Abbas Fazal, CIM

Senior Portfolio Manager & Investment Advisor

April 22, 2026

Increasing Retirement Income with an IPP

By providing the maximum benefits permitted under the Income Tax Act, an IPP generally allows higher tax-deductible contribution amounts than those permitted under an RRSP. For individuals who wish to maintain their pre-retirement lifestyle when retired, IPPs are an effective way to accumulate tax-sheltered funds.

Who can Open an IPP?

IPPs are designed for incorporated business owners and incorporated professionals.

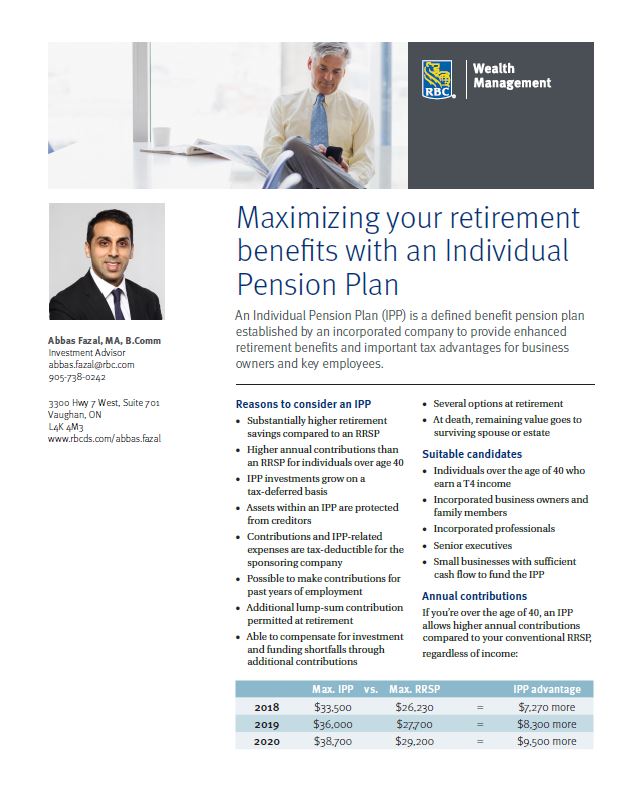

Reasons to Consider an IPP

- Substantially higher retirement savings compared to an RRSP

- Higher annual contributions than an RRSP for individuals over age 40

- IPP investments grow on a tax-deferred basis

- Assets within an IPP are protected from creditors

- Contributions and IPP related expenses are tax-deductible for the sponsoring company

- Possible to make contributions for past years of employment

- Additional lump-sum contribution permitted at retirement

- Able to compensate for investment and funding shortfalls through additional contributions

- Several options at retirement

- At death, remaining value goes to surviving spouse or estate

Suitable Candidates

- Individuals over the age of 40 who earn a T4 income

- Incorporated business owners and family members

- Incorporated professionals

- Senior executives

- Small businesses with sufficient cash flow to fund the IPP

IPP

See attached article for more information on Individual Pension Plans.