happens more often than investors realize. A fund may have appreciated securities sitting inside it. If the fund later sells those holdings because of rebalancing, redemptions, strategy changes, a merger or even a fund closure, those gains can be distributed to the investors who remain.

Illustrative example for educational purposes

I recently looked through the financial statements for a sample of some of the largest ETFs and mutual funds in Canada. The unrealized gains sitting inside the funds ranged from roughly 15% to almost 40% of net asset value. That does not mean an immediate tax bill is coming, but it does mean many pooled vehicles carry meaningful deferred gains.

This is one reason direct ownership of individual securities can be attractive for larger taxable portfolios. Even if you are largely replicating an index, you control your own cost base. You decide when to realize gains, harvest losses and avoid inheriting a fund’s tax history.

Tax-loss selling is probably the first reason to consider direct indexing or direct ownership. This may be the second.

To be clear, this is not an argument against ETFs. Large, liquid, low-turnover ETFs can be incredibly effective structures. But not all pooled vehicles are equal.

For taxable investors, the question is not just: “What is the fee?” or “What is the yield?”

It is also: “How much embedded gain am I buying into?” and “How likely is the fund to realize it?”

Structure matters more than most investors realize.

2. Covered Call ETFs: Why They’ve Exploded in Popularity

Covered call ETFs have become one of the fastest-growing categories in Canadian investing.

And honestly, it’s not hard to understand why.

Many now advertise:

•10%+ yields,

•monthly cash flow,

•lower perceived volatility,

•and “enhanced income” from blue-chip equities.

To many investors, it can feel like getting equity returns with bond-like income.

The problem is: yield is not return. In many cases, these strategies are simply converting part of a portfolio’s future upside into current cash flow. That tradeoff can absolutely make sense in the right environment — but investors should understand what they’re giving up.

Only a few years ago, Canada had roughly 50 covered call ETFs with less than $10 billion in assets. Today, there are well over 200, with nearly $10 billion of inflows in 2025 alone. That’s an enormous amount of capital moving into one strategy in a very short period of time — and whenever investors aggressively crowd into the same category, it’s usually worth slowing down and asking a few more questions.

For anyone who wants a plain-English explanation of how covered calls work, this is a helpful overview of the terminology.

Psychologically, these products are easy to like because:

•investors receive regular monthly cash flow,

•volatility may appear lower,

•and the distributions can resemble stable “income.”

But economically, part of what’s happening underneath the surface is:

•future upside is being sold away,

•some distributions may include return of capital,

•and investors may effectively be receiving back part of their own money over time.

If a fund consistently distributes more than it earns, the net asset value eventually reflects it.

That doesn’t automatically make covered call ETFs “bad.” It simply means investors should focus on total return, not just yield.

Over long periods, many covered call strategies have historically lagged the underlying equity indexes.

That shouldn’t be surprising. Investors still fully participate in market declines while often sacrificing a meaningful portion of the upside during strong recoveries. This can become a meaningful drag over time.

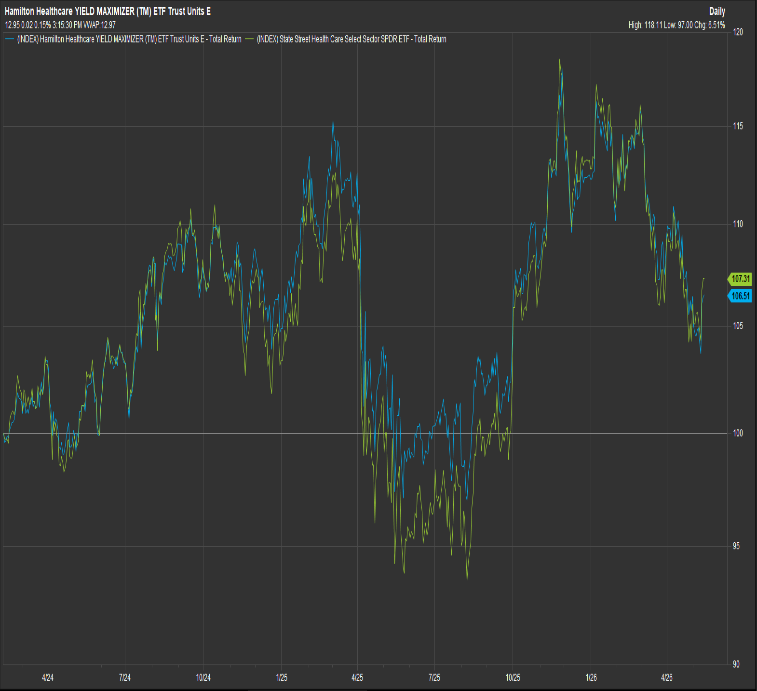

A recent comparison I looked at between two healthcare covered call ETFs and the underlying healthcare index was particularly interesting.

