Ari Black, CFA

Investment Advisor

June 28, 2026

Most physicians have accountants but are often missing:

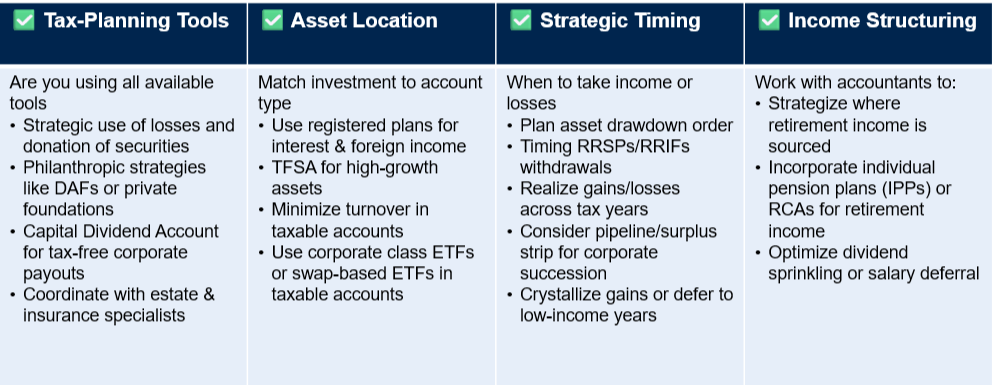

- Asset location and tax efficiency: structuring investments across corporate and personal accounts to improve after tax outcomes

- Corporate investment strategy: Managing how investments are made inside the corporation to minimize unnecessary tax drag including the impact of passive income rules

- Cash flow and extraction planning: Determining when and how to move capital from the corporation – balancing tax deferral today with future flexibility

- Income management inside the corporation: reducing unintended passive income exposure and preserving small business deduction eligibility where possible

- Insurance as a planning tool: Using corporate-owned insurance strategically, including tax-efficient capital extraction and estate planning considerations

- Liquidity and borrowing decisions: Evaluation when it makes sense to draw from the corporation versus borrowing personally to meet cash flow needs

- Coordination with your accountant: Ensuring alignment on key items such as RDTOH, CDA balances and book value tracking – so decisions are made proactively, not at year end.

Specialized planning tools for specific situations:

- Pension Planning/IPPs: For certain physicians these can build tax-efficient retirement income greater than an RRSP

- Insurance (including IFAs): Tax-free extraction from the corporation

- Estate planning: Specialized planners ensuring there is a clear plan and coordination with your legal and tax advisors