Despite:

•a relatively choppy market,

•elevated volatility,

•and conditions that should theoretically favour covered calls,

Source: Factset. The healthcare sector is shown in green, represented by the XLV ETF.

…the long-term total returns (including dividend reinvestment) ended up relatively similar - and in some cases slightly worse for the covered call strategy once fees and trading costs were considered.

The covered call investor did receive:

•significantly more cash flow along the way,

•potentially smoother returns,

•and in some cases tax deferral through return of capital.

But those benefits were largely offset by giving up upside participation and paying higher costs.

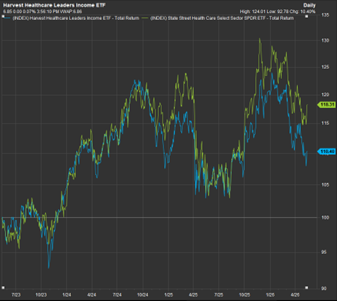

The contrast becomes even more obvious in stronger bull markets. One of the oldest Canadian covered call bank ETFs significantly lagged a plain vanilla bank ETF over time despite producing much higher distributions along the way.

Source: Factset. The covered call ETF is in blue (ZWB), while the plain vanilla ETF is in green (ZEB).

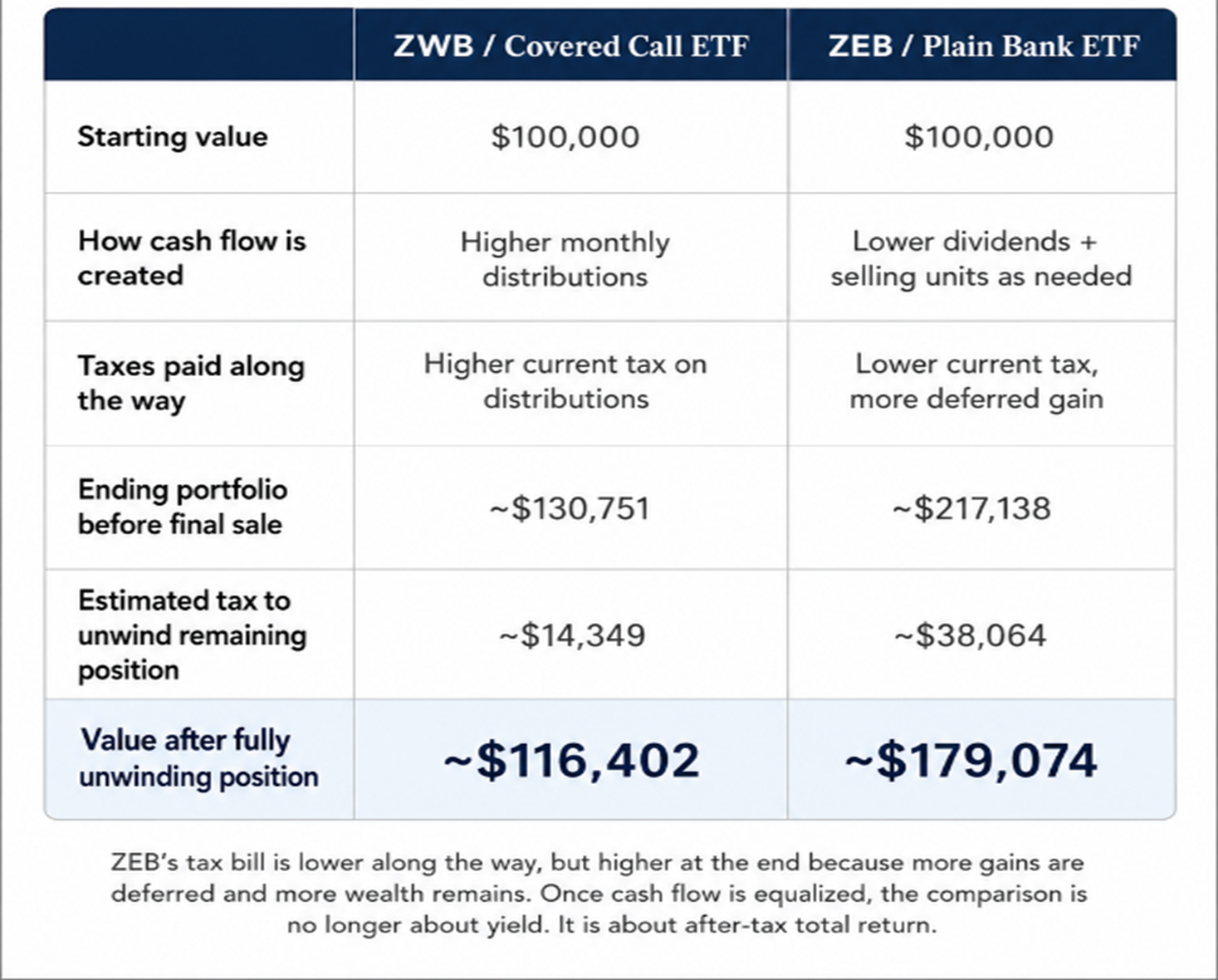

The key question isn’t how much income a strategy distributes.It’s how much after-tax wealth you’re left with at the end. To illustrate the difference, below is a simple comparison between taking a monthly distribution versus generating your own cash flow by selectively selling units over time.

Source: Illustrative example based on data from Factset

Better income today can sometimes come at the expense of lower long-term growth tomorrow.

My view

Covered call ETFs can absolutely play a role in portfolios. If you believe markets will remain range bound and want a potentially more tax-efficient way to generate cash flow, they can make sense in the right situation.

But investors should understand what they are actually trading away.

Personally, if someone wants a more conservative portfolio, I’d rather explicitly build downside protection through:

•diversification,

•structured solutions,

•long/short strategies,

•or proper asset allocation,

instead of simply sacrificing future upside while remaining heavily exposed to equity market drawdowns.

If something promises: equity exposure, bond-like stability, and a 12% yield…it’s worth asking where the risk is actually being transferred.

3. Anything About Costco Usually Gets My Attention… And 30% of Americans

There are so many articles about Costco, including this one which I liked because it also has some really good-looking recipes (Chocolate Babka Knots recipe is saved!).

I was shocked to learn that roughly 30% of Americans are Costco members. The article also makes an interesting comparison between Costco and casinos through the idea of “variable reward frequency” – you never know what treasure you’ll find walking the aisles, which is the appeal.

Source: Tastecooking.com

4. Like We Needed More Reasons to Drink Coffee

This Wired article suggesting coffee may actually be good for you won’t change my intake whatsoever, but it does give me a more scientific-sounding excuse. Apparently coffee may influence the gut, inflammation, mood and even stress response – which is exactly the kind of science I am happy to accept before my fourth cup.

Source: www.wired.com

5. Hi, My Name is Ari and I’m a Disneyaholic

I’m embarrassed to admit how many times I’ve been to Disney (although I can at least claim it doubled as stock due diligence).

But apparently, I don’t even come close to many travellers. This article shocked me after my latest rant about how busy and expensive Disney has become.

It highlights a Disney employee who spends almost all of her money at the parks - including on pins - and surveys suggesting that 25-45% of Disney visitors go into debt for a trip.

I started by teaching my son how to trade Disney pins. Apparently, the next lesson should be position sizing and budgeting.

Source: The New Yorker

If you have any issues opening these articles reach out to me.

Closing Thoughts

Markets right now continue to reward quality, liquidity, disciplined duration, and thoughtful tax planning. They’re far less forgiving of stretched yield, illiquidity, or narratives that rely more on optimism than fundamentals.

Ari Black, CFA, HBA | Investment Advisor

RBC Dominion Securities Inc.

| T: 416-756-8886 | 2 St. Clair Ave West, Suite 1900, Toronto, ON M4V 1L5 | Personal Website | LinkedIn

If you ever want an objective second opinion, not a sales pitch, I’m always happy to help where appropriate